- Media & Entertainment

- Synthetic Media Market

Synthetic Media Market Size, Share, and Growth Forecast, 2026 - 2033

Synthetic Media Market by Media Type (Text‑Based Synthetic Media, Video‑Based Synthetic Media, Others), Enterprise (Large Enterprises, Tech‑Enabled SMBs, Others), Application, Delivery Model, and Regional Analysis for 2026 - 2033

Synthetic Media Market Size and Trends Analysis

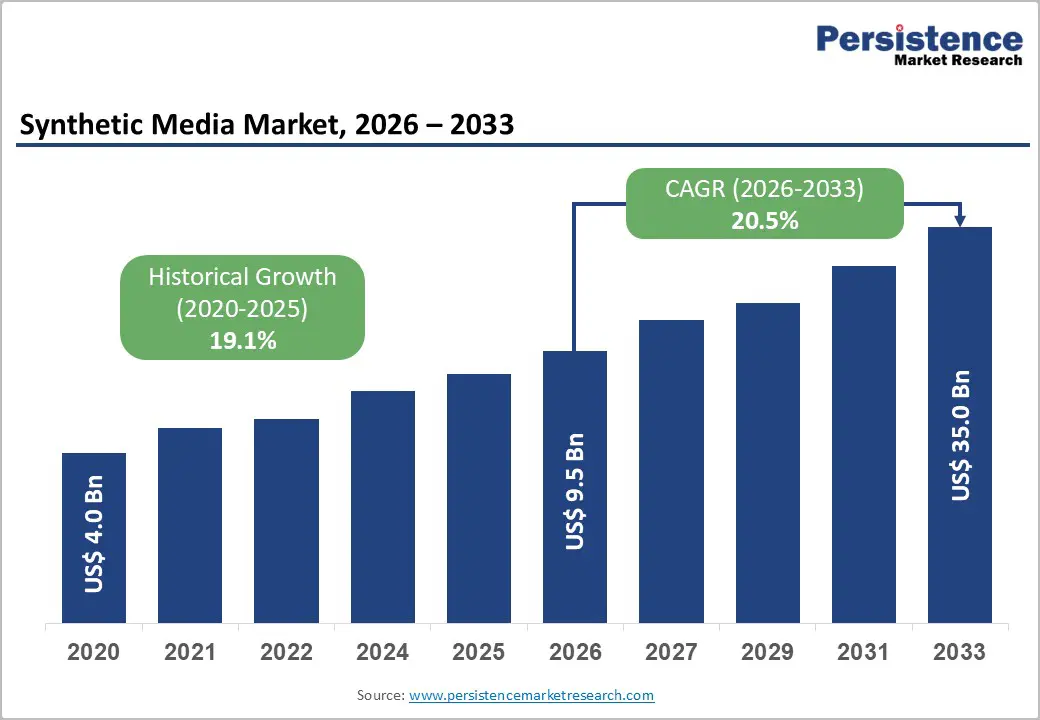

The global synthetic media market size is likely to be valued at US$9.5 billion in 2026 and is expected to reach US$35.0 billion by 2033, growing at a CAGR of 20.5% between 2026 and 2033, driven by rising enterprise demand for automated content production, multilingual digital communication, AI-powered personalization, and avatar-led engagement across marketing, training, customer service, and entertainment applications.

Regulatory focus on transparency, watermarking, and provenance verification is influencing enterprise and public-sector adoption. Meanwhile, synthetic media technologies are evolving into enterprise-grade production tools, enabling organizations to generate AI-based text, video, voice, and virtual characters to reduce costs, accelerate content delivery, and improve localization efficiency.

Key Industry Highlights:

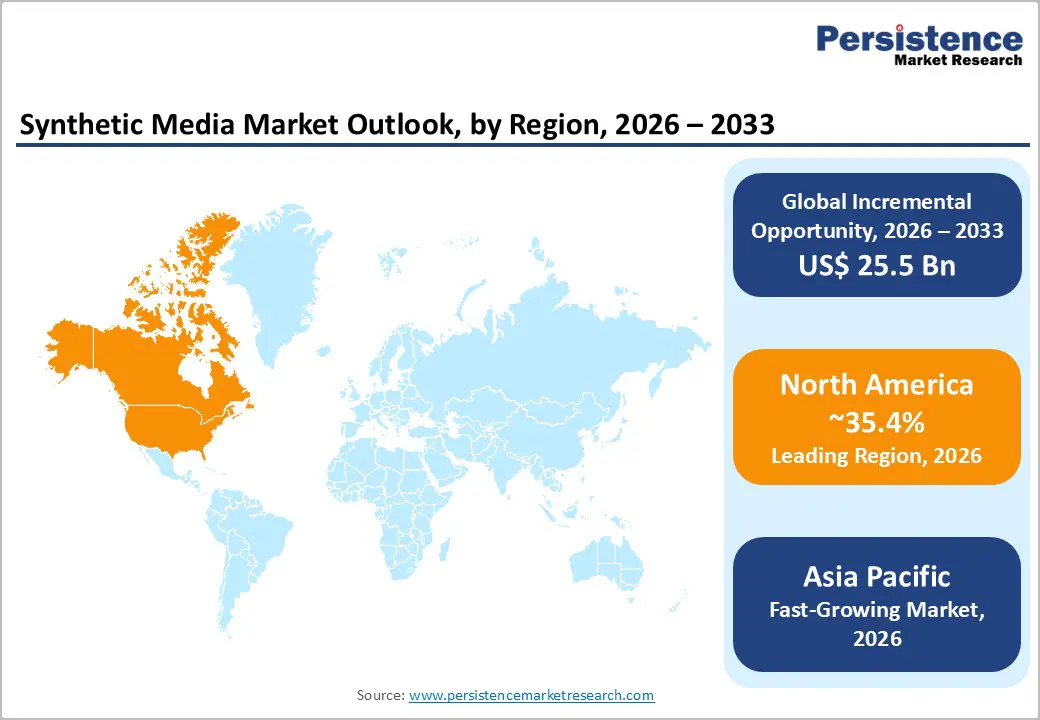

- Leading Region: North America is projected to account for approximately 35.4% of the market share in 2026, due to strong AI infrastructure, enterprise software adoption, and the presence of major technology companies across the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is projected to expand, supported by rapid digitalization, multilingual content demand, and increasing AI investments across China, India, Japan, South Korea, and ASEAN countries.

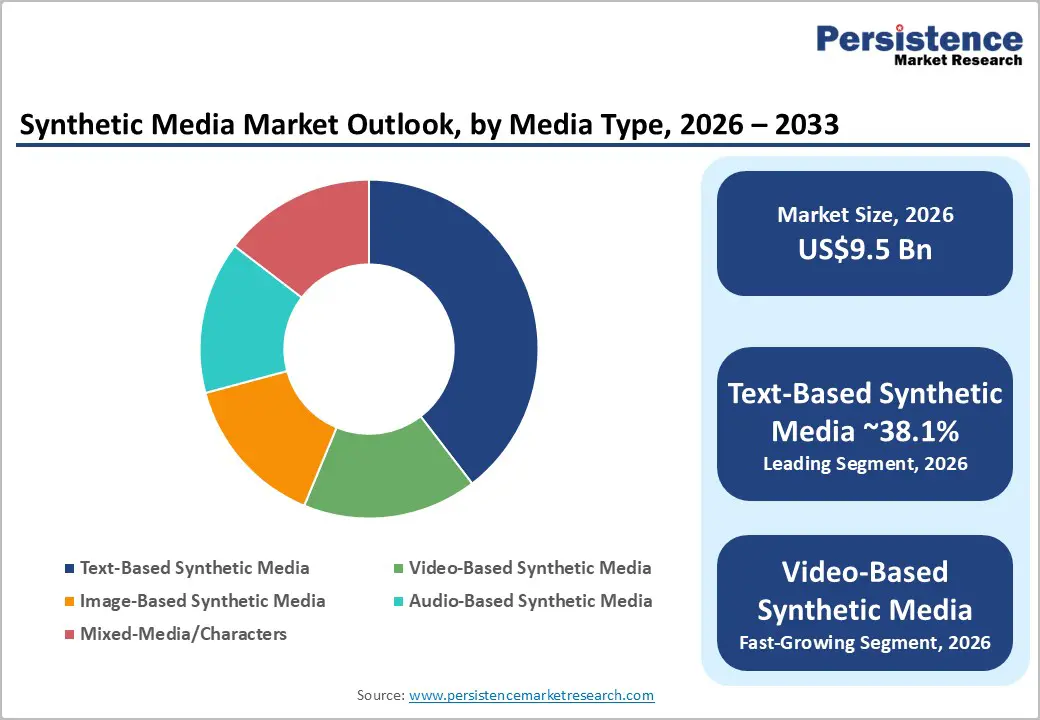

- Dominant Media Type: Text-based synthetic media is anticipated to hold approximately 38.1% market share in 2026, due to broad enterprise adoption across content marketing, customer support, business communication, and workflow automation applications.

- Leading Enterprise: Large enterprises are expected to account for nearly 46.2% of market share in 2026, driven by enterprise-scale AI deployment, centralized governance requirements, and rising adoption of AI-powered communication and training systems.

DRO Analysis

Driver - Enterprise Adoption of AI-Driven Content Automation Accelerates Market Expansion

Enterprises across media, retail, education, BFSI, and technology sectors are rapidly integrating synthetic media into content production workflows to improve operational efficiency and reduce production timelines. AI-powered platforms now support automated script generation, image creation, synthetic voice production, multilingual localization, and avatar-based communication at scale. This transition is being fueled by rising demand for digital-first customer engagement and always-on content delivery models.

Organizations are increasingly prioritizing scalable content production to support omnichannel marketing strategies, e-learning platforms, product demonstrations, and customer-support operations. Synthetic media significantly reduces dependence on traditional production resources, including studios, actors, editors, and localization teams. Large enterprises are deploying these tools to improve campaign turnaround time and optimize marketing expenditure while maintaining personalization standards.

The growing integration of generative AI into enterprise productivity suites, design ecosystems, and cloud platforms is further accelerating adoption. Technology providers are embedding AI generation capabilities into workflow software, enabling enterprises to operationalize synthetic media across departments rather than limiting deployment to experimental innovation teams.

Regulatory Frameworks Are Increasing Demand for Provenance and Verification Solutions

The expansion of AI governance frameworks across North America, Europe, and Asia Pacific is creating structural demand for synthetic media authentication and content verification technologies. Governments and regulatory agencies are increasingly focused on deepfake disclosure, digital watermarking, content provenance, and AI-generated media transparency requirements.

The introduction of AI transparency obligations in Europe, alongside deepfake-related enforcement activity in the U.S. and Asia, is compelling enterprises to adopt compliance-oriented synthetic media solutions. Organizations operating in regulated industries such as BFSI, healthcare, education, and government communications are prioritizing platforms capable of supporting auditability, content traceability, and disclosure mechanisms.

This evolving regulatory environment is reshaping procurement priorities. Enterprises are no longer evaluating synthetic media platforms solely on generation quality and productivity gains; governance capabilities, brand safety controls, and compliance infrastructure are becoming equally important decision criteria. As a result, vendors offering integrated verification, watermarking, and moderation tools are gaining competitive advantages in enterprise deployments.

Restraint - Deepfake Misuse, Intellectual Property Concerns, and Trust Deficits Limit Adoption

Despite strong market momentum, synthetic media adoption continues to face resistance due to concerns surrounding misinformation, identity fraud, copyright disputes, and reputational risk. The increasing sophistication of AI-generated deepfakes has intensified scrutiny from governments, enterprises, and consumers, particularly in politically sensitive and highly regulated sectors.

Organizations deploying synthetic media must address complex legal and ethical challenges related to ownership rights, consent management, and unauthorized replication of voices, likenesses, and copyrighted material. These concerns are increasing compliance costs and extending approval timelines for enterprise-scale deployments. Companies are also investing heavily in moderation systems, legal reviews, and content governance frameworks to mitigate operational risks.

The absence of globally harmonized regulatory standards further complicates market expansion, especially for multinational enterprises operating across multiple jurisdictions. Uncertainty regarding future compliance requirements may delay procurement decisions and slow adoption rates in sectors with strict reputational and regulatory exposure.

Opportunity - Content Provenance and Verification Platforms Create High-Value Commercial Opportunities

The increasing regulatory emphasis on AI transparency is creating substantial opportunities for vendors specializing in content verification, provenance tracking, watermarking, and synthetic media governance. Enterprises deploying AI-generated content at scale require mechanisms capable of authenticating media origin, identifying manipulated assets, and ensuring compliance with emerging disclosure regulations.

Content credentialing technologies are evolving into standalone commercial categories rather than supplementary platform features. Organizations are increasingly seeking integrated governance layers capable of monitoring synthetic content throughout production, distribution, and archival workflows. This demand is especially strong in news media, financial services, healthcare communications, and public-sector information systems, where content integrity is strategically critical.

Vendors capable of combining generation and verification capabilities within unified enterprise ecosystems are positioned to capture long-term recurring revenue opportunities. The growing requirement for responsible AI deployment is expected to accelerate investments in auditability, digital signatures, metadata tracking, and AI content authentication infrastructure.

Multilingual Synthetic Video and Conversational AI Open New Enterprise Use Cases

Rapid advances in multilingual video generation, AI voice synthesis, and conversational avatar technology are expanding the commercial potential of synthetic media across global enterprise operations. Organizations increasingly require scalable communication systems capable of supporting geographically distributed customers, employees, and partners in multiple languages.

Synthetic media platforms now enable enterprises to generate localized training modules, customer-support content, product explainers, onboarding materials, and marketing campaigns without traditional production bottlenecks. AI-generated avatars and voice systems significantly reduce localization costs while enabling rapid deployment across international markets. Industries including e-learning, retail, telecommunications, healthcare, and enterprise software are expected to emerge as major adopters of conversational synthetic media systems during the forecast period.

Category-wise Analysis

Media Type Insights

Text-based synthetic media is anticipated to account for 38.1% of the market share in 2026, due to its widespread adoption across content marketing, customer support, enterprise communication, and workflow automation. Businesses increasingly use AI-generated text for copywriting, multilingual translation, chatbot interactions, automated reporting, and search optimization.

Platforms such as ChatGPT, Microsoft Copilot, and Google Gemini are accelerating enterprise adoption by integrating AI text generation into productivity and collaboration software. The segment benefits from lower deployment complexity and faster enterprise integration compared with video and avatar-based systems. Growing demand for scalable digital communication and automated content workflows is expected to sustain segment dominance throughout the forecast period.

Video-based synthetic media is projected to be the fastest-growing segment due to rising enterprise demand for scalable visual communication and personalized digital engagement. AI-generated video significantly reduces production costs associated with filming, editing, localization, and studio infrastructure. Companies are increasingly deploying synthetic video solutions for employee training, e-commerce demonstrations, marketing campaigns, and educational content.

Platforms such as Synthesia, Runway, and HeyGen are expanding adoption through AI avatars, text-to-video generation, and multilingual video capabilities. The rapid growth of short-form video content and video-first marketing strategies continues to strengthen demand across media, retail, and enterprise communication sectors.

Enterprise Insights

Large enterprises are anticipated to account for 46.2% of market share in 2026, due to stronger IT budgets, enterprise governance requirements, and large-scale digital transformation initiatives. These organizations are integrating synthetic media across marketing, customer engagement, workforce training, and multilingual communication workflows.

Enterprises prioritize security controls, compliance infrastructure, workflow integration, and centralized governance capabilities. Companies such as Adobe, Microsoft, and NVIDIA are increasingly offering enterprise-grade AI content ecosystems designed for scalable deployment. The ability to reduce production costs while maintaining consistent global communication is driving strong adoption among multinational organizations.

Tech-enabled SMBs are projected to be the fastest-growing customer segment as cloud-based AI platforms, subscription pricing, and self-service tools reduce adoption barriers. Smaller businesses are increasingly utilizing synthetic media to improve marketing efficiency, accelerate content production, and strengthen e-commerce engagement without investing heavily in creative infrastructure.

Platforms such as Canva, Descript, and ElevenLabs are supporting SMB adoption through affordable AI-driven content creation, voice synthesis, and editing solutions. The expansion of startup ecosystems, creator economies, and digital commerce platforms is expected to sustain strong growth momentum among SMBs during the forecast period.

Regional Insights

North America Synthetic Media Market Trends

North America remains the leading regional market, accounting for approximately 35.4% of the global market share.

U.S. Synthetic Media Market Trends

The U.S. dominates the North American synthetic media market due to its advanced AI innovation ecosystem, strong cloud infrastructure, and concentration of major technology companies. The country benefits from significant venture capital investment and rapid commercialization of generative AI technologies across media, advertising, e-commerce, education, and enterprise software sectors.

U.S.-based companies, including Adobe, Microsoft, OpenAI, NVIDIA, Runway, and Meta, continue expanding investments in synthetic video generation, conversational AI, and enterprise-grade content platforms. Regulatory developments related to AI governance, deepfake disclosure, and consumer protection are also influencing enterprise procurement strategies. Businesses increasingly prioritize compliant and transparent synthetic media solutions capable of supporting auditability and enterprise risk management.

Canada Synthetic Media Market Trends

Canada is strengthening its position in the synthetic media market through government-backed AI research initiatives, growing startup activity, and increasing enterprise adoption of AI-powered communication tools. The country benefits from a strong academic AI ecosystem and expanding investments in generative AI commercialization.

Canadian enterprises are increasingly utilizing synthetic media for customer engagement, multilingual communication, digital marketing, and corporate training applications. Regulatory focus on ethical AI deployment and responsible innovation is also encouraging demand for transparent and governance-oriented synthetic media platforms.

Europe Synthetic Media Market Trends

Europe is emerging as a compliance-driven synthetic media market characterized by strong regulatory oversight and increasing enterprise investment in responsible AI deployment.

U.K. Synthetic Media Market Trends

The U.K. remains one of Europe’s leading synthetic media markets due to strong AI startup activity, advanced digital infrastructure, and growing enterprise investment in generative AI technologies. Businesses across advertising, media, ecommerce, and enterprise communication sectors are increasingly deploying synthetic media for content automation and digital engagement.

The country is also emphasizing responsible AI deployment through digital governance and online safety initiatives. Increasing demand for AI-generated video, voice synthesis, and conversational avatars is supporting market expansion across both enterprises and creator-driven platforms.

Germany Synthetic Media Market Trends

Germany is witnessing strong adoption of synthetic media technologies across enterprise communication, manufacturing training, automotive marketing, and industrial digitalization initiatives. German companies prioritize secure and enterprise-grade AI systems capable of integrating into broader digital transformation strategies.

The country’s emphasis on regulatory compliance, data security, and workflow efficiency is encouraging the adoption of synthetic media solutions with advanced governance and provenance-tracking capabilities. Demand for multilingual training content and AI-powered enterprise communication tools is also increasing across large industrial organizations.

Asia Pacific Synthetic Media Market Trends

Asia Pacific is projected to be the fastest-growing regional market, expanding at an estimated 18.3% CAGR during the forecast period.

China Synthetic Media Market Trends

China remains one of the largest synthetic media markets in Asia Pacific, due to strong government support for AI development, rapid digitalization, and large-scale adoption of AI-powered content platforms. The country’s e-commerce, entertainment, gaming, and social media sectors are major users of synthetic video, AI-generated avatars, and voice technologies.

Chinese technology companies are investing heavily in generative AI infrastructure, multilingual content systems, and AI-driven digital engagement platforms. Regulatory oversight related to deepfake disclosure, cybersecurity, and AI governance is also shaping enterprise deployment strategies across the market.

India Synthetic Media Market Trends

India is emerging as one of the fastest-growing synthetic media markets, due to expanding internet penetration, rapid digital commerce growth, and strong demand for multilingual communication tools. Enterprises are increasingly utilizing synthetic media for customer engagement, education technology, marketing automation, and workforce training applications.

The country’s large multilingual population creates strong demand for AI-generated voice, translation, and localized video solutions. Growth in startup ecosystems, SaaS platforms, and creator-driven digital content industries is expected to further accelerate market adoption during the forecast period.

Japan Synthetic Media Market Trends

Japan is strengthening synthetic media adoption across gaming, entertainment, robotics, enterprise communication, and digital marketing industries. Companies are increasingly deploying AI-generated avatars, virtual humans, and voice synthesis technologies to improve customer interaction and content personalization.

The country’s advanced technology infrastructure and strong investment in automation are supporting enterprise adoption of AI-powered communication systems. Businesses are also prioritizing secure and compliant AI deployment strategies aligned with Japan’s broader digital transformation initiatives.

Competitive Landscape

The global synthetic media market remains moderately fragmented, with competition distributed across AI infrastructure providers, generative AI platform vendors, synthetic video companies, voice-synthesis providers, and enterprise workflow software developers. While several global technology firms maintain advantages in cloud infrastructure, AI model development, and enterprise distribution, specialized vendors continue to compete effectively through innovation and niche application expertise.

Leading companies are prioritizing product innovation, enterprise trust, platform integration, and workflow scalability. Vendors are increasingly focusing on responsible AI deployment, multimodal generation capabilities, localization efficiency, and API-based ecosystem expansion. Strategic differentiation is increasingly based on governance infrastructure, enterprise-grade security, and integrated content verification capabilities.

Key Industry Developments:

- In February 2025, Adobe announced the launch of its new Firefly application and Firefly Video Model in public beta, enabling enterprises and creators to generate commercially safe AI-powered video, image, and audio content integrated directly with Creative Cloud workflows.

- In May 2025, ElevenLabs launched Conversational AI 2.0 with multilingual detection, HIPAA-compliant infrastructure, and enterprise-grade security enhancements to expand adoption across customer service, healthcare, and multilingual communication applications.

Companies Covered in Synthetic Media Market

- Adobe

- OpenAI

- Microsoft

- Meta

- NVIDIA

- Runway

- Synthesia

- ElevenLabs

- HeyGen

- D-ID

- Stability AI

- Descript

- Colossyan

- Midjourney

- Canva

Frequently Asked Questions

The global synthetic media market is anticipated to be valued at US$9.5 billion in 2026.

The synthetic media market is projected to reach approximately US$35.0 billion by 2033.

Major trends include the rapid adoption of AI-generated video content, conversational AI, multilingual synthetic voice technologies, avatar-based communication, and content provenance systems.

Text-based synthetic media is anticipated to remain the leading segment, accounting for approximately 38.1% of market share, supported by strong enterprise adoption across marketing, customer support, workflow automation, and digital communication applications.

The synthetic media market is projected to expand at a CAGR of 20.5% between 2026 and 2033.

Major companies include Adobe, Microsoft, OpenAI, NVIDIA, and Synthesia.