- Media & Entertainment

- Over the Top Devices and Services Market

Over the Top Devices and Services Market Size, Share, and Growth Forecast 2026 - 2033

Over the Top Devices and Services Market by Device Type (Streaming Media Players, Streaming Sticks), by Service Type (OTT Media Services, OTT Communication Services), by OTT Business Model, by Platform, and Regional Analysis, 2026 - 2033

Over the Top Devices and Services Market Size and Trends Analysis

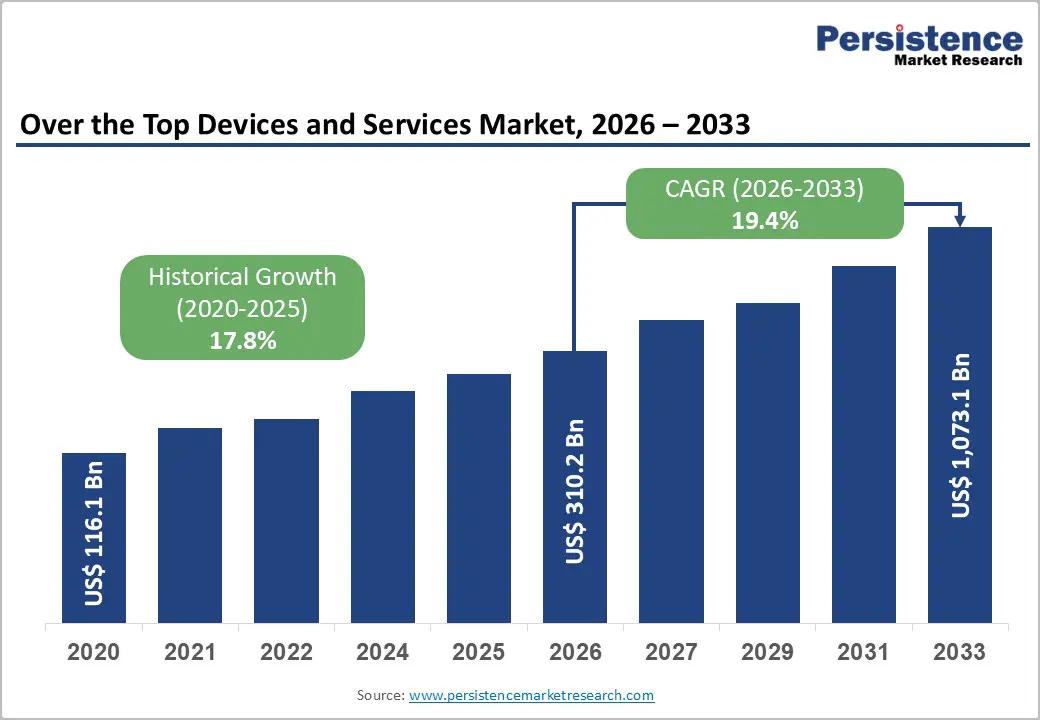

The global over the top devices and services market size is likely to be valued at US$310.2 billion in 2026 and is expected to reach US$1,073.1 billion by 2033, growing at a CAGR of 19.4% during the forecast period from 2026 to 2033, driven by the ongoing shift from linear television to on-demand streaming, which is supported by rising smart TV and connected device penetration across households.

Key Industry Highlights:

- Leading Device Type: Streaming media players, approximately 68.2% share in 2026, as these provide a low-cost solution that converts traditional TVs into smart streaming hubs.

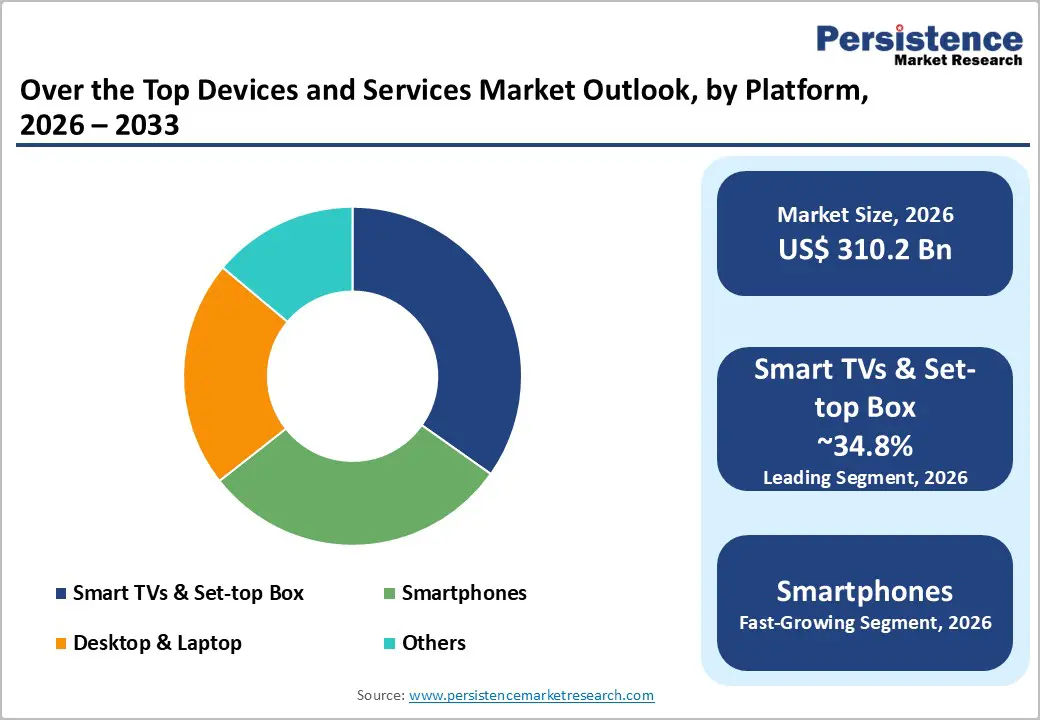

- Dominant Platform: Smart TVs and set-top boxes, nearly 34.8% in 2026, as large-screen viewing remains preferred for long-form content.

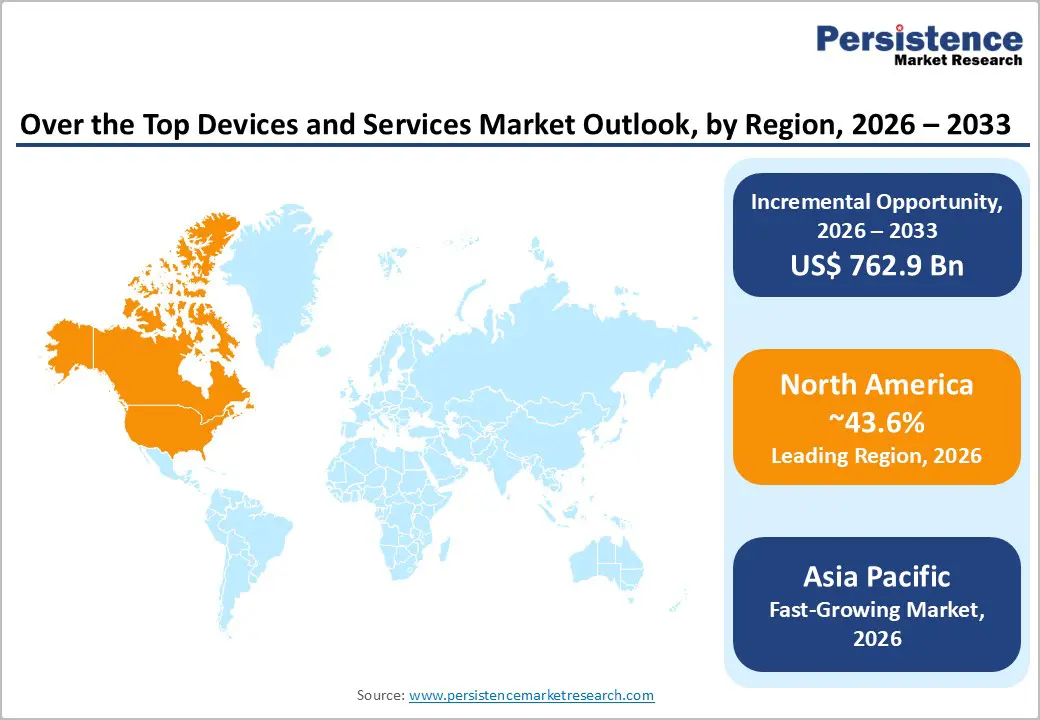

- Leading Region: North America, with about 43.6% share in 2026, owing to its mature streaming interface and high broadband penetration.

- Fast-growing Region: Asia Pacific, backed by rising smartphone usage and expanding 5G networks.

- Latest Collaboration: In April 2026, Frodoh entered a strategic partnership with Chaupal to introduce a first-screen monetization framework for subscription-led OTT services. The initiative was designed to create additional advertising revenue streams without interrupting viewer content experiences.

DRO Analysis

Driver - Ongoing Shift toward Anytime and Anywhere Viewing

Viewers are moving away from fixed broadcast schedules in favor of watching what they want, when they want. OTT services allow consumers to access a large library of content on demand across PCs, tablets, smartphones, and smart televisions from any location, releasing them from strict television schedules. This behavioral shift is backed by device trends.

In 2024, apps made up 59% of OTT content consumption, rising from just 40% the year before, with audiences watching 1.5 billion minutes on mobile and TV apps. It was nearly double the minutes recorded on web platforms. Device accessibility also plays a direct role. Streaming sticks are witnessing high popularity, propelled by their affordability, portability, and ease of installation. Developments such as 4K streaming support, voice control, and integration with smart home ecosystems are further expected to boost the market.

Regional Content, Smart Recommendations, and Tiered Pricing

OTT platforms are moving well beyond English-language content to attract viewers across income levels and geographies. Localized content drives 26% of OTT subscriptions in emerging markets, while Netflix reports that approximately 80% of its watched content stems from AI-supported recommendations. AI-generated subtitles and dubbing are also reducing the cost barrier to localization. By 2024, these tools had reduced localization costs by 62% across platforms.

On pricing, flexibility is attracting a diverse range of income groups. Ad-supported models are gaining impetus, particularly in price-sensitive emerging markets. In January 2025, for example, Viaplay launched a tiered subscription model in the Netherlands. It offers a basic ad-supported plan and an ad-free standard plan, catering to users across budget ranges.

Restraint - Content Scattered across Platforms May Push Users to Cancel

As content rights become more fragmented, viewers are compelled to hold multiple subscriptions just to follow their preferred shows. As of 2024, the average American subscribes to four different OTT services. Managing multiple subscriptions can be cumbersome, leading to subscription fatigue. The financial and psychological toll is well-documented. According to a 2025 report, 47% of U.S. consumers feel overwhelmed by the number of subscriptions they manage, with nearly one-third planning to cut at least one service.

A peer-reviewed study published in SAGE Journals confirms the mechanism. High search costs and subscription fees propel discontinuation, while 45% of multi-homing users cancel at least one service, citing high subscription costs as the main reason. This fragmentation is also pushing consolidation. Paramount+ and Showtime are in the process of merging as a direct response to declining engagement and the inability to compete with large-scale platforms.

Opportunity - Emergence of Ad-Supported Free Streaming

Free Ad-Supported Streaming TV (FAST) is filling a key gap for viewers unwilling to pay for multiple subscriptions. Rather than replacing paid platforms, it delivers a feasible alternative at zero cost to the viewer. Free ad-supported streaming services collectively captured about 5.7% of total U.S. TV viewing in May 2025, a combined FAST share that now exceeds the individual viewing share of any single broadcast network.

The scope of individual platforms reflects this momentum. Fox Corporation announced that Tubi reached 97 million monthly active users and 10 billion streaming hours in 2024. Also, the Super Bowl LIX broadcast on FOX and Tubi together generated US$800 million in combined advertising revenue in February 2025. Content variety is expanding, too. Reality programming channels on FAST surged 626% between July 2024 and March 2025, surging from 19 to 138 channels globally.

5G Rollout and Cloud-Native Infrastructure

Improved network infrastructure is directly addressing long-standing quality complaints about live and on-demand streaming. The ongoing integration of 5G networks has increased mobile streaming speeds by nearly 45%, enabling ultra-high-definition streaming without latency bottlenecks. Cloud-native approaches are bringing down costs while improving reliability. AWS's 2025 Media & Entertainment Cloud Report found that broadcasters adopting serverless transcoding workflows reduced their video processing costs by an average of 58% compared to VM-based approaches.

Network slicing is a prominent development here. Verizon and T-Mobile both launched commercial IPTV-optimized 5G slices in 2025. These enabled OTT providers to purchase dedicated slice capacity from mobile carriers and ensured their streams receive priority bandwidth regardless of total network load. For live events, a U.S.-based sports streaming pilot in 2024 reduced latency by 42% using edge-based AI encoding. This pointed to significant headroom for improvement in quality-sensitive use cases.

Category-wise Analysis

Device Type Insights

The streaming media players segment is predicted to lead with around 68.2% of share in 2026, owing to their ability to provide low-cost access to multiple streaming services without requiring consumers to replace existing televisions. Devices such as Roku, Amazon Fire TV, Apple TV, and Chromecast have become central entertainment hubs by combining OTT apps, gaming, voice assistants, and advertising-supported content into one interface. Roku stated in 2025 that streaming through Roku-powered devices surpassed broadcast TV viewing in the U.S. for three consecutive months. Roku accounted for around 21.4% of all television viewing time in July 2025.

Streaming sticks are expected to be the fastest-growing segment in 2026, as these provide an inexpensive upgrade path for older televisions while supporting unique features such as 4K streaming, AI recommendations, and cloud gaming. Governments and broadcasters are also recognizing streaming sticks as mainstream television delivery equipment. The U.K. government’s online prominence policy specifically identified streaming sticks, smart TVs, and set-top boxes as primary internet television devices, as they are now widely used for video viewing in households.

Platform Insights

Smart TVs and set-top boxes are projected to dominate with nearly 34.8% of share in 2026, as television screens continue to be the primary environment for long-form content consumption. According to the U.K. government and Ofcom data, TV sets accounted for 84% of total in-home video viewing in 2023, while smart TV household penetration reached 76% in the country. Smart TVs have evolved beyond passive displays into integrated entertainment ecosystems supporting OTT apps, live TV, gaming, and targeted advertising. Broadcasters and advertisers increasingly prioritize connected TV environments as they allow audience tracking, personalized advertising, and subscription monetization.

Smartphones are anticipated to remain in the second position in the forecast period. Mobile viewing has become deeply integrated into everyday digital behavior. OTT consumption is no longer limited to living rooms. Users stream content during commuting, work breaks, and travel. In markets such as India and Southeast Asia, smartphones often serve as the primary internet device due to lower smartphone costs compared to laptops and televisions. The Consumer Technology Association also highlighted in 2025 that 92% of U.S. adults received emergency alerts via smartphones, reinforcing how mobile devices remain constantly accessible and central to digital engagement.

Regional Insights

North America Over the Top Devices and Services Market Trends

In 2026, North America is expected to lead with approximately 43.6% of the share, as the region has high smart home penetration, mature digital payment systems, well-established broadband infrastructure, and some of the world’s largest streaming companies. Companies such as Netflix, Amazon, Disney, Roku, Apple, and Warner Bros. Discovery have created a novel streaming interface supported by premium advertising and subscription models. Connected TV advertising is particularly superior in North America, as advertisers can precisely target audiences using streaming analytics. Roku also reported that more than half of U.S. internet-enabled homes now use Roku-powered devices or operating systems.

U.S. Over the Top Devices and Services Market Trends

The U.S. is witnessing steady growth as consumers are constantly shifting away from cable television toward app-based viewing ecosystems. Streaming services now compete not only on content but also on user interface quality, AI recommendations, sports rights, and advertising technology. Roku’s 2025 viewing data showed streaming overtaking broadcast television in the country, showcasing how OTT has become mainstream rather than supplementary entertainment. The rise of ad-supported streaming tiers from Netflix, Disney+, and Amazon Prime Video is also accelerating adoption among price-sensitive consumers.

Asia Pacific Over the Top Devices and Services Market Trends

Asia Pacific is anticipated to be the fastest-growing market in the forecast period, attributed to rising smartphone penetration, expanding 5G infrastructure, low-cost internet availability, and superior regional-language content demand. Countries such as India, Indonesia, South Korea, and Thailand are witnessing rising connected TV adoption alongside mobile streaming growth. International OTT providers are also investing in local-language originals and sports broadcasting to capture regional audiences. The region further benefits from a younger digital population that prefers on-demand streaming over scheduled television programming.

Japan Over the Top Devices and Services Market Trends

Japan remains a key market due to its unique broadband infrastructure, high smart TV adoption, and rising demand for anime, gaming, and premium digital entertainment. Local consumers are also early adopters of high-resolution streaming technologies and hybrid entertainment ecosystems combining gaming consoles, OTT apps, and smart televisions. Global OTT providers continue partnering with Japan-based studios to secure anime distribution rights, which has made the country strategically important for international content expansion.

India Over the Top Devices and Services Market Trends

India represents one of the most competitive OTT markets globally, owing to its massive multilingual audience base and mobile-first viewing culture. Ormax Media estimated India’s OTT audience at more than 601 million users in 2025, while connected TV audiences increased by around 87% within a year to reach over 129 million users. Cricket streaming, regional-language entertainment, telecom bundling, and affordable data pricing continue pushing OTT adoption. Connected TVs have also overtaken laptops and tablets to become India’s second-most-used streaming device after smartphones. Platforms such as JioHotstar, Netflix, Amazon Prime Video, SonyLIV, and ZEE5 are heavily investing in regional content and sports rights to maintain subscriber growth.

Europe Over the Top Devices and Services Market Trends

Europe is growing steadily as consumers are gradually transitioning from traditional broadcasting to hybrid streaming environments rather than abandoning linear television entirely. Broadcasters across the region are integrating OTT services with existing television infrastructure to retain audiences. Smart TV penetration, broadband quality, and connected advertising interfaces continue improving across Western Europe, supporting sustainable OTT growth rather than sudden disruption.

U.K. Over the Top Devices and Services Market Trends

The U.K. is experiencing rapid OTT growth as streaming has started overtaking traditional television viewing behavior, especially among younger demographics. Ofcom reported that YouTube became the second most-watched media service in the country behind the BBC. Younger viewers opened YouTube immediately after turning on televisions. Separate U.K. viewing studies in 2025 also showed app-based broadcaster viewing surpassing over-the-air television for the first time. Regulatory modernization under the Media Act is further encouraging the expansion of internet-delivered television services and OTT integration.

Germany Over the Top Devices and Services Market Trends

Germany is witnessing decent OTT growth as consumers are now adopting subscription streaming services alongside connected TV platforms while still maintaining strong public broadcasting consumption habits. The country’s growth is also being supported by high broadband penetration, expanding smart TV usage, and increasing adoption of hybrid TV-streaming services. Audiences have further shown rising demand for international streaming content, sports packages, and localized OTT originals. It has encouraged both global and regional streaming providers to expand their portfolios in the market.

Competitive Landscape

The global over the top devices and services market is moderately fragmented at the platform level but consolidated around a few dominant companies. Companies such as Netflix, Amazon, Disney, Roku, Apple, and Samsung Electronics are strengthening their positions through vertically integrated strategies. These combine streaming services, smart TV operating systems, advertising technology, and exclusive content libraries.

Competition in OTT services is also being driven by bundled offerings, sports rights, and ad-supported streaming tiers. Amazon has strengthened Prime Video by integrating shopping data and targeted advertising tools, while Netflix and Disney continue expanding low-cost ad-supported plans to reduce subscriber churn. In 2025, Amazon Prime Video reportedly led U.S. streaming share with around 22%, slightly ahead of Netflix.

Key Industry Developments:

- In December 2025, Yupp Video Services partnered with regional OTT platform Chaupal to overhaul the latter’s streaming infrastructure across more than 25 devices. The upgrade included AI-supported recommendation systems, backend expansion improvements, and improved playback optimization for regional-language audiences.

- In May 2025, OTTplay Premium collaborated with GTPL Hathway to launch GTPL Genie+. It is a bundled OTT entertainment offering providing access to content from over 29 streaming platforms through GTPL’s digital interface.

- In February 2025, JioStar launched JioHotstar by merging JioCinema and Disney+ Hotstar into a single OTT platform. The new service combined over 300,000 hours of entertainment and live sports content while introducing AI-based recommendations and multilingual streaming support across devices.

Companies Covered in Over the Top Devices and Services Market

- Netflix, Inc.

- Amazon.com, Inc.

- Disney+ Hotstar

- Apple, Inc.

- Warner Bros.

- Discovery, Inc.

- Hulu, LLC

- Tencent Holdings Ltd.

- Roku, Inc.

- Akamai Technologies

- Baidu, Inc.

- Others

Frequently Asked Questions

The global over the top devices and services market is projected to be valued at US$310.2 billion in 2026.

The over the top devices and services market is expected to reach US$1,073.1 billion by 2033.

Key market trends include the rise of ad-supported streaming tiers and the increasing integration of OTT with telecom bundles.

Streaming media players are estimated to be the leading devices with a share of about 68.2% in 2026, owing to their ability to aggregate multiple OTT platforms in a single unified environment.

The over the top devices and services market is expected to grow at a CAGR of 19.4% from 2026 to 2033.

Netflix, Inc., Amazon.com, Inc., Disney + Hotstar, and Apple, Inc. are a few key market players.