- Clothing, Footwear, & Accessories

- Surfing Apparel and Accessories Market

Surfing Apparel and Accessories Market Size, Share, and Growth Forecast 2026 - 2033

Surfing Apparel and Accessories Market by Product (Apparels: Wetsuits, Board Shorts, Surf Tees, Others; Accessories: Surfboard Leash, Fins, Others), by Material (Neoprene, Lycra/Spandex, Polyester, Nylon, Recycled Materials, Organic Fabrics), by Distribution Channel (Offline, Online), by End User (Men, Women, Unisex), and Regional Analysis, 2026 - 2033

Surfing Apparel and Accessories Market Size and Trend Analysis

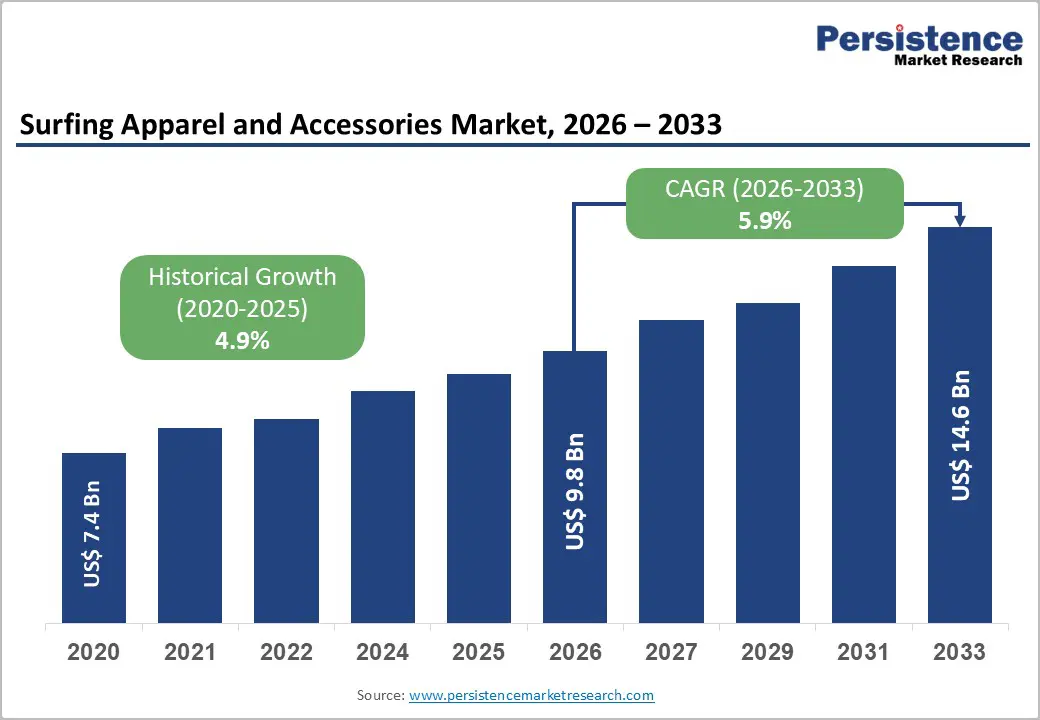

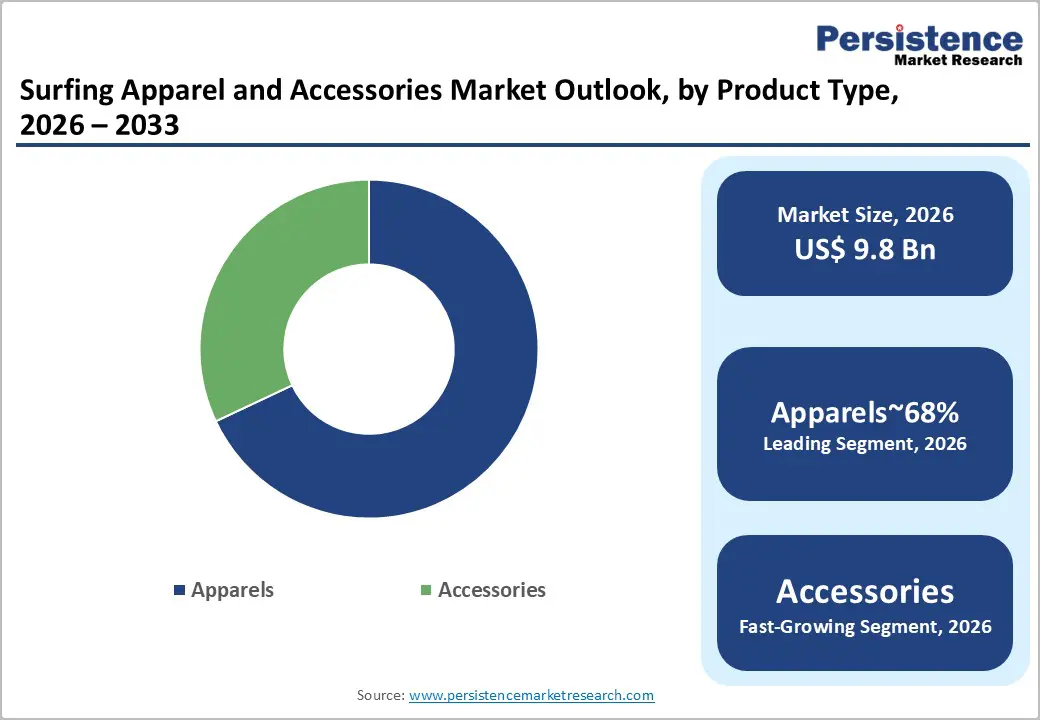

The global Surfing Apparel and Accessories market is likely to be valued at US$ 9.8 Billion in 2026 and is expected to reach US$ 14.6 Billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

Market growth is driven by rising global surfing participation, boosted by its inclusion in the Olympic Games, which increased visibility and commercial appeal. Expanding female participation, sustainable wetsuit innovations, surf-inspired athleisure trends, and growing e-commerce access are further accelerating demand, especially across Asia Pacific and Latin America markets.

Key Industry Highlights:

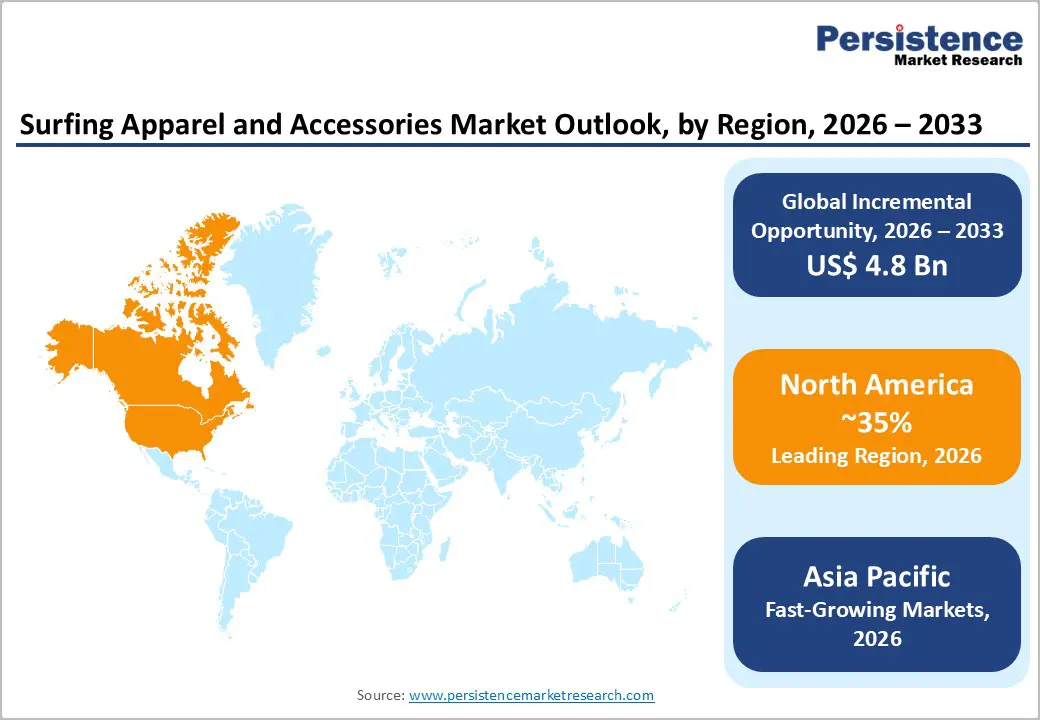

- Leading Region: North America leads the global Surfing Apparel and Accessories market holding 35% share in the market, with the United States hosting the world's highest concentration of surf brand headquarters, including Quiksilver, Inc., Hurley, Inc., and Volcom, LLC, and sustaining a massive domestic lifestyle and performance surf apparel consumer base across California, Hawaii, and Florida.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 7.1%, driven by expanding surf cultures in Indonesia, Japan, and India, the ISA's grassroots development programs across over 100 countries, and the confirmed hosting of surfing as an Olympic discipline at the Brisbane 2032 Olympic Games, generating sustained regional participation growth and brand investment.

- Leading Segment: The Apparel segment dominates by product category with approximately 68% market share, anchored by the high-value wetsuit sub-category and high-volume board shorts and surf tees that generate consistent lifestyle fashion demand extending well beyond the active surfer demographic into the global athleisure and surf-culture consumer base.

- Fastest-Growing Segment: The Recycled Materials segment is the fastest-growing material category, driven by the surfing community's deep ocean conservation culture, bluesign and GRS certification adoption by leading brands, and documented 20% annual growth in global recycled fiber markets per Textile Exchange, compelling all major players to transition product portfolios.

- Key Opportunity: A significant market opportunity lies in developing purpose-built women's surf apparel lines, supported by the ISA's gender equality programs and WSL's equal prize money policy, targeting the fastest-growing active participant demographic with performance-validated, fit-optimized wetsuits and technical surf apparel that command premium pricing and strong brand loyalty among female surfers globally.

| Key Insights | Details |

|---|---|

|

Surfing Apparel and Accessories Market Size (2026E) |

US$ 9.8 Billion |

|

Market Value Forecast (2033F) |

US$ 14.6 Billion |

|

Projected Growth CAGR (2026–2033) |

5.9% |

|

Historical Market Growth (2020–2025) |

4.9% |

Market Dynamics

Driver - Olympic Inclusion and the Rise in Global Surf Participation Drives Sustained Demand Growth

Surfing’s inclusion in the Olympic Games, beginning with Tokyo 2020, followed by Paris 2024, and confirmed for Brisbane 2032, has significantly increased the sport’s global visibility and credibility. This exposure has expanded surfing beyond traditional coastal strongholds into new and emerging markets. The International Surfing Association, affiliated with the International Olympic Committee, reports that surfing is now practiced in more than 100 countries, with over 35 million active participants worldwide.

Olympic recognition has encouraged both government and private investment in surf academies, coastal infrastructure, and national development programs across Asia, Latin America, and Africa. These initiatives are creating new generations of surfers who require full apparel and equipment kits. As participation continues to expand structurally, demand for wetsuits, board shorts, surf tees, and performance accessories is expected to grow steadily through 2033 across both entry-level and competitive consumer segments.

Surf Culture's Integration into Mainstream Athleisure Fashion Expanding the Addressable Consumer Base

Surf-inspired fashion has successfully moved beyond the beach and into mainstream athleisure and streetwear culture, significantly expanding the total addressable market for surf apparel brands. Products such as board shorts, rash guards, printed tees, and branded casual wear are increasingly worn by urban consumers who identify with surf culture even if they do not actively surf. Leading brands including Quiksilver, Inc., Billabong, Volcom, LLC, and RVCA have positioned themselves as lifestyle fashion labels rather than purely performance-focused surf brands.

According to the Surf Industry Manufacturers Association, lifestyle surf apparel consistently generates higher revenue than technical surf equipment. This broader consumer appeal allows brands to sustain premium pricing and expand retail distribution globally. As a result, revenue growth is increasingly supported by lifestyle-driven purchases, reducing dependence solely on active surf participation.

High Cost of Premium Wetsuits and Technical Surf Accessories Constraining Entry-Level Adoption

The high price of premium surf apparel, especially advanced wetsuits, remains a key barrier to wider participation. High-performance wetsuits made with specialized neoprene technology often retail between US$200 and US$600, depending on insulation level and construction quality. Leading brands such as O'Neill and Billabong dominate this premium segment, but their pricing can discourage new and cost-sensitive consumers.

In emerging markets across South Asia, Africa, and parts of ASEAN, surfing participation is growing; however, purchasing power remains moderate. As a result, many new surfers delay or limit investments in high-end gear. This affordability gap slows revenue growth compared to participation growth. While demand fundamentals remain strong, the premium pricing structure moderates faster market expansion in developing regions and among recreational users.

Environmental and Sustainability Concerns Pressuring Conventional Neoprene Manufacturing

Environmental concerns surrounding conventional neoprene production are creating increasing pressure on surf apparel manufacturers. Traditional neoprene is derived from petrochemicals and involves carbon-intensive manufacturing processes, which conflict with surfing’s strong environmental values. Organizations such as the Surfrider Foundation actively advocate for ocean conservation and sustainable product innovation within the industry. As environmental awareness grows, consumers are becoming more selective and favor brands that demonstrate measurable sustainability commitments.

Companies that continue relying solely on traditional petroleum-based materials face reputational risks and potential loss of environmentally conscious customers. Regulatory attention on textile sustainability is also strengthening globally. This shift in consumer behavior and regulatory oversight is encouraging manufacturers to accelerate investment in recycled and bio-based alternatives. Brands that fail to adapt may gradually lose market share within a community that strongly values ocean protection and environmental responsibility.

Growth of Women's Surf Participation as a High-Value Untapped Commercial Opportunity

The rapid growth of female participation in surfing represents one of the most attractive commercial opportunities in the global surf apparel market. Historically, women’s surfwear was adapted from men’s designs with minimal structural changes, leaving performance and fit gaps. However, participation trends are changing significantly. The International Surfing Association has actively promoted gender equality in development programs, while the World Surf League offers equal prize money and strong media coverage for women’s competitions.

This visibility has increased interest among female athletes and recreational surfers. Brands such as Roxy have demonstrated that purpose-built, performance-driven women’s lines can command premium pricing and strong loyalty. Companies that invest in technically advanced, stylish, and athlete-endorsed women’s collections are well positioned to capture above-average growth in this expanding segment.

Sustainable and Recycled Material Innovation Unlocking Premium Product Positioning and Brand Differentiation

Sustainability-driven innovation is emerging as a powerful competitive advantage in the surf apparel industry. Consumers increasingly prefer products made from recycled or bio-based materials, aligning with surfing’s environmental values. Patagonia pioneered the use of recycled polyester and plant-based neoprene alternatives, setting new standards for responsible production. In response, brands such as Billabong have introduced limestone-based neoprene and Yulex natural rubber to reduce petroleum dependence and carbon emissions.

According to the Textile Exchange, the recycled fiber market is growing at nearly 20% annually, providing scalable supply chains for sustainable manufacturing. Certifications such as bluesign, OEKO-TEX, and Global Recycled Standard enhance brand credibility. Companies that achieve recognized sustainability standards are increasingly able to justify premium pricing and secure favorable retail positioning in competitive global markets.

Category-wise Analysis

Product Insights

The apparels segment dominates the global Surfing Apparel and Accessories market, accounting for nearly 68% of the total market share. Within this segment, wetsuits generate the highest average revenue per unit, while board shorts and surf tees contribute the highest sales volumes due to their affordability, lifestyle appeal, and year-round demand that is not limited to peak surf seasons.

Wetsuits are considered essential performance gear, particularly in temperate and cold-water surfing destinations such as California, Cornwall in the UK, Portugal, Japan, and Australia’s southern coastline, where thermal insulation is critical for extended sessions. According to the Surf Industry Manufacturers Association, apparel consistently represents the largest revenue category in the surf industry. This leadership reflects both the high purchase frequency of soft goods and the strong lifestyle premium that surf-inspired fashion commands beyond core surfing participation.

Material Insights

The Neoprene segment leads the global Surfing Apparel and Accessories market by material type, holding approximately 34% of total material share. This dominance is primarily due to neoprene’s essential role in wetsuit manufacturing, which remains the highest-priced product category in surf apparel. Neoprene offers an unmatched combination of thermal insulation, water resistance, buoyancy, and flexibility, making it highly suitable for the varying water temperatures surfers encounter worldwide.

Leading brands such as O'Neill, Billabong, and Rip Curl have heavily invested in improving neoprene formulations, including limestone-based and bio-derived alternatives that maintain performance while reducing environmental impact. At the same time, recycled materials are emerging as the fastest-growing material category, reflecting strong consumer demand for sustainable products and increasing brand commitments to environmentally responsible sourcing across the surf apparel value chain.

Distribution Channel Insights

The Offline distribution channel currently leads the global Surfing Apparel and Accessories market, accounting for approximately 56% of total sales. Physical retail outlets, including dedicated surf specialty stores, branded outlets, sporting goods chains, and beachfront boutiques, maintain strong relevance due to the technical nature of key products such as wetsuits.

These items require accurate fitting, thermal rating selection, and fabric assessment, which consumers prefer to evaluate in person. Established retailers such as Ron Jon Surf Shop and numerous independent coastal surf shops offer expert fitting services and personalized product guidance, resulting in higher conversion rates compared to purely online channels. However, the online channel is expanding rapidly as brands such as Quiksilver, Inc., Roxy, Inc., and Volcom, LLC invest in advanced digital commerce tools, including AI-driven size recommendations and immersive direct-to-consumer platforms.

End-user Insights

The Men segment leads the global Surfing Apparel and Accessories market, accounting for approximately 52% of total end-user share. Historically, men have represented the majority of active surfers worldwide, resulting in higher aggregate demand across both technical performance gear and lifestyle apparel categories. Core product lines such as wetsuits, board shorts, and surf tees targeted at male consumers form the primary revenue base for leading surf brands.

High-profile competitions, including the WSL Men's Championship Tour, provide strong athlete endorsement platforms that significantly influence brand perception and purchasing decisions. However, the Women segment is growing at a faster pace, supported by global initiatives promoting gender equality in surfing. The International Surfing Association has actively prioritized equal participation programs, contributing to rising female engagement in both recreational and competitive surfing and driving above-average growth in women’s surf apparel sales.

Regional Insights

North America Surfing Apparel and Accessories Trends

North America remains the leading regional market for surfing apparel and accessories, with the United States serving as its primary commercial hub. California continues to represent the cultural and economic center of global surf culture, hosting major brand headquarters including Quiksilver, Inc., Hurley, Inc., Volcom, LLC, RVCA, and REEF.

According to the Surf Industry Manufacturers Association, the U.S. surf industry generates billions in annual retail revenue, led by Southern California, Hawaii, and Florida. Hawaii, recognized as the birthplace of surfing, commands some of the highest per-capita surf apparel spending globally. Environmental regulations, particularly in California, are accelerating the shift toward sustainable textiles. Additionally, Canada’s Pacific coastline and the rise of inland surf simulation facilities are expanding the overall consumer base beyond traditional coastal markets.

Europe Surfing Apparel and Accessories Trends

Europe is the second-largest and a highly developed regional market for surfing apparel and accessories, supported by strong surf cultures in France, Spain, Portugal, and the United Kingdom. France’s Basque region, particularly Hossegor and Biarritz, is widely recognized as Europe’s surf capital and hosts major events such as the Quiksilver Pro France and Rip Curl Pro Search. Portugal’s Nazaré has gained global recognition for record-breaking big-wave surfing, strengthening its surf tourism economy.

The United Kingdom, especially Cornwall and Devon, sustains demand for cold-water wetsuits from brands like O'Neill and Billabong. EU regulatory frameworks, including REACH Regulation, enforce strict chemical compliance, encouraging sustainable material innovation and reinforcing Europe’s leadership in eco-certified surf apparel demand.

Asia Pacific Surfing Apparel and Accessories Trends

Asia Pacific is the fastest-growing regional market for surfing apparel and accessories, driven by expanding participation across Australia, Japan, Indonesia, the Philippines, India, and China. The sport’s inclusion in the Brisbane 2032 Olympic Games and multiple World Surf League events have significantly increased regional visibility. Australia remains the most mature market, with Surf Life Saving Australia reporting over 175,000 trained surf lifesavers, supporting strong domestic demand.

Indonesia, particularly Bali’s Uluwatu and G-Land, is both a global surf tourism hotspot and a growing consumer market. Japan demonstrates high brand loyalty and premium spending patterns, while China’s emerging surf culture, especially in Hainan Island, is supported by government sports initiatives. The region’s strong textile manufacturing base in China, Vietnam, and Bangladesh further enhances cost competitiveness for both domestic sales and global exports.

Competitive Landscape

The consolidation strategy of Boardriders, Inc., which brought multiple leading brands under one portfolio, has further strengthened market competition. Meanwhile, direct-to-consumer challengers and sustainability-focused brands are reshaping the mid-market landscape. Digital expansion and crossover athletic-lifestyle product development remain key strategic priorities influencing future competitive dynamics.

Key Developments:

- In February 2025: Billabong unveiled its enhanced Furnace wetsuit collection featuring advanced limestone neoprene and graphene-infused thermal lining to deliver superior warmth and flexibility. This upgrade targets premium cold-water surfing markets in Europe, Japan, and North America with performance improvements.

- In August 2024: Roxy, Inc. announced a multi-year extension as an official apparel partner for the World Surf League Women’s Championship Tour, reinforcing its commitment to elite women’s surf sponsorship and capitalizing on growing global competitive and Olympic-driven interest in female surfers.

- In April 2023: Volcom introduced a dedicated sustainable apparel line made with bluesig -certified recycled polyester and organic cotton, marking a notable step toward fully traceable, environmentally responsible sourcing and supply chain transparency among major surf lifestyle brands.

Companies Covered in Surfing Apparel and Accessories Market

- Billabong

- Hurley, Inc.

- O'Neill

- RVCA

- Volcom, LLC

- GLOBE INTERNATIONAL LIMITED

- REEF

- Roxy, Inc.

- Curl Ltd.

- Quiksilver, Inc.

- NSP International

- Katin

- Ananas Surf

- ThunderMonkey Surf Gear

- TianHao Sports

- Rip Curl

- Patagonia, Inc.

- Body Glove International

- Xcel Wetsuits

- Vissla

Frequently Asked Questions

The global Surfing Apparel and Accessories market is valued at US$ 9.8 Billion in 2026 and is projected to reach US$ 14.6 Billion by 2033, growing at a CAGR of 5.9% during the forecast period. Historical growth between 2020 and 2025 was recorded at a CAGR of 4.9%, driven by Olympic inclusion of surfing, rising global participation tracked by the International Surfing Association (ISA) across over 100 countries, and the pervasive integration of surf-inspired aesthetics into mainstream global athleisure and lifestyle fashion consumption.

The primary growth drivers are the landmark inclusion of surfing in the Olympic Games-including Tokyo 2020, Paris 2024, and confirmed Brisbane 2032-which has expanded global participation to an estimated 35 million surfers across 100+ countries per ISA data, and the deep integration of surf-inspired lifestyle fashion into mainstream athleisure culture. The Surf Industry Manufacturers Association (SIMA) confirms that lifestyle apparel revenues consistently exceed purely functional surf equipment categories, significantly amplifying total addressable market value beyond active participant spending alone.

The Apparels segment leads with approximately 68% market share, driven by the high average selling price of technical wetsuits-essential for surfers in temperate and cold-water destinations globally-and the extremely high unit volume of board shorts and surf tees that generate consistent lifestyle fashion demand independent of active surf participation. The Surf Industry Manufacturers Association (SIMA) has consistently confirmed apparel's dominant contribution to total surf industry retail revenues, reflecting both high purchase frequency and the substantial lifestyle premium generated by surf-branded fashion consumed by non-participating cultural consumers.

North America, led by the United States, is the dominant regional market, home to global surf brand headquarters including Quiksilver, Inc., Hurley, Inc., Volcom, LLC, and RVCA and generating the world's highest concentration of surf lifestyle consumer spending anchored in California, Hawaii, and Florida. The U.S. innovation ecosystem drives continuous wetsuit material advancement and sustainability certification adoption, while California's stringent environmental regulations and the Surf Industry Manufacturers Association (SIMA's) industry sustainability initiatives maintain the region's global leadership in responsible surf apparel manufacturing practices.

The most significant growth opportunity lies in the women's surf apparel segment, which is the fastest-growing end-user category driven by the ISA's gender equality participation development programs, the WSL Women's Championship Tour's equal prize money policy, and rising female surf engagement following Olympic inclusion. Brands capable of developing technically validated, purpose-built women's wetsuits and performance apparel-as demonstrated by Roxy, Inc.'s elite WSL sponsorship strategy-are positioned to capture premium-priced, high-loyalty consumer relationships with the global female surf participant community through 2033.