- Semiconductor Materials & Components

- Structured Cabling Market

Structured Cabling Market Size, Share, and Growth Forecast 2026 - 2033

Structured Cabling Market by Product Type (Copper Cables, Fiber Optic Cables, Others), Application (LAN, Data Centre), Vertical (Government, Industrial, IT & Telecommunication, Residential & Commercial, Others), and Regional Analysis for 2026 - 2033

Structured Cabling Market Size and Trend Analysis

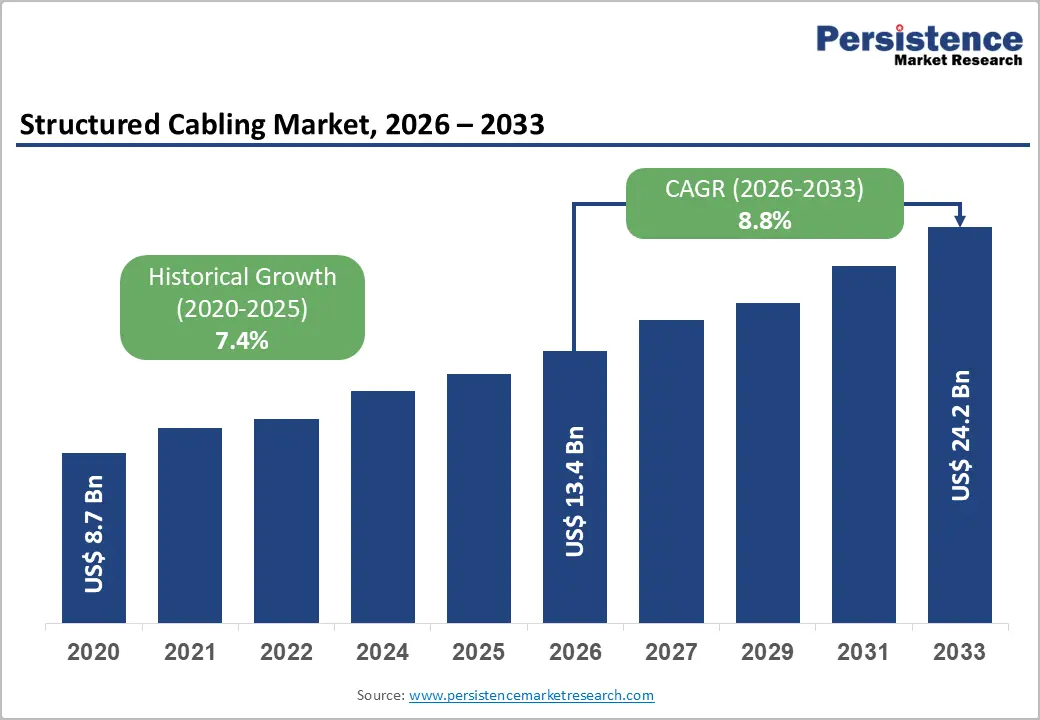

The global structured cabling market size is valued at US$ 13.4 billion in 2026 and is projected to reach US$ 24.2 billion by 2033, growing at a CAGR of 8.8% between 2026 and 2033.

The market expansion is primarily driven by the exponential rise in global data center investments, the accelerating deployment of 5G networks, and the growing adoption of cloud computing and Internet of Things (IoT) technologies across enterprise verticals. As organizations across sectors such as IT & Telecommunication, healthcare, BFSI, and government accelerate their digital transformation journeys, structured cabling infrastructure has emerged as the indispensable physical backbone that enables high-speed, low-latency, and highly reliable data transmission.

Key Industry Highlights:

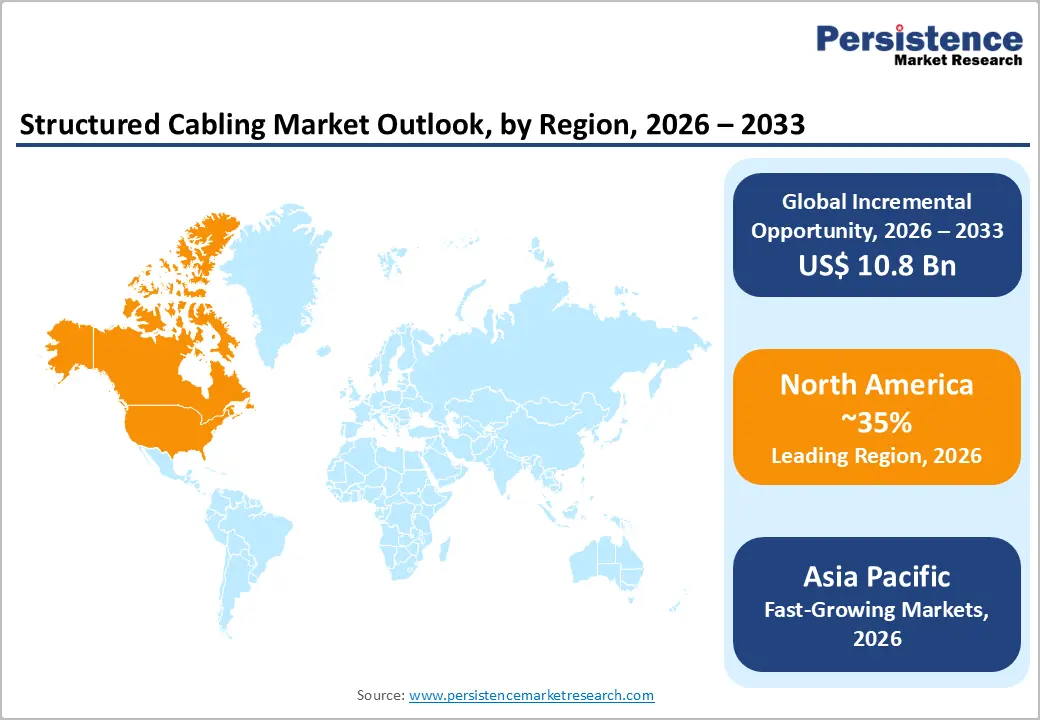

- Leading Region - North America dominates the global structured cabling market, holding approximately 34% revenue share, underpinned by hyperscale data center concentrations, robust enterprise IT spending, and the U.S. broadband infrastructure investment program, driving significant cabling upgrades.

- Fastest Growing Region - Asia Pacific is the fastest-growing structured cabling market, driven by China's New Infrastructure initiative, India's BharatNet program, and ASEAN data center investments, accounting for nearly 40% of new global data center deployments, generating sustained cabling demand.

- Dominant Segment - Copper Cables holds approximately 49% market share, driven by widespread Cat6A adoption in enterprise LAN environments, cost advantages over fiber in horizontal cabling, and Wi-Fi 6/6E backhaul requirements reinforcing continued copper infrastructure investments.

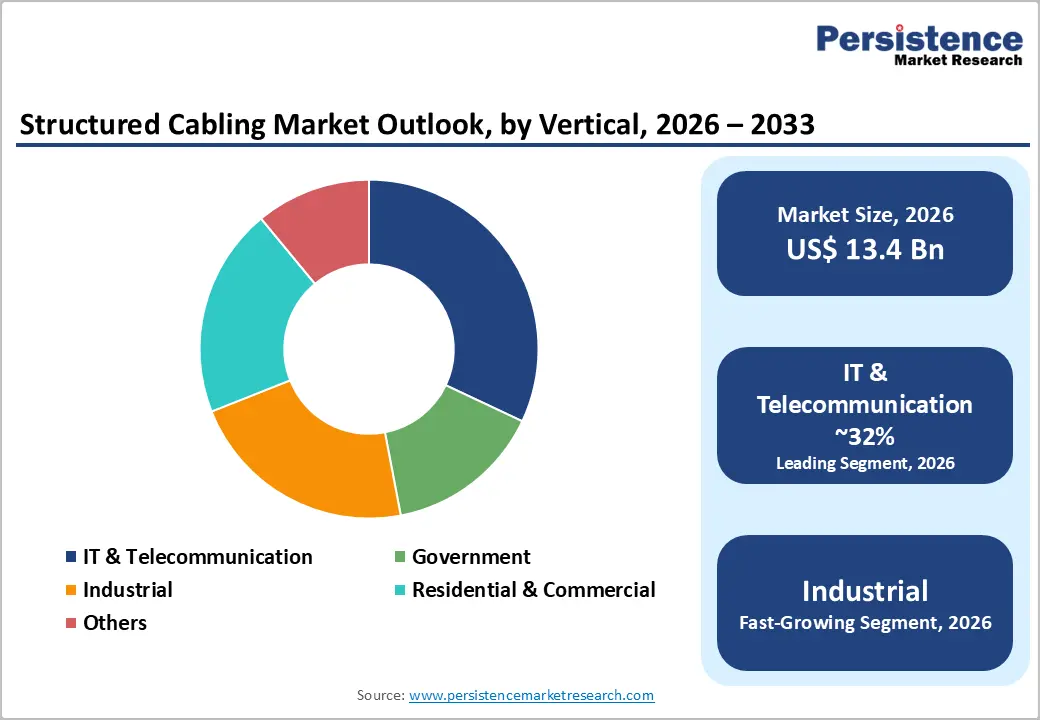

- Fastest Growing Segment- The IT & Telecommunication vertical is projected to grow at the fastest CAGR of approximately 9.7%, fueled by 5G network infrastructure expansion, cloud data center buildouts, and enterprise network modernization to support real-time analytics and automation workloads.

- Key Opportunity - The transition to AI workloads, requiring over 10x more fiber than traditional data centers, presents a transformational opportunity for high-density pre-terminated fiber solution providers, particularly as 800G and 1.6T optical interconnect deployments accelerate globally.

| Key Insights | Details |

|---|---|

| Structured Cabling Market Size (2026E) | US$ 13.4 Billion |

| Market Value Forecast (2033F) | US$ 24.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.8% |

| Historical Market Growth (2020-2025) | 7.4% CAGR |

DRO Analysis

Drivers - Surging Data Center Expansion and Hyperscale Infrastructure Investments

One of the most powerful growth catalysts for the structured cabling market is the unprecedented global expansion of data centers, particularly hyperscale and colocation facilities. According to the Telecommunications Industry Association (TIA), global data center construction spending surpassed US$ 400 Bn cumulatively over the 2021-2024 period, with demand intensifying further due to the rise of artificial intelligence workloads and real-time analytics.

In early 2025, Corning Incorporated released a guide, in collaboration with NVIDIA, indicating that AI-optimized data centers require over 10 times more fiber than conventional data centers, thereby amplifying demand for high-density fiber-optic structured cabling solutions. As hyperscale operators such as major cloud service providers continue to commission new facilities globally, structured cabling systems enabling seamless server-to-storage-to-network connectivity are witnessing sustained procurement.

Global Proliferation of 5G Networks and Smart Building Deployments

The worldwide rollout of 5G networks is a transformative driver of demand for structured cabling. As of 2024, over 40 countries had commercially launched 5G services, with densification of small cells and edge nodes requiring robust cabling backhaul infrastructure. According to the International Telecommunication Union (ITU), global mobile data traffic is projected to grow at a CAGR of approximately 20% through 2030, placing immense bandwidth demands on the physical cabling layer.

Simultaneously, the proliferation of smart buildings and Industry 4.0 facilities is requiring integrated cabling frameworks that support building automation systems, security, and environmental controls. The U.S. Department of Energy's smart building initiative estimates that over 5.9 million commercial buildings in the United States alone are candidates for structured network upgrades, creating a sustained, multi-year addressable market for cabling infrastructure providers.

Restraints - High Installation and Upgrade Costs Limiting SME Adoption

Despite robust macro-level demand, the high upfront costs of structured cabling installation, certification, and periodic upgrades remain a significant barrier to broader adoption, particularly among small and medium-sized enterprises. According to BICSI's industry analysis, properly certified structured cabling projects can cost between US$ 1,000 and US$ 5,000 per rack unit in enterprise data center environments, depending on cable category and density requirements.

The need for specialized installation professionals holding BICSI RCDD and related certifications further adds to project costs. For organizations in emerging markets operating on constrained capital budgets, the total cost of ownership for high-performance Cat6A or fiber-based infrastructure often results in deferred investments or adoption of lower-specification alternatives, thereby constraining market penetration in tier-2 and tier-3 cities.

Installation Complexity and Shortage of Skilled Professionals

The structured cabling sector faces a significant operational restraint: a persistent skilled labor shortage. According to a 2024 BICSI survey, approximately 70% of network outages were traced to physical-layer failures, often due to non-compliant or improperly installed cabling. As standards such as ANSI/TIA-568.2-E (revised in October 2024) impose increasingly stringent requirements around Power over Ethernet delivery, cable bundling, and performance verification, the demand for certified cabling technicians is outpacing supply.

This labor gap is particularly pronounced in rapidly developing markets across the Asia Pacific and Latin America, where digitalization investments are accelerating but trained workforce capacity lags, delaying project timelines and increasing rework costs, which negatively affect market velocity.

Opportunities - Accelerating Fiber Optic Adoption for AI-Ready and Next-Generation Data Centers

The transition to artificial intelligence-driven computing architectures presents a significant and immediate opportunity for fiber-optic structured cabling providers. Major hyperscale operators are actively investing in facilities capable of supporting 800G and, eventually, 1.6T optical interconnects, which require pre-terminated, high-density fiber solutions. In September 2025, Corning Incorporated unveiled a new line of high-density fiber-optic cables, specifically engineered to optimize rack space and improve data transmission speeds in AI data centers.

The Uptime Institute's 2024 Global Data Center Survey noted that fiber-based cabling deployments in new data center builds increased by over 27% year-on-year in 2024. With AI workloads doubling data center power and connectivity requirements, vendors offering modular, scalable, and rapid-deployment fiber solutions, such as pre-terminated trunk cables and high-density patch panels, are well positioned to capture a significant share of this expanding opportunity.

Smart City and Government Infrastructure Modernization Programs

Government-led smart city and digital infrastructure modernization programs globally represent a substantial growth opportunity for structured cabling market participants. In the United States, the Infrastructure Investment and Jobs Act allocated over US$ 65 Bn for broadband and telecommunications infrastructure expansion, a significant portion of which involves physical cabling upgrades in public buildings, transportation hubs, and municipal facilities.

In Europe, the European Commission's Digital Decade 2030 targets connectivity for all households, driving national cabling modernization projects. Across the Asia Pacific region, government initiatives such as India's BharatNet Phase III and China's New Infrastructure program are driving billions of dollars into structured cabling for rural broadband and urban smart city deployments. These programs create long-term, government-backed demand pipelines that offer cabling vendors stable, large-volume procurement opportunities with reduced revenue volatility.

Category-wise Analysis

Product Type Insights

Within the product type category, copper cables represent the leading segment, commanding approximately 49% of the overall market share. The dominance of copper cabling is sustained by its continued relevance in enterprise local area network deployments, where Category 6A (Cat6A) and Category 8 (Cat8) cables are widely used for short-to-medium-distance high-speed data transmission at substantially lower per-port costs than fiber-optic alternatives.

According to 2024 Belden Inc. pricing references cited by the TIA, Cat6A copper cable costs approximately US$ 0.80 per foot, versus US$ 2-5 per foot for fiber-optic solutions, making copper the economically preferred choice for floor-level horizontal cabling in commercial buildings and campuses. While fiber optic is gaining share in backbone and data center segments, copper maintains its primacy in horizontal structured cabling installations across enterprise verticals, including BFSI, education, and healthcare.

Application Insights

In terms of application, the Local Area Network (LAN) segment holds the dominant market share, accounting for approximately 81% of the total market. The overwhelming dominance of LAN applications reflects the widespread deployment of structured cabling in commercial office buildings, educational institutions, healthcare facilities, and enterprise campuses, where internal network connectivity is a foundational infrastructure requirement.

According to the Telecommunications Industry Association (TIA), over 92% of enterprise networks globally rely on standardized structured cabling, with LAN environments accounting for the bulk of annual port deployments. The rollout of Wi-Fi 6 and Wi-Fi 6E access points, which require Cat6A or higher copper cabling for backhaul, has further reinforced LAN segment demand as enterprises simultaneously upgrade their wireless and wired network infrastructure.

Vertical Insights

Among market verticals, the IT & Telecommunication sector holds the leading position, with a market share of approximately 32%. This vertical's dominance is driven by the sector's intensive reliance on high-performance, standardized cabling infrastructure to support cloud service delivery, enterprise networking, and telecommunications backbone operations. The ongoing proliferation of cloud computing, expansion of carrier-grade data center facilities, and deployment of next-generation 5G core networks have generated sustained demand for Cat6A copper and high-density single-mode fiber cabling systems within this vertical.

Notably, the IT & Telecommunication segment is also projected to register the fastest CAGR through 2033 at approximately 9.7%, reflecting continued capital expenditure by telecom operators upgrading network backbone and enterprise IT firms modernizing their digital infrastructure to support real-time analytics, automation, and hybrid cloud environments.

Regional Analysis

North America Structured Cabling Market Trends

North America is the dominant regional market for structured cabling, holding approximately 34% of global market revenue. The region's leadership is underpinned by its concentration of hyperscale data centers operated by major cloud service providers, extensive enterprise IT infrastructure, and one of the world's most active technology innovation ecosystems. The U.S. Infrastructure Investment and Jobs Act, which allocated US$ 65 Bn for broadband and telecommunications infrastructure, has further accelerated physical cabling investments across public sector buildings and last-mile broadband deployments.

In the United States, the structured cabling market continues to benefit from significant corporate real estate activity and ongoing data center construction across key hubs, including Northern Virginia, Phoenix, and Silicon Valley. In Q1 2025, CommScope secured a multi-million-dollar structured cabling contract for a major U.S. bank's nationwide branch modernization program, underscoring the robust demand from the financial services vertical. Canadian market demand is also growing, supported by government digital transformation programs and investments in smart city infrastructure in cities such as Toronto and Vancouver.

Asia Pacific Structured Cabling Market Trends

Asia Pacific is the fastest-growing regional market for structured cabling, driven by rapid industrialization, large-scale government-backed digital infrastructure programs, and significant private-sector investment in data centers and telecommunications. China leads the region in absolute investment volume, with the country's New Infrastructure initiative converting hundreds of billions of renminbi into 5G networks, data centers, and smart city deployments that collectively drive demand for structured cabling. Japan continues to invest heavily in network modernization and smart manufacturing as part of its Society 5.0 national strategy.

India is emerging as one of the most dynamic individual country markets within Asia Pacific, supported by the government's BharatNet Phase III broadband connectivity program and rapid enterprise IT expansion in cities such as Bengaluru, Hyderabad, and Pune. ASEAN nations, particularly Singapore, Indonesia, and Vietnam, are attracting significant data center foreign direct investment, driving structured cabling procurement across new hyperscale facility builds.

Europe Structured Cabling Market Trends

Europe is the second-largest regional market, with growth increasingly driven by the European Commission's Digital Decade 2030 policy framework, which mandates broadband connectivity for all EU households and sets ambitious targets for smart infrastructure deployment. Germany, the United Kingdom, France, and Spain are the primary contributors to regional demand, supported by large-scale enterprise cabling upgrades and the modernization of legacy telecom infrastructure.

Regulatory harmonization across the EU through CENELEC EN 50173 standards, which align with ISO/IEC 11801, is driving uniformity in cabling specifications across member states, simplifying large-scale multi-country deployments by multinational enterprises. The region's growing emphasis on green data centers and energy-efficient infrastructure is also creating demand for advanced low-loss fiber cabling solutions that reduce power consumption per bit transmitted. In November 2024, Nexans partnered with BIMobject to integrate its cabling products into Building Information Modeling (BIM) workflows, enabling early-stage structured cabling planning in new construction and renovation projects across European markets.

Competitive Landscape

The global structured cabling market exhibits a moderately consolidated structure, with a handful of multinational corporations commanding significant revenue share alongside a broader ecosystem of regional players and specialists. Leading global vendors, including CommScope, Corning Incorporated, Legrand SA, Belden Inc., and Nexans, compete primarily through portfolio breadth, innovation in fiber optic and high-density copper solutions, strategic acquisitions, and global service networks.

Key competitive differentiators include investment in proprietary standards-aligned product platforms, integration with Building Information Modelling (BIM) workflows, and development of end-to-end certified installation programs. Emerging trends include the integration of intelligent infrastructure management software with physical cabling systems, sustainability-focused product innovation such as lower-carbon cables and recyclable materials, and the development of modular pre-terminated cabling systems that reduce on-site labor requirements.

Key Developments:

- In January 2026, Vistance Networks completed its rebranding following the divestiture of Connectivity and Cable Solutions to Amphenol; ticker changed from COMM to VISN.

- In August 2025, Amphenol announced a USD 10.5 billion deal to acquire CommScope’s Connectivity and Cable Solutions business, expanding its data-center fiber offerings.

Companies Covered in Structured Cabling Market

- ABB Ltd

- Belden Inc.

- CommScope Holding Company, Inc.

- Corning Incorporated

- Furukawa Electric Co., Ltd.

- Legrand SA

- Nexans

- Schneider Electric

- Siemens AG

- TE Connectivity Ltd.

Frequently Asked Questions

The global Structured Cabling market is valued at US$ 13.4 Bn in 2026 and is projected to reach US$ 24.2 Bn by 2033, registering a forecast CAGR of 8.8%. The market recorded a historical CAGR of 7.4% between 2020 and 2025, supported by data centre expansion and rising enterprise network investments.

The primary demand drivers include the rapid global expansion of hyperscale and colocation data centers, the worldwide rollout of 5G networks requiring dense physical cabling backhaul, the proliferation of cloud computing and IoT devices, and growing enterprise investment in digital transformation and smart building infrastructure.

Copper Cables represent the leading segment with approximately 49% market share, driven by the widespread adoption of Cat6A and Cat8 cables in enterprise LAN environments. While fiber optic is gaining share in data centre backbone applications, copper remains dominant for horizontal cabling due to its cost efficiency and compatibility with PoE and Wi-Fi 6 backhaul applications.

North America leads the global structured cabling market with approximately 34% revenue share, driven by its high concentration of hyperscale data centers, robust enterprise IT infrastructure, strong adoption of advanced cabling standards such as ANSI/TIA-568.2-E, and significant government investments in broadband and telecommunications infrastructure under the U.S. Infrastructure Investment and Jobs Act.

The leading companies operating in the global structured cabling market include CommScope Holding Company, Inc., Corning Incorporated, Legrand SA, Belden Inc., Nexans, ABB Ltd, TE Connectivity Ltd., Schneider Electric, Siemens AG, Furukawa Electric Co., Ltd., Panduit Corp., and Siemon Company, among others.