- Semiconductor Materials & Components

- Integrated Passive Device Market

Integrated Passive Device Market Size, Share, and Growth Forecast, 2026 - 2033

Integrated Passive Device Market by Device Type (Inductors, Capacitors, Resistors, Filters, Others), Application (EMI / ESD Protection, RF Signal Processing, Signal Conditioning, Power Management, Others), Industry (Consumer Electronics, Automotive, IT & Telecom, Healthcare, Aerospace & Defense, Industrial, Others), and Regional Analysis for 2026 - 2033

Integrated Passive Device Market Size and Trends

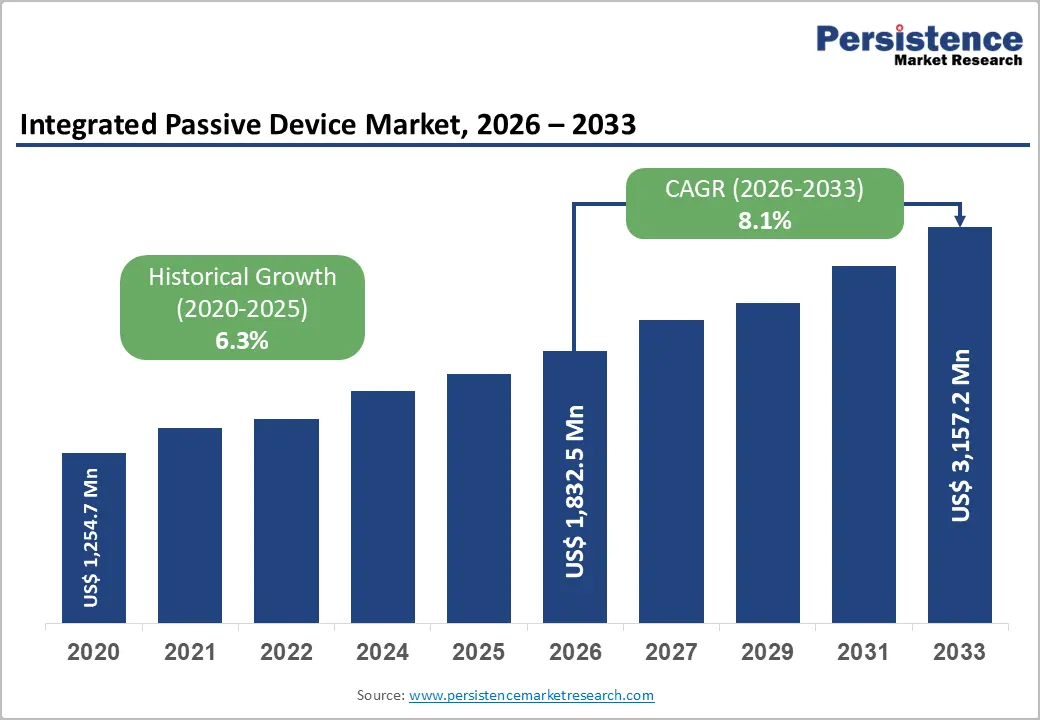

The global Integrated Passive Device (IPD) Market size is projected to rise from US$ 1,832.5 Mn in 2026 to US$ 3,157.2 Mn by 2033. It is anticipated that the market will grow at a CAGR of 8.1% from 2026 to 2033, driven by the rapid miniaturization of electronic components and the proliferation of high-performance consumer electronics.

Increasing integration of passive components into semiconductor substrates is enhancing efficiency and reducing footprint, particularly in advanced applications such as 5G infrastructure and automotive electronics. The surge in connected devices and IoT deployments is accelerating demand for compact, reliable, and high-frequency passive components, reinforcing long-term market expansion.

Key Industry Highlights:

- Leading Device Type: Resistors dominate with over 34% market share in 2026, valued at more than US$ 623.1 Mn, driven by their essential role in voltage regulation, signal conditioning, and integration compatibility in compact electronic designs. Inductors are the fastest-growing, driven by demand for power management, EMI suppression, and energy-efficient systems in automotive and industrial applications.

- Leading Application: EMI / ESD Protection holds over 45% market share in 2026, valued at more than US$ 824.6 Mn, fueled by increasing device miniaturization and regulatory compliance in automotive, medical, and consumer electronics. RF Signal Processing is the fastest-growing application, driven by 5G, Wi-Fi 6, and other advanced wireless communication technologies that require high-frequency, low-loss integrated solutions.

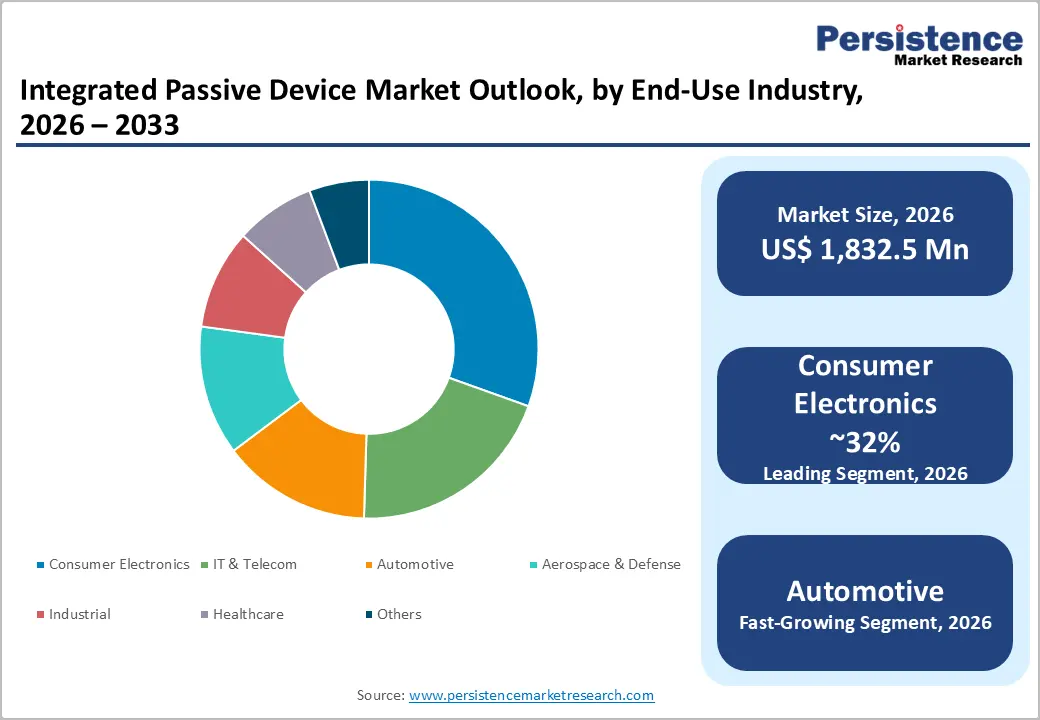

- Leading Industry: Consumer Electronics commands the largest market share at over 32% in 2026, valued at more than US$ 586.4 Mn, due to high demand for compact, multifunctional devices like smartphones, wearables, and smart home products. Automotive is the fastest-growing segment, with a 12.1% CAGR, supported by electrification, advanced ADAS systems, and EV powertrain integration.

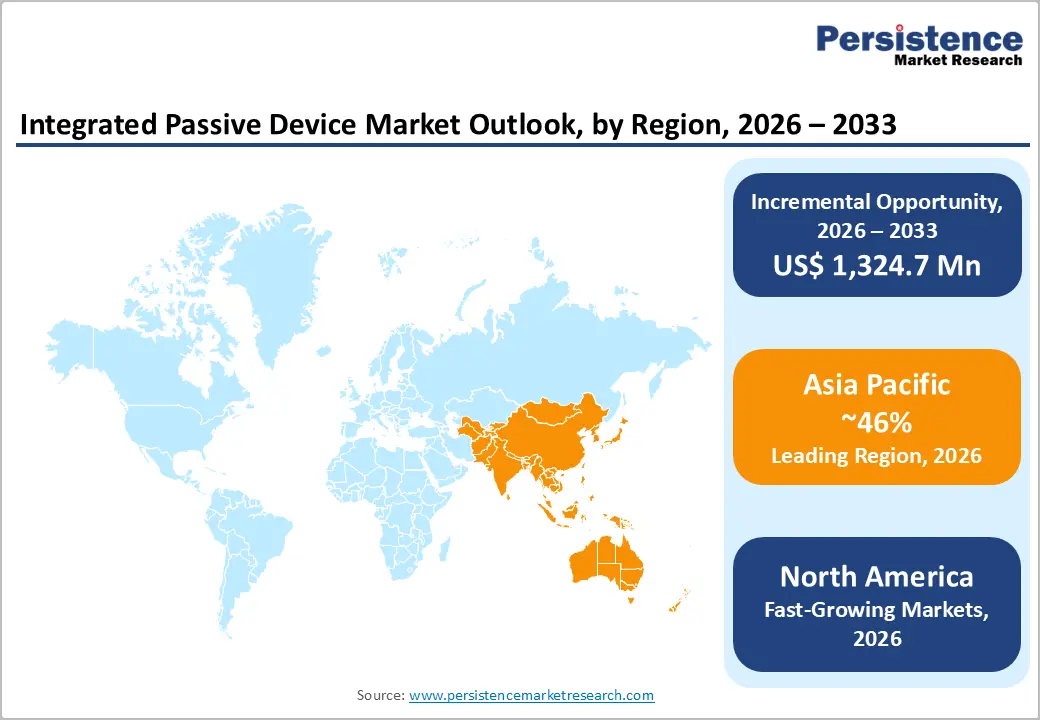

- Leading Region: Asia Pacific leads with over 46% share in 2026, valued at US$ 843 Mn, supported by China, Japan, South Korea, and Taiwan’s strong semiconductor ecosystem, 5G deployments, and government-backed initiatives. North America follows with 22% share, valued at US$ 403 Mn, driven by robust R&D, CHIPS Act funding, and consumer electronics and defense demand.

| Key Insights | Details |

|---|---|

|

Integrated Passive Device Market Size (2026E) |

US$ 1,832.5 Mn |

|

Market Value Forecast (2033F) |

US$ 3,157.2 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

8.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.3% |

Market Dynamics

Driver - Growing Trend of Compact and Efficient Electronic Designs

The global push toward smaller, lighter, and more energy-efficient electronic devices is a key factor for the Integrated Passive Device (IPD) market. In smartphones, wearables, tablets, and IoT modules, printed circuit boards (PCBs) are constrained by limited real estate, forcing designers to replace discrete passive components such as capacitors, inductors, and resistors with integrated passive devices (IPDs). For example, IPDs allow integration of LC filters, baluns, and matching networks onto a single silicon or glass substrate, reducing the number of surface-mount components, improving yield, and lowering assembly costs. According to a study, miniaturization and system-in-package (SiP) architectures could reduce component count by up to 30–40% in high-density RF modules, thereby accelerating the adoption of RF-integrated passive device solutions.

Surging 5G Network Deployments and RF Component Demand

With 5G subscriptions crossing 3.5 billion in 2026 and projected to grow further with mass-market adoption across North America, Asia Pacific, and Europe, demand for RF-integrated passive devices, including baluns, filters, and impedance matchers, is rising sharply. IPDs embedded in radio frequency front-end (RFFE) modules allow for miniaturized design with superior signal fidelity, reduced power loss, and lower PCB real estate. Companies have accelerated the development of silicon-based IPDs optimized specifically for sub-6 GHz and mmWave 5G applications, enabling more capable and compact smartphones, base stations, and connected devices globally.

Restraint - High Design Complexity and Long Development Cycles

Discrete passive components, which are readily sourced and swapped, require extensive upfront design effort tailored to specific circuit architectures, substrate types, and frequency requirements. This increases time-to-market, especially for smaller OEMs and startups that lack specialized semiconductor design expertise. The need for advanced photolithography-based fabrication and thin-film deposition further limits manufacturing to a handful of qualified foundries, creating supply constraints and inflexibility in scaling production rapidly to meet demand fluctuations.

Elevated Production Costs and Substrate Material Constraints

IPD manufacturing involves precision semiconductor fabrication processes on substrates such as silicon, glass wafer, or ceramic, all of which entail significant capital investments in cleanroom infrastructure and specialized equipment. Glass-based IPDs, while offering superior high-frequency performance due to low dielectric loss and thermal stability, are considerably more expensive to fabricate than silicon alternatives. The International Technology Roadmap for Semiconductors (ITRS) has noted that over 60% of high-performance IPDs utilize ceramic-based substrates, which carry elevated raw material and processing costs. These elevated production costs translate into higher unit prices, deterring cost-sensitive segments such as consumer IoT and mass-market electronics, limiting penetration in price-competitive product categories.

Opportunity - Next-Generation EMI/RFI Filtering in Automotive and Industrial Systems

Modern electric vehicles (EVs), industrial drives, and renewable-energy inverters generate high-frequency electromagnetic noise due to fast-switching power semiconductors, which disrupt onboard sensors, communication buses, and safety-critical control units. IPD-based EMI filters and common-mode chokes are integrated directly into DC-DC converters, on-board chargers (OBCs), and motor-control modules to suppress conducted and radiated emissions while occupying minimal board area. Automotive OEMs and Tier-1 suppliers are increasingly adopting IPD integrated filter modules certified to AEC-Q101 and CISPR 25 standards, which mandate strict EMI limits in vehicle cabins. For IPD vendors, this represents a structural opportunity to supply application-specific filter arrays tailored to EV powertrains, solar micro-inverters, and servo-drive control boards.

Miniaturized IPDs for Wearable and Implantable Medical Devices

Wearable ECG patches, continuous glucose monitors (CGMs), smart hearing aids, and IoT-enabled rehabilitation devices demand ultra-compact, low-power RF and sensor interfaces, where IPDs replace multiple discrete capacitors, inductors, and filters with a single miniaturized die. For example, IPD-based antenna-matching networks and noise-filtering circuits are critical in BLE-enabled patient monitors to ensure reliable wireless telemetry while minimizing form factor and battery drain. In the implantable segment, where pacemakers, neurostimulators, and RF-enabled bio-sensors must operate reliably for years inside the human body. IPD-integrated passive networks can be fabricated in biocompatible packages to provide EMI shielding, RF coupling and power management functions in sub-millimeter spaces, reducing the risk of signal distortion and device failure. Regulatory-driven RF-immunity standards, such as FDA-recognized AIM 7351731-type test protocols, are reinforcing the need for robust, integrated passive architectures in medical electronics.

Category-wise Analysis

Device Type Insights

Resistors dominate the market, capturing more than 34% market share in 2026 with a value exceeding US$ 623.1 Mn, due to their fundamental role in voltage regulation, current limiting, and signal conditioning across virtually all electronic circuits. The rising complexity of miniaturized electronic systems has increased the need for embedded resistors that ensure stability and reliability in compact designs. Their compatibility with semiconductor fabrication processes makes them ideal for integration within silicon-based IPDs. Their cost-effectiveness and scalability also support mass adoption in high-volume manufacturing environments.

Inductors are expected to grow rapidly as demand for efficient power management and noise filtering in advanced electronic systems increases. As devices become more compact and power-dense, integrated inductors help reduce electromagnetic interference and improve energy efficiency. Advancements in materials and fabrication techniques are enabling better integration of inductors within IPDs. The transition toward electric vehicles and renewable energy systems further amplifies their importance in power conversion and regulation circuits.

Application Insights

EMI/ESD Protection holds over 45% market share in 2026, with a value exceeding US$ 824.6 Mn, driven by the increasing sensitivity of modern electronic devices to electromagnetic interference and electrostatic discharge. As electronic components become smaller and more densely packed, the risk of signal disruption and damage rises significantly, necessitating robust protection mechanisms. IPDs offer integrated solutions that enhance circuit reliability while reducing footprint and cost. Regulatory requirements and quality standards in industries like automotive and healthcare also contribute to sustained growth.

RF Signal Processing is expected to grow significantly as wireless communication technologies such as 5G, Wi-Fi 6, and satellite systems expand rapidly. IPDs enable high-frequency signal handling with improved performance, reduced losses, and compact design, making them essential for RF front-end modules. The need for better signal integrity and reduced interference in high-speed communication systems is accelerating innovation in this segment.

Industry Insights

Consumer electronics command the largest share at over 32% in 2026, with a value exceeding US$ 586.4 Mn, driven by the massive demand for compact, high-performance, and multifunctional devices such as smartphones, tablets, wearables, and smart home products. The trend toward device miniaturization and increased functionality necessitates integrating passive components into smaller footprints, which IPDs effectively address. High production volumes and rapid product innovation cycles further reinforce this segment's dominance. Cost efficiency and improved performance make IPDs highly suitable for consumer electronics manufacturing.

The automotive industry is expected to grow at a CAGR of 12.1% due to the increasing electrification and digitalization of vehicles. Modern vehicles incorporate advanced electronic systems for safety, infotainment, connectivity, and power management, all of which require compact and reliable passive components. The shift toward electric vehicles and autonomous driving technologies significantly boosts demand for high-performance IPDs. These devices help optimize space, reduce weight, and enhance system efficiency in automotive electronics. Stringent reliability and durability requirements in automotive applications further drive the adoption of integrated passive solutions.

Regional Insights

North America Integrated Passive Device Market Trends

North America holds over 22% share in 2026, reaching US$ 403 Mn value. The region benefits from a robust semiconductor innovation ecosystem, significant federal investments, and strong demand from consumer electronics, defense, and automotive sectors. Programs such as the National Science Foundation’s SRC foster university-industry collaboration, producing advanced IPD prototypes for high-frequency applications. The CHIPS and Science Act, providing US 52.7 billion in funding, is accelerating domestic semiconductor R&D and manufacturing, boosting IPD production capacity. Major players continue to lead in R&D and IPD technology, consolidating regional dominance.

Asia Pacific Integrated Passive Device Market Trends

Asia Pacific holds over 46% share in 2026, reaching US$ 843 Mn value, fueled by the region’s dominant electronics ecosystem. China, Japan, South Korea, and Taiwan account for the majority of global IPD manufacturing capacity, with China’s Made in China 2025 policy targeting semiconductor self-sufficiency. South Korea’s K-Semiconductor Strategy plans KRW 510 trillion in semiconductor infrastructure by 2030. Japan hosts leading IPD manufacturers such as Murata, TDK, and Kyocera, dominating ceramic and silicon-based passive components. Emerging markets in ASEAN and India benefit from expanding consumer electronics production, accelerated 5G rollouts in over 100 Indian cities, and the PLI Scheme attracting global semiconductor investments.

Europe Integrated Passive Device Market Trends

Europe is expected to hold more than 17% share by 2026. Germany leads due to its automotive industry and the shift of OEMs like BMW, Volkswagen, and Mercedes-Benz toward electric and connected vehicles, requiring high-reliability IPDs for ADAS and battery management systems. The European Chips Act, aiming to double Europe’s semiconductor share to 20 percent by 2030, reinforces policy support for advanced electronics manufacturing. The United Kingdom and France also contribute through aerospace and defense demand, requiring certified, high-performance passive components. Key regional players drive technology adoption, supported by Europe’s push for 5G connectivity and industrial IoT applications.

Competitive Landscape

The global integrated passive device market is moderately consolidated, with a small number of vertically integrated semiconductor manufacturers controlling the majority of market revenues. Market leaders differentiate through proprietary substrate technologies, advanced thin-film fabrication processes, and close customer co-design relationships with OEMs. Competitive strategies include aggressive R&D investment, strategic acquisitions to expand technology capabilities, and geographic diversification of manufacturing. Emerging business models involve foundry partnerships where fabless IPD design houses collaborate with leading semiconductor foundries and the increasing customization of application-specific IPD.

Key Industry Developments:

- In November 2025, Murata Manufacturing Co., Ltd. launched a new integrated passive device (IPD) for the Semtech LoRa Connect SX126x family, replacing multiple discrete components with a compact 2.00mm x 1.25mm LTCC part. The LFB21892MDZ7F957 targets US/European ISM bands, while LFB21892MDZ7F821 is optimized for Eurocentric designs, enhancing both size and performance.

Companies Covered in Integrated Passive Device Market

- Murata Manufacturing Co., Ltd.

- Broadcom Inc.

- STMicroelectronics N.V.

- Skyworks Solutions, Inc.

- ON Semiconductor

- Qorvo, Inc.

- Infineon Technologies AG

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Analog Devices, Inc.

- Kyocera Corporation

- TDK Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Others

Frequently Asked Questions

The global integrated passive device market is projected to be valued at US$ 1,832.5 Mn in 2026.

The growing demand for miniaturized, energy-efficient electronic devices, where space constraints on printed circuit boards push designers to replace discrete passive components with compact, integrated solutions are key drivers of the market.

The integrated passive device market is expected to witness a CAGR of 8.1% from 2026 to 2033.

Next‑Generation EMI/RFI filtering & Miniaturized IPDs for wearable and implantable medical devices are creating strong growth opportunities.

Murata Manufacturing Co., Ltd., Broadcom Inc., STMicroelectronics N.V., Skyworks Solutions, Inc., ON Semiconductor, Qorvo, Inc., Infineon Technologies AG, Texas Instruments Incorporated, NXP Semiconductors N.V. are among the leading key players.