- Semiconductor Materials & Components

- Network Advisory Market

Network Advisory Market Size, Share, and Growth Forecast, 2026 – 2033

Network Advisory Market by Service Type (Network Consulting, Network Design, Spending Analysis, Others), Enterprise Size (SMEs, Large Enterprises), Industry Vertical (IT & Telecom, Retail, Manufacturing, Healthcare, Others), and Regional Analysis 2026 – 2033

Network Advisory Market Size and Trends Analysis

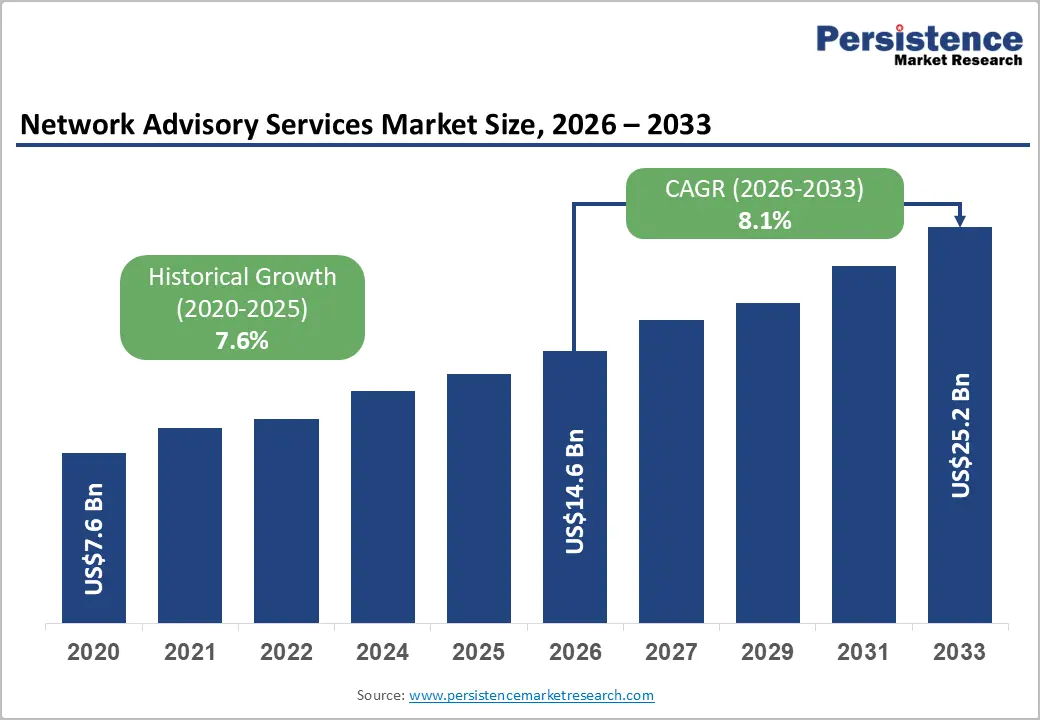

The global network advisory market size is likely to be valued at US$14.6 billion in 2026 and is expected to reach US$25.2 billion by 2033, growing at a CAGR of 8.1% during the forecast period from 2026 to 2033, driven by the increasing complexity of digital infrastructure, which is fueling demand for specialized planning and consulting services.

Organizations are placing greater emphasis on secure network architectures to support remote and hybrid operating models, accelerating the adoption of professional network design frameworks. Additionally, the need for reliable connectivity across geographically dispersed operations is reinforcing demand for robust network solutions. The expanding adoption of cloud technologies and IoT further amplifies the requirement for optimized, high-performance, and secure architectures, positioning the market for steady growth as enterprises continue to prioritize resilient infrastructure.

Key Industry Highlights:

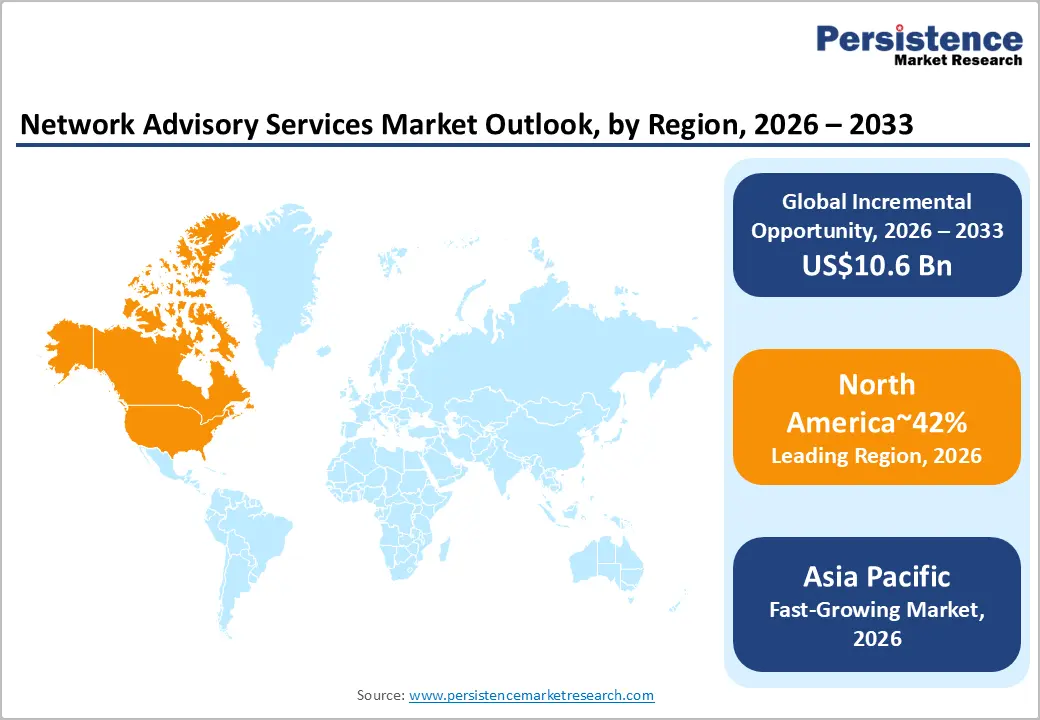

- Leading Region: North America is projected to lead, accounting for approximately 42% share in 2026, supported by a high concentration of technology vendors and rapid 5G deployment.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by accelerating digital infrastructure investments and massive industrial modernization projects.

- Leading Service Type: Network design is expected to lead, accounting for approximately 44% share in 2026, anchored by the necessity for foundational infrastructure modernization.

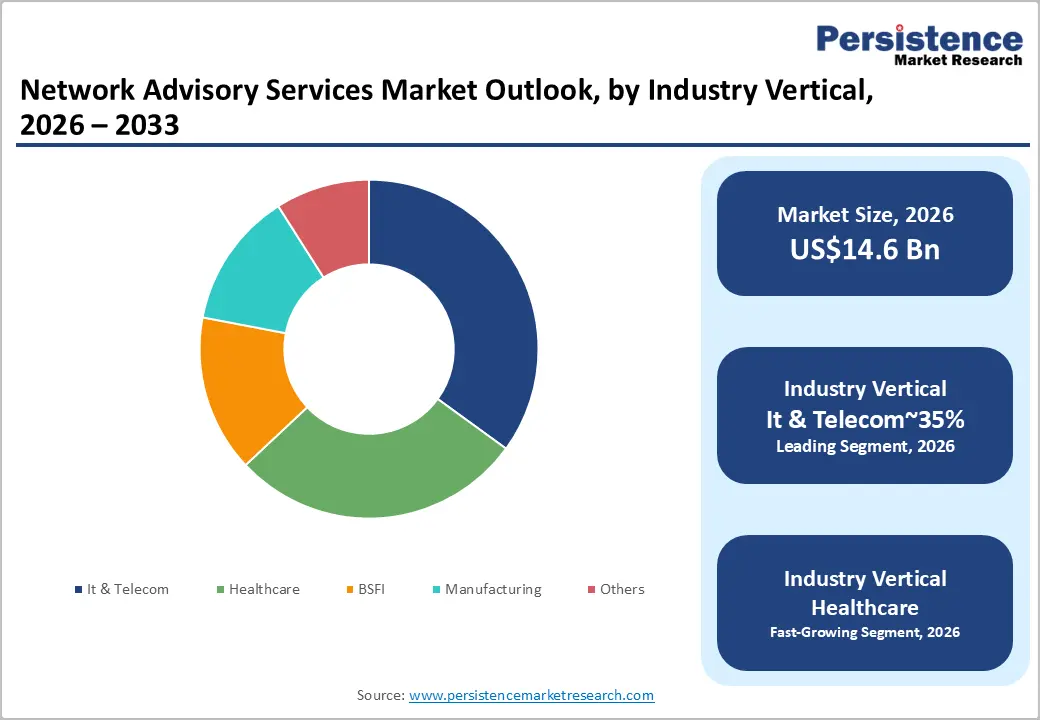

- Leading Industry Vertical: The IT & telecom segment is projected to dominate, holding approximately 35% share in 2026, driven by continuous network upgrades and edge computing expansion.

| Key Insights | Details |

|---|---|

| Network Advisory Market Size (2026E) | US$14.6 Bn |

| Market Value Forecast (2033F) | US$25.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

DRO Analysis

Driver Analysis – Accelerated 5G Industrial Integration

Industrial entities require robust connectivity to maintain high production uptime. Legacy wired systems are increasingly insufficient for modern automated factory floors. Wireless infrastructures offer the necessary flexibility for dynamic manufacturing processes. This requirement generates a steady demand for specialized network design advisory. Adoption remains anchored in operational resilience and lower maintenance costs. Efficient signal distribution remains a core priority for large-scale facilities.

Cisco, with Lifecycle Services, assists industrial clients with complex wireless transitions. This provision enables seamless integration of low-latency sensors into existing workflows. Nokia, with AVA Network Planning, facilitates precise spectrum allocation for private networks. These capabilities reduce interference risks in densely populated industrial environments. Such technical advancements are positioned to sustain high procurement rates. Improved connectivity supports the broader shift toward autonomous factory operations.

Cloud Migration Acceleration Driving Demand for Intelligent Network Advisory

Accelerated enterprise migration toward hybrid and multi-cloud environments is intensifying demand for advanced network advisory services. Distributed workload architectures require sophisticated integration frameworks to ensure seamless interoperability across fragmented infrastructure environments. Latency sensitivity across mission-critical applications is compelling organizations to prioritize network performance optimization capabilities. This transition is increasing reliance on intelligent monitoring systems that provide real-time visibility into data flows. These combined pressures are embedding network intelligence as a core requirement within digital transformation investment cycles.

Technology evolution in artificial intelligence-driven network optimization is redefining service delivery models across enterprise connectivity ecosystems. Advanced analytics platforms enable predictive traffic management and automated remediation of performance bottlenecks across distributed systems. Integration of intelligent campus and enterprise networking solutions is supporting adaptive infrastructure aligned with dynamic workload demands. Margin structures are increasingly influenced by value-added software capabilities embedded within network management platforms. This convergence of automation, intelligence, and infrastructure scalability is reinforcing sustained commercial momentum within network optimization markets.

Restraint Analysis – Legacy System Interoperability Constraints Limiting Network Modernization Momentum

Legacy hardware architectures remain structurally misaligned with emerging software-defined networking protocols across enterprise environments. This incompatibility generates operational friction during large-scale infrastructure transformation and integration initiatives. Organizations face challenges in embedding advanced advisory frameworks within rigid and fragmented legacy system configurations. Capital preservation priorities discourage replacement of still functional assets despite evident technological obsolescence risks. These constraints reshape cost structures by extending lifecycle management expenses and delaying efficiency gains from modernization. Regulatory and compliance requirements further complicate transitions where legacy systems remain embedded within critical operations.

Efforts to bridge interoperability gaps through cloud native and virtualized frameworks face limitations from entrenched system dependencies. Integration complexity increases implementation risk, particularly within environments requiring uninterrupted service continuity and data integrity assurance. Technology providers are adapting solutions to support hybrid compatibility, yet scalability remains constrained by foundational infrastructure rigidity. Vendor ecosystems are responding with modular and adaptive architectures, though full system transformation remains resource-intensive. Margin pressures emerge as service providers allocate additional resources to customization and integration support functions. This persistent friction continues to moderate near-term adoption of advanced network advisory and optimization solutions.

Skilled Talent Shortages Constraining Advanced Network Advisory Capacity

Limited availability of software specialists, defined networking, and network function virtualization restricts advisory scalability across enterprises. Rapid evolution of networking architectures is outpacing workforce development across core infrastructure and cloud integration domains. Organizations face challenges executing complex transformation strategies due to insufficient internal technical expertise and experience. Competition for skilled professionals increases consulting costs and extends implementation timelines across large-scale deployments. This talent imbalance constrains market penetration, particularly within emerging applications requiring specialized network design capabilities.

Service providers are expanding managed talent models to address persistent workforce constraints across enterprise networking ecosystems. Reliance on external consulting firms increases as organizations seek expertise for complex integration and optimization requirements. Integration complexity across hybrid environments further intensifies dependency on skilled architects and network engineers. Despite vendor initiatives, supply limitations continue to restrict project volumes and delay the adoption of advanced solutions. This structural workforce gap remains a key constraint shaping service delivery capacity and overall market expansion.

Opportunity Analysis – Sustainable Network Designs Driving Energy-Efficient Advisory Practices

Efficiency requirements are increasingly guiding advisory services toward low-power network architectures across 5G and cloud infrastructures. Enterprises are prioritizing green optimizations to achieve ESG compliance and reduce the total cost of ownership across deployments. Virtualization and software-defined technologies create avenues for energy reduction while maintaining performance across complex networks. Power-conscious network strategies influence capital allocation and long-term operational expenditure within enterprise and service provider ecosystems. These dynamics are reshaping value propositions, emphasizing environmental performance alongside reliability and scalability considerations.

Advanced network solutions integrate eco-efficient designs across core, edge, and campus environments to meet regulatory and market pressures. Cisco, with Provider Connectivity Assurance, and IBM, with Network Intelligence, embed sustainability monitoring within operational workflows. Huawei, with Xinghe solutions, enhances power efficiency across campus network deployments. Energy-aware network planning aligns technology evolution with organizational sustainability mandates, supporting optimized lifecycle performance. Such practices are reinforcing commercial value for providers offering integrated, low-impact network design and management services.

AI Native Network Automation Expanding Advisory Value Creation Potential

Artificial intelligence integration is redefining network monitoring and management across enterprise infrastructure environments. AIOps platforms enable proactive fault detection and automated traffic optimization across distributed network segments. This capability enhances operational reliability while reducing dependence on manual intervention and reactive maintenance processes. Automation-driven architectures are reshaping cost structures by lowering error rates and improving system efficiency. This transition is creating new revenue streams for service providers offering predictive and intelligent network management solutions.

Evolution in data analytics and automation is elevating expectations for real-time visibility into network performance. Advanced platforms support adaptive optimization, enabling continuous improvement across dynamic and multi-layer infrastructure environments. Integration of intelligent systems reduces operational complexity while strengthening service consistency across enterprise deployments. Procurement strategies increasingly favor solutions that embed automation within core network management capabilities. These dynamics are supporting margin expansion for vendors delivering specialized, high-value advisory and automation services.

Category–wise Analysis

Service Type Insights

Network design is expected to lead, accounting for approximately 44% share in 2026, reinforced by foundational infrastructure modernization needs. High-performance connectivity requires meticulous structural planning to avoid future operational bottlenecks. Enterprises prioritize scalable architectures that can accommodate rapid data volume increases.

Cisco with Lifecycle Services provides the necessary blueprints for these high-capacity environments. Nokia, with AVA Network Planning, further supports the creation of resilient wireless networks. These design services ensure that digital assets remain accessible and secure. Adoption remains anchored in the necessity for long-term technological future-proofing. This focus on structural integrity sustains the segment's dominant market position.

Network Deployment/Design is anticipated to be the fastest-growing segment, driven by the immediate need for rapid infrastructure implementation. Accelerating digital transformation cycles requires shorter intervals between planning and active operation. Organizations are seeking integrated solutions that combine advisory with hands-on execution. Accenture, with Cloud First Network, facilitates this accelerated transition for global enterprises.

IBM with Hybrid Cloud Network Services streamlines the rollout of complex multi-cloud architectures. This trend reflects a broader shift toward agile and responsive networking models. This momentum positions the segment for superior growth relative to traditional consulting.

Industry Vertical Insights

The IT & telecom segment is expected to lead, accounting for approximately 35% share in 2026, anchored by constant infrastructure upgrade cycles. Telecommunication providers must continuously modernize their networks to support rising bandwidth demands. This vertical remains the primary driver of innovation in global networking protocols. Ericsson, with Managed Services Platform, supports operators in optimizing their vast wireless estates. Lumen with Network Consulting Services assists in the management of high-speed fiber backbones.

Reliability and speed are non-negotiable requirements for participants in this sector. Consistent investment in 5G and fiber networks sustains high advisory volumes. This technical leadership ensures the segment remains the largest vertical contributor.

The healthcare segment is anticipated to be the fastest-growing segment, driven by the rapid expansion of digital health and telemedicine. Medical facilities require secure and ultra-reliable connectivity to transmit sensitive patient data. The shift toward remote monitoring increases the number of connected edge devices. Dell with Edge Network Advisory addresses the specific latency needs of medical environments. Orange with Open Tech Network Services provides the secure frameworks necessary for regulatory compliance. Digitalization of health records necessitates robust and redundant network architectures. As healthcare providers modernize their facilities, specialized network advisory becomes a priority.

Regional Insights

North America Network Advisory Market Trends

North America is expected to remain the leading regional market, accounting for approximately 42% share in 2026, supported by high technology density and advanced 5G networks. The region serves as a global hub for networking innovation and major software providers. Enterprises here are early adopters of software-defined architectures and AI-driven management tools. This proactive stance toward technology sustains a high volume of advisory engagements.

High labor costs also drive the demand for automated network optimization solutions. Policy alignment toward secure and domestic supply chains further influences procurement strategies. Regional dominance is anchored in the continuous modernization of established industrial and financial sectors.

The U.S. is expected to anchor regional momentum through significant investments in national digital infrastructure and high-speed connectivity. Federal initiatives aimed at expanding broadband access are generating extensive requirements for network design. Cisco with Lifecycle Services remains a primary choice for American enterprises seeking resilient architectures. Regulatory focus on cybersecurity standards is compelling organizations to seek professional advice for compliance.

Domestic firms are prioritizing the integration of edge computing to support autonomous manufacturing hubs. This investment environment positions the country as the central driver of North American growth. Strategic focus on technological sovereignty continues to bolster the local advisory market.

Asia Pacific Network Advisory Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid urbanization and industrial expansion accelerate market participation. Regional governments are prioritizing digital connectivity as a foundation for economic development. Massive investments in smart cities and high-tech manufacturing hubs generate diverse networking needs. This dynamic environment attracts global advisory firms seeking to support large-scale projects. Adoption of mobile-first business models increases the demand for robust wireless architectures.

Cost-driven adoption of cloud services further stimulates the need for professional network planning. The region's expansion is characterized by the leapfrogging of traditional legacy systems.

China is anticipated to drive regional acceleration through massive state-led investments in 5G and industrial internet platforms. National strategies focusing on digital self-reliance are fostering a robust domestic networking ecosystem. Nokia, with AVA Network Planning, facilitates the expansion of critical infrastructure across diverse provinces. Regulatory frameworks emphasizing data security are increasing the necessity for localized advisory expertise.

Large-scale manufacturing facilities are adopting private networks to enhance operational efficiency and control. This concentration of industrial activity sustains a high demand for specialized design services. Significant capital flows into the technology sector reinforce the nation's pivotal market role.

Europe Network Advisory Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in compliance and security upgrades. Stringent data privacy regulations, such as GDPR, necessitate highly secure and transparent network architectures.

Organizations are focused on reconciling legacy systems with modern sovereign cloud requirements. This regulatory pressure sustains steady procurement of network consulting and design services. The region also emphasizes environmental sustainability, driving demand for green networking advisory. Mature industrial sectors such as automotive and aerospace continue to invest in reliable connectivity. Consistent service-led demand ensures the market remains resilient against economic fluctuations.

Germany sustains momentum via regulatory reforms that incentivize network investments in electricity and telecom. Bundesnetzagentur determinations simplify cost frameworks, accelerating broadband and fiber advisory needs. Fujitsu, with AI-powered networks, gains from efficiency-focused strategies in underserved areas. Policy shifts toward digital autonomy elevate procurement in infrastructure hubs.

Competitive Landscape

The network advisory market is characterized by a moderately fragmented structure, where global technology giants and specialized consulting firms coexist. This fragmentation is justified by the diverse technical requirements across different industry verticals and geographic regions. Leading players exert significant functional influence by defining the standards for network security and performance. Their extensive technology footprints allow them to offer integrated solutions that smaller competitors cannot easily replicate. Cisco with Lifecycle Services, Accenture with Cloud First Network, and IBM with Hybrid Cloud Network Services serve as industry benchmarks for comprehensive advisory. Procurement relationships are often built on long-term trust and proven reliability in mission-critical environments. These established vendors leverage deep research and development capabilities to maintain high brand equity.

Competitive positioning emphasizes vertical differentiation, with premium players pursuing AI-centric platforms and value-oriented ones focusing on cloud migrations. Huawei, with Xinghe AI Campus and Fujitsu AI networks, contrasts tier strategies via intelligent campus solutions. M&A trends consolidate capabilities, partnerships evolve ecosystems, and platform updates target automation. Intensity heads toward AI specialization, where agentic archetypes gain ground in complex environments.

Key Industry Developments:

- In March 2026, Ericsson and Nokia announced a landmark collaboration to advance intelligent automation across Open RAN and cloud networks. This partnership allows cross-ecosystem integration of automation applications (rApps), significantly reducing vendor lock-in and accelerating the transition toward self-managing autonomous networks.

- In January 2026, Cisco prioritized its corporate strategy around AI-ready infrastructure and digital resilience. By unveiling AI Pods and the "Hypershield" fabric in collaboration with Nvidia, Cisco is positioning its advisory services to lead the "AI transformation" for enterprise data centers.

Frequently Asked Questions

The network advisory market is valued at US$14.6 billion in 2026 and is projected to reach US$25.2 billion by 2033, driven by rising demand for advisory services supporting digital transformation initiatives.

Cloud and 5G complexities drive procurement for optimized designs. AI tools address performance needs across enterprises. This sustains expansion.

The network advisory market is expected to grow at a CAGR of 8.1% from 2026 to 2033, supported by ongoing infrastructure modernization and accelerating adoption across key industry verticals.

North America is projected to lead the network advisory market, accounting for approximately 42% of the total share in 2026, supported by its mature technology ecosystem and strong presence of established vendors.

Key players in the network advisory market include major technology providers such as IBM (with Network Intelligence), Cisco (with Crosswork), and HPE Aruba, which lead in technology-driven advisory services. Emerging contributors such as Huawei (with Xinghe) and Fujitsu (focused on AI-enabled networks) are also strengthening their presence. Additionally, expert consulting firms such as GLG play a key role by providing specialized insights and advisory support.