- Non-food Packaging

- Steel Drums & IBCs Market

Steel Drums & IBCs Market Size, Share, and Growth Forecast, 2026 - 2033

Steel Drums & IBCs Market by Product Type (Tight-Head Steel Drums, Steel IBCs, Others), End-Use Industry (Chemicals, Food & Beverages, Others), Content Type, and Regional Analysis for 2026 - 2033

Steel Drums & IBCs Market Size and Trends Analysis

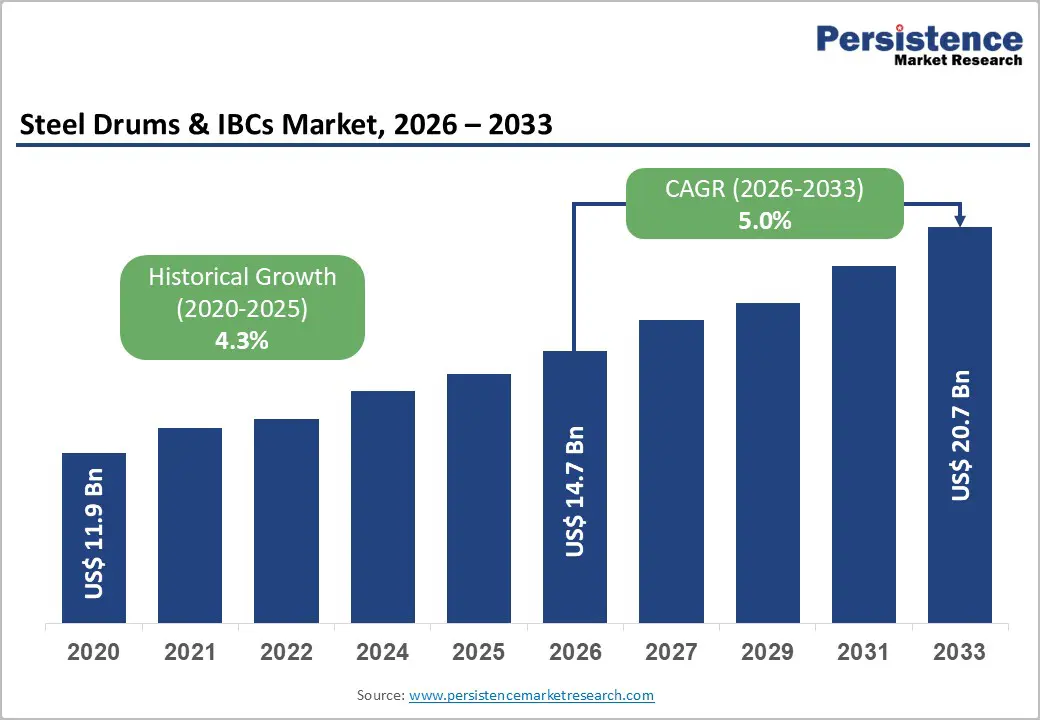

The global steel drums & IBCs market size is likely to be valued at US$14.7 billion in 2026 and is expected to reach US$20.7 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033, driven by sustained expansion in the chemical sector, tightening hazardous-goods transport regulations, and the increasing adoption of reusable and reconditioned metal containers. Industrial output growth in Asia Pacific and compliance-driven replacement cycles in North America and Europe will reinforce both volume expansion and gradual product premiumization over the forecast period.

Metal drums and steel IBCs remain integral to global bulk logistics because they combine structural integrity, stacking efficiency, chemical compatibility, and long service life. As industrial supply chains prioritize safety, traceability, and sustainability, steel packaging formats continue to demonstrate strong lifecycle economics compared with certain single-use alternatives.

Key Industry Highlights

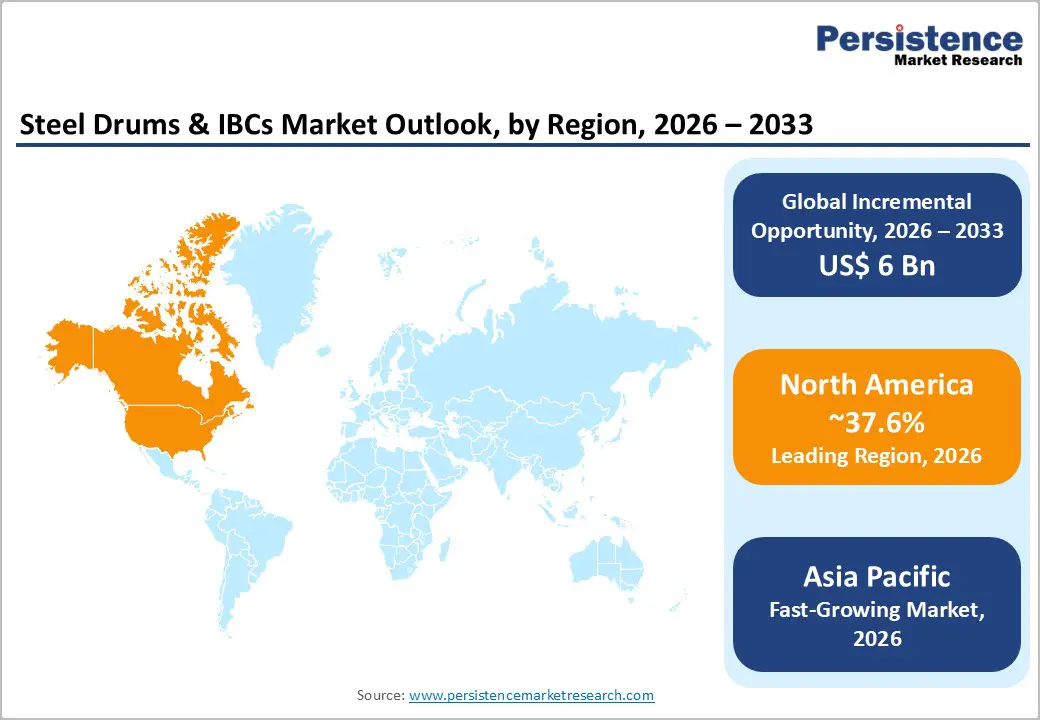

- Leading Region: North America is projected to lead the market, accounting for approximately 37.6% of revenue share, supported by its extensive petrochemical infrastructure and strong regulatory enforcement framework.

- Fastest-growing Region: Asia Pacific represents the fastest-growing region, driven by expanding chemical production in China, India, and ASEAN economies, along with rising export-oriented manufacturing activity.

- Investment Plans: Industry participants are investing in automated forming lines, advanced coating and lining technologies, reconditioning infrastructure, and digital asset tracking systems to enhance compliance, traceability, and operational efficiency across regions.

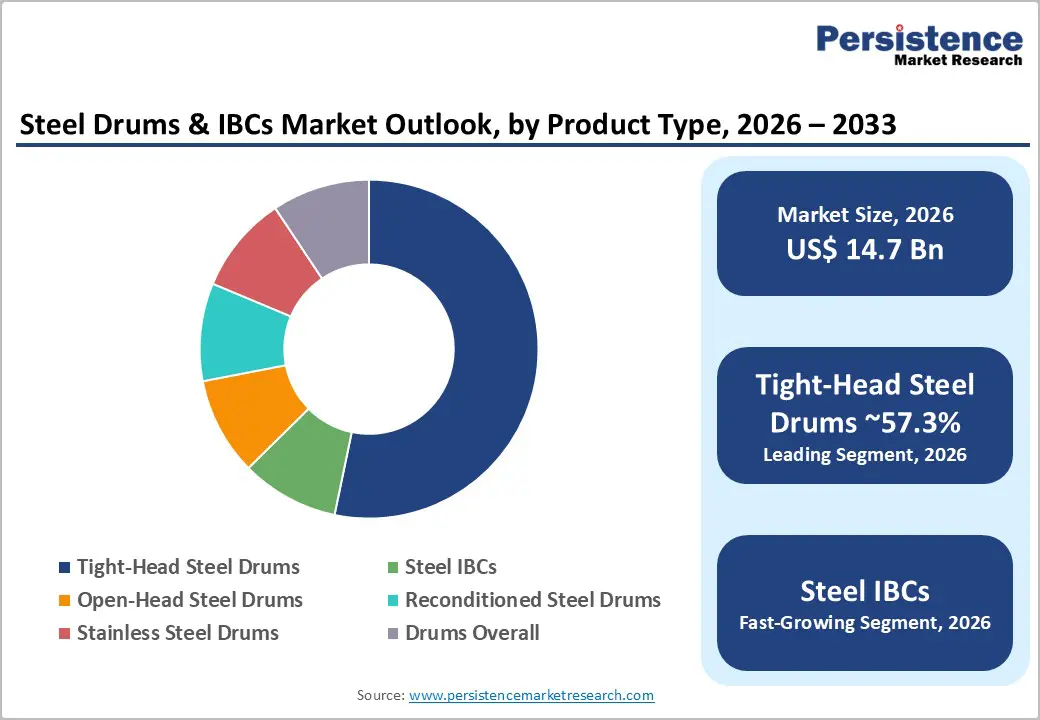

- Dominant Product Type: Tight-head steel drums are anticipated to hold approximately 57.3% market share, maintaining dominance due to their sealed design, global dimensional standardization, and strong compatibility with liquid chemicals.

- Leading End-use Industry: The chemicals sector is estimated to account for approximately 50.8% of revenue, supported by recurring procurement cycles and stringent hazardous-material compliance requirements.

| Key Insights | Details |

|---|---|

| Steel Drums & IBCs Market Size (2026E) | US$14.7 Bn |

| Market Value Forecast (2033F) | US$20.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Tightening for Hazardous Goods Transport

International and domestic regulations governing the transport of dangerous goods continue to reinforce demand for certified steel drums and IBCs. Regulatory frameworks such as UN Recommendations on the Transport of Dangerous Goods and ADR standards establish rigorous performance testing, design approval, periodic inspection, and lifecycle requirements for packaging used in hazardous cargo flows. Steel containers, particularly tight-head drums and metal IBCs, consistently meet these structural and pressure-resistance criteria. Compliance obligations increase the cost of non-certified packaging and strengthen procurement of approved metal formats. In the chemical, petroleum, and specialty materials sectors, regulatory adherence directly influences packaging selection. As hazardous goods volumes expand globally, compliance-driven replacement and certification cycles create recurring revenue streams for steel drum and IBC manufacturers.

End-Market Demand from Chemicals and Industrial Manufacturing

The global chemical industry remains the largest consumer of steel drums and IBCs. Continuous manufacturing models require recurring bulk transportation of intermediates, additives, resins, solvents, and specialty formulations. Steel packaging offers durability, compatibility with aggressive substances, and secure sealing for export and domestic transport. Even moderate growth in chemical output produces disproportionate packaging demand due to high turnover frequency and mandatory packaging specifications for regulated materials. Industrial sectors such as coatings, lubricants, construction chemicals, and specialty materials further contribute to steady demand. As supply chains stabilize and manufacturing investments increase across Asia Pacific and North America, steel drums and IBC volumes benefit from sustained industrial production cycles.

Raw Material Dynamics and Lifecycle Economics

Steel pricing and availability influence production economics across the industry. Fluctuations in crude steel output, scrap pricing, and energy costs affect manufacturing margins and procurement strategies. During periods of price stability, producers invest in automation, lining technologies, and value-added product enhancements. When steel input costs rise sharply, customers reassess lifecycle cost structures. Reconditioning and reuse programs become more attractive, reducing the total cost of ownership over multiple filling cycles. This dynamic reinforces long-term demand for durable metal containers capable of withstanding repeated inspection and refurbishment. The ability to extend asset life through certified reconditioning differentiates steel packaging from certain disposable alternatives.

Barrier Analysis - Price Sensitivity and Substitute Materials

Steel drums and metal IBCs often involve higher upfront costs compared with plastic or composite containers in non-hazardous applications. Buyers operating in cost-sensitive segments evaluate packaging based on immediate capital expenditure rather than lifecycle value. When steel prices increase more than 10% year-over-year, margin compression can occur unless manufacturers successfully pass through cost adjustments. In less regulated segments, substitution toward plastic drums or composite IBCs may temporarily accelerate. This price sensitivity constrains premium expansion in commoditized applications.

Fragmented Reconditioning Infrastructure

Reconditioning services vary significantly in quality and regulatory compliance across regions. Inconsistent inspection protocols and documentation standards can introduce risk for chemical and pharmaceutical buyers. Many industrial customers require internal inspection pass rates exceeding 95% before approving refurbished drums for reuse. Regions with fragmented service networks face higher audit and compliance costs. Without standardized quality assurance systems, reconditioning adoption may be limited despite strong sustainability benefits.

Opportunity Analysis - Certified Circular Economy and Reconditioning Services

The expansion of structured return-and-reuse programs presents a major growth avenue. Certified reconditioning, supported by digital traceability and documented inspection protocols, aligns with corporate sustainability targets and Scope 3 emissions reduction goals. Strategically located reconditioning hubs near chemical clusters can reduce transportation costs and shorten turnaround cycles. By offering inspection, relining, refurbishment, and asset tracking services under warranty-backed programs, manufacturers can create recurring revenue streams while reducing raw material exposure. Over two to three reuse cycles, lifecycle cost parity with single-use alternatives becomes achievable, strengthening long-term customer retention.

Advanced Product Innovation and Telemetry-Enabled IBCs

Steel IBCs equipped with corrosion-resistant linings, stainless steel components, and integrated monitoring systems address higher-value industrial segments. Sensor-enabled IBCs capable of tracking temperature, pressure, and fill levels provide risk mitigation for sensitive chemical and food-grade products. Integration of telemetry with logistics software supports improved supply chain transparency and asset utilization. Suppliers that position steel IBCs as intelligent logistics assets rather than passive containers can command premium pricing and secure long-term supply contracts in pharmaceutical and specialty chemical sectors.

Category-wise Analysis

Product Type Insight

Tight-head steel drums are anticipated to account for approximately 57.3% of the market share in 2026, maintaining their position as the dominant product category. Their widespread adoption stems from strong compatibility with liquid chemicals, hermetically sealed closures that prevent leakage and vapor emissions, and efficient stacking capabilities that optimize warehouse and container utilization. Global dimensional standardization, including 55-gallon (200-liter) formats, enables seamless integration into international shipping and handling systems. Industries such as petrochemicals, agrochemicals, and specialty chemical manufacturing rely heavily on tight-head drums for transporting solvents, resins, lubricants, and petroleum derivatives. For example, bulk shipments of methanol, industrial solvents, and base oils commonly use sealed steel drums to meet hazardous material compliance requirements. High-volume manufacturing and established reconditioning networks reduce lifecycle costs, reinforcing their dominance.

Steel Intermediate Bulk Containers (IBCs) are projected to expand, making them the fastest-growing product segment. Their palletized, forklift-compatible design enhances operational efficiency by reducing manual handling and lowering per-liter transportation costs. Compared to traditional drums, IBCs offer higher volumetric capacity, typically ranging from 800 to 1,000 liters, which supports bulk consolidation strategies. Large chemical producers and industrial distributors increasingly adopt steel IBCs for centralized warehousing and long-distance exports. For instance, multinational chemical companies shipping specialty additives or high-value intermediates across regions favor reusable steel IBC systems integrated with tracking and return logistics. Lifecycle management programs, including leasing, inspection, and refurbishment services, further strengthen adoption rates. As industrial consolidation drives larger shipment sizes and just-in-time supply chains, steel IBCs provide scalable and reusable logistics solutions that align with cost optimization and sustainability goals.

End-use Industry Insights

The chemicals sector is anticipated to account for approximately 50.8% of the market share in 2026. Continuous and batch processing facilities require reliable packaging formats for solvents, specialty chemicals, catalysts, and industrial intermediates. Steel packaging solutions ensure structural integrity under high-weight loads and maintain chemical compatibility for hazardous substances. Regulatory compliance remains a decisive factor in this segment. United Nations (UN) certification standards for dangerous goods transport reinforce demand for high-strength steel drums and IBCs. For example, exports of flammable solvents and corrosive acids often mandate UN-rated packaging to comply with international shipping regulations. Recurring procurement cycles from chemical manufacturers create stable demand, positioning this sector as the backbone of the steel industrial packaging market.

Food and beverage applications are projected to grow, representing the fastest-expanding end-use segment. Rising global trade in edible oils, corn syrups, flavor concentrates, and liquid sweeteners increases demand for hygienic, internally lined steel containers. Manufacturers supplying food-grade epoxy-lined drums and corrosion-resistant steel IBCs benefit from stricter traceability requirements and quality certifications such as HACCP compliance. For instance, bulk exports of palm oil, glucose syrups, and beverage concentrates frequently use coated steel drums to prevent contamination and preserve product integrity. Enhanced cleaning validation protocols and tamper-evident sealing systems support premium pricing within this segment. As food ingredient globalization accelerates, steel packaging providers with certified sanitation and compliance capabilities are well positioned to capture higher-margin contracts.

Regional Insights

North America Steel Drums & IBCs Market Trends - Gulf Coast Petrochemical Scale Driving High-Spec Steel Packaging Demand

North America is projected to account for approximately 37.6% of market share in 2026, supported primarily by the extensive petrochemical, refining, and specialty chemical base concentrated in the U.S. along the Gulf Coast. States such as Texas and Louisiana host large-scale production facilities operated by companies including ExxonMobil and Dow, which generate sustained demand for UN-certified steel drums and IBCs for solvents, resins, and industrial intermediates. Strict enforcement of hazardous materials transportation standards under U.S. Department of Transportation regulations reinforces the use of high-specification steel packaging solutions.

The region also benefits from a mature reconditioning ecosystem. Companies such as Greif and Mauser Packaging Solutions operate extensive drum reconditioning and recycling networks across the U.S. and Canada, strengthening circular packaging adoption and reducing total lifecycle costs for chemical producers. Manufacturing reshoring initiatives and increased intra-regional trade under the U. S.-Mexico-Canada Agreement support steady bulk transport requirements. Recent investments in automation, leak detection systems, and digital asset tracking technologies have improved quality control and traceability, enhancing supplier competitiveness. Firms with nationwide compliance capabilities and strategically located service hubs maintain a structural advantage in serving high-volume chemical and lubricant customers.

Europe Steel Drums & IBCs Market Trends-Regulatory Harmonization and Technical Specialization Sustaining Premium Positioning

Europe represents a mature yet technologically advanced steel drums & IBCs market characterized by regulatory harmonization and high product standards. Germany remains a leading production hub, supported by its strong chemical manufacturing base, including multinational groups such as BASF. The country is known for high-specification lined and stainless-steel drum production that serves specialty chemicals and pharmaceutical intermediates. The U.K., France, and Spain also maintain established drum manufacturing clusters that supply both domestic and export markets.

The harmonization of dangerous goods transport regulations under the ADR framework has created consistent compliance requirements across the European Union. This regulatory clarity promotes reuse, reconditioning, and material recovery, aligning with the European Green Deal’s sustainability targets. For instance, Schütz has expanded its European reconditioning and collection infrastructure to strengthen closed-loop IBC systems, enabling customers to meet environmental reporting standards. Suppliers increasingly differentiate through advanced internal linings, food-grade certifications, and pharmaceutical compliance capabilities. In this environment, revenue growth depends more on technical specialization and value-added services than on incremental volume expansion, supporting margin resilience despite modest demand growth.

Asia Pacific Steel Drums & IBCs Market Trends - Export-Led Chemical Expansion Accelerating UN-Compliant Packaging Demand

Asia Pacific is the fastest-growing regional market, driven by expanding chemical production capacity in China, India, and ASEAN economies. China continues to invest heavily in downstream petrochemicals and specialty chemical clusters, creating large-scale demand for industrial drums and IBCs. India’s chemical exports have expanded steadily, supported by government initiatives to strengthen domestic manufacturing under programs such as “Make in India,” which indirectly stimulate packaging requirements for export-grade containers.

Major regional players and global manufacturers are increasing localized production capacity to capture this growth. For example, Balmer Lawrie & Co. Ltd. operates large steel drum manufacturing facilities in India, supplying lubricant and chemical producers across South Asia and the Middle East. Global firms such as Greif have expanded manufacturing and reconditioning operations in China and Southeast Asia to align with multinational customer demand. Investment in automated forming lines, high-performance coating systems, and export-compliant UN certification enhances product reliability and global acceptance.

Regulatory alignment with international packaging standards continues to improve export competitiveness across the region. As Asian chemical producers increase outbound shipments to North America and Europe, demand for globally compliant steel packaging solutions strengthens. Companies that combine localized manufacturing efficiency with international quality assurance frameworks are positioned to capture high-growth opportunities in this region.

Competitive Landscape

The global steel drums & IBCs market demonstrates moderate fragmentation globally, with a combination of large integrated suppliers and numerous regional producers. Leading players typically hold single-digit to low-teen percentage shares individually. Competitive positioning depends on compliance expertise, manufacturing scale, reconditioning infrastructure, and geographic coverage. High-value segments such as certified IBC fleets and stainless steel drums show greater concentration. Key strategic themes include vertical integration across manufacturing and reconditioning, premium product development with certified linings and stainless options, and service-based models incorporating rental, lifecycle management, and digital asset tracking.

Key Industry Developments:

- In February 2025, SCHÜTZ partnered with NPF to establish a licensed production facility for its ECOBULK IBCs near Dammam in the GCC region, set to begin local manufacturing in 2026 to improve supply security for chemicals, oil, and food industry customers.

- In September 2025, Greif, Inc. announced the launch of its EcoBalance™ Low Carbon Emission Steel Drums, produced with approximately 75% recycled steel in partnership with ArcelorMittal, reducing carbon footprint by around 60% while maintaining performance standards.

Companies Covered in Steel Drums & IBCs Market

- Greif

- Mauser Packaging Solutions

- Schütz

- Balmer Lawrie & Co. Ltd.

- Sicagen India Limited

- Time Technoplast Ltd.

- Thielmann

- Patrick J. Kelly Drums

- North Coast Container

- Industrial Container Services

- Rahway Steel Drum Company

- General Steel Drum LLC

- Cloud Manufacturing

- Skolnik Industries

- Fibrestar Drums Limited

- Nippon Steel Drums Co. Ltd.

- Snyder Industries

- Hoover Ferguson

Frequently Asked Questions

The global steel drums & IBCs market size is projected to reach approximately US$14.7 billion in 2026.

By 2033, the steel drums & IBCs market is expected to reach approximately US$20.7 billion.

Key trends include rising adoption of reconditioned and reusable steel drums, expansion of steel IBC rental and lifecycle management programs, automation of drum forming and inspection lines, advanced internal lining technologies for food and pharmaceutical applications, and integration of digital asset tracking systems to improve traceability and compliance.

Tight-head steel drums represent the leading product segment, anticipated to account for approximately 57.3% of market share, due to their sealed design, chemical compatibility, and global dimensional standardization.

The steel drums & IBCs market is projected to grow at a CAGR of approximately 5.0% in the near term.

Major players with strong global portfolios include Greif, Mauser Packaging Solutions, Schütz, Balmer Lawrie & Co. Ltd., and Sicagen India Limited.