- Non-food Packaging

- Cannabis Packaging Market

Cannabis Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Cannabis Packaging Market by Material Type (Plastic, Paper & Paperboard, Others), Product Type (Bags & Pouches, Bottles & Jars, Boxes & Cartons, Others), Application (Medical, Recreational), and Regional Analysis for 2026 - 2033

Cannabis Packaging Market Size and Trend Analysis

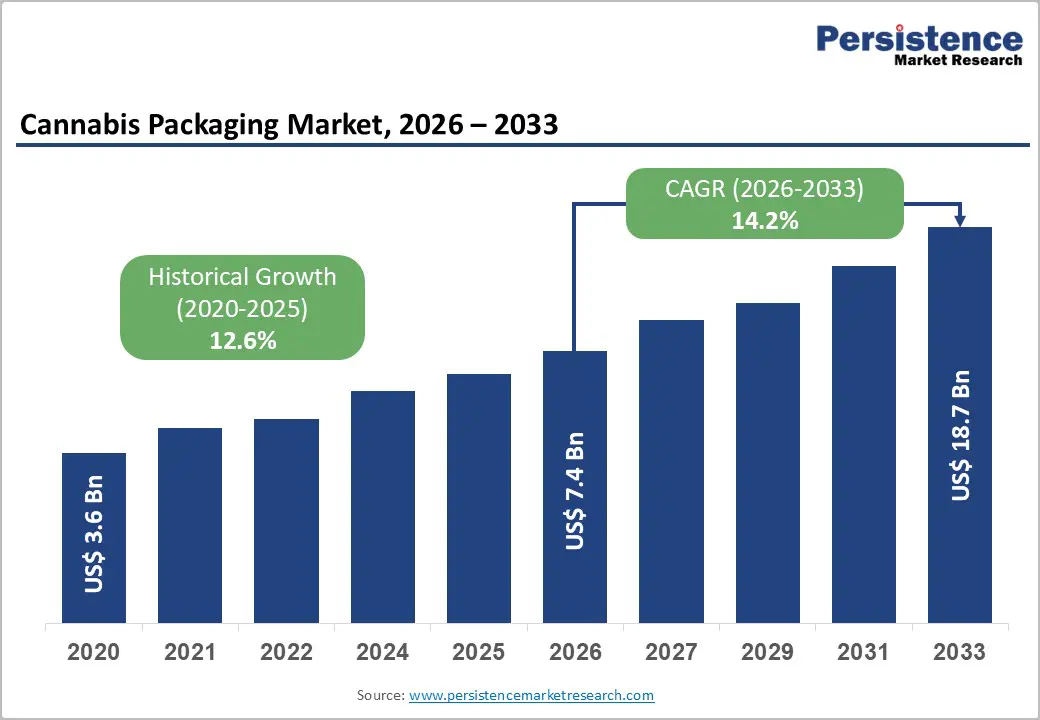

The global cannabis packaging market is valued at US$ 7.4 billion in 2026 and is projected to reach US$ 18.7 billion by 2033, growing at a CAGR of 14.2% between 2026 and 2033. Accelerating market expansion is primarily driven by the rapid global legalization wave reshaping cannabis commerce.

As of early 2026, 42 U.S. states plus Washington, D.C. permit medical cannabis, while 24 states have legalized recreational use, creating sustained demand for compliant packaging. Simultaneously, Germany's Cannabis Act (CanG), effective April 1, 2024, established Europe's largest cannabis legalization framework, catalyzing demand for child-resistant, tamper-evident, and EU-GMP-compliant packaging.

Key Industry Highlights:

- Leading Region: North America dominates the global Cannabis Packaging market, driven by the U.S. legal cannabis industry generating US$ 30.1 Bn in sales in 2024, with 24 states legalizing recreational use and 42 states permitting medical cannabis, ensuring sustained high-volume packaging procurement.

- Fastest Growing Region: Asia Pacific is the fastest-growing region in the Cannabis Packaging market, propelled by Australia's expanding TGA-regulated medical cannabis program, Japan's amended Cannabis Control Act permitting medical THC use from 2024, and China's cost-competitive contract packaging manufacturing capabilities.

- Dominant Segment Plastic (Material Type): Plastic commands approximately 55% of the Cannabis Packaging market by material type, favored for its superior moisture, oxygen, and UV barrier properties, cost efficiency, and widespread compatibility with child-resistant closure regulatory requirements across U.S. and international jurisdictions.

- Fastest Growing Segment Paper & Paperboard (Material Type): Paper & Paperboard is the fastest-growing material segment, driven by Extended Producer Responsibility regulations, consumer demand for eco-friendly packaging, and the rising adoption of recyclable cartons and compostable board formats by cannabis brands committed to sustainability targets.

- Key Market Opportunity: Smart and sustainable packaging innovations including RFID-enabled traceability, QR code-integrated consumer engagement tools, and compostable or PCR-content formats, represent high-value growth opportunities as regulations tighten seed-to-sale compliance requirements and consumer eco-consciousness accelerates globally.

| Key Insights | Details |

|---|---|

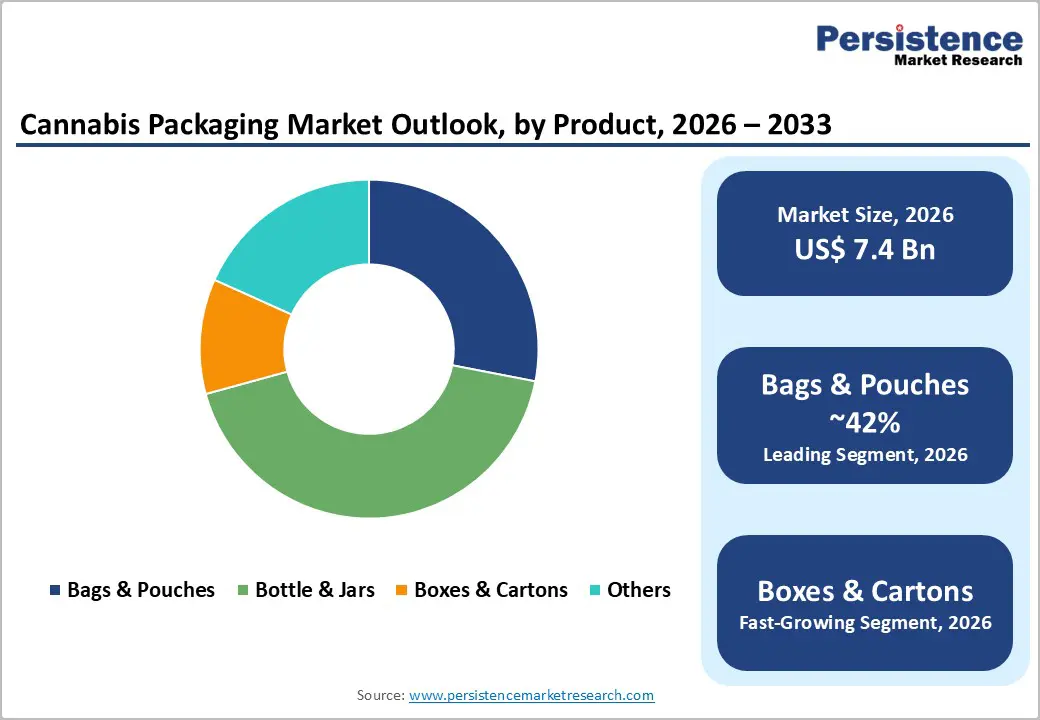

| Cannabis Packaging Market Size (2026E) | US$ 7.4 Bn |

| Market Value Forecast (2033F) | US$ 18.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 14.2% |

| Historical Market Growth (2020 - 2025) | 12.6% |

DRO Analysis

Surging Cannabis Legalization Fueling Compliant Packaging Demand

The single most powerful driver of cannabis packaging demand is the accelerating global legalization of cannabis for medical and recreational use. According to the U.S. National Survey on Drug Use and Health (NSDUH) 2024, approximately 64.2 million Americans aged 12 and above reported cannabis use in the past year, accounting for 22.3% of the population. Legal cannabis sales across U.S. states reached US$ 30.1 Bn in 2024, according to Whitney Economics, generating massive demand for regulatory-compliant packaging.

Every additional state or country that formalizes cannabis commerce adds direct volume to the packaging supply chain. Cannabis producers operating in regulated markets are legally mandated to use child-resistant, tamper-evident, opaque, and properly labelled packaging making packaging a non-optional, recurring expenditure across the value chain.

Stringent Child-Resistant and Tamper-Evident Packaging Regulations

Regulatory frameworks across jurisdictions universally mandate child-resistant (CR) and tamper-evident packaging for all cannabis products. In the United States, the Poison Prevention Packaging Act (PPPA) and individual state cannabis authorities require all flower, edibles, and vape cartridges to be housed in CR-certified formats. Non-compliance risks product recalls, fines, and license revocation.

With adult-use cannabis generating over US$ 4.4 Bn in state tax revenues in 2024 alone, governments are intensifying packaging compliance enforcement to safeguard public health. This direct regulatory requirement ensures structural, recurring demand for specialized packaging manufacturers and forces producers to continually re-invest in compliant packaging formats.

Restraints - High Cost of Sustainable and Compliant Packaging Materials

The dual requirement for child-resistant functionality and environmental sustainability significantly elevates packaging material costs, creating a financial burden particularly for smaller cannabis producers. Sustainable inputs such as compostable resins, bioplastics, and post-consumer recycled (PCR) polymers command substantial price premiums over conventional plastics.

For instance, in Canada one of the world's most mature legal cannabis markets the legal sector generates millions of pounds of packaging waste annually, yet strict opacity requirements hinder recyclability, limiting cost-sharing benefits for eco-friendly alternatives. These elevated production costs compress margins for licensed producers, particularly multi-state operators seeking economies of scale, and can slow the adoption of premium or sustainable packaging tiers.

Complex and Fragmented Regulatory Landscape Across Jurisdictions

Cannabis packaging regulations vary dramatically between states, provinces, and countries, creating significant compliance complexity and cost inefficiencies. In the United States alone, each of the 24 states with recreational legalization maintains distinct packaging rules around label requirements, serving sizes, THC warnings, and use-by date mandates some effective from January 1, 2024.

Simultaneously, Europe's evolving frameworks, including Germany's CanG requirements, add another layer of divergence. This fragmented regulatory mosaic drags on speed-to-shelf, increases compliance overheads, and makes it exceedingly difficult for packaging suppliers to develop universally deployable product lines.

Opportunity - Eco-Friendly and Sustainable Packaging Innovation as a Strategic Differentiator

Growing consumer preference for environmentally responsible products and tightening Extended Producer Responsibility (EPR) regulations are converging to make sustainable packaging a high-value opportunity for market participants. Innovations such as compostable packaging systems exemplified by Contempo Specialty Packaging's DIN CERTCO- and BPI-certified compostable system launched in June 2024 demonstrate the commercial viability of eco-friendly formats.

Similarly, hemp-based and ocean-bound plastics pioneered by companies such as Sana Packaging address dual mandates of child safety and recyclability. Companies that develop packaging solutions combining regulatory compliance with a measurable environmental footprint reduction will achieve strong differentiation, command brand loyalty, and gain preferred supplier status with leading cannabis producers committed to sustainability targets.

Smart Packaging Technologies Enabling Product Traceability and Brand Engagement

The integration of smart packaging technologies including RFID tags, QR codes, and IoT-enabled freshness sensors represents a significant growth opportunity for premium cannabis packaging providers. Canada streamlined its packaging rules in March 2025 to explicitly permit transparent windows and scannable QR codes without compromising child-resistant metrics, reducing unit costs.

Furthermore, StashStock's RFID readers, which integrate with METRC compliance systems and scan up to 40 tags per second, illustrate how smart packaging can simultaneously address traceability, inventory reconciliation, and brand differentiation. As regulators tighten seed-to-sale tracking requirements globally, smart packaging becomes both a compliance tool and a brand engagement asset, enabling packaging companies to shift from commodity to value-added supplier relationships.

Category-wise Analysis

Material Type Insights

Plastic dominates the Cannabis Packaging market by material type, commanding approximately 55% of the total market share. The dominance of plastic is underpinned by its functional versatility, cost efficiency, and superior barrier properties. Plastic packaging effectively shields cannabis products from moisture, oxygen, and UV light environmental factors that degrade potency and aroma. High-density polyethylene (HDPE) and polypropylene (PP) are widely used in child-resistant closures, jars, and vials across both medical and recreational segments.

The development of PCR-50 polypropylene containers, such as the Crativ PCR50 launched by Amcor and CRATIV Packaging in November 2023, integrating 50% post-consumer recycled plastic content, further reinforces plastic's relevance through sustainability innovation. Paper & Paperboard is the fastest-growing material, gaining traction for secondary packaging.

Product Type Insights

Bottles & Jars constitute the leading product type segment, holding approximately 38% of the Cannabis Packaging market by product type. Their dominance is driven by their superior product protection, ease of use, and high compatibility with regulatory child-resistant closure requirements. Glass and premium plastic bottles and jars offer excellent barriers against light, moisture, and air critical parameters for preserving the quality, potency, and terpene profile of cannabis flower and concentrates.

Most bottles and jars are designed with push-and-turn or squeeze-and-turn CR closures that meet Consumer Product Safety Commission (CPSC) standards in the U.S. The premiumization trend in recreational cannabis is further fueling demand for aesthetically sophisticated glass jars that enhance retail shelf appeal, while medical cannabis operators prefer pharmaceutical-grade amber glass jars for precise dosing and contamination prevention.

Application Insights

The medical application segment holds the leading share in the Cannabis Packaging market, representing approximately 56% of total market revenue. Medical cannabis packaging is subject to the most rigorous regulatory standards, requiring tamper-evident, child-resistant, and opaque formats in virtually all jurisdictions. According to the U.S. Congress Research Service (March 2026), medical cannabis is now legally accessible in 40 U.S. states plus Washington D.C., Puerto Rico, Guam, and the U.S. Virgin Islands, creating a large, stable procurement base.

Pharmaceutical-grade packaging including amber glass vials, blister packs, and pharmaceutical cartons commands higher per-unit value relative to recreational formats. The rising acceptance of cannabis-derived medications and medical dispensary expansion across Europe further reinforces the medical segment's market leadership through the forecast period.

Regional Analysis

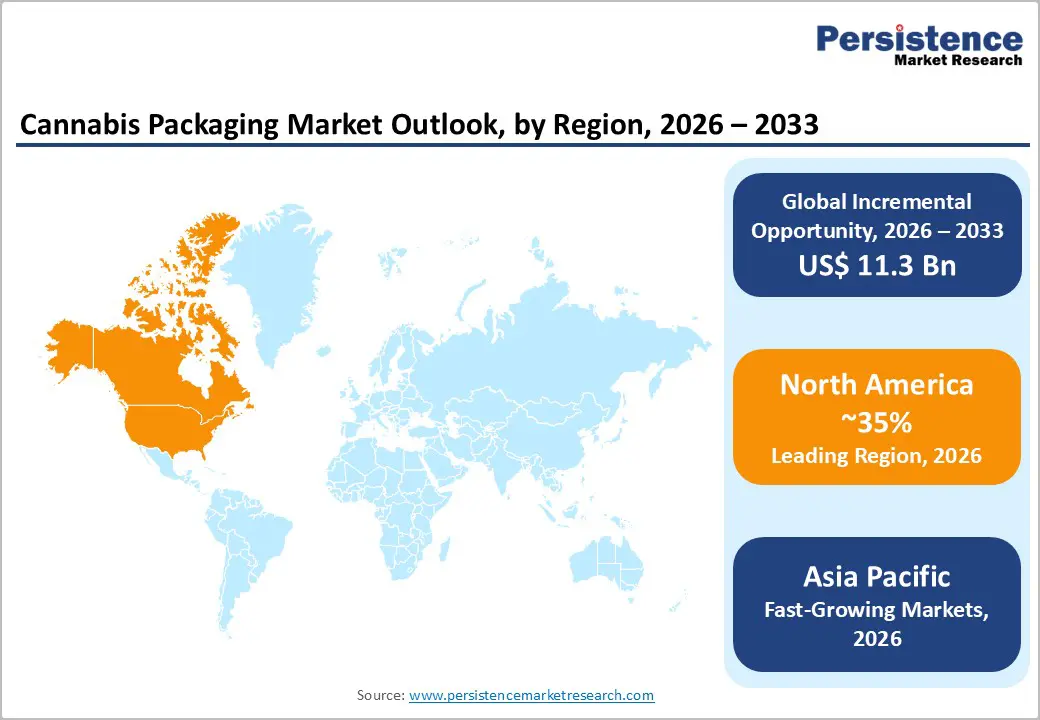

North America Cannabis Packaging Market Trends

North America is the dominant region in the global Cannabis Packaging market, accounting for the largest revenue share driven by the world's most advanced legal cannabis infrastructure. In the United States, legal cannabis sales totaled US$ 30.1 Bn in 2024 (Whitney Economics), underpinning robust and recurring packaging procurement. With 24 states and Washington D.C. permitting adult-use cannabis, and 42 states supporting medical programs, the U.S. market offers packaging suppliers unmatched scale.

Canada continues to mature as a highly standardized market after federal legalization under the Cannabis Act (2018). Notably, in March 2025, Canada streamlined regulations to permit transparent packaging windows and scannable QR codes, reducing unit costs and enabling brand differentiation.

Asia Pacific Cannabis Packaging Market Trends

Asia Pacific is the fastest-growing region in the global Cannabis Packaging market, driven by an emerging wave of regulatory reforms, expanding medical programs, and strong manufacturing cost advantages. Australia leads the region with an established medical cannabis program regulated by the Therapeutic Goods Administration (TGA), creating demand for pharmaceutical-grade packaging including CR closures and tamper-evident labels.

India is emerging as both a manufacturing hub and a nascent regulatory market, with several states re-examining cannabis policy for industrial hemp and medical applications. ASEAN nations including Thailand despite reversing its full recreational liberalization in June 2025 continue to supply medical cannabis internationally, sustaining packaging export demand.

Europe Cannabis Packaging Market Trends

Europe is witnessing rapid regulatory evolution that is generating significant new demand for specialized cannabis packaging. The landmark development is Germany's Cannabis Act (CanG), which entered into force on April 1, 2024, making Germany the first major EU member state to legalize recreational cannabis possession and home cultivation. With approximately 4.5 million Germans estimated to use cannabis, the German legalization has catalyzed demand for EU-GMP-compliant and serialized-traceability packaging.

Beyond Germany, the United Kingdom represents a significant future opportunity with an estimated EUR 9.5 Bn (approximately US$ 11.19 Bn) potential market pending regulatory clarity. Italy and the Netherlands maintain active medical cannabis supply chains requiring amber glass and blister-strip packaging.

Competitive Landscape

The global cannabis packaging market is characterized by a moderately fragmented competitive structure, with a blend of established packaging conglomerates and specialized niche players. Large global packaging companies such as Amcor and Berry Global are increasingly committing capital to cannabis-specific formats, leveraging their scale to offer cost-competitive, compliant solutions. Meanwhile, specialist firms including Greenlane Holdings, Kush Supply Co., and N2 Packaging Systems differentiate through deep regulatory expertise, child-resistant innovation, and just-in-time delivery models.

Key Market Developments

- In December 2025, Tap Tubes LLC, based in Alaska, is transforming cannabis packaging with a groundbreaking solution that prioritizes environmental sustainability and operational efficiency. The company's product range, which features biodegradable Tap Tubes and a specially designed automatic labelling machine, seeks to challenge wasteful practices and promote a circular economy within the cannabis sector.

- In December 2025: Cannabliss unveiled a new selection of tailored packaging solutions specifically for the cannabis sector, featuring enhanced formats such as child-resistant closures, containers for edibles, and packaging for concentrates, all designed with a focus on safety, compliance, and improved functionality.

Companies Covered in Cannabis Packaging Market

- Amcor

- Sanner GmbH

- The BoxMaker

- Kush Supply Co.

- Greenlane Holdings Inc.

- Primary Packaging Inc.

- Atlantic Packaging

- Kaya Packaging

- Diamond Packaging

- Green Rush Packaging

- N2 Packaging Systems LLC

Frequently Asked Questions

The global Cannabis Packaging market is valued at US$ 7.4 Bn in 2026 and is expected to reach US$ 18.7 Bn by 2033, registering a CAGR of 14.2% over the forecast period.

The primary drivers of the Cannabis Packaging market are the rapid legalization of cannabis across 24 U.S. states for recreational use and 42 states for medical use, combined with stringent regulatory mandates for child-resistant (CR) and tamper-evident packaging.

Plastic is the leading material type segment in the Cannabis Packaging market, holding approximately 55% of total market share. Its dominance is attributable to superior moisture, oxygen, and UV light barrier properties; cost efficiency; design flexibility for CR closures; and the availability of sustainable variants such as post-consumer recycled (PCR) plastics that maintain compliance while meeting environmental standards.

North America is the leading region in the global Cannabis Packaging market. The region's dominance is driven by the United States' advanced legal cannabis infrastructure, which generated US$ 30.1 Bn in legal sales in 2024.

Key players operating in the global Cannabis Packaging market include Amcor, Greenlane Holdings Inc., Kush Supply Co., Sanner GmbH, The BoxMaker, Primary Packaging Inc., Atlantic Packaging, Kaya Packaging, Diamond Packaging, Green Rush Packaging, and N2 Packaging Systems LLC, among others.