- Medical Devices

- Specialty Actives in Personal Care Market

Specialty Actives in Personal Care Market Size, Share and Growth Forecast, 2026 - 2033

Specialty Actives in Personal Care Market by Ingredient Function (Anti-Aging, Brightening, Hydration, Anti-Acne, UV Protection), Application (Skincare, Haircare, Sun Care, Cosmetic, Functional Dermatological), Source & Technology (Synthetic, Biotechnological, Botanical, Marine-Derived, Microbiome-Supported), and Regional Analysis for 2026 - 2033

Specialty Actives in Personal Care Market Share and Trends Analysis

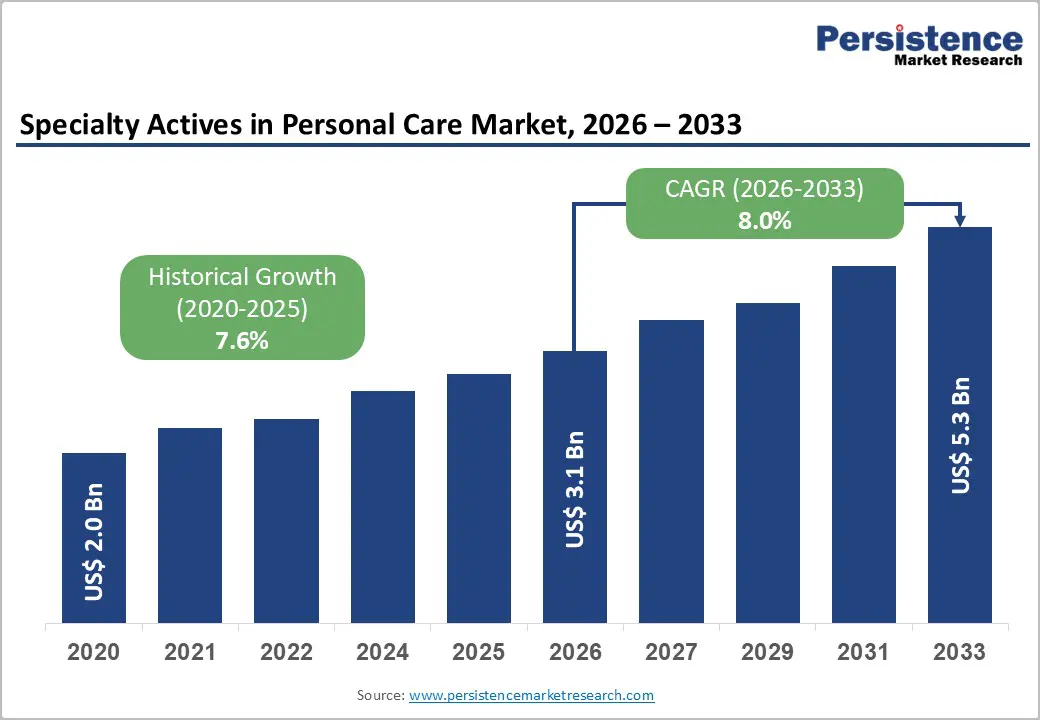

The global specialty actives in personal care market size is likely to be valued at US$3.1 billion in 2026 and is projected to reach US$5.3 billion by 2033, growing at a CAGR of 8.0% during the forecast period 2026-2033.

The market is expanding due to shifting consumer preferences toward efficacy-driven and multifunctional formulations. Rising demand for anti-aging, hydration, and UV protection actives reflects increased awareness of preventive skincare, while the popularity of natural and microbiome-supported ingredients aligns with sustainability trends. Skincare and functional dermatological applications are driving adoption, as consumers seek clinically substantiated benefits such as improved elasticity, pigmentation control, and acne management. Simultaneously, emerging markets and urbanization are accelerating growth, with rising disposable incomes in Asia Pacific and Latin America enabling access to premium personal care products. Expanding retail infrastructure and digital channels further amplify product reach, increasing per-capita consumption and supporting consistent market expansion across diverse regions.

Key Industry Highlights

- Dominant Function Segments: Anti-aging actives are set to command around 38% of the revenue share in 2026, while UV protection actives are likely to grow the fastest at 9.5% CAGR through 2033, as preventive skincare awareness and multifunctional product demand rise.

- Leading Applications: Skincare applications are anticipated to lead with an estimated 52% share in 2026, while functional dermatological applications are projected as the fastest-growing at 9.8% CAGR through 2033, reflecting increasing clinical validation and targeted treatment adoption.

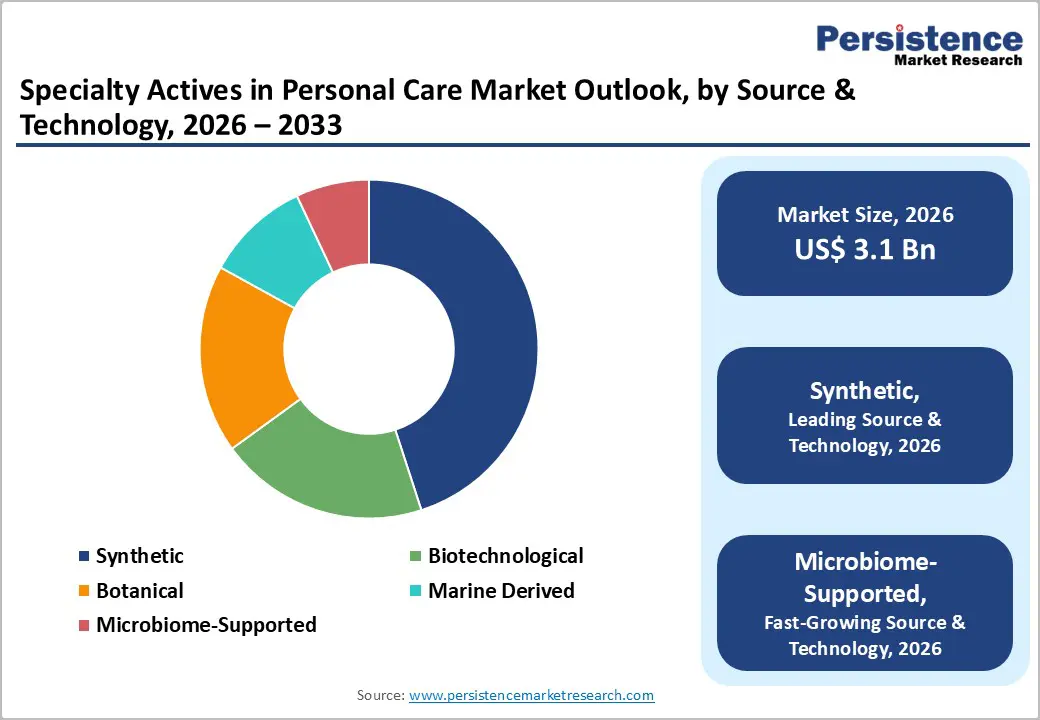

- Leading Sources & Technology: Synthetic actives are set to dominate with a combined share of 45% in 2026, while microbiome-supported are expected to grow the fastest at 10.1% CAGR through 2033, driven by sustainability and novel efficacy claims.

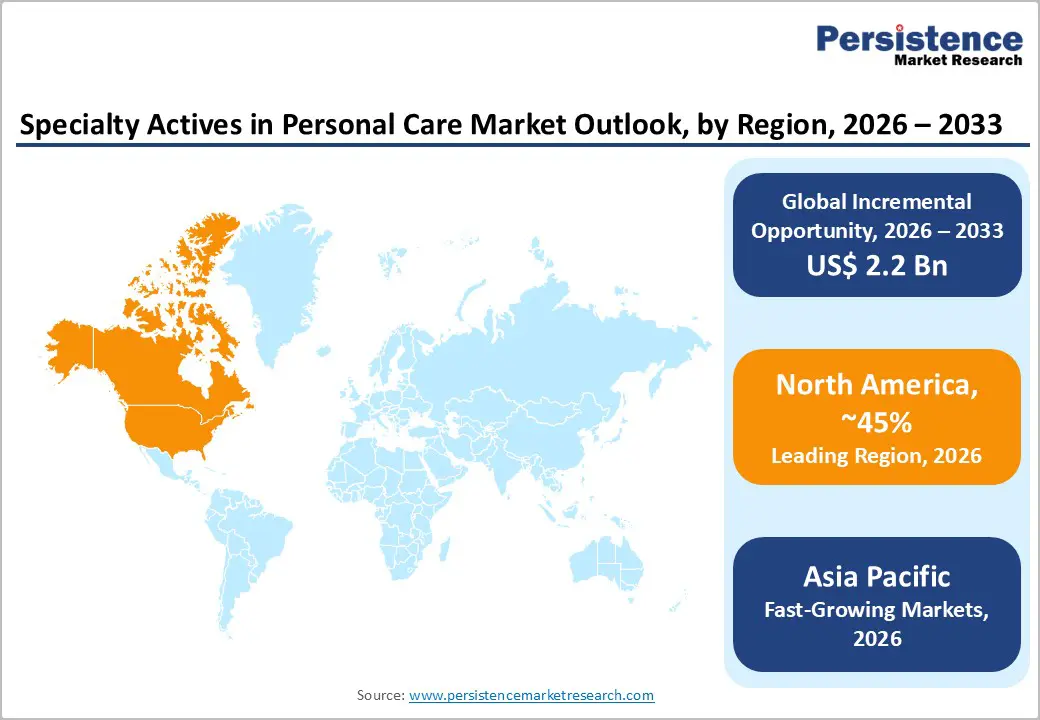

- Regional Leadership: North America is poised to lead with an estimated 45% share in 2026, while Asia Pacific is likely to grow the fastest at 10.2% CAGR through 2033, supported by urbanization, rising disposable incomes, and expanding middle-class consumption.

- Competitive Environment: Strategic moves include biotech acquisitions, microbiome-active launches, and emerging market expansion in 2025–2026, enhancing innovation pipelines and regional penetration.

| Key Insights | Details |

|---|---|

|

Specialty Actives in Personal Care Market Size (2026E) |

US$ 3.1 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.6% |

DRO Analysis

Driver - Demographic Expansion, Evolving Preferences, and Demand for High-Performance Actives

Population ageing in developed markets and increasing youth adoption of targeted skincare regimens are expanding specialty actives demand (e.g., anti-ageing, anti-acne). Consumers aged 35+ demonstrate higher per-transaction spending on premium, efficacy-driven actives, supported by greater purchasing power and demand for clinically proven anti-aging solutions, which supports segment growth. Also, the expanding middle-class cohorts with rising disposable incomes are accelerating product adoption rates. Market research indicates that as disposable income rises, consumers allocate a growing share toward high-performance actives, particularly in skincare and UV protection categories. This shift is further supported by increased awareness of long-term skin health and preventive care routines among urban populations.

This demand is increasingly concentrated around clinically proven actives such as retinol, peptides, niacinamide, and vitamin C, which directly address visible skin concerns. Retinol and peptides stimulate collagen production and improve elasticity, while niacinamide strengthens the skin barrier, reduces inflammation, and controls oil. Vitamin C provides antioxidant protection and brightening benefits, supporting pigmentation control and environmental defense. These targeted benefits reinforce consumer willingness to invest in efficacy-driven formulations and drive premium product adoption across both mature and emerging markets.

Technological Innovation and Shift toward Sustainable & Next-Generation Actives

Advances in biotechnology, peptide engineering, and delivery systems such as liposomes are enabling the development of novel functional actives with improved bioavailability and targeted performance. At the same time, there is a strong uptick in demand for natural and ethically sourced ingredients, with nearly 60% of skincare consumers considering clean labeling and sustainability as key purchase factors. This dual trend is accelerating R&D investments in both high-performance biotech ingredients and sustainable alternatives. Additionally, companies are increasingly focusing on traceability and environmentally responsible sourcing to strengthen brand credibility.

Emerging actives such as hyaluronic acid, microbiome-supported ingredients, and exfoliating acids (AHAs/BHAs) are gaining traction due to their multifunctional benefits. Hyaluronic acid delivers deep hydration and skin plumping by retaining significant moisture levels, while microbiome-supporting actives enhance skin barrier health and immune response. Exfoliating acids improve cell turnover, unclog pores, and enhance texture, making them essential in acne and brightening formulations. These innovations strengthen product differentiation while aligning with sustainability and personalization trends, accelerating long-term market growth and enabling brands to address a wider range of consumer needs.

Restraint - Regulatory Complexity and Rising Compliance Burden

Despite strong demand, regulatory environments (e.g., EU Cosmetics Regulation, FDA Safety Standards) impose rigorous testing and safety substantiation requirements. These compliance costs can delay new active rollouts and constrain smaller manufacturers’ agility. Regulatory approval timelines vary significantly across major markets, potentially increasing development costs by up to 20–30%. In addition, evolving ingredient restrictions and labeling requirements require continuous reformulation efforts, increasing operational complexity. This is particularly evident in markets with frequent regulatory updates and stricter enforcement timelines.

The European Commission expanded restrictions on carcinogenic and hazardous substances under updated cosmetic regulations, while additional ingredient bans and compliance deadlines have increased the burden on manufacturers. Also, the U.S. FDA’s expanded oversight under the Modernization of Cosmetics Regulation Act (MoCRA) has introduced mandatory facility registration and product listing requirements. These evolving frameworks are extending approval timelines, increasing compliance costs, and creating higher entry barriers, particularly for smaller and mid-sized players operating across multiple regions. This trend is expected to continue as regulatory bodies emphasize consumer safety and transparency.

Raw Material Price Volatility and Supply Chain Constraints

Many high-performing actives, especially botanically derived or microbiome-supported ingredients, are subject to supply fluctuations. Price volatility in natural extracts, peptides, and marine-derived compounds can compress margins (reported swings of 10–15% annually in key biotech ingredient categories), disproportionately impacting mid-sized players. Seasonal availability, environmental factors, and geopolitical disruptions further contribute to inconsistent supply and cost instability. These fluctuations are becoming more pronounced as demand for specialized actives continues to rise globally.

Industry developments in past years are amplifying these pressures. New restrictions on commonly used ingredients such as UV filters, preservatives, and synthetic additives are forcing companies to reformulate products and shift toward alternative raw materials, often at higher costs. Additionally, the rollout of microplastics restrictions in the European Union is accelerating the transition away from conventional inputs, increasing dependence on specialized and limited supply sources. These changes are creating procurement challenges, raising input costs, and adding uncertainty to long-term sourcing strategies across the value chain. As a result, companies are prioritizing supply chain diversification and ingredient innovation to mitigate risk.

Opportunities - Expansion in Emerging Economies and Digital Commerce Penetration

Emerging markets in the Asia Pacific and Latin America exhibit strong forecasted growth rates, supported by rising beauty-conscious populations and digital commerce adoption. Market estimates point to Asia Pacific capturing a growing share of global specialty actives demand by 2033 as disposable incomes and retail access expand. Rapid urbanization and increasing internet penetration are further enabling access to premium personal care products across tier-2 and tier-3 cities. This is supported by the growing influence of social media and beauty influencers in shaping consumer preferences.

Recent industry developments in 2025–2026 provide strong real-world validation of this trend. For instance, India’s beauty market is witnessing rapid expansion, attracting global investments and projected to grow significantly, driven by a young, digital-first population and rising e-commerce penetration across smaller cities. Additionally, Southeast Asian governments are actively supporting the cosmetics sector through R&D incentives, trade facilitation, and digital infrastructure development, strengthening regional supply chains and market accessibility. This combination of demographic momentum, policy support, and digital expansion is creating scalable growth opportunities for specialty active manufacturers targeting high-growth regions.

Innovation in Next-Generation Actives: Microbiome, Marine, and Biotech-Derived Ingredients

Next generation actives targeting skin microbiome balance and personalized skincare formulations represent a high growth frontier. Early adoption of microbiome supported actives is expected to catalyze bespoke product offerings and subscription based models with estimated incremental revenue potential of US$1 Bn+ by 2033. Increasing consumer awareness around skin health and barrier function is driving interest in products that deliver targeted and long-term benefits. This shift is encouraging brands to invest in advanced research and clinical validation of innovative actives.

Rapid innovation in new actives is redefining product performance and differentiation. The ingredients such as exosomes, growth factors, PDRN (salmon DNA), and advanced peptide complexes have gained traction for their ability to enhance cell communication, stimulate collagen production, and accelerate skin repair. These are complemented by bio-fermented actives and postbiotics, which improve absorption, strengthen the skin barrier, and reduce inflammation while maintaining stability. In parallel, marine-derived actives are gaining momentum, supported by initiatives such as Norway’s expansion of seaweed farming under its national bioeconomy strategy, aimed at scaling sustainable marine biomass production for industrial applications, including cosmetics. This is improving raw material availability, enabling consistent supply chains, and accelerating the commercialization of marine-based ingredients across global markets.

Category-wise Analysis

Source & Technology Insights

Synthetic actives are expected to dominate the market in 2026, contributing an estimated 45% share of total revenue, driven by high scalability, consistent quality, and the ability to engineer targeted functional benefits. Biotechnological actives, including peptides and growth factors, are valued for their precision and clinically validated performance, enabling reliable and reproducible outcomes across formulations. Advancements in formulation science have improved stability and absorption, enhancing overall product effectiveness while maintaining cost efficiency through established supply chains. Recent innovations, including AI-assisted ingredient discovery and fermentation-based production, are accelerating the development of bioengineered actives. The introduction of lab-grown collagen and precision peptides is reducing dependence on traditional extraction methods while improving sustainability and consistency.

Microbiome-supported actives are anticipated as the fastest-growing segment, expected to register a CAGR of approximately 10.1% through 2033, driven by demand for natural, sustainable, and science-backed ingredients. Microbiome actives enhance skin barrier function and immune response, while marine-derived ingredients provide antioxidant and anti-inflammatory benefits. Consumer preference for clean-label and eco-friendly formulations is accelerating adoption across premium skincare categories. In 2025–2026, innovations such as postbiotic-based actives and high-purity algae extracts have improved efficacy and formulation stability. Advancements in marine biotechnology are enabling scalable extraction from algae and deep-sea microorganisms. These developments are positioning the segment as a high-value growth frontier in specialty actives.

Ingredient Function Insights

Anti-aging actives are likely to remain the leading segment in 2026, accounting for approximately 38% of the total ingredient function market, driven by strong demand for peptides, retinoids, and antioxidant complexes targeting wrinkles and loss of elasticity. The segment benefits from an aging population and higher per-capita spending on premium skincare solutions, alongside growing adoption of preventive skincare among younger consumers. Continuous innovation in delivery systems has enhanced ingredient stability and efficacy, improving consumer outcomes. The advancements, such as encapsulated retinol and next-generation peptide blends, have improved tolerability while maintaining performance. These innovations are expanding usage across sensitive skin categories and increasing product adoption. As a result, anti-aging actives continue to anchor revenue generation and maintain segment leadership.

UV protection actives are projected to represent the fastest-growing segment, projected to expand at a CAGR of around 9.5% through 2033, driven by rising awareness of sun-induced damage and pigmentation concerns. Ingredients such as niacinamide, zinc oxide, and advanced UV filters are gaining traction due to multifunctional benefits, including protection, tone correction, and barrier support. Increasing regulatory emphasis on sunscreen efficacy and safety is further supporting market expansion. In 2025–2026, new broad-spectrum SPF formulations combined with antioxidants and anti-pollution actives have enhanced product performance. Demand for hybrid skincare-SPF products is accelerating adoption across daily routines. These trends position UV protection actives as a critical future growth driver.

Regional Analysis

North America Specialty Actives in Personal Care Market Trends

North America is expected to continue its domination in specialty actives market in 2026, accounting for roughly 45% of total revenue, with the United States driving a significant portion of demand. Strong consumer awareness, high disposable incomes, and a clear preference for clinically proven, performance-driven skincare are sustaining this dominance. Anti-aging and UV protection actives remain particularly strong, supported by a mature retail ecosystem and widespread adoption of premium formulations. The region also benefits from a dense concentration of global brands, contract manufacturers, and ingredient innovators, creating a highly competitive and innovation-led environment.

What further strengthens North America’s position is its deep-rooted biotechnology and clinical research ecosystem. The U.S. Food and Drug Administration (FDA) advanced enforcement under MoCRA, increasing transparency and pushing companies toward higher-quality, evidence-backed formulations. At the same time, companies such as Estée Lauder Companies have expanded investments in longevity-focused skincare research, reflecting a broader shift toward science-led innovation. The region’s real advantage lies in its ability to develop high-purity, lab-engineered actives at scale, backed by strong infrastructure and regulatory clarity, making it a global benchmark for premium, efficacy-driven ingredients.

Europe Specialty Actives in Personal Care Market Trends

Europe holds its position as the second-largest market, with key demand centers across Germany, the U.K., France, and Spain. Unlike North America’s performance-driven focus, Europe’s growth is shaped more by sustainability, transparency, and ingredient integrity. Consumers here are highly conscious of what goes into their products, which has accelerated demand for botanical, natural, and microbiome-supporting actives. Premium and luxury skincare segments remain particularly influential, driving consistent demand for high-quality formulations.

The regulatory environment plays a defining role in shaping this market. Also, the European Commission intensified its push under the EU Green Deal and Chemicals Strategy for Sustainability, encouraging a shift toward safer and environmentally responsible ingredients. This has prompted companies such as BASF SE and Croda International to expand their portfolios of plant-based and bio-fermented actives. Europe’s natural advantage lies in its rich botanical biodiversity and leadership in green chemistry, especially in countries such as France and Germany. Combined with strong research collaboration networks, this positions the region as a global center for sustainable and high-quality ingredient innovation.

Asia Pacific Specialty Actives in Personal Care Market Trends

Asia Pacific is projected as the fastest-growing regional market expected to expand at a CAGR of around 10.2% through 2033, fueled by rapid urbanization, rising incomes, and an increasingly beauty-conscious population. Markets such as China, India, Japan, and Southeast Asia are driving this momentum, each contributing unique demand patterns. Consumers are not only adopting premium skincare faster but are also showing strong interest in both high-performance and naturally derived actives. The rise of digital platforms and social commerce is further accelerating product discovery and adoption, particularly among younger consumers.

In 2025–2026, China’s NMPA continued to streamline approvals for new cosmetic ingredients, making it easier for brands to introduce innovative actives. In India, government-led seaweed cultivation programs under the Blue Economy initiative are improving access to marine-based raw materials. Meanwhile, institutions such as RIKEN in Japan are advancing research in bioactive and regenerative skincare ingredients. The region’s advantage lies in its diverse natural resources, ranging from marine inputs to traditional herbal systems such as Ayurveda and Kampo, paired with cost-efficient production, making it both a supply hub and a demand powerhouse for specialty actives.

Competitive Landscape

The global specialty actives in personal care market is moderately consolidated, with leading players such as BASF SE, Croda International, Evonik Industries, and DSM-Firmenich accounting for a significant revenue share. These companies leverage strong R&D capabilities, global supply chains, and diversified ingredient portfolios. Their focus on clinically validated, high-performance actives supports premium positioning. Continuous investments in biotechnology and sustainable chemistry reinforce their market leadership.

Players such as Ashland Global and Clariant are targeting niche segments such as microbiome, botanical, and clean-label actives. High entry barriers, including regulatory compliance and formulation complexity, limit the number of new participants. However, innovation-driven startups are entering through differentiated biotech offerings. Strategic partnerships and acquisitions are on the rise as companies expand capabilities in high-growth segments.

Key Industry Developments:

- In January 2026, Croda International introduced new bio-based and sustainable ingredient technologies at in-cosmetics Global 2026, including advanced Matrixyl peptide variants and PEG-free systems. These innovations focus on longevity skincare and climate-adaptive formulations, reinforcing Croda’s strategic push toward high-performance, eco-friendly actives.

- In March 2025, Persán S.A. acquired Mibelle Group, including its biotech arm Mibelle Biochemistry, to expand into specialty cosmetic actives. This move strengthens Persán’s position in high-value biotech ingredients and marks a strategic diversification into the personal care actives segment.

Companies Covered in Specialty Actives in Personal Care Market

- BASF SE

- Croda International

- Evonik Industries

- DSM-Firmenich

- Lonza

- Clariant

- Ashland Global

- Givaudan Active Beauty

- Solvay

- Symrise AG

- Lubrizol Corporation

- Seppic SA

Frequently Asked Questions

The global specialty actives in personal care market is projected to reach US$ 3.1 billion in 2026.

Rising demand for high-performance skincare, increasing consumer focus on efficacy, and advancements in biotechnology are driving the market.

The market is expected to grow at a CAGR of 8.0% from 2026 to 2033.

Expansion in emerging markets, innovation in biotech and marine-derived actives, and growth of personalized skincare solutions create key opportunities.

Key players include BASF SE, Croda International, Evonik Industries, and DSM-Firmenich.