- Automation & Robotics

- Robotic Lawn Mower Market

Robotic Lawn Mower Market Size, Share, and Growth Forecast, 2026 - 2033

Robotic Lawn Mower Market by Capacity (Up to 1 kW, 1 to 3 kW, Above 3 kW)., Level of Autonomy (Remote Controlled, Assisted, Autonomous), End-user (Utilities, PV Parks, Airport, Municipalities, Agriculture, Cemeteries, Others), Distribution Channel (Online, Offline), and Regional Analysis for 2026 - 2033

Robotic Lawn Mower Market Size and Trends Analysis

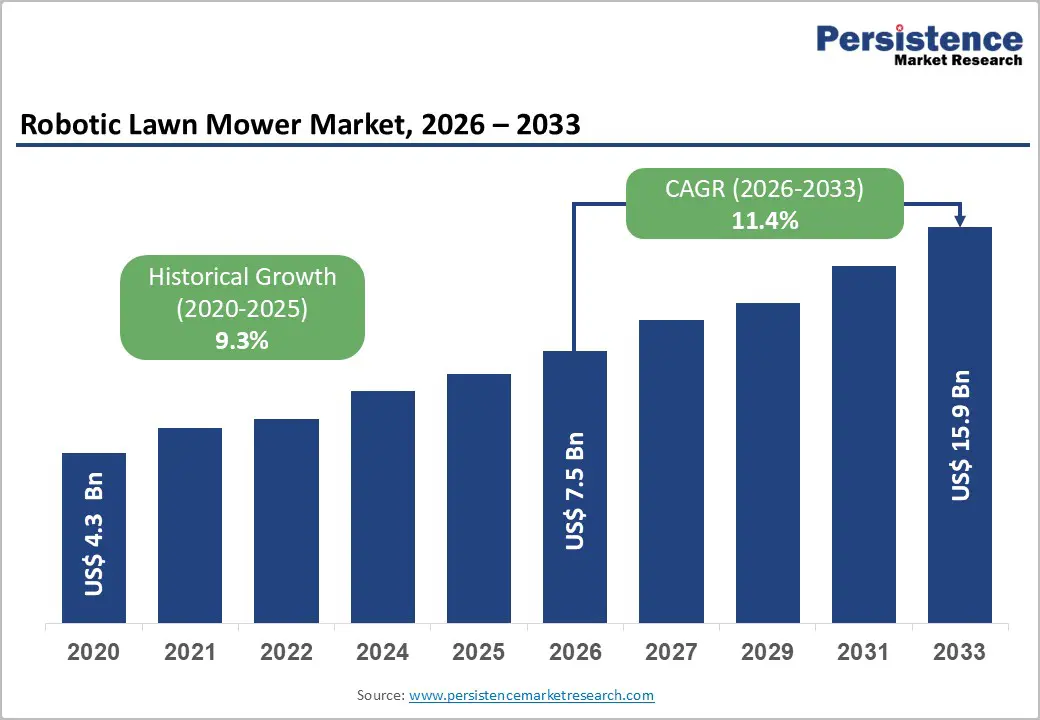

The Global Robotic Lawn Mower Market size is likely to be valued at US$ 7.5 billion in 2026 and is projected to reach US$ 15.9 billion by 2033, growing at a CAGR of 11.4% between 2026 and 2033.

The primary forces shaping this trajectory include the rapid commercial scaling of wire-free AI navigation platforms, persistent workforce shortages in professional landscaping services, and progressively stringent emissions and noise regulations in Europe and North America that systematically favor battery-electric automated alternatives over petrol-powered conventional equipment. Expanding procurement across municipalities, photovoltaic parks, sports facilities, and large commercial estates is progressively broadening the Robotic Lawn Mower Market's addressable base well beyond its historically residential-centric origins.

Key Industry Highlights:

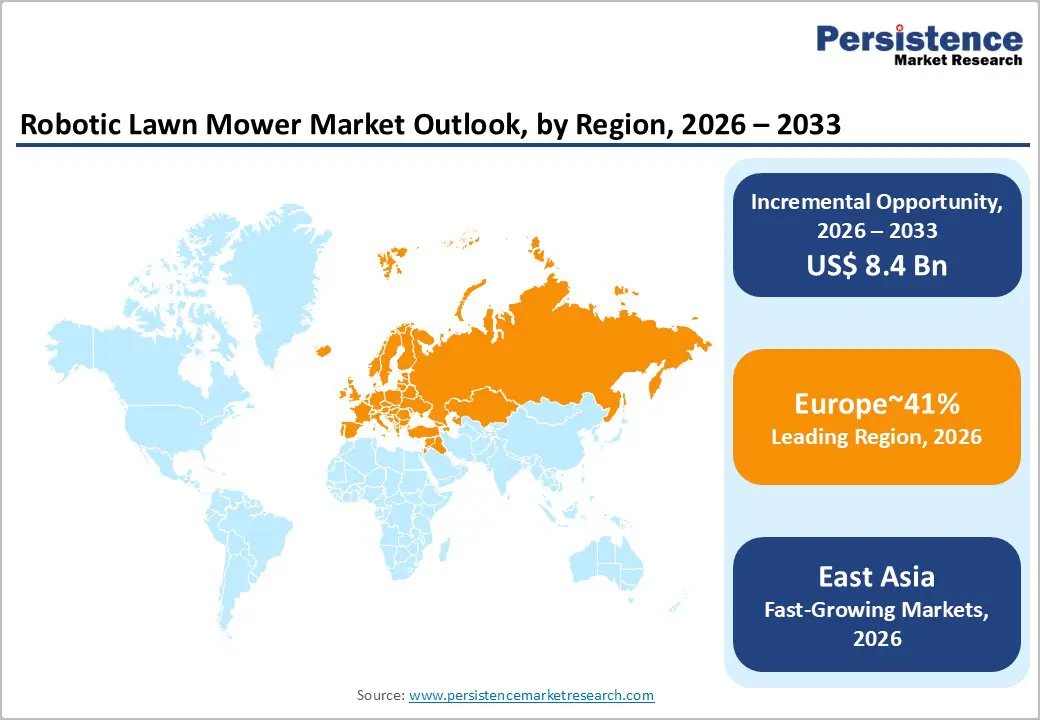

- Europe Market Leadership: Europe dominates the Robotic Lawn Mower Market with approximately 43% share, driven by strong regulatory frameworks, high residential adoption, and well-established landscaping ecosystems.

- North America Market Scenario: North America holds around 30% share, supported by large residential lawn sizes, labor shortages in landscaping, and increasing smart home integration.

- Autonomous Segment Dominance: Autonomous robotic mowers lead with approximately 68% share, reflecting rapid adoption of AI-enabled, self-operating lawn care systems across residential and commercial users.

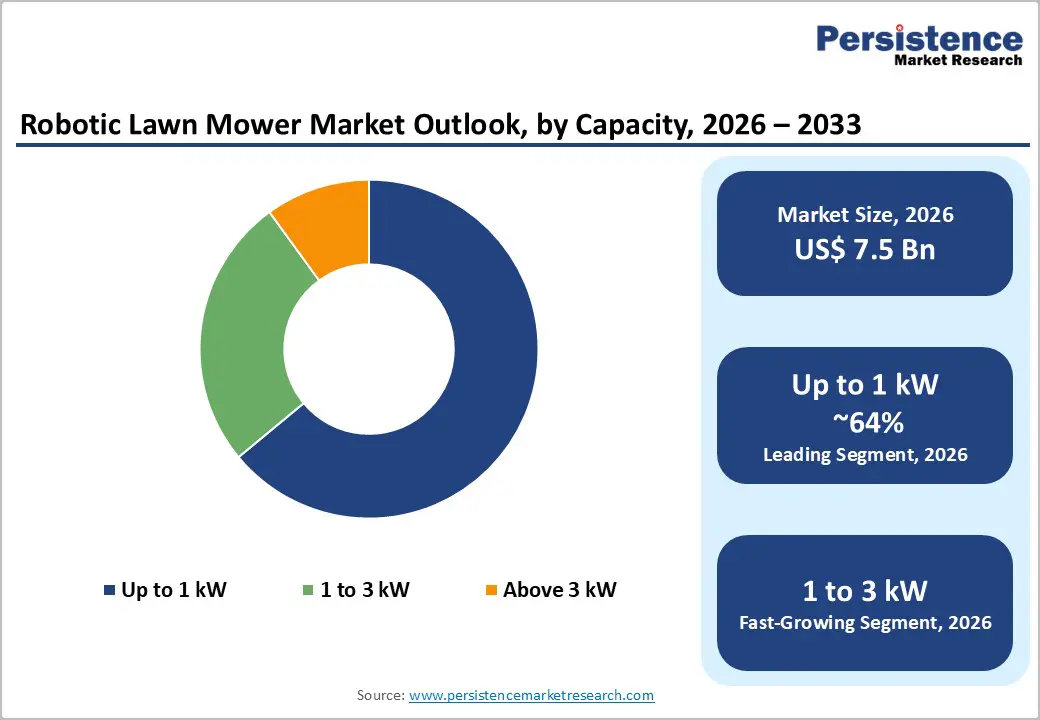

- Up to 1 kW Leading Capacity Segment: The up to 1 kW segment accounts for nearly 64% share, driven by high-volume residential demand and suitability for small to medium-sized lawns.

- Municipalities Leading End-user: Municipalities hold around 26% share, supported by large-scale public green space maintenance and increasing smart city infrastructure investments.

- AI-Driven Wire-Free Technology Transformation: Advancements in RTK-GNSS, LiDAR, and AI vision are eliminating boundary wires and redefining precision, efficiency, and scalability in robotic mowing solutions.

- PV Parks Emerging High-Growth Opportunity: Rapid expansion of solar infrastructure is creating strong demand for autonomous vegetation management, positioning PV parks as a key future growth segment.

| Key Insights | Details |

|---|---|

|

Market Robotic Lawn Mower Size (2026E) |

US$ 7.5 Bn |

|

Market Value Forecast (2033F) |

US$ 15.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.3% |

DRO Analysis

Drivers - Advancement of AI-Enabled Wire-Free Navigation Technology Reshaping Product Capability Standards

The transition from boundary-wire-dependent robotic systems to AI-powered, wire-free autonomous platforms represents the most consequential technology transformation in the Robotic Lawn Mower Market. RTK-GNSS positioning, AI vision, LiDAR sensor fusion, and multi-sensor obstacle detection now enable centimeter-level accuracy across complex multi-zone lawn geometries that legacy wired systems could not support.

Husqvarna Group's portfolio expansion to 24 wire-free models covering from 600 sqm to over 50,000 sqm, Honda's Miimo wireless series integrating RTK-GNSS with 4G cloud connectivity, and Segway-Ninebot's Navimow i Series with AI-assisted mapping collectively confirm this industry-wide platform shift. STIGA's APX Pro, integrating GPS-RTK, LiDAR, and AI vision for coverage up to 27,000 sqm with real-time adaptive navigation, and John Deere's autonomous commercial mower with AI-based 360-degree computer vision, establishes wire-free intelligence as the competitive standard. Positec Group's USD 250 million equity financing round to scale AI-driven wire-free technologies across its Worx and Kress brands further underscores the substantial commercial investment.

Structural Labor Shortages in Professional Landscaping Services Compelling Automation Investment

Persistent labor shortages within the professional landscaping industry represent one of the most structurally compelling demand drivers for the Robotic Lawn Mower Market. Seasonal visa restrictions, cross-sector workforce competition, and the physically demanding nature of outdoor maintenance work have collectively constrained labor supply across North America, Europe, and urban centers in Japan and Australia.

Commercial robotic mowers with a coverage capacity of 50,000 sqm can effectively replace three conventional ride-on mowers, enabling meaningful reductions in annual labor expenditure for sports facilities and institutional operators. Landscape companies deploying robotic mowing fleets can maintain service schedules without proportional workforce additions, allowing skilled crews to redirect effort toward higher-margin services such as landscape design and hardscaping. Positec Group's USD 250 million financing explicitly targets this commercial opportunity, funding R&D in AI-driven mowing across both consumer and commercial segments. The Asia-Pacific region, particularly in urban centers in Japan and Australia, faces comparable labor cost pressures, indicating a broadening global demand base for automated solutions in the Robotic Lawn Mower Market.

Regulatory Pressure and Environmental Policy Mandates Favoring Battery-Electric Autonomous Equipment

Tightening emissions regulations, noise ordinances, and sustainability frameworks across major markets are creating a well-defined policy-driven catalyst for the Robotic Lawn Mower Market. The European Union's Outdoor Noise Directive 2000/14/EC, updated through Directive 2024/2839 and supported by a delegated act published to update noise measurement methods under the Zero Pollution Action Plan, creates a structured regulatory environment favoring low-emission, low-noise battery-electric mowing equipment.

The EU Battery Regulation, Regulation EU 2023/1542, progressively mandates carbon footprint declarations and labeling requirements for rechargeable batteries placed on the EU market, directly shaping the design and supply chain standards of battery-powered robotic mowers. The EU Green Deal's climate neutrality target creates systemic institutional demand for precision, data-driven landscaping and maintenance technologies. Agricultural land accounted for 38.8% of the EU's total area, while residential, recreational, and community service land accounted for 5.8%, collectively representing a vast managed green space base that supports long-term demand for compliant autonomous mowing solutions across the robotic lawn mower market.

Restraint - High Upfront Acquisition Cost Constraining Mass-Market Residential Penetration

Despite clear operational benefits, the high initial cost of wire-free robotic lawn mowers with RTK-GNSS navigation, AI vision, and cloud connectivity remains a significant adoption barrier in price-sensitive residential segments and small-scale commercial operations. Premium commercial-grade models command substantially higher retail prices relative to conventional alternatives, creating hesitancy among cost-sensitive consumers and limiting broader market penetration beyond early adopters. In emerging markets across Asia and Latin America, constrained consumer financing options and lower average household income levels further slow adoption velocity in the Robotic Lawn Mower Market, creating a structural ceiling on near-term volume conversion from awareness to purchase.

Cybersecurity Risks and Data Privacy Compliance Burdens in Connected Autonomous Systems

As robotic lawn mowers integrate 4G communications, GPS mapping, AI-driven data collection, and cloud-based fleet management platforms, cybersecurity vulnerabilities and data privacy compliance obligations have become meaningful operational concerns. Connected autonomous systems that continuously map terrain and log usage data present potential attack surfaces for unauthorized access, carrying reputational and liability implications for commercial and municipal operators.

Compliance with the EU's General Data Protection Regulation and equivalent data governance frameworks in North America and Asia adds design, legal, and operational cost burdens for manufacturers deploying connected platforms across multiple regulatory jurisdictions, constraining the pace and cost structure of product development within the robotic lawn mower market.

Opportunities - Photovoltaic Park Vegetation Management as a High-Value Autonomous Mowing Application

Utility-scale solar photovoltaic installations create a structurally new and commercially significant end-use application for robotic powers. PV park operators require consistent, low-clearance vegetation management beneath and around panel arrays to prevent shading-induced losses in energy output efficiency, while manual mowing operations at large-scale sites introduce operational complexity, elevated costs, and safety risks near live electrical infrastructure.

Robotic mowers with RTK-GPS navigation, AI obstacle avoidance, and remote fleet management are technically well-suited to these requirements. As national renewable energy targets and international decarbonization frameworks drive continued solar capacity additions globally, PV park operators are seeking scalable autonomous mowing solutions with long-cycle reliability and minimal operator intervention. Manufacturers developing purpose-built PV park configurations with low-profile chassis, weather-resistant enclosures, and fleet management software integration stand to secure long-term commercial supply contracts with utility companies, positioning the robotic lawn mower market to capture a sustained high-value demand stream from the energy sector.

Smart City Infrastructure Programs Generating Scaled Municipal Robotic Mowing Procurement

Municipal authorities across Europe, North America, and East Asia are under mounting pressure to optimize public green space maintenance budgets while simultaneously expanding urban green infrastructure in line with climate resilience and liveability commitments. Parks, roadside verges, sports fields, cemeteries, and institutional grounds represent a large, recurring, and maintenance-intensive asset base for which robotic autonomous mowing offers compelling operational efficiency.

The EU's LUCAS survey confirms that residential, recreational, and community service land collectively covered 5.8% of EU's total land area, reflecting substantial public green space under regular maintenance. STIGA's APX Pro, explicitly designed for municipalities, sports fields, and golf courses with a coverage capacity of 27,000 sqm and real-time AI navigation, demonstrates active commercial targeting of this opportunity. As smart city infrastructure investment programs scale globally, procurement models integrating robotic mowing fleets with centralized fleet management platforms represent high-volume, multi-unit deployment pathways for Robotic Lawn Mower Market participants targeting the public sector.

Category-wise Analysis

Capacity Insights

The up to 1 kW capacity segment commands approximately 64% of the Robotic Lawn Mower Market, driven by its strong alignment with standard residential end-use requirements. Mowers within this power range deliver energy-efficient operation, reduced noise output, and cost-effective battery performance suited to household gardens typically below 2,000 sqm. The segment's commercial prevalence reflects the historically residential-centric adoption curve of robotic mowers, where compact, lightweight sub-1 kW designs provide adequate mowing performance compatible with standard residential electrical infrastructure and lower total ownership costs across key markets in Europe and North America.

The 1 to 3 kW capacity tier is demonstrating the fastest adoption momentum within the Robotic Lawn Mower Market's capacity classification, driven by commercial and large residential applications requiring extended operational range and superior terrain capability. Products in this power range, including Husqvarna's professional EPOS series and STIGA's APX Pro, target coverage from 5,000 sqm to over 27,000 sqm, addressing professional landscaping, sports field management, and municipal requirements. The convergence of higher-capacity battery platforms with wire-free navigation has enabled this segment to compete compellingly for institutional procurement programs.

Level of Autonomy Insights

The autonomous segment commands approximately 68% share in 2025, reflecting the core value proposition of fully self-operating systems requiring minimal human intervention. Autonomous robotic mowers with RTK-GNSS navigation, AI vision, radar-based obstacle detection, and cloud connectivity execute pre-programmed schedules and adaptive route planning without operator input during mowing cycles. Husqvarna's 24 wire-free autonomous models, Honda's Miimo series with app-based autonomous zone control, and John Deere's AI-powered commercial mower with 360-degree computer vision collectively represent the sustained commercial investment.

The assisted autonomy segment, encompassing semi-autonomous systems that combine human operator inputs with automated navigation and adaptive obstacle management, is registering the fastest adoption trajectory within the Robotic Lawn Mower Market's autonomy classification. Assisted systems address complex commercial environments, including irregular terrain, multi-obstacle sports facilities, and institutional grounds where fully autonomous navigation benefits from supplementary human oversight. Honda's ProZision autonomous riding mower unveiled at Equip Exposition, integrating GNSS navigation with radar and LiDAR for 360-degree obstacle detection alongside operator-supported route optimization, exemplifies the technically intermediate product category driving this segment's adoption.

End-user Insights

Municipalities represent the leading end-user segment of the robotic lawn mower market, accounting for approximately 26% of total market share. Municipal authorities manage extensive and diverse green space portfolios, including parks, roadside verges, recreational areas, and cemeteries, generating consistent high-frequency mowing demand that aligns directly with robotic automation's operational strengths. Budget constraints, sustainability mandates, and workforce limitations within public sector maintenance departments have accelerated fleet procurement. EU land data confirms that residential, recreational, and community service areas collectively cover 5.8% of EU total land area, providing a substantial public maintenance base, particularly across Germany, France, Belgium, and the Netherlands.

PV Parks represent the fastest-adoption end-user segment in the Robotic Lawn Mower Market, reflecting the global scaling of utility solar installations and the operational necessity of systematic, precision vegetation management across panel arrays. Solar farm operators require low-clearance, multi-pass mowing protocols to prevent panel shading and maintain ground cover density, requirements that robotic mowers address with navigational precision and programmable coverage patterns. STIGA's APX Pro, explicitly targeting large commercial operators including solar and utility-grade applications with up to 27,000 sqm coverage and real-time adaptive AI navigation, reflects active manufacturer engagement with this rapidly expanding segment.

Regional Insights and Trends

North America Robotic Lawn Mower Market Trends

North America accounts for approximately 30% of the robotic lawn mower market globally, with the United States as the primary demand center. The U.S. robotic lawn mower market alone generated approximately USD 1.01 billion, reflecting North America's position as the second-largest regional segment worldwide.

Chronic labor shortages in the U.S. landscaping industry, high suburban residential lawn ownership, and strong smart home technology adoption among dual-income households. Suburban U.S. homes predominantly feature lawns in the 0.25 to 0.5-acre range, creating a large addressable residential customer base for medium-capacity robotic mower configurations.

John Deere's autonomous battery-electric zero-turn stand-on commercial mower, featuring fully electric operation and AI-based 360-degree navigation, marks the company's formal entry into the autonomous commercial lawn care segment targeting professional landscaping efficiency. Positec Group's USD 250 million financing to scale wire-free AI mowing technologies across its Worx and Kress brands signals deep investment in both consumer and commercial North American demand.

Europe Robotic Lawn Mower Market Trends

Europe is the largest regional market, accounting for approximately 43% of global Robotic Lawn Mower Market share. Germany, Sweden, France, the United Kingdom, and the Netherlands represent the core demand centers, supported by high consumer spending power, well-established professional landscaping industries, and regulatory frameworks that structurally favor battery-electric autonomous equipment. The EU Outdoor Noise Directive and its delegated noise measurement update under the Zero Pollution Action Plan create a codified regulatory environment incentivizing adoption of low-emission autonomous mowers.

Agricultural land accounts for 38.8% of the EU's total land area, while land used for services and residential purposes, encompassing parks, recreational areas, and community services, reached 5.8% of EU total area, up 2.1% compared to the prior survey cycle. This expansion of managed green space reinforces the structural demand base for robotic mowing solutions. EU Battery Regulation 2023/1542, introducing mandatory carbon footprint declarations for rechargeable batteries, is reshaping supply chain and product design standards for battery-powered robotic mowers sold across the bloc. Key competitive dynamics are defined by Husqvarna's portfolio leadership with 24 wire-free models and STIGA's APX Pro targeting professional municipal and commercial applications.

East Asia Robotic Lawn Mower Market Trends

East Asia represents approximately 12% of the robotic lawn mower market, with China, Japan, and South Korea as the primary demand centers. China has emerged as both a major manufacturing hub and a fast-adoption domestic market, hosting globally competitive manufacturers including Shenzhen Mammotion Technologies, Globe Tools Group, Segway Inc. as a Ninebot subsidiary, EcoFlow Technology, FJDynamics, and Zhuhai Kelitong.

Japan and South Korea face notable labor cost pressures in urban outdoor maintenance operations, creating institutional demand for autonomous residential and municipal mowing solutions. South Korea's robotic lawn mower market is supported by high consumer awareness of smart home technologies and a government policy environment promoting green technology adoption, with the market projected to demonstrate approximately 12% CAGR over the medium term. Mammotion's LUBA series, featuring AWD configuration and RTK navigation, has gained commercial traction globally from its Chinese engineering base, while Segway-Ninebot's Navimow i Series launch in the U.S. market reflects East Asian manufacturers' increasingly aggressive international expansion strategies targeting the Robotic Lawn Mower Market.

Competitive Landscape

The global robotic lawn mower market exhibits a moderately consolidated to oligopolistic structure, where a few dominant players hold a significant share while several emerging companies contribute to competitive intensity. Established players such as Husqvarna Group, Honda, STIGA, Robert Bosch GmbH, Deere & Company, and Positec Group Ltd. dominate the market through strong brand positioning, extensive distribution networks, and continuous technological innovation.

Competition is primarily driven by advancements in AI-based navigation, wire-free technology, and battery efficiency, with leading companies heavily investing in R&D to differentiate their offerings. While top players maintain leadership through scale and innovation, the market also sees participation from regional and niche manufacturers focusing on cost-effective and application-specific solutions.

Key Developments

- In March, 2026, STIGA introduced the APX Pro, an AI-powered autonomous robotic lawn mower designed for large-scale professional applications such as sports fields, municipalities, and golf courses. The model integrates advanced technologies including GPS-RTK, LiDAR, AI vision systems, and a high-capacity battery platform, enabling coverage of up to 27,000 m² with real-time adaptive navigation. This launch strengthens STIGA’s position in the high-performance, commercial robotic lawn care segment.

- In October, 2025, Husqvarna Group announced the launch of seven new robotic lawnmowers featuring advanced AI Vision technology and night-time IR camera capabilities for its 2026 lineup. The new models enable wire-free installation, precise navigation, and smart obstacle detection, catering to both residential and commercial lawn sizes. This development strengthens the company’s position in intelligent and automated lawn care solutions.

- In October 2025, Honda unveiled its ProZision Autonomous battery-powered riding lawn mower at Equip Exposition 2025, marking its entry into advanced autonomous lawn care solutions. The model integrates GNSS-based navigation along with radar and LiDAR sensors for 360-degree obstacle detection and route optimization, enabling fully autonomous mowing operations. This development highlights Honda’s expansion into intelligent, battery-powered lawn care technologies targeting professional landscaping efficiency.

Companies Covered in Robotic Lawn Mower Market

- Husqvarna AB

- ANDREAS STIHL AG & Co. KG

- Honda Motor Co., Ltd.

- Deere & Company

- Robert Bosch GmbH

- Positec Technology Co., Ltd.

- STIGA S.p.A. (3i Group plc)

- Globe Tools Group Co., Ltd.

- Segway Inc. (Ninebot Ltd.)

- Shenzhen Mammotion Technologies Co., Ltd.

- EcoFlow Technology Inc.

- FJDynamics International Ltd.

- Yamabiko Corporation

Frequently Asked Questions

The global Robotic Lawn Mower Market is projected to be valued at US$ 7.5 Bn in 2026.

The Autonomous segment is expected to account for approximately 68% of the Global Robotic Lawn Mower Market by Level of Autonomy in 2026.

The market is expected to witness a CAGR of 11.4% from 2026 to 2033.

Robotic lawn mower market growth is driven by the rapid adoption of AI-enabled wire-free technologies, rising labor shortages in landscaping, and increasing regulatory push for battery-electric, low-noise autonomous equipment.

Key opportunities in the robotic lawn mower market are driven by expanding PV park vegetation management and growing municipal demand under smart city infrastructure programs requiring large-scale autonomous mowing solutions.

Key players in the Robotic Lawn Mower Market include Husqvarna Group, Honda, STIGA, Robert Bosch GmbH, Deere & Company, and Positec Group Ltd.