- Renewable Energy

- Renewable Diesel Market

Renewable Diesel Market Size, Share, and Growth Forecast 2026 - 2033

Renewable Diesel Market by Feedstock (Soybean Oil, Palm Oil, Animal Fats, Vegetable Oils, Used Cooking Oil), Application (Transportation Fuel, Aviation (SAF), Marine, Industrial Use, Power Generation, Others), by Regional Analysis, 2026 - 2033

Renewable Diesel Market Size and Trend Analysis

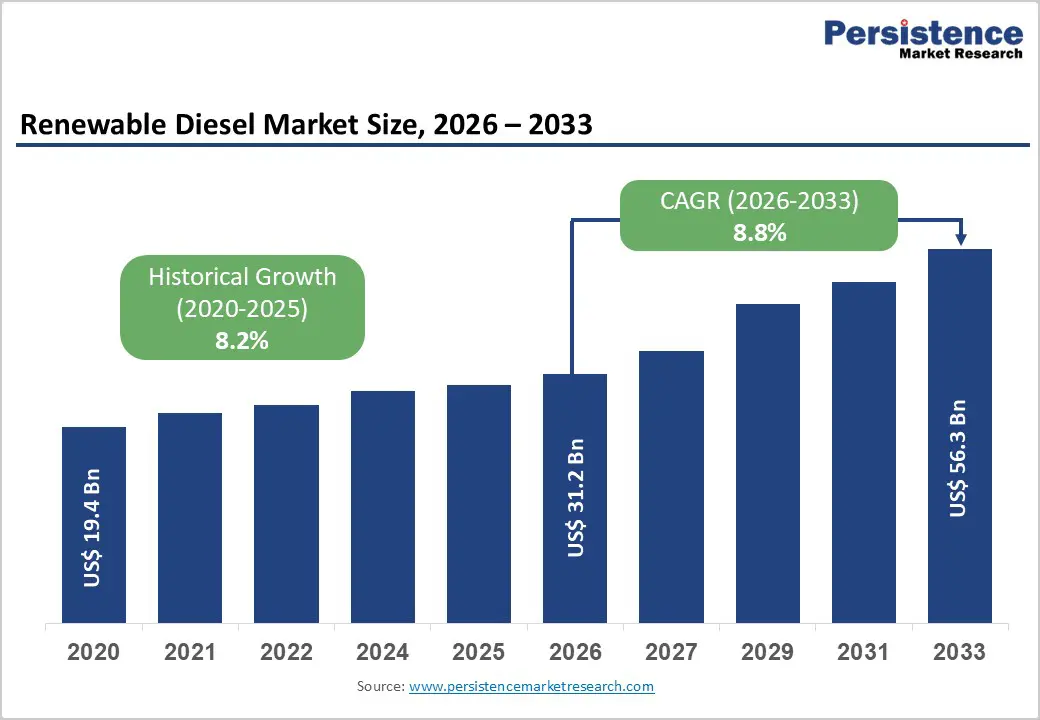

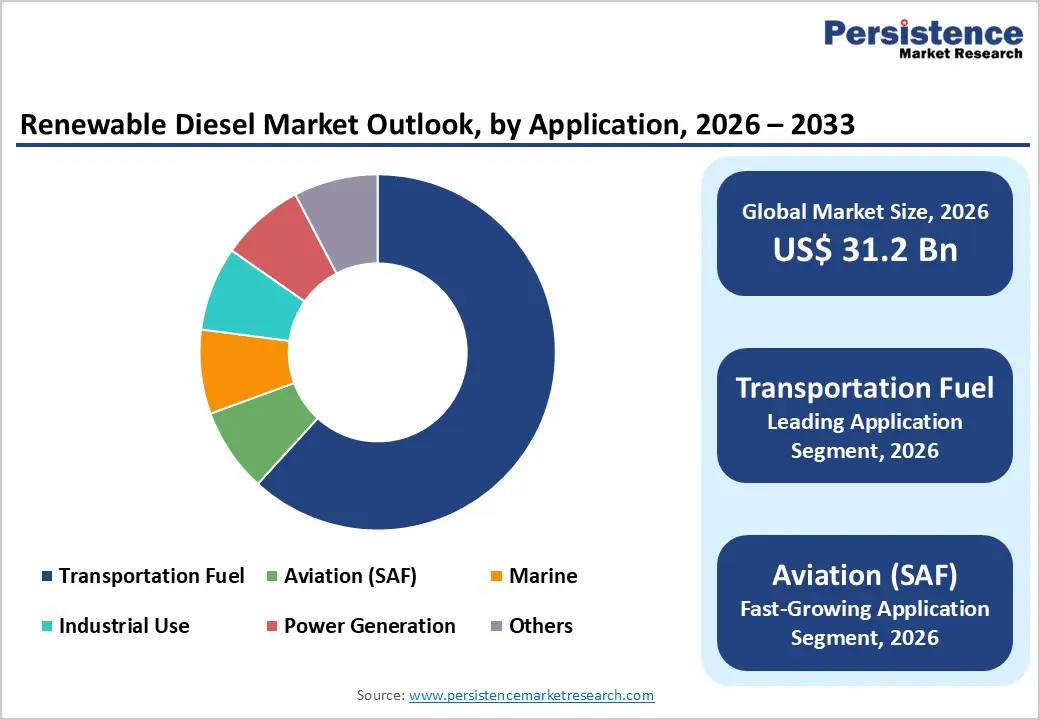

The global Renewable Diesel market size is expected to be valued at US$ 31.2 billion in 2026 and projected to reach US$ 56.3 billion by 2033, growing at a CAGR of 8.8% between 2026 and 2033.

Surging global demand for low-carbon transportation fuels, anchored by mandatory policy frameworks such as the U.S. Renewable Fuel Standard (RFS) and California's Low Carbon Fuel Standard (LCFS), is the primary catalyst propelling this growth. Renewable diesel's chemical identity with petroleum diesel, enabling direct drop-in use across existing engines and pipelines, gives it a decisive advantage over conventional biodiesel. Furthermore, expanding refinery conversion projects, record investments in HEFA (Hydroprocessed Esters and Fatty Acids) technology, and growing corporate net-zero pledges from logistics, aviation, and marine sectors are collectively reinforcing robust demand across all major geographies through 2033.

Key Industry Highlights

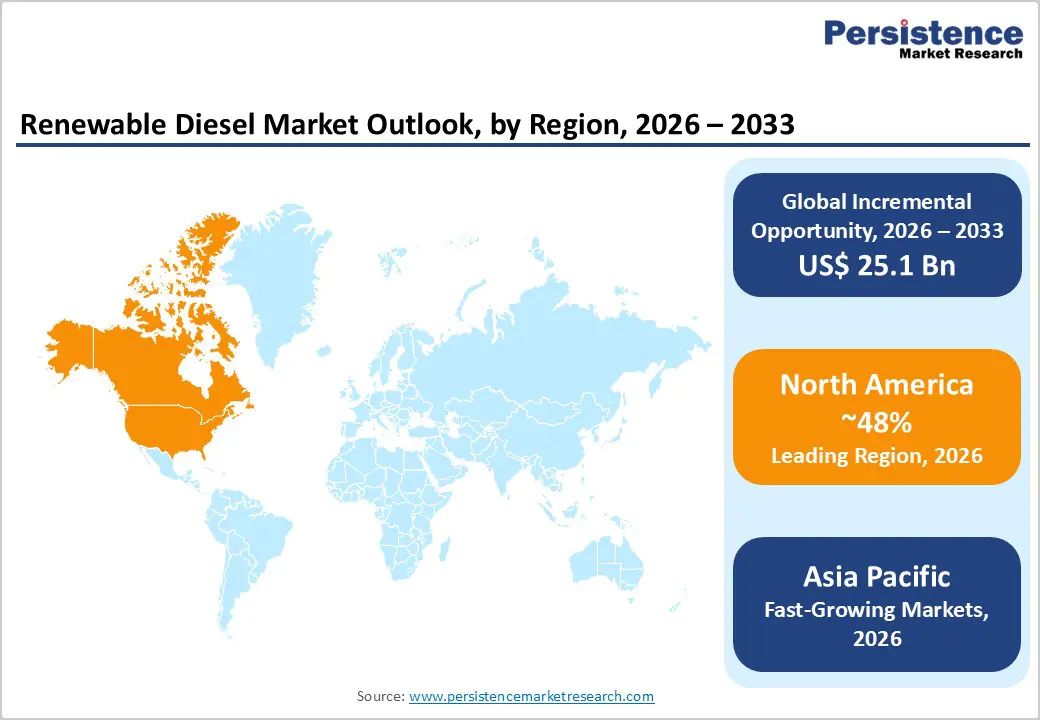

- Leading Region: North America, particularly the United States, leads the global renewable diesel market with roughly 48% share in 2025, anchored by the federal Renewable Fuel Standard (RFS) and California's LCFS, which together drive billions in annual production investment and blending mandates.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, fueled by China's 14th Five-Year Plan biofuel targets, India's National Biofuel Policy 5% blending mandates, and Neste's Singapore refinery serving as a strategic production hub.

- Dominant Segment: Vegetable oils hold 57% feedstock share in 2025 owing to high energy density, established soybean and canola supply chains, and HEFA process compatibility, making them the preferred low-carbon-intensity feedstock for major biorefineries globally.

- Fastest Growing Segment: The aviation SAF sub-segment is the fastest growing application, driven by EU's ReFuelEU mandates, IATA's 10% SAF target by 2030, and large-scale HEFA-SAF investments by Diamond Green Diesel, Neste, Shell, and TotalEnergies.

- Key Market Opportunity: Marine and industrial decarbonization represents a high-value opportunity, as the IMO's 50%-by-2050 GHG reduction mandate and growing utility-sector commitments of over US$ 116 billion annually create durable incremental demand beyond road transport.

| Key Insights | Details |

|---|---|

|

Renewable Diesel Market Size (2026E) |

US$ 31.2 Billion |

|

Market Value Forecast (2033F) |

US$ 56.3 Billion |

|

Projected Growth CAGR (2026–2033) |

8.8% |

|

Historical Market Growth (2020–2025) |

8.2% |

Market Dynamics

Market Growth Drivers

Robust Regulatory Mandates and Fiscal Incentives Fueling Demand

Government-backed policy frameworks remain the most powerful demand accelerator for the global renewable diesel market. In the United States, the Environmental Protection Agency (EPA) finalized biomass-based diesel Renewable Volume Obligations (RVOs) for 2026–2027 at approximately 5.25 billion gallons, a significant increase from 3.35 billion gallons in 2025, directly mandating higher blending volumes. Complementarily, the Inflation Reduction Act of 2022 (IRA) extended and enhanced biomass-based diesel production tax credits, catalyzing over US$ 6 billion in new refinery investments. Across Europe, the EU Renewable Energy Directive (RED III) targets a 29% share of renewables in transport energy by 2030, creating a structural pull for renewable diesel. These interlocking legislative pillars are providing long-term revenue visibility, incentivizing capital deployment, and anchoring multi-year offtake agreements between producers and large fleet operators.

Expanding Production Capacity and Refinery Conversions

A sweeping wave of refinery conversions and greenfield biorefinery investments is significantly enlarging the global supply base for renewable diesel. According to the U.S. Energy Information Administration (EIA), U.S. renewable diesel production capacity surpassed 2.6 billion gallons per year (gal/y) as early as 2022, with projections estimating a potential rise to nearly 5.9 billion gal/y by 2025 if all announced projects were completed. Major players such as Marathon Petroleum and Chevron have repurposed conventional petroleum refineries into dedicated renewable diesel facilities, dramatically reducing capital expenditure compared to building new plants. In Canada, Alberta granted a tax incentive for a US$ 507 million renewable diesel facility by Imperial Oil, with a daily output of 20,000 barrels. These capacity expansions are progressively reducing unit production costs, improving supply chain resilience, and positioning the market for sustained double-digit volume growth globally.

Market Restraints

Feedstock Supply Constraints and Price Volatility

Despite strong demand, feedstock availability and cost volatility represent a significant headwind for the renewable diesel market. The rapid scaling of U.S. production has turned the country into a net importer of soybean oil, a structural shift reported by the USDA in 2023, as domestic refining capacity outpaced domestic oilseed crop output. Soybean oil prices surged over 40% between 2020 and 2023, squeezing producer margins. Animal fats and Used Cooking Oil (UCO) supply chains remain fragmented and geographically concentrated, limiting scalability. As multiple large biorefineries compete for the same limited pool of low-carbon-intensity feedstocks, procurement costs remain elevated and unpredictable, directly undermining the economic competitiveness of renewable diesel versus conventional petroleum diesel.

High Capital Intensity and Uncertain Policy Continuity

The capital-intensive nature of renewable diesel infrastructure presents a structural barrier to entry. Converting a petroleum refinery requires investments ranging from US$ 300 million to over US$ 1 billion, with extended payback periods. Moreover, policy uncertainty, exemplified by debates over the scope of the RFS, periodic reviews of LCFS credit values, and changes in import tariff structures, creates risk for long-term project financing. In 2025, the EIA reported a notable decline in U.S. renewable diesel imports, averaging just 5,000 barrels per day (b/d) in early 2025, down from 33,000 b/d in the same period of 2024, partly attributed to shifting federal tax credit structures, underscoring how policy adjustments can rapidly disrupt trade flows and investment plans.

Market Opportunities

Aviation Sector Demand for Sustainable Aviation Fuel (SAF)

The rapidly growing mandate for Sustainable Aviation Fuel (SAF) represents one of the most transformative opportunities for renewable diesel producers. HEFA-based SAF, derived from the same feedstock pathways as renewable diesel, is currently the dominant commercially available SAF technology, enabling producers to leverage existing assets. The International Air Transport Association (IATA) targets 10% of global aviation fuel to be SAF by 2030, and the EU's ReFuelEU Aviation regulation mandates a 2% SAF blend by 2025, escalating to 70% by 2050. In late 2024, Diamond Green Diesel (DGD) completed a SAF expansion project at its Port Arthur, Texas plant capable of producing up to 235 million gallons of neat SAF per year, establishing it as one of the world's largest SAF producers and demonstrating the enormous upside available to renewable diesel manufacturers willing to pivot toward aviation-grade fuel production.

Marine and Industrial Decarbonization as Emerging Revenue Streams

Beyond road transportation, the marine and industrial sectors are emerging as high-growth application areas for renewable diesel. The International Maritime Organization (IMO) has set a target to reduce shipping's total annual GHG emissions by at least 50% by 2050 compared to 2008 levels, spurring demand for drop-in low-carbon fuels. Renewable diesel's direct compatibility with marine diesel engines, without any hardware modification, makes it an immediately deployable solution for ship operators seeking compliance. Simultaneously, in power generation, a US$ 116 billion annual commitment to clean energy by global utility firms pledged in September 2024 is creating backup and peaking power opportunities for renewable diesel. Industrial facilities seeking to decarbonize off-road fleets, construction machinery, and mining equipment represent an additional addressable market, expanding the commercial opportunity well beyond conventional road transport segments.

Category-wise Insights

Feedstock Analysis

Vegetable oils represent the dominant feedstock category in the global renewable diesel market, commanding approximately 57% of market share in 2025. This leadership is rooted in the high energy density, favorable fatty acid profiles, and established global supply chains of crops such as soybean, canola, rapeseed, and palm. Soybean oil is particularly dominant in North America, where it accounts for a substantial portion of hydroprocessing feedstock at major U.S. biorefineries. According to the EIA and USDA, the U.S. became a net importer of soybean oil in 2023 due to booming renewable diesel capacity, underscoring the scale of demand. Vegetable oils are compatible with existing HEFA refining infrastructure, requiring minimal modification. Their renewable carbon content and ability to deliver verified Greenhouse Gas (GHG) reductions under programs like the RFS and LCFS further reinforce their preferred status among producers seeking maximum RIN credit value.

Application Analysis

Transportation fuel remains the dominant application segment for renewable diesel, holding approximately 63% of global market share in 2025. The transportation sector's dominance is driven by the product's chemical equivalence to petroleum diesel, enabling seamless adoption across heavy-duty trucking, public transit fleets, freight logistics, and agriculture without any engine modification. Major logistics operators and fleet managers are increasingly mandating renewable diesel use in response to Environmental, Social, and Governance (ESG) commitments and customer sustainability requirements. As per US EPA, over 65% of transport distillate consumed in California in Q3 2024 was renewable diesel, a testament to the fuel's entrenched position in commercial transport. Policy frameworks such as the LCFS and the federal RFS generate significant financial incentives for fleet operators to prioritize renewable diesel procurement, further cementing its dominant position through 2033.

Regional Insights

North America Renewable Diesel Market Trends and Insights

North America is the undisputed leader in the global renewable diesel market, accounting for approximately 48% of total market share in 2025. The United States alone commands over 90% of the regional market, powered by the complementary impact of the federal Renewable Fuel Standard (RFS) and state-level programs, most prominently California's Low Carbon Fuel Standard (LCFS), which together generate robust economic incentives for producers and consumers alike. The EPA's finalized RVOs for 2026–2027 at ~5.25 billion gallons signal continued policy momentum.

The U.S. innovation ecosystem is unparalleled: major projects by Diamond Green Diesel, Marathon Petroleum, Phillips 66, and Chevron have transformed former petroleum refineries into world-scale renewable fuel facilities. Canada is accelerating too, with Alberta granting fiscal incentives to Imperial Oil's US$ 507 million facility, expected to produce 20,000 b/d. The region's mature logistics infrastructure, deep capital markets, and growing corporate fleet sustainability mandates ensure North America's market leadership through 2033.

Europe Renewable Diesel Market Trends and Insights

Europe represents the second-largest market for renewable diesel globally, driven by the European Union's Renewable Energy Directive III (RED III), which mandates a minimum 29% renewable energy share in transport by 2030. Finland hosts Neste, the world's largest producer of renewable diesel and SAF, whose Rotterdam and Singapore refineries collectively serve European and global markets. Sweden's Preem AB is investing heavily in converting its refinery capacity to biofuels. In Germany, the Greenhouse Gas Reduction Quota (THG-Quote) incentivizes blending, while France and Spain are expanding blending mandates for road and aviation fuels.

The ReFuelEU Aviation regulation is stimulating SAF-grade renewable diesel demand across European airlines. Shell's 820,000-tonne-per-year biofuels facility at its Rotterdam Energy and Chemicals Park is expected to be among Europe's largest SAF and renewable diesel production sites. Eni's Gela and Venice biorefineries in Italy are also scaling output from waste-based feedstocks. The strong regulatory harmonization across member states, combined with growing corporate sustainability procurement policies, positions Europe as the fastest-growing region for renewable diesel on a percentage basis through 2033.

Asia Pacific Renewable Diesel Market Trends and Insights

Asia Pacific is the fastest-growing regional market for renewable diesel, propelled by ambitious national decarbonization targets in China, India, and ASEAN economies. China's 14th Five-Year Plan prioritizes energy transition and biofuel integration into transportation, while India's National Biofuel Policy targets a 5% blending of advanced biofuels in diesel by 2030. Neste's Singapore refinery, one of the world's largest single-site renewable diesel facilities, serves as a critical supply hub for the entire Asia Pacific region. Indonesia and Malaysia provide a large and growing supply of palm oil-based feedstocks, offering a regional feedstock advantage.

Japan is emerging as an important market under its Green Growth Strategy, targeting carbon neutrality by 2050 with significant investment in biofuel infrastructure. South Korea has introduced a Renewable Fuel Standard analogous to the U.S. model. Australia is pursuing biofuel blending policy reforms. The region's lower labor and construction costs relative to Western markets provide a manufacturing cost advantage for new greenfield refineries. Combined with rapid urbanization, growing freight demand, and government net-zero pledges, Asia Pacific is set to record the highest CAGR during the 2026–2033 forecast period.

Competitive Landscape

The global renewable diesel market demonstrates a moderately consolidated structure, with a limited number of large integrated players accounting for a significant share of overall capacity. Market concentration is driven by high capital requirements, access to feedstock supply chains, and regulatory compliance capabilities, creating entry barriers for smaller participants. Leading companies continue to expand through refinery-to-biorefinery conversions, enabling rapid capacity addition while optimizing existing infrastructure.

Strategically, the market is evolving toward feedstock diversification to mitigate price volatility and ensure supply security, alongside increasing adoption of waste-based and low carbon intensity inputs. Long-term offtake agreements with aviation, logistics, and marine sectors are emerging as a key revenue stabilization strategy. Additionally, players are focusing on product diversification, particularly into sustainable aviation fuel, while investing in advanced processing technologies, carbon capture integration, and circular economy solutions to enhance sustainability positioning and regulatory alignment.

Key Developments

- February 2026: Aemetis Inc. announced that its India subsidiary began biodiesel deliveries under a US$ 24 million allocation to supply over 27 million liters to state-owned OMCs, supporting India’s target to increase biodiesel blending to 5%.

- August 2025: Imperial Oil commenced renewable diesel production at its Strathcona refinery in Canada, with a capacity of around 20,000 barrels per day, supplying lower-emission fuel to regional markets using locally sourced bio-feedstocks.

- February 2025: Chevron Corporation announced that its Geismar biorefinery renewable diesel expansion project in Louisiana entered final commissioning, aiming to increase production capacity from about 90 million to 340 million gallons per year.

Companies Covered in Renewable Diesel Market

- BP

- Cargill

- Carolina Renewable Products

- Chevron Corporation

- Diamond Green Diesel (DGD)

- Eni S.p.A.

- Gevo, Inc.

- Shell plc

- TotalEnergies SE

- Valero Energy Corporation

- Marathon Petroleum Corporation

- Neste Corporation

- Petrobras

- Phillips 66

- Preem AB

- World Energy

- Darling Ingredients Inc.

- Renewable Energy Group (REG)

- PBF Energy Inc.

- Repsol S.A.

Frequently Asked Questions

The global Renewable Diesel market is valued at US$ 31.2 billion in 2026 and is projected to reach US$ 56.3 billion by 2033 at a CAGR of 8.8%.

Key drivers include government blending mandates, compatibility with existing diesel infrastructure, corporate net-zero goals, and growing SAF demand.

North America leads the market with around 47–48% share, driven by strong policy support and refinery investments in the United States.

The biggest opportunity lies in Sustainable Aviation Fuel (SAF) production using existing renewable diesel infrastructure.

Major players include Neste, Diamond Green Diesel, Valero, Chevron, Phillips 66, Marathon Petroleum, Shell, TotalEnergies, BP, Eni, Preem, Gevo, Petrobras, and Cargill.