- Renewable Energy

- Waste Recycling Services Market

Waste Recycling Services Market Size, Share, and Growth Forecast, 2026 - 2033

Waste Recycling Services Market by Source (Industrial, Residential, Others), Material Type (Paper & Paperboard, Plastics, Others), Recycling Process, End-User Industry, and Regional Analysis for 2026 - 2033

Waste Recycling Services Market Size and Trends Analysis

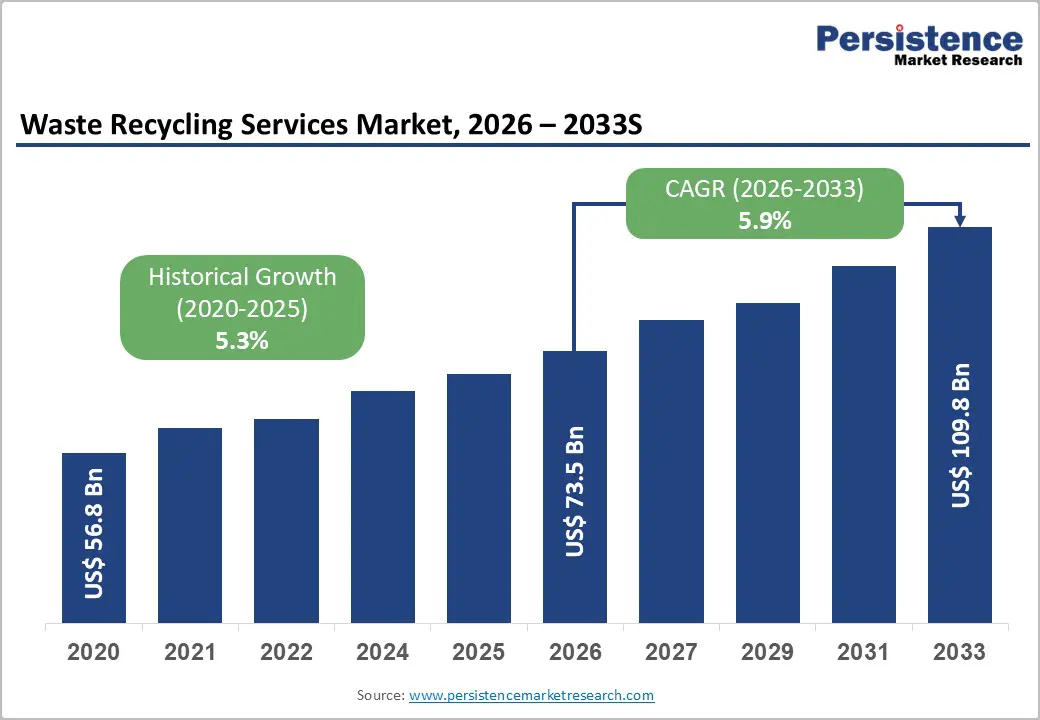

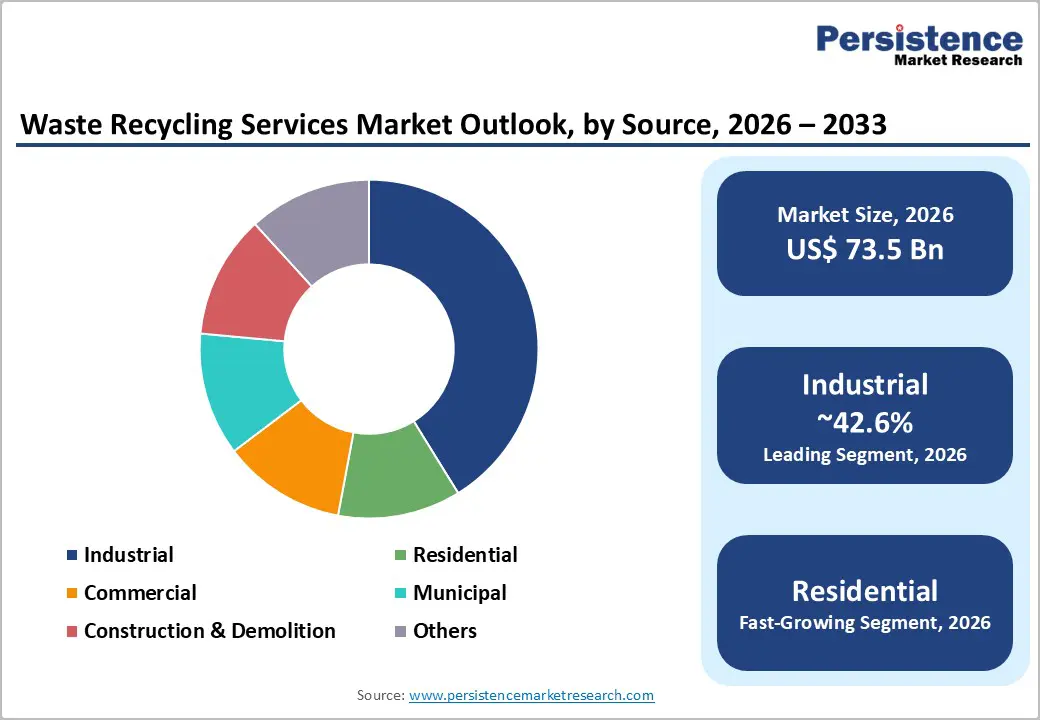

The global waste recycling services market size is likely to be valued at US$ 73.5 billion in 2026 and is expected to reach US$109.8 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033, driven by the continuous rise in global waste generation, stricter regulatory enforcement of recycling targets, and increasing investments in advanced sorting and processing technologies.

Rapid urbanization, industrial expansion, and evolving consumption patterns are contributing to higher waste volumes worldwide. In response, governments are implementing more stringent recycling mandates and limiting landfill usage. At the same time, advancements such as AI-driven sorting systems and chemical recycling technologies are enhancing material recovery efficiency. These trends are shifting value creation toward recycling service providers, especially those offering advanced processing capabilities and integrated service solutions.

Key Industry Highlights:

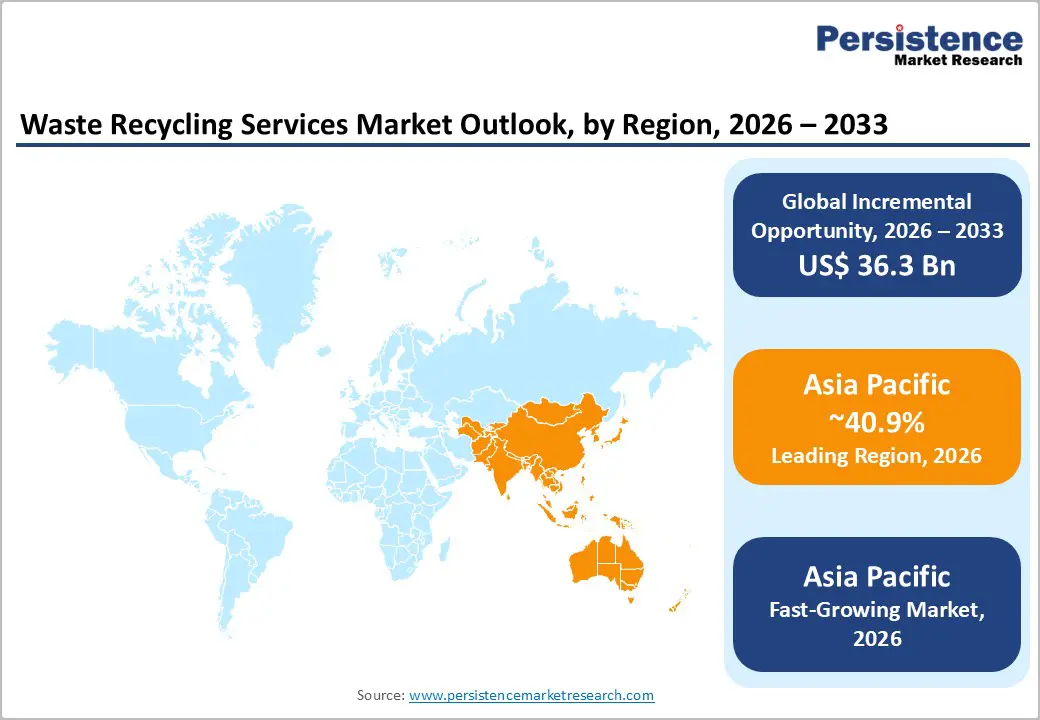

- Leading Region: Asia Pacific is projected to lead the market with approximately 40.9% share, supported by strong manufacturing activity, rapid urbanization, and expanding recycling infrastructure across China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by increasing waste generation, government-led recycling initiatives, and rising investments in modern waste management systems, particularly in emerging economies.

- Investment Plans: Major industry players are investing heavily in advanced sorting technologies, chemical recycling, and renewable energy integration. Companies such as Waste Management, Veolia, and Republic Services are allocating multi-billion-dollar capital expenditures toward automation, material recovery facilities, and circular economy infrastructure.

- Dominant Source: Industrial source is anticipated to dominate the market with approximately 42.6% share, driven by high-volume, low-contamination waste streams and long-term contractual agreements with manufacturing industries.

- Leading Material Type: Paper & paperboard is estimated to account for approximately 36.4% of the market share, supported by established recycling systems, high recovery rates, and strong demand from the packaging and logistics sectors.

| Key Insights | Details |

|---|---|

| Waste Recycling Services Market Size (2026E) | US$73.5 Bn |

| Market Value Forecast (2033F) | US$109.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Tightening and EPR Adoption

Stringent environmental regulations and the global expansion of Extended Producer Responsibility (EPR) programs are creating sustained demand for recycling services. Governments are implementing higher recycling targets, landfill diversion policies, and packaging compliance mandates. These frameworks require producers to manage post-consumer waste, often through third-party service providers. As a result, recycling companies benefit from predictable demand and long-term contracts. Regulatory certainty supports capital-intensive investments in infrastructure such as material recovery facilities (MRFs) and advanced recycling technologies, while also encouraging public-private partnerships and outsourcing of municipal waste management services.

Technology-Driven Efficiency Improvements

Advancements in sorting technologies, including AI-powered optical sorters, robotics, and sensor-based separation, are significantly improving recovery rates and reducing contamination. These technologies enable higher throughput and better-quality output materials, which command higher market value. Improved operational efficiency reduces processing costs per ton and enhances profitability. Companies investing in automation gain a competitive advantage by increasing yield and minimizing labor dependency, particularly in handling complex waste streams such as plastics and electronic waste.

Corporate Sustainability and Circular Economy Initiatives

Global corporations are increasingly adopting circular economy principles, setting targets for recycled content usage and waste reduction. These commitments are driving demand for high-quality recycled materials, encouraging long-term procurement agreements with recycling service providers. Stable demand from corporate buyers enables recyclers to invest in advanced processing technologies and expand capacity. Strategic collaborations between recyclers and manufacturers are also emerging, supporting closed-loop supply chains and enhancing revenue predictability.

Barrier Analysis - Feedstock Contamination and Inefficiencies in Collection Systems

High contamination levels in mixed waste streams reduce recovery efficiency and lower the value of recycled materials. Inadequate source segregation leads to increased processing costs and lower-quality outputs. Contamination can reduce recoverable value by 10-30%, depending on material type, negatively affecting margins and extending payback periods for new facilities.

High Capital Requirements and Operational Complexity

Modern recycling infrastructure requires significant capital investment, particularly for advanced mechanical and chemical recycling systems. Smaller operators often face financial constraints, limiting their ability to scale operations. High upfront costs and uncertain returns, driven by fluctuations in recycled material prices, can delay project development and limit market expansion in emerging regions.

Opportunity Analysis - Expansion of Chemical and Advanced Recycling Technologies

Chemical recycling technologies offer solutions for processing complex and contaminated plastic waste that cannot be handled through conventional mechanical methods. These technologies, including pyrolysis and depolymerization, are gaining traction due to increasing demand for high-quality recycled feedstocks that meet virgin-equivalent standards. As regulatory pressure on plastic waste intensifies, industries are actively seeking scalable solutions that support circular material use. Opportunity: Companies can integrate upstream collection with downstream processing to capture additional value across the supply chain. Strategic partnerships with petrochemical firms and manufacturers can further secure long-term offtake agreements, reduce demand volatility, and improve return on investment for advanced recycling infrastructure.

Urbanization and Infrastructure Development in Emerging Markets

Rapid urban growth in developing economies is significantly increasing waste generation, particularly in densely populated cities with limited existing infrastructure. Governments are prioritizing the modernization of waste management systems, creating demand for efficient recycling and collection services. Many municipalities are transitioning toward outsourced or concession-based models to improve service delivery and operational efficiency. Service providers can enter these markets through public-private partnerships, leveraging modular and cost-efficient technologies to establish scalable operations. Early entry enables companies to build long-term contracts, benefit from policy support, and capture growing waste volumes as urban populations expand.

Service Diversification and Integrated Waste Management Solutions

Recycling companies are increasingly expanding into adjacent service areas such as waste-to-energy, composting, anaerobic digestion, and hazardous waste management to enhance their value proposition. This diversification allows firms to manage a broader range of waste streams while optimizing resource recovery. Offering integrated, end-to-end solutions strengthens customer relationships and improves contract retention by providing a single service provider for multiple waste needs. It also enables better asset utilization, reduces operational inefficiencies, and creates additional revenue streams, particularly in markets where comprehensive waste management services are still underdeveloped.

Category-wise Analysis

Source Insights

Industrial waste is anticipated to dominate the market with 42.6% of market share in 2026, due to its high volume, consistency, and strong economic value. Manufacturing sectors such as automotive, chemicals, electronics, and consumer goods generate large quantities of recyclable materials, including metals, plastics, and packaging waste. These streams are typically well-segregated at the source and exhibit lower contamination levels, making them more efficient and cost-effective to process. Long-term service agreements between recyclers and industrial clients ensure stable revenue streams and optimized logistics. For example, automotive manufacturers often partner with recycling firms to recover scrap metals and reuse materials within production cycles, while packaging companies implement closed-loop recycling systems for corrugated and plastic materials. This structured supply chain reinforces industrial waste as the backbone of recycling service revenues.

Residential waste is the fastest-growing segment, driven by expanding curbside collection programs, urban population growth, and increasing consumer awareness of recycling practices. Government initiatives promoting waste segregation at the household level, along with pay-as-you-throw (PAYT) schemes, are encouraging higher participation rates. Service providers are investing in smart bins, route optimization software, and advanced material recovery facilities (MRFs) to handle rising volumes efficiently. For instance, several municipalities in North America and Europe are upgrading single-stream systems to dual-stream collection to reduce contamination and improve material quality. In emerging economies, pilot projects focused on door-to-door segregated waste collection are further accelerating adoption. These factors collectively support sustained growth in the residential segment.

Material Type Insights

The paper and paperboard segment continues to lead with 36.4% of market share in 2026, due to their high recyclability, well-established collection systems, and consistent demand from packaging and paper manufacturing industries. The widespread use of corrugated boxes in e-commerce and logistics further strengthens this segment’s position. High recovery rates, relatively simple processing methods, and lower capital requirements make paper recycling highly cost-efficient. For example, large retailers and logistics companies have implemented dedicated paper recycling streams to recover corrugated packaging waste at distribution centers. Recycled paper is widely used in packaging, tissue, and printing applications, ensuring steady demand and relatively stable pricing dynamics across regions.

Plastic recycling is experiencing the fastest growth due to tightening environmental regulations and corporate commitments to incorporate recycled content into products. Governments are introducing mandates for minimum recycled content in packaging, while consumer goods companies are investing in sustainable packaging solutions. Technological advancements in sorting, washing, and chemical recycling are improving the recyclability of complex and multi-layer plastics. For instance, beverage companies are increasingly adopting recycled PET (rPET) in bottle manufacturing, while chemical recycling projects are being developed to process mixed plastic waste into high-quality feedstock. Growth is particularly strong in regions investing in advanced recycling infrastructure and where strong policy support aligns with corporate sustainability goals.

Regional Insights

North America Waste Recycling Services Market Trends - Tech-Driven Recycling Expansion & EPR-Led Market Consolidation

North America represents a significant share of the market, with the U.S. leading due to its advanced waste management infrastructure, high per-capita waste generation, and strong presence of large private operators. The region benefits from a mature ecosystem where municipalities widely outsource waste collection and recycling services to specialized firms, enabling operational efficiency and scale. Major players such as Waste Management and Republic Services continue to expand their recycling capabilities through investments in high-tech material recovery facilities (MRFs) and renewable energy integration.

Key growth drivers include corporate sustainability commitments, increasing demand for recycled content, and technological innovation in sorting and processing. For instance, Waste Management has announced multi-billion-dollar investments in automated recycling facilities and renewable natural gas projects, improving material recovery rates and reducing landfill dependency. The regulatory environment, which varies significantly across states, creates both complexity and opportunity. States, including California, are implementing stricter recycling and extended producer responsibility (EPR) policies, pushing service providers to upgrade infrastructure. Strategic acquisitions, including the integration of Stericycle assets, are strengthening capabilities in hazardous and specialized waste streams, further consolidating the market and enhancing service diversification.

Europe Waste Recycling Services Market Trends - Circular Economy Policies & AI-Enabled Recycling Optimization

Europe is characterized by stringent environmental regulations, ambitious recycling targets, and a strong policy framework supporting circular economy initiatives. Countries such as Germany, the U.K., France, and Spain have well-developed recycling infrastructures and high levels of public participation in waste segregation programs. The region benefits from harmonized regulations under EU directives, which create a consistent demand for compliance-driven recycling services.

Growth in Europe is driven by landfill restrictions, extended producer responsibility schemes, and strong consumer awareness regarding sustainability. Leading companies such as Veolia and SUEZ are actively investing in advanced recycling technologies and expanding their operational footprint through strategic partnerships and acquisitions. For example, ongoing consolidation and portfolio optimization activities by Veolia following its integration of SUEZ assets have strengthened its position in the European recycling market. At the same time, technology providers such as Tomra Group are deploying AI-based sorting systems across facilities to improve material purity and meet stringent EU recyclate quality standards. These developments are accelerating the transition toward a more efficient and technology-driven recycling ecosystem across the region.

Asia Pacific Waste Recycling Services Market Trends - Urbanization-Driven Growth & Policy-Led Recycling Infrastructure Development

Asia Pacific is projected to lead the global waste recycling services market with approximately 40.9% share and is the fastest-growing region, driven by rapid urbanization, industrialization, and population expansion. Countries such as China, India, and Japan are major contributors to regional waste generation and recycling demand. The region’s growth is further supported by expanding manufacturing sectors, which create strong demand for recycled raw materials. Governments across Asia Pacific are implementing policies to modernize waste management systems and promote recycling.

For instance, India has introduced nationwide initiatives to improve waste segregation and formalize recycling systems, encouraging private sector participation. In China, restrictions on waste imports have accelerated domestic recycling capacity development, prompting investments in local processing infrastructure. Meanwhile, Veolia and SUEZ are expanding their presence in the region through joint ventures and municipal contracts, particularly in Southeast Asia. In Japan, advanced recycling systems for electronics and plastics are being deployed to support circular economy goals. These developments, combined with increasing adoption of public-private partnerships and technology-driven solutions, are reinforcing Asia Pacific’s leadership and accelerating its transition toward sustainable waste management practices.

Competitive Landscape

The global waste recycling services market is semi-consolidated, with a mix of global leaders and regional players. Large companies benefit from economies of scale, advanced technology, and strong financial resources, while smaller firms focus on niche markets and localized services. Competitive differentiation is driven by service integration, operational efficiency, and regulatory compliance capabilities.

Key strategies include vertical integration, technology adoption, and market expansion through acquisitions and partnerships. Companies are focusing on improving operational efficiency, securing long-term contracts, and diversifying service offerings to strengthen their competitive position.

Key Industry Developments

- In November 2025, Veolia announced the acquisition of U.S.-based hazardous waste company Clean Earth from Enviri for approximately US$3 billion, aiming to significantly expand its hazardous waste treatment capacity and strengthen its position as a leading player in the U.S. recycling and environmental services market.

Companies Covered in Waste Recycling Services Market

- Waste Management

- Republic Services

- Veolia

- SUEZ

- Clean Harbors

- Waste Connections

- Covanta

- Remondis

- Biffa

- Renewi

- DS Smith

- Stericycle

- GFL Environmental

- Casella Waste Systems

- Paprec Group

- Hitachi Zosen Corporation

Frequently Asked Questions

The global waste recycling services market is estimated to be valued at US$73.5 billion in 2026.

The waste recycling services market is projected to reach US$109.8 billion by 2033.

Key trends include increasing adoption of chemical and advanced recycling technologies, expansion of integrated waste management solutions, rising corporate sustainability commitments, and growing investments in automation and AI-based sorting systems.

The industrial source segment leads the market, accounting for approximately 42.6% share, supported by consistent waste generation and long-term recycling contracts.

The waste recycling services market is expected to grow at a CAGR of 5.9% between 2026 and 2033.

Major players include Veolia, SUEZ, Republic Services, and Clean Harbors.