- Healthcare Services

- Drug Discovery Outsourcing Market

Drug Discovery Outsourcing Market Size, Share, and Growth Forecast 2026 - 2033

Drug Discovery Outsourcing Market by Service Type (Medicinal Chemistry Services, Biology Services), Drug Type (Small Molecules, Large Molecules), Therapeutic Area (Oncology, Infectious Disease), End-user, and Regional Analysis, 2026 - 2033

Drug Discovery Outsourcing Market Size and Trends Analysis

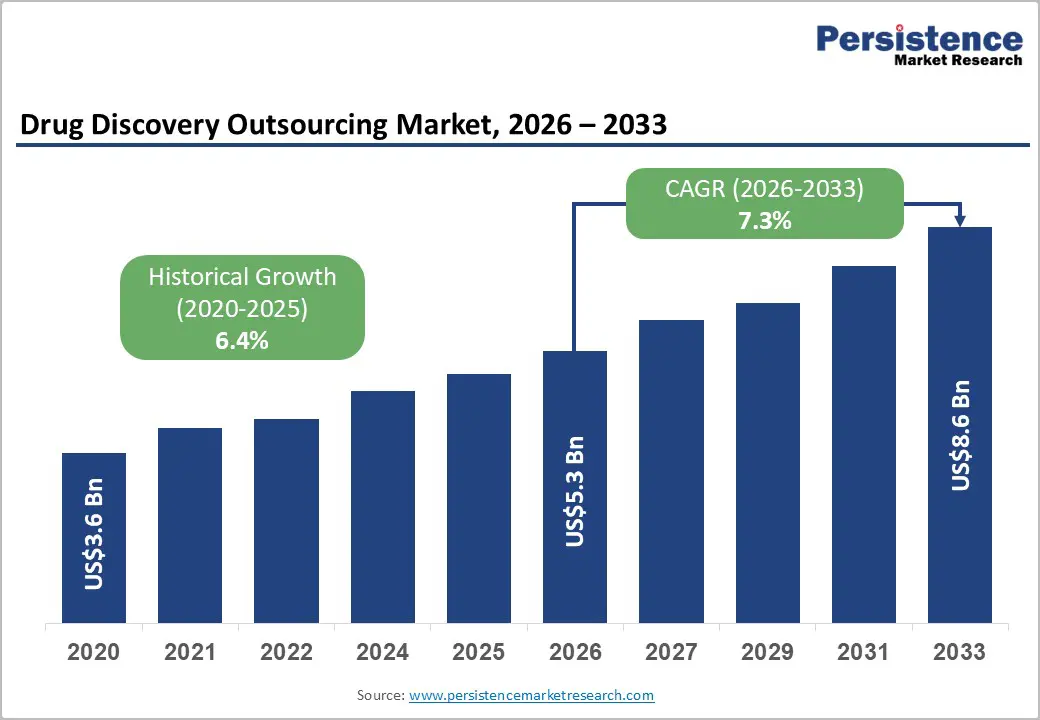

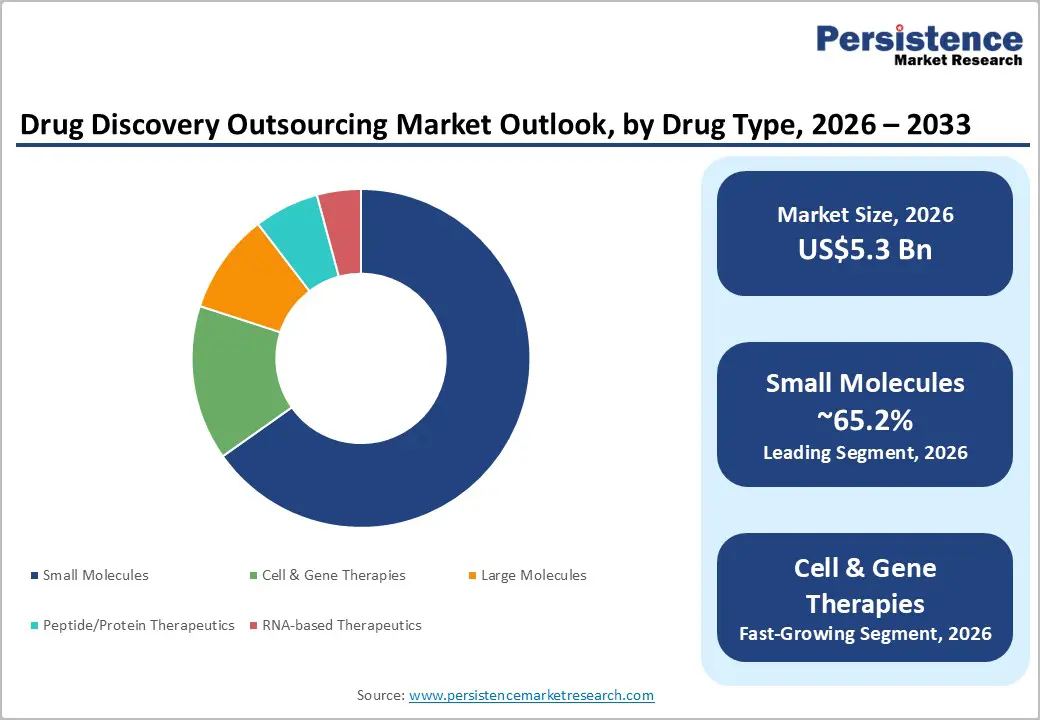

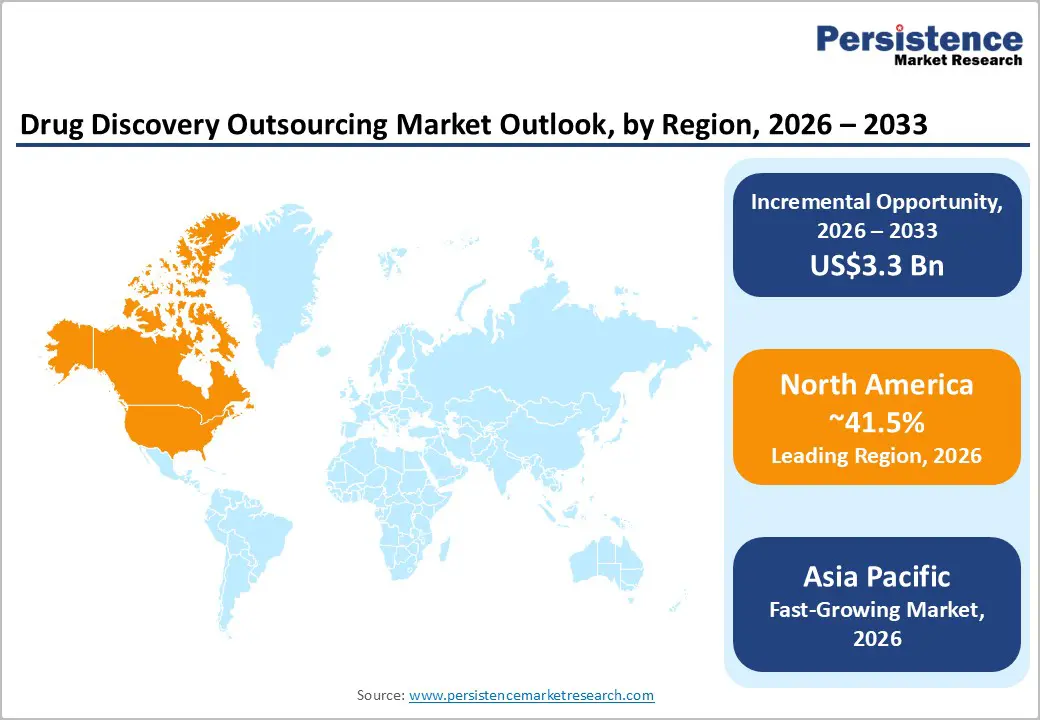

The global drug discovery outsourcing market size is likely to be valued at US$5.3 billion in 2026 and is expected to reach US$8.6 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by the increasing pressure on pharmaceutical and biotechnology companies to improve research and development productivity while reducing fixed infrastructure costs.

Key Industry Highlights

- Leading Service Type: Medicinal chemistry services, approximately 38.2% share in 2026, as drug developers heavily rely on outsourced lead optimization and compound synthesis.

- Dominant Drug Type: Small molecules, nearly 65.2% in 2026, as they have well-established regulatory pathways.

- Strategic Announcement: In March 2026, Jefferies named Sai Life Sciences its top CRDMO pick, citing its integrated model and growth trajectory, with a Buy rating and an INR 1,300 (US$15.3) price target. Sai Life Sciences also announced plans to hire over 700 professionals during 2026 to 2027, signaling continued expansion of operations.

- Leading Region: North America, with about 41.5% share in 2026, owing to its concentration of leading pharmaceutical companies and advanced CRO infrastructure.

- Fast-growing Region: Asia Pacific, as pharma companies are shifting outsourcing activities to countries such as India and China for cost-efficient research.

DRO Analysis

Driver - Surging Incidence of Chronic and Rare Diseases Fuels Drug Pipelines

The surge in chronic and rare disease cases is pushing pharma companies to build more complex drug pipelines, and most lack the internal capabilities to handle this alone. Rare diseases have become a prominent pipeline driver. According to the Food and Drug Administration’s (FDA) Office of Orphan Products Development, orphan drugs accounted for 47% of novel therapy approvals in 2024. That share jumped to 62.5% in 2025, making it the highest on record. Orphan drugs represented over 60% of novel therapies approved so far in 2025, which was a sharp rise from 47% in 2024 and 49% in 2023.

Diseases such as cancer, neurological conditions, and autoimmune disorders are equally pushing early-stage demand. Oncology, immunology, neurology, and cardiovascular conditions together represented 71% of the 5,318 clinical trials started in 2024. Three neurological conditions, namely, Alzheimer's, depression, and Parkinson's disease, each recorded over 200 new trial starts in the last five years. Since most rare disease programs require niche expertise in target identification, small-batch manufacturing, and regulatory navigation, sponsors are increasingly turning to CROs and CDMOs to fill these gaps.

Increasing Pharma and Biotech Research Investments to Boost Contract Services

High research and development budgets are not just funding more science, but they are influencing how that science gets done. Companies are now directing a large share of spending toward external partners instead of building in-house capacity. Research and development funding reached a 10-year high of US$102 billion in 2024, up sharply from US$71 billion in 2023, augmenting demand for novel therapeutics and modalities. Large pharma research and development spend grew 9.7% in 2024, with Eli Lilly and Novo Nordisk, buoyed by blockbuster GLP-1 drugs, contributing the most to that growth. This spending is translating directly into outsourcing demand.

Obesity clinical trials reached 101 starts in 2024 alone, a nine-fold increase over the past decade and a 77% jump versus 2023, with the active pipeline now holding 173 drugs from Phase I through post-approval. As pipelines become more complex, the cost and time required to build in-house capabilities make outsourcing the more viable path. By 2025, more than 65% of pharma firms reported shifting from internal manufacturing to CDMOs, showcasing how deeply research investment growth is feeding the outsourcing market.

Restraint - Steep Investment Costs for Unique Discovery Platforms

Running a competitive drug discovery CRO today requires far more than bench space. Platforms built around AI-supported molecular design, high-throughput screening, cryo-EM imaging, and automated synthesis demand substantial upfront capital. Keeping pace with these tools is not optional, as sponsors expect CROs to have them.

According to a report published in Drug Discovery World (Spring 2025), CROs need to continuously adopt AI infrastructure to remain relevant. Yet, several large CROs operate as aggregators of capacity and tend to invest only in more established technologies, leaving them at risk of falling behind as data-centric discovery becomes the norm. Rising digital transformation costs are increasingly pressuring mid-tier CROs, according to the CRO Industry Outlook 2026 published in Clinical Leader.

Opportunity - Increasing Regulatory Confidence in Outsourced Trial Data

Regulators are not just accepting CRO-generated data, but they are building formal frameworks to govern it. The ICH E6(R3) Good Clinical Practice guideline, adopted in January 2025 and formally incorporated into FDA guidance on September 9, 2025, responds to innovations such as decentralized clinical trials and digital health technologies. For CROs, this is a meaningful shift.

The updated guideline formally recognizes outsourced data governance as a shared responsibility between sponsors and CROs, lending more credibility to externally generated datasets in regulatory submissions. By early 2026, over 150 IND applications submitted to the FDA included AI-derived data or computationally predicted properties. This surging regulatory comfort is removing a long-standing barrier for sponsors who were hesitant to rely on CRO-generated data packages in high-stakes submissions.

Rise of Lean and No-Lab Biotech Models to Create Demand Base for CROs

Small and capital-efficient biotech companies are now the primary engine of new drug pipelines. Emerging biopharma companies, mostly pre-commercial, were responsible for 63% of clinical trial starts in 2024, up from 56% in 2019, according to IQVIA data cited in Contract Pharma. These firms rely entirely on CRO networks to run discovery, preclinical, and clinical work.

4M Therapeutics, for instance, is preparing clinical trials with an approximately US$10 million budget without owning a single laboratory. The company relies solely on a network of contract laboratories for the various tasks necessary in drug development, according to reporting in The Harvard Crimson. As this asset-light model becomes the default for early-stage biotech, CROs are no longer optional service providers, but they are the operating infrastructure.

Category-wise Analysis

Service Type Insights

Medicinal chemistry services are expected to dominate with a share of nearly 38.2% in 2026, as they remain the foundation of small-molecule drug development, which leads the global pharmaceutical pipeline. Even with the rise of biologics and gene therapies, most oral drugs entering clinical development still require extensive medicinal chemistry optimization for potency, selectivity, bioavailability, and toxicity reduction. Pharmaceutical companies mainly outsource this work as medicinal chemistry demands large teams of experienced chemists and continuous analog synthesis, which is expensive to maintain in-house.

High-Throughput Screening (HTS) is predicted to remain in the second position in 2026, as pharmaceutical companies are under pressure to identify viable drug candidates quickly while reducing failure rates in early discovery. HTS enables researchers to screen hundreds of thousands of compounds against biological targets in a highly automated manner, dramatically accelerating hit identification. Modern HTS platforms now combine robotics, AI-assisted analytics, miniaturized assays, and cloud-based informatics, making them far more efficient than earlier systems.

Drug Type Insights

Small molecules are projected to lead with approximately 65.2% of share in 2026, as they are easier to manufacture, cheaper to expand, and more convenient for patients than biologics or advanced therapies. Most small-molecule drugs can be administered orally, have well-established regulatory pathways, and possess long commercial histories with predictable manufacturing processes. They also remain highly effective in chronic diseases such as cardiovascular disorders, diabetes, inflammation, and several types of cancers. Pharmaceutical companies continue investing heavily in small molecules as they are compatible with AI-backed discovery platforms and HTS workflows.

Cell and gene therapies are estimated to be the fastest-growing segment in 2026, as they provide the possibility of long-term or potentially curative treatment for diseases that conventional drugs cannot adequately address. Strong momentum in oncology, rare genetic disorders, and autoimmune diseases is pushing pharmaceutical companies to broaden investment in these therapies. Technologies such as CRISPR gene editing, CAR-T therapy, and mRNA-based delivery systems are transforming treatment approaches, especially for previously untreatable conditions.

Regional Insights

North America Drug Discovery Outsourcing Market Trends

A share of nearly 41.5% is expected in 2026 for North America, as it has the world’s largest concentration of pharmaceutical companies, biotech start-ups, academic research centers, and venture capital funding. The U.S. alone hosts a key share of global clinical-stage biotech firms and consistently leads in drug approvals, AI-based drug discovery investments, and research & development spending. Large pharmaceutical companies mainly outsource discovery activities to reduce fixed costs while focusing internal resources on high-value strategic research.

U.S. Drug Discovery Outsourcing Market Trends

Growth in the U.S. is being pushed by the ongoing expansion of biotech start-ups and AI-integrated drug discovery models. Pharmaceutical companies are signing large partnerships with AI-focused firms to accelerate target identification and molecule design. Venture capital funding for AI-backed biotech companies remains superior despite broad biotech funding fluctuations. The U.S. is also seeing strong outsourcing demand from small-scale biotech firms that prefer asset-light operating models instead of building expensive laboratory infrastructure.

Asia Pacific Drug Discovery Outsourcing Market Trends

Asia Pacific is the fastest-growing region because global pharmaceutical companies are shifting outsourcing activities toward low-cost yet scientifically capable countries. The region now delivers far more than labor arbitrage. Countries such as China, India, South Korea, and Singapore have developed unique research infrastructure, experienced scientific talent, and government-backed biotech ecosystems. Increasing pharmaceutical manufacturing investments, rising local biotech innovation, and supportive regulatory reforms are also accelerating regional growth.

China Drug Discovery Outsourcing Market Trends

China is seeing steady growth as it has developed one of the world’s largest integrated pharmaceutical outsourcing ecosystems. Domestic CROs and CDMOs built strong capabilities in medicinal chemistry, biologics, antibody discovery, and preclinical research over the past decade. Companies such as WuXi AppTec and WuXi Biologics became global outsourcing leaders due to rapid execution speed, extensive infrastructure, and large scientific workforces. China also benefits from superior domestic biotech innovation, with local start-ups increasingly developing first-in-class oncology and immunology therapies.

India Drug Discovery Outsourcing Market Trends

India is witnessing steady growth because it is increasingly viewed as the preferred alternative destination for pharmaceutical outsourcing diversification. The country combines low operational costs with a large English-speaking scientific workforce and strong expertise in chemistry-driven drug discovery. India-based CROs are moving beyond generic chemistry services into biologics, antibody-drug conjugates, peptide synthesis, and computational drug discovery. Companies such as Syngene International, Jubilant Biosys, and Laurus Labs are expanding CDMO and discovery capabilities to capture global contracts.

Europe Drug Discovery Outsourcing Market Trends

Europe’s growth outlook remains decent due to its concentration of advanced biotech research, precision medicine initiatives, and academic innovation networks. Local CROs are particularly competitive in biologics research, rare diseases, neuroscience, and AI-assisted discovery. The region benefits from collaborative funding programs and cross-border scientific partnerships. Several pharmaceutical companies are also increasing outsourcing activity to improve research & development efficiency with rising research costs and patent expiration pressures.

Germany Drug Discovery Outsourcing Market Trends

Germany is seeing decent growth as it remains one of Europe’s most prominent pharmaceutical and industrial biotechnology hubs. The country has a well-established base in biologics, antibody engineering, precision manufacturing, and automation technologies. Local CROs and biotech firms are mainly integrating AI and unique screening platforms into drug discovery workflows. Companies such as Evotec have extended partnerships with leading pharmaceutical firms to support integrated discovery programs. Germany also benefits from close collaboration between universities, biotech start-ups, and industrial research institutes.

U.K. Drug Discovery Outsourcing Market Trends

The U.K. market is benefiting from its superior biotechnology infrastructure and globally recognized academic institutions. Clusters around Cambridge, Oxford, and London continue generating high levels of biotech start-up activity and venture funding. The country is becoming increasingly important in AI-backed drug discovery, supported by companies such as BenevolentAI and Exscientia. The National Health Service (NHS) also provides large-scale clinical and genomic datasets that support precision medicine research and biomarker discovery.

Competitive Landscape

The global drug discovery outsourcing market is moderately fragmented, with a mix of large global CROs and a long tail of specialized, mid-sized, and niche service providers competing across different stages of the discovery value chain. Competition is no longer centered on cost arbitrage alone. Leading players such as WuXi AppTec, Charles River Laboratories, Evotec, IQVIA, Syngene International, and Thermo Fisher Scientific are differentiating through integrated target-to-IND capabilities. They are allowing pharma companies to outsource entire discovery workflows to a single partner.

Partnerships between pharmaceutical companies and tech-driven firms are also influencing competition. For instance, Eli Lilly has expanded its collaboration with Insilico Medicine, while Takeda Pharmaceutical is working with Iambic Therapeutics. This signals that CROs without superior computational and AI capabilities are gradually losing relevance, especially in early-stage discovery, where speed and target validation accuracy matter.

Key Industry Developments:

- In March 2026, ESTEVE CDMO commenced a US$15.5 million investment in its Morton Grove, Illinois, facility, acquired in July 2025. The expansion includes reactor upgrades, addition of powder transfer systems, and cleanroom upgrades, broadening the reactors' operational temperature range from -15°C to +140°C.

- In January 2026, Vetter announced plans to build a US$574 million production facility in the Saarland region of southwest Germany, with construction scheduled to begin in Q2 2026 and operations expected to commence in 2031. The company also began construction on a new US$285 million clinical manufacturing site in Des Plaines, Illinois.

- In September 2025, Fujifilm Biotechnologies officially opened its US$3.2 billion commercial-scale cell-culture biomanufacturing site in Holly Springs, North Carolina. The launch marked the culmination of the company's over US$8 billion global manufacturing investment program.

Companies Covered in Drug Discovery Outsourcing Market

- Albany Molecular Research Inc. (Curia Global, Inc.)

- EVOTEC

- Laboratory Corporation of America Holdings

- GenScript

- Thermo Fisher Scientific, Inc.

- Charles River Laboratories International, Inc.

- WuXi AppTec

- Merck & Co., Inc.

- Dalton Pharma Services

- Oncodesign

- Jubilant Biosys

- QIAGEN

- Eurofins SE

- Syngene International Limited

- Dr. Reddy Laboratories Ltd.

- Pharmaron Beijing Co., Ltd.

- TCG Lifesciences Pvt Ltd.

- Domainex Ltd.

- Others

Frequently Asked Questions

The global drug discovery outsourcing market is projected to be valued at US$5.3 billion in 2026.

The drug discovery outsourcing market is expected to reach US$8.6 billion by 2033.

Rising demand for integrated end-to-end CRO partnerships and expansion of high-throughput screening platforms are a few key market trends.

Small molecules are expected to lead with around 65.2% of share in 2026, as they integrate efficiently with AI-supported drug design and high-throughput screening.

The drug discovery outsourcing market is expected to grow at a CAGR of 7.3% from 2026 to 2033.

Albany Molecular Research Inc. (Curia Global, Inc.), EVOTEC, Laboratory Corporation of America Holdings, and GenScript are a few key market players.