- Smart Packaging

- Recycled Containerboard Market

Recycled Containerboard Market Size, Share, and Growth Forecast 2026 - 2033

Recycled Containerboard Market by Product Type (Linerboard, Corrugating Medium), Industry (Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Others), and Regional Analysis for 2026 - 2033

Recycled Containerboard Market Size and Trend Analysis

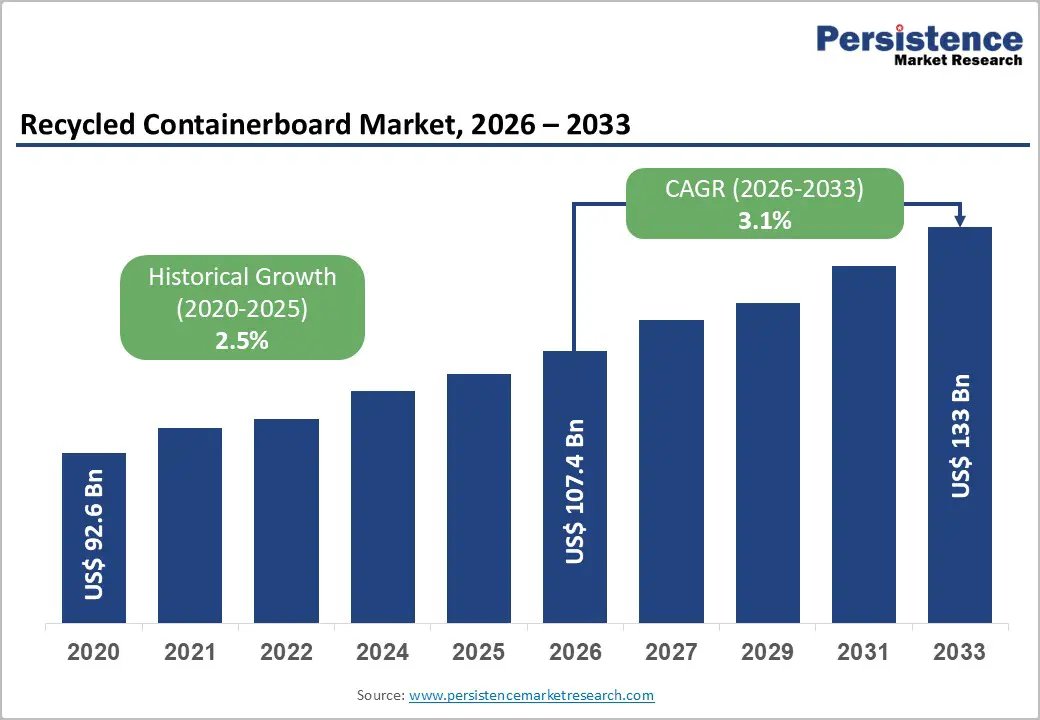

The global recycled containerboard market size is expected to be valued at US$ 107.4 billion in 2026 and is projected to reach US$ 133.0 billion by 2033, growing at a CAGR of 3.1% between 2026 and 2033.

This consistent growth is driven by accelerating global commitments to sustainable packaging solutions, surging e-commerce packaging demand that relies overwhelmingly on corrugated containerboard, and stringent regulatory mandates across major economies requiring higher recycled content in paper-based packaging.

The market demonstrated steady historical growth supported by expanding circular economy and recycling infrastructure globally, the proliferation of online retail generating unprecedented corrugated box volumes, and growing consumer and institutional preference for recycled-fiber packaging over virgin fiber and plastic alternatives particularly across food & beverages, personal care, and pharmaceutical end-use sectors.

Key Industry Highlights:

- E-commerce Demand Surge: Global e-commerce exceeding US$ 5.8 trillion and U.S. production of 400 billion sq. ft. corrugated boxes annually are significantly boosting recycled containerboard demand, reinforcing circular economy benefits and sustained packaging consumption growth.

- Regulatory Sustainability Push: Policies like EU PPWR and UK Plastic Packaging Tax (>30% recycled content) are accelerating adoption, ensuring long-term demand stability for recycled containerboard across major economies and strengthening sustainability-driven market expansion globally.

- OCC Price Volatility Impact: Recovered paper (OCC) prices fluctuating over 200% annually are creating supply chain instability, compressing margins, and impacting production planning, posing challenges for consistent pricing and investment in recycled containerboard capacity.

- Recycled Fiber Limitations: Recycled fibers show 15-25% lower strength than virgin materials, limiting usage in high-performance applications and requiring higher grammage or blending, increasing costs and affecting competitiveness in premium packaging segments.

- Advanced Recycling Innovation: New technologies and lightweighting enable 10-20% material reduction, improving performance and sustainability, allowing manufacturers to enhance product quality while reducing costs and carbon footprint in recycled containerboard production.

- Linerboard Market Dominance: Linerboard leads with 62% market share (2025) due to its structural role in packaging strength and printability, driven by strong demand from e-commerce, food, and retail sectors globally.

- Corrugating Medium Growth: Corrugating medium is fastest-growing with 4.2% CAGR (2026 - 2033), supported by rising e-commerce demand for lightweight, durable packaging and improved recycling technologies expanding production capabilities.

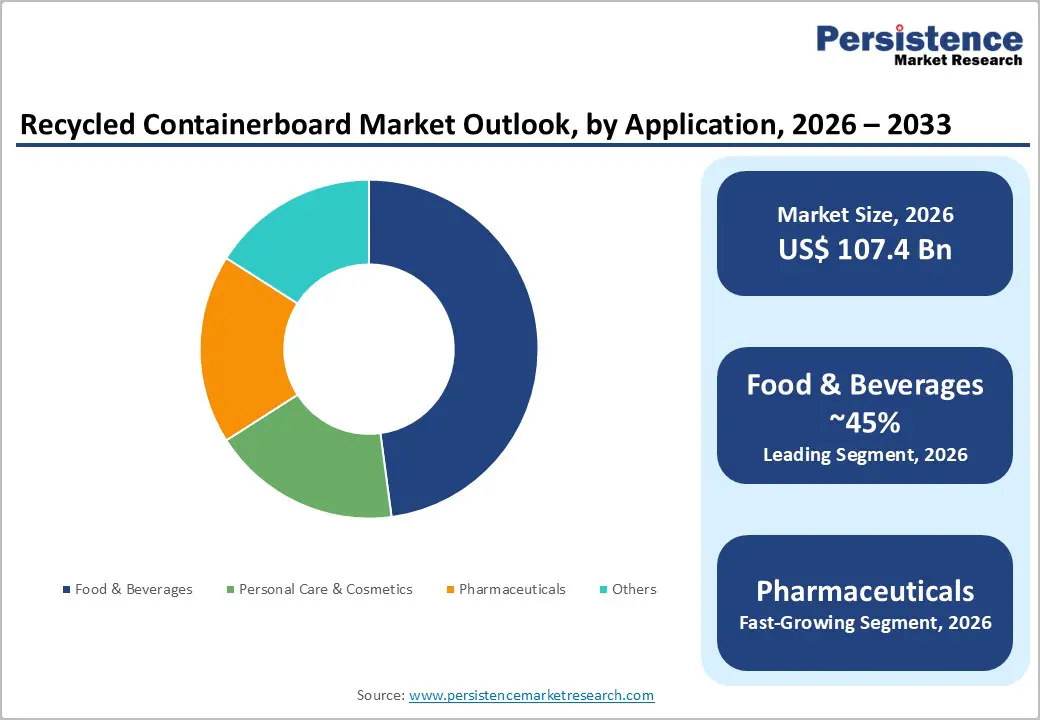

- Food Industry Leadership: Food & beverages dominate with 45% market share (2025), while pharmaceuticals grow at 4.8% CAGR, driven by sustainable packaging regulations and increasing demand for eco-friendly, compliant packaging solutions globally.

Market Dynamics

Drivers - Surging E-commerce Packaging Demand Generating Unprecedented Corrugated Box Volumes

The explosive growth of global e-commerce is the most powerful near-term demand driver for recycled containerboard, as virtually all e-commerce shipments rely on corrugated boxes made from linerboard and corrugating medium both primary recycled containerboard products. The United Nations Conference on Trade and Development (UNCTAD) reports that global e-commerce sales have grown to represent over US$ 5.8 trillion annually, with continued double-digit growth projected across Asia Pacific, Latin America, and the Middle East.

The Fibre Box Association (FBA) reports that the U.S. alone produces approximately 400 billion square feet of corrugated containers annually. The e-commerce packaging demand surge is structurally distinct from traditional industrial packaging because it involves smaller-sized, single-use corrugated boxes consumed by billions of individual consumers, creating enormous recycled fiber recovery opportunities that feed back into the containerboard recycling supply chain and reinforce the circular economy model underpinning the recycled containerboard sector's growth.

Regulatory Mandates for Recycled Content and Sustainable Packaging Across Major Economies

Stringent regulatory requirements for recycled content in paper-based packaging are creating structural demand guarantees for recycled containerboard producers globally. The European Union's Packaging and Packaging Waste Regulation (PPWR) mandates minimum recycled content requirements for packaging across member states, with containerboard facing some of the highest targets due to its already-elevated recyclability credentials. In the U.S., California's SB 54 Plastic Pollution Producer Responsibility Act and equivalent state-level measures are directing packaging design toward recyclable fiber-based alternatives.

The UK's Plastic Packaging Tax levying charges on packaging with less than 30% recycled content further incentivizes the shift from virgin materials toward recycled containerboard in packaging applications. These regulatory tailwinds, applied to the world's largest packaging consumption markets, provide durable and growing demand certainty for recycled containerboard producers through the forecast period, supporting sustainable packaging solutions adoption at industrial scale.

Restraints - Fluctuating Recovered Paper (OCC) Prices and Supply Chain Volatility

Old corrugated containers (OCC) the primary raw material feedstock for recycled containerboard are subject to significant price volatility driven by fluctuating collection volumes, export policy changes, and competition between domestic mills and international markets. RISI/Fisher International data documents OCC price swings of over 200% within single-year cycles in recent years. This input cost volatility compresses producer margins and complicates capital planning for recycled containerboard mills, deterring capacity investment during low-OCC-price environments and creating supply bottlenecks during high-demand periods.

The resulting market uncertainty impacts the competitiveness of recycled vs. virgin containerboard in cost-sensitive procurement decisions.

Quality Limitations of Recycled Fiber in High-Performance Packaging Applications

Recycled containerboard faces inherent quality limitations compared to virgin fiber products in demanding packaging applications requiring maximum burst strength, moisture resistance, or top-load compression performance. Each recycling cycle degrades cellulose fiber length and bonding strength, limiting the number of times individual fibers can be successfully recycled. The Technical Association of the Pulp and Paper Industry (TAPPI) documents that recycled fibers typically deliver 15-25% lower burst and tensile strength versus virgin fiber equivalents at the same basis weight, necessitating heavier grammages or fiber blending that increase material costs for high-performance applications.

Opportunities - Advanced Recycling Technologies and Lightweight Containerboard Innovation

Investment in advanced recycling technologies including enzyme-assisted fiber upgrading, wet-strength resin removal processes, and optical sorting for recovered paper streams is enabling recycled containerboard producers to close the quality gap with virgin fiber products while maintaining the sustainability credentials of recycled inputs. Companies including Smurfit Westrock, International Paper, and DS Smith (now part of International Paper) have invested in proprietary fiber upgrading technologies that enhance tensile and burst performance of recycled containerboard.

Simultaneously, lightweight containerboard innovation reducing basis weights through improved fiber orientation, micro-fluting, and advanced forming section technology enables the same structural performance at 10-20% lower material consumption. The American Forest & Paper Association (AF&PA) identifies lightweighting as a priority sustainability initiative that reduces both material cost and carbon footprint per packaging unit, creating a competitive advantage for producers that master advanced recycling technologies and lightweight containerboard production simultaneously.

Pharmaceutical and Personal Care Packaging Shift from Plastic to Recycled Fiber Substrates

The pharmaceutical and personal care sectors represent high-value, fast-growing application opportunities for premium recycled containerboard, driven by regulatory pressure to reduce plastic packaging and growing brand owner commitments to sustainable packaging solutions. The European Medicines Agency (EMA) and consumer goods companies including Unilever, Procter & Gamble, and L'Oreal have committed to transitioning packaging portfolios to recycled-fiber alternatives. ECMA (European Carton Makers Association) data indicates consistent growth in pharmaceutical carton and secondary packaging demand.

Recycled containerboard meeting EU Regulation 1935/2004 food contact standards and pharmaceutical-grade cleanliness requirements commands significant pricing premiums offering producers that can certify compliance with health and safety standards an important market differentiation opportunity with structurally growing, high-margin end-user segments through 2033.

Category-wise Analysis

Product Type Insights

Linerboard is the dominant product type in the recycled containerboard segment, accounting for approximately 62% market share in 2026. Recycled linerboard produced from old corrugated containers (OCC) and mixed paper forms the flat outer and inner facings of corrugated boxes and is the highest-volume recycled containerboard product globally. Its dominance reflects the structural role of linerboard in determining corrugated box compression strength and printability, making it the specification focus for packaging converters and brand owners seeking aesthetically acceptable recycled packaging solutions.

The Confederation of European Paper Industries (CEPI) reports that containerboard predominantly recycled linerboard accounts for the largest single category of European paper production by volume. The shift toward sustainable packaging solutions across food, beverage, and e-commerce applications is sustaining consistent linerboard demand growth, while advances in surface treatment and coating technologies are improving the printability of recycled linerboard, further broadening its application scope.

Corrugating Medium is the fastest growing product type segment, projected to grow at a CAGR of approximately 4.2% share with a CAGR of 3.1% in the forecast period. This growth is driven by the explosion of e-commerce packaging demand, which requires high-flute-performance corrugating medium for lightweight, stackable single-wall corrugated boxes. Advanced recycling technologies enabling the production of higher-basis-weight corrugating medium from mixed recovered fiber streams are also expanding the addressable material base for this segment.

Industry Insights

Food & beverages is the leading industry segment, accounting for approximately 45% of the total recycled containerboard market share in 2026. Food & beverage packaging requires corrugated containers at every stage of the supply chain, from primary shipping cases for canned goods, beverages, and fresh produce to retail-ready packaging and e-commerce direct-to-consumer delivery boxes.

The Food and Agriculture Organization (FAO) reports global food production volumes generating enormous, corrugated packaging demand, with fresh produce alone requiring high-humidity-resistant recycled containerboard that combines functional performance with sustainability credentials. Regulatory frameworks, including EU Regulation 1935/2004 on materials in contact with food, are being progressively updated to accommodate recycled-fiber packaging, removing a historic compliance barrier to recycled containerboard adoption in direct food contact applications and opening additional growth avenues for producers meeting enhanced food-safety recycled content standards.

Pharmaceuticals is the fastest growing end-use segment, projected to expand at a CAGR of approximately 4.8% by forecast period driven by major pharma brand owners' plastic reduction commitments, EMA guidance updates accommodating fiber-based secondary packaging, and growing demand for track-and-trace compatible recycled containerboard packaging that supports pharmaceutical supply chain integrity and regulatory compliance requirements.

Regional Insights

North America Recycled Containerboard Market Trends

North America is a mature, highly efficient recycled containerboard market anchored by the United States' world-class paper recycling infrastructure and the continent's most developed e-commerce packaging ecosystem. The American Forest & Paper Association (AF&PA) reports that the U.S. paper recycling rate consistently exceeds 68%, providing abundant OCC feedstock for recycled containerboard mills. Major capacity investments by Smurfit Westrock and Packaging Corporation of America (PCA) are expanding recycled linerboard capacity to meet growing e-commerce packaging demand.

The region is witnessing accelerating adoption of lightweight containerboard as brand owners prioritize both material efficiency and sustainability credentials under voluntary commitments and state-level packaging regulations. Canada's Extended Producer Responsibility (EPR) programs are strengthening OCC collection infrastructure, improving recovered fiber supply quality and sustainability metrics for North American recycled containerboard producers.

- U.S. Recycled Containerboard Market Size

The United States is by far the most important national market in North America, commanding approximately 83% of the regional recycled containerboard market revenue in 2026. With annual OCC consumption at recycled containerboard mills exceeding 30 million short tons per AF&PA data, the U.S. operates the world's most integrated recycled fiber supply chain.

E-commerce packaging demand growth, with U.S. Census Bureau data documenting U.S. e-commerce retail sales exceeding US$ 1.1 trillion annually, sustains high corrugated containerboard consumption. The U.S. market is projected to grow at approximately 2.8% CAGR by 2033, led by the recycled linerboard segment serving e-commerce, food & beverage, and industrial packaging applications. State-level packaging legislation in California, Oregon, and Colorado mandating recycled content reinforces structural recycled containerboard demand throughout the forecast period.

Europe Recycled Containerboard Market Trends

Europe is the world leader in recycled containerboard sustainability, driven by the EU Packaging and Packaging Waste Regulation (PPWR), Green Deal, and member state EPR frameworks that collectively mandate high recycled content and recyclability in packaging. The Confederation of European Paper Industries (CEPI) reports European containerboard recycling rates consistently above 80% among the highest globally, providing a robust and reliable recovered fiber supply base for regional mills.

The region is transitioning toward higher-performance, lighter-weight recycled linerboard grades as circular economy and recycling policy frameworks create competitive pressure to maintain quality while increasing recycled content. Smurfit Westrock, Mondi Group, and DS Smith (now International Paper) operate extensive integrated European recycled containerboard mill networks, reinvesting in fiber upgrading and lightweighting technologies to maintain competitiveness.

- Germany Recycled Containerboard Market Size

Germany is the largest European recycled containerboard market, accounting for approximately 21% of regional market revenue in 2026. Germany's world-leading paper recycling infrastructure, underpinned by the Gesellschaft zur Förderung der Kreislaufwirtschaft (GKR) dual packaging system, delivers OCC recycling rates exceeding 90%, providing exceptional recovered fiber supply for domestic mills. Germany is home to major containerboard producers, including Klingele Papierwerke and Hamburger Containerboard. The German market is projected to grow at approximately 3.0% CAGR through 2033, supported by strong e-commerce growth, food & beverage packaging demand, and EU PPWR compliance investments.

- U.K. Recycled Containerboard Market Size

The United Kingdom holds approximately 13% of Europe recycled containerboard market revenue in 2025. The UK's Plastic Packaging Tax, charging £217.85 per tonne on packaging with less than 30% recycled content, has materially accelerated brand owner adoption of recycled containerboard alternatives. DS Smith (now part of International Paper) is the UK's leading recycled containerboard producer with integrated mill operations. The UK market is projected to grow at approximately 3.2% CAGR by 2033, outperforming the European average due to the ongoing material substitution effect driven by the Plastic Packaging Tax.

- France Recycled Containerboard Market Size

France accounts for approximately 10% of Europe recycled containerboard market revenue in 2025. France's Loi Anti-Gaspillage pour une Economie Circulaire (AGEC) mandates progressive increases in recycled content and recyclability across packaging categories, including containerboard applications. French producers, including Saica Group and Ondulys, serve domestic corrugated box demand across food, retail, and e-commerce channels. France is projected to grow at approximately 2.8% CAGR by 2033, with pharmaceutical and personal care end-uses growing fastest.

- Italy Recycled Containerboard Market Size

Italy contributes approximately 8% of Europe recycled containerboard market revenue in 2025. Italy is a significant corrugated packaging producer, home to companies including Burgo Group and Reno De Medici, serving domestic food & beverage, consumer goods, and industrial packaging demand. Italy's CONAI (National Packaging Consortium) EPR program maintains a strong OCC collection and processing infrastructure. The Italian market is projected to grow at approximately 2.6% CAGR, with export-oriented food packaging demand a key growth driver.

Asia Pacific Recycled Containerboard Market Trends

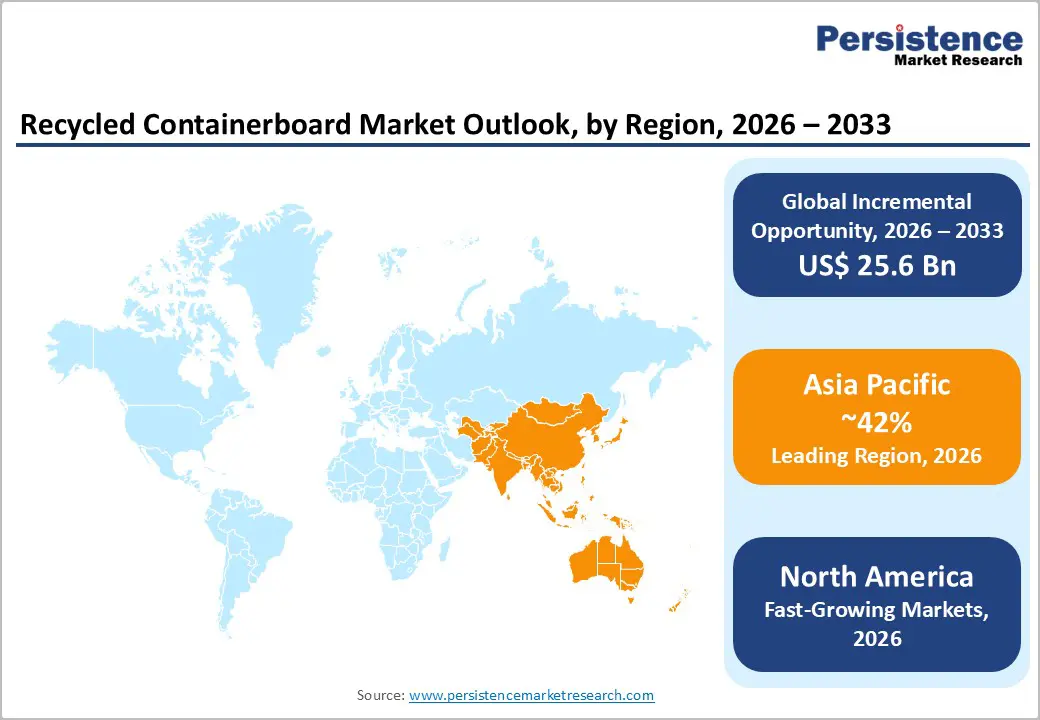

Asia Pacific is both the largest and fast-growing recycled containerboard market, driven by China's massive integrated papermaking and packaging industry, India's rapidly expanding e-commerce ecosystem, and ASEAN's growing manufacturing and export packaging demand. China accounts for approximately 55% of the Asia Pacific market demand, with domestic giants including Nine Dragons Paper, Lee & Man Paper Manufacturing, and Shanying International operating the world's largest recycled containerboard mill complexes.

China's National Sword policy banning most recovered paper imports has accelerated domestic OCC collection infrastructure investment, while India's Plastic Waste Management Rules and ASEAN nations' packaging sustainability regulations are progressively channeling packaging demand toward recycled fiber alternatives. The region's manufacturing cost advantages and growing middle-class consumption of packaged goods position Asia Pacific for consistent recycled containerboard demand growth through 2033.

- China Recycled Containerboard Market Size

China dominates the Asia Pacific market, accounting for approximately 55% of regional revenue in 2025. Following the National Sword policy, China has invested massively in domestic OCC collection and sorting infrastructure, with the China Renewable Resources Recycling Association (CRRA) reporting significant increases in domestic recovered paper collection rates.

Major producers, including Nine Dragons Paper and Lee & Man Paper Manufacturing, operate recycled containerboard mills with combined capacity exceeding 20 million tonnes per year. China's market is projected to grow at approximately 3.5% CAGR through 2033, supported by e-commerce packaging demand and export corrugated box production for Asian manufacturing supply chains.

- India Recycled Containerboard Market Size

India represents approximately 12% of Asia Pacific recycled containerboard market revenue in 2025 and is growing rapidly. India's e-commerce boom, with NASSCOM reporting consistent double-digit online retail growth, is generating surging corrugated packaging demand. India's domestic OCC supply is expanding as urban paper recycling collection improves under the Swachh Bharat Mission waste management programs. The Indian market is projected to grow at approximately 4.5% CAGR by 2033, well above the global average, driven by e-commerce packaging demand, FMCG sector growth, and expanding pharmaceutical packaging requirements.

- South Korea Recycled Containerboard Market Size

South Korea contributes approximately 7% of Asia Pacific recycled containerboard market revenue in 2025. South Korea operates one of the world's most efficient paper recycling systems, with OCC recovery rates exceeding 85% per Korea Paper Manufacturers Association data. Domestic producers, including Hansol Holdings and Asia Pulp & Paper Korea, serve a well-developed corrugated packaging market anchored by electronics, automotive, and food export packaging. South Korea's market is projected to grow at approximately 3.0% CAGR through 2033, with pharmaceutical and personal care packaging growth outperforming the broader market.

Competitive Landscape

The global recycled containerboard market exhibits a moderately consolidated competitive structure at the top tier, with multinational integrated producers including Smurfit Westrock, International Paper, Mondi Group, and Nine Dragons Paper controlling significant production capacity across multiple regions. Key competitive differentiators include integrated OCC sourcing networks, mill energy efficiency, fiber upgrading technology, and product quality consistency.

Emerging business model trends include vertical integration into corrugated box converting for margin capture, development of food-contact-compliant recycled linerboard grades, and sustainability certification programs (FSC Recycled, PEFC Chain of Custody) that command specification preference among major brand owner customers with public recycled content commitments. Regional players in Asia, Latin America, and Eastern Europe compete aggressively on price in standard commodity grades.

Key Developments:

- April 2026: In a significant development for the paper and packaging industry, Star Paper Mill Paper Industry LLC commenced operations of its Recycled Containerboard Mill at Khalifa Economic Zones Abu Dhabi (KEZAD) on April 11, 2026. This milestone strengthens sustainable manufacturing practices and reinforces the UAE’s commitment to advancing eco-friendly paper production.

- March 2025: Smurfit Westrock completed its landmark merger of Smurfit Kappa and WestRock, creating the world's largest integrated recycled containerboard and corrugated packaging company with combined annual production capacity exceeding 40 million tonnes across North America, Europe, and Latin America.

- September 2024: International Paper completed its acquisition of DS Smith, establishing the world's second-largest integrated recycled containerboard and corrugated packaging group with a leading position across European and North American markets and strategic access to growing emerging market channels.

- January 2023: Nine Dragons Paper announced a major capacity expansion at its Chinese recycled containerboard complex, adding 1.5 million tonnes of new recycled linerboard production capacity specifically engineered for high-burst-strength e-commerce packaging grades serving domestic and export markets.

Companies Covered in Recycled Containerboard Market

- Smurfit Westrock

- International Paper (DS Smith)

- Mondi Group

- Nine Dragons Paper Holdings

- Lee & Man Paper Manufacturing

- Packaging Corporation of America

- Cascades Inc.

- Shanying International Holdings

- Klingele Papierwerke

- Hamburger Containerboard

- Saica Group

- Hansol Holdings

Frequently Asked Questions

The global recycled containerboard market is projected to reach US$ 133.0 billion by 2033, growing from US$ 107.4 billion in 2026 at a CAGR of 3.1%. The market grew from US$ 92.6 billion in 2020 at a historical CAGR of 2.5%. Growth is driven by e-commerce packaging demand, EU PPWR recycled content mandates, and the global transition from plastic and virgin-fiber packaging to recycled containerboard solutions across food, pharma, and personal care sectors.

Primary drivers include e-commerce packaging demand with the Fibre Box Association documenting ~400 billion square feet of U.S. corrugated production annually and UNCTAD reporting global e-commerce surpassing US$ 5.8 trillion and regulatory mandates including the EU PPWR, UK Plastic Packaging Tax on packaging with less than 30% recycled content, and California's SB 54. These combined demand and compliance factors create durable structural growth for recycled containerboard through 2033.

Recycled linerboard is the leading product type with approximately 62% market share in 2025, driven by its structural role as the outer and inner facing of corrugated boxes across e-commerce, food & beverage, and industrial packaging applications. CEPI reports containerboard as Europe's highest-volume paper category by production, with recycled linerboard representing the dominant share. Advances in surface coating technology are improving printability of recycled linerboard, expanding its application scope in brand-sensitive retail packaging.

Asia Pacific leads with approximately 42% global market share in 2026, anchored by China, which accounts for ~55% of regional demand through Nine Dragons Paper and Lee & Man Paper Manufacturing operating mills with combined capacity exceeding 20 million tonnes per year. India is the fast-growing market at ~4.5% CAGR, driven by NASSCOM-documented double-digit e-commerce growth and improving OCC collection under Swachh Bharat Mission waste management programs.

The foremost opportunity lies in advanced recycling technologies, including enzyme-assisted fiber upgrading and micro-fluting lightweight containerboard innovation, reducing basis weights by 10-20%, enabling competitive quality at lower material cost. The pharmaceutical and personal care segments offer premium-priced growth, as Unilever, Procter & Gamble, and L'Oreal pursue plastic-to-fiber packaging transitions, with EU Regulation 1935/2004 food-contact-compliant recycled containerboard commanding significant pricing premiums in these high-value end-use categories.

The leading companies are Smurfit Westrock (the world's largest integrated recycled containerboard and packaging company post-2024 merger), International Paper (strengthened by DS Smith acquisition), Mondi Group, Nine Dragons Paper Holdings, Lee & Man Paper Manufacturing, Packaging Corporation of America, Cascades Inc., and Shanying International Holdings. These companies compete through integrated OCC sourcing, fiber upgrading technology, and sustainability certifications, including FSC Recycled and PEFC Chain of Custody.