- Industrial Machinery

- Pressure Gauges Market

Pressure Gauges Market Size, Share, and Growth Forecast, 2026 - 2033

Pressure Gauges Market by Technology (Mechanical Gauges, Digital Gauges, Hybrid Gauges), Pressure Type (Gauge Pressure, Absolute Pressure, Differential Pressure, Sealed Pressure), End-Use Industry (Power Generation, HVACR, Automotive & Transportation, Oil & Gas, Semiconductor & Electronics, Others), and Regional Analysis for 2026 - 2033

Pressure Gauges Market Share and Trends Analysis

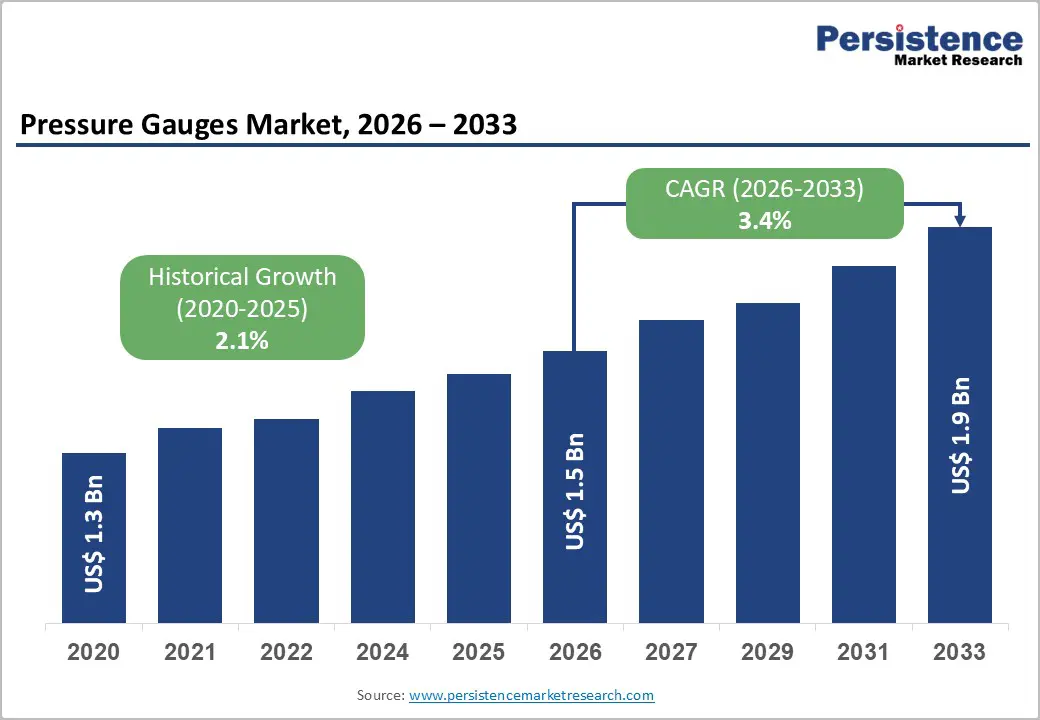

The global pressure gauges market size is likely to be valued at US$ 1.5 billion in 2026, and is estimated to reach US$ 1.9 billion by 2033, growing at a CAGR of 3.4% during the forecast period 2026 - 2033.

Growth is being driven by incremental industrial automation and regulatory requirements rather than rapid demand expansion. Process industries such as oil and gas, chemicals, and power generation are forming the core demand base, as pressure monitoring remains essential for operational safety and efficiency. Replacement cycles are accounting for nearly 65% of total demand, ensuring stable revenue flows. Demand patterns are shifting toward digital instrumentation and compliance-driven monitoring under frameworks such as the Occupational Safety and Health Administration (OSHA), the ATEX Directive in the European Union (EU), and International Organization for Standardization (ISO) 9001 and ISO 14001 standards. Emerging sectors such as hydrogen infrastructure, semiconductor manufacturing, and heating ventilation, & air conditioning (HVAC) systems are heightening the need for high-precision gauges. The market is evolving toward a value-focused structure, where digital and application-specific solutions are gaining share in high-compliance and precision-driven environments.

Key Industry Highlights

- Leading Technologies: Mechanical gauges are expected to lead with an estimated 62% revenue share in 2026, while digital gauges are anticipated to grow the fastest through 2033, driven by industrial Internet of Things (IIoT) integration.

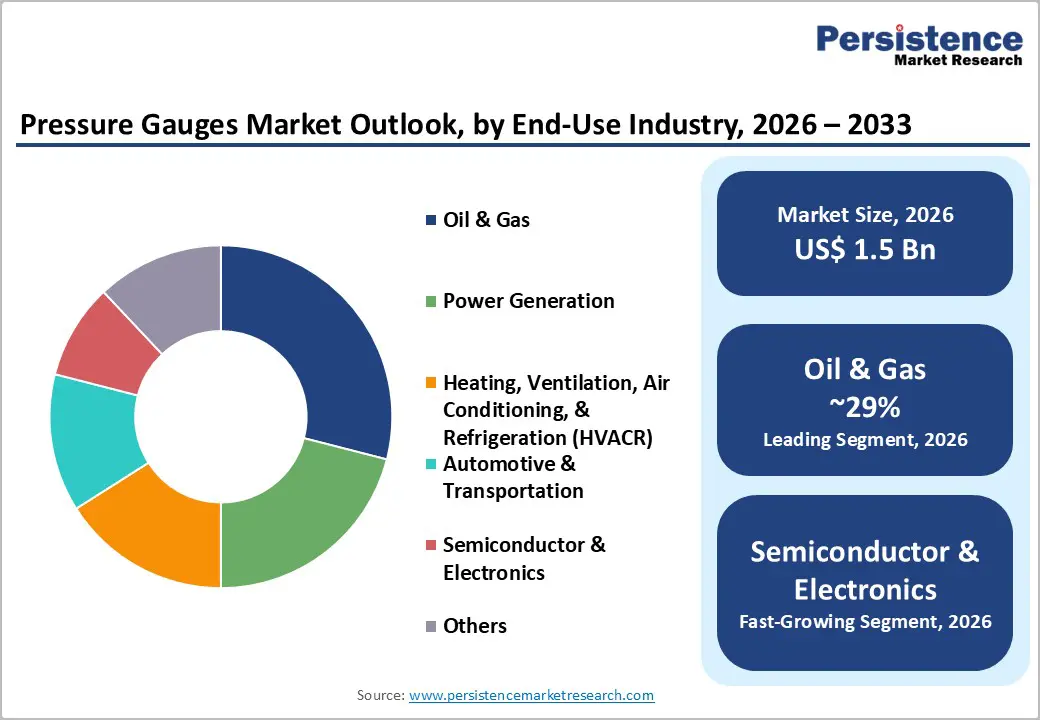

- Dominant End-Use Industries: Oil & gas is projected to dominate with an estimated 29% revenue share in 2026, whereas semiconductor and electronics applications are set to register the highest 2026 - 2033 CAGR of about 6.1%, due to high-precision requirements.

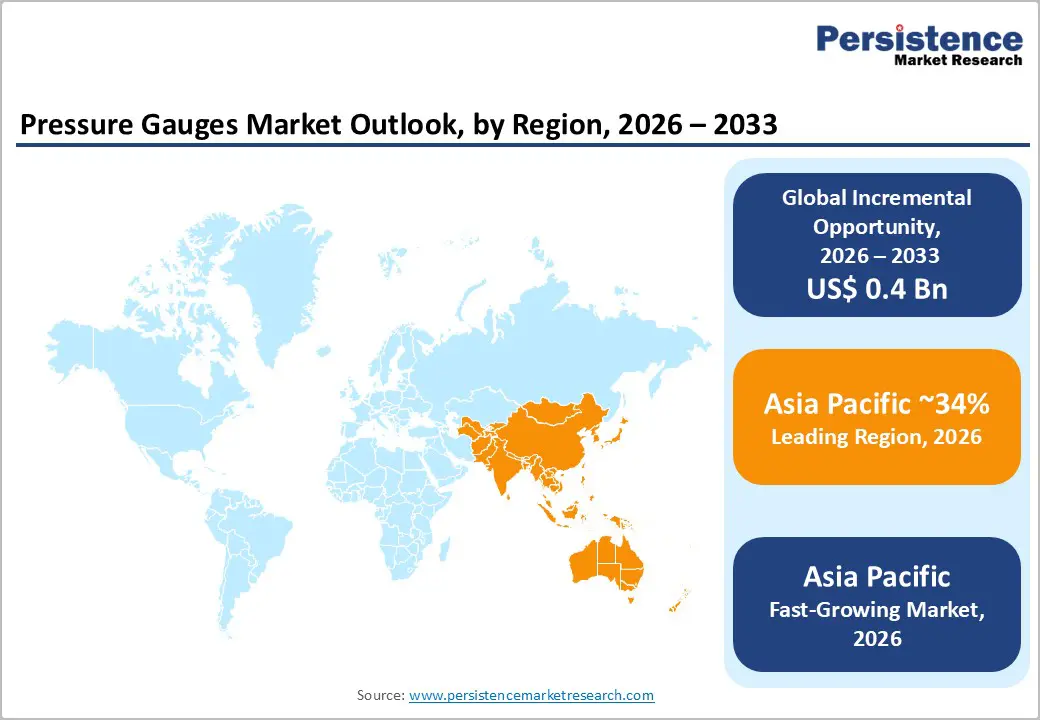

- Dominant Region: Asia Pacific is likely to command approximately 34% market share in 2026, supported by rapid industrialization and high manufacturing output in China and India.

- Fastest-growing Market: The Asia Pacific market is likely to record the highest growth, with an estimated CAGR of 4.2% through 2033, driven by expanding semiconductor fabrication and energy infrastructure development.

- Competitive Environment: Increasing focus on smart pressure gauges, digital integration, and regional manufacturing expansion is indicating a shift toward higher-value offerings.

- February 2026: Additel teamed up with Kingsway Instruments to launch new digital pressure gauges and multifunction process calibrators featuring high accuracy up to 0.02% full scale, extended battery life, Bluetooth connectivity, and ATEX-certified models.

| Key Insights | Details |

|---|---|

| Pressure Gauges Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 1.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.1% |

Market Factors - Growth, Barriers, and Opportunity

Industrial Safety Compliance Tightening across Process Industries

Regulatory bodies such as the OSHA in the U.S., the European Commission (EC) under the ATEX Directive 2014/34/EU, and the ISO are mandating real-time pressure monitoring and equipment integrity validation across hazardous industrial environments. Process safety management (PSM) enforcement is intensifying in oil and gas and chemical operations, where pressure deviations are driving operational risk. The International Labour Organization (ILO) is reporting over 2.3 million workplace fatalities annually linked to industrial hazards, which is reinforcing the need for continuous monitoring systems and stricter compliance frameworks.

These regulatory shifts are driving sustained demand for pressure gauges, particularly differential and high-accuracy variants used in filtration, pipeline systems, and safety-critical applications. Industrial operators are deploying redundant monitoring architectures to ensure compliance and system reliability, which is increasing unit installations per facility. Replacement cycles are shortening to 4 to 6 years in high-risk environments, which is strengthening aftermarket revenue visibility. This trend is creating a predictable demand base while encouraging investment in higher-specification instrumentation.

Expansion of Hydrogen, Semiconductor, and Clean Energy Infrastructure

Global energy transition policy directions provided by the International Energy Agency (IEA) and national hydrogen programs are accelerating investments in green hydrogen, carbon capture, and advanced energy systems. These applications are requiring high-precision pressure monitoring across storage and transport infrastructure. The IEA estimates global hydrogen demand to exceed 115 million tons by 2030, which is driving deployment of high-pressure systems. This shift is increasing demand for reliable instrumentation in energy networks and is expanding opportunities for suppliers aligned with clean energy value chains.

Semiconductor manufacturing is expanding in Asia and the United States under initiatives such as the CHIPS and Science Act, which is raising demand for ultra-clean pressure gauges in vacuum and gas delivery systems. These environments are requiring accuracy levels below ±0.25%, far exceeding conventional industrial standards. This transition is increasing value per unit and is favoring manufacturers offering microelectromechanical systems (MEMS)-based digital gauges and corrosion-resistant designs. Suppliers targeting these segments are strengthening margins and positioning within premium instrumentation categories.

Commoditization of Mechanical Gauges and Pricing Pressure

Mechanical pressure gauges, particularly Bourdon tube variants, are dominating volume demand but are offering limited differentiation across suppliers. Manufacturing hubs in China and India are producing gauges at 20% to 40% lower costs, which is intensifying global price competition. Industry data is indicating that average selling prices (ASPs) have declined by 1% to 2% annually over the past decade. This trend is reducing pricing leverage and is shifting procurement decisions toward cost efficiency in standard applications.

Margin compression is limiting revenue expansion despite stable shipment volumes. Original equipment manufacturers (OEMs) are prioritizing low-cost sourcing, which is increasing vendor switching and weakening brand-driven differentiation. Fragmentation is rising due to the presence of small regional manufacturers, especially in emerging markets. This dynamic is creating a structural constraint where volume growth is not translating into proportional value growth, particularly as mechanical gauges are accounting for more than 60 percent of total market share.

Extended Product Lifecycles and Low Replacement Frequency

Pressure gauges are durable industrial components with lifecycles ranging from 5 to 10 years depending on operating conditions. In non-critical environments, units are operating beyond recommended replacement timelines, which is delaying aftermarket demand. This trend is visible in sectors such as water treatment, HVAC, and general manufacturing, where pressure conditions remain stable and failure risk is limited. Operators are prioritizing equipment utilization over early replacement, as performance degradation is gradual and does not immediately impact operations.

Replacement demand is shifting toward reactive maintenance, especially in cost-sensitive markets where short-term cost control is guiding procurement decisions. Facilities are extending equipment usage until failure thresholds are reached instead of following preventive replacement schedules. This behavior is reducing purchase frequency while keeping installed base volumes stable. New installations are not offsetting delayed replacement cycles, which is creating a demand plateau across the market. Even in regulated environments, companies are relying on calibration and periodic servicing to meet compliance requirements rather than investing in new units, which is constraining revenue growth and reinforcing a service-driven business model.

Digital and Smart Pressure Gauges in IIoT Ecosystems

The integration of pressure gauges into IIoT ecosystems is creating a high-value growth segment within industrial instrumentation. Smart gauges are incorporating wireless connectivity, real-time data logging, and predictive maintenance capabilities, which are supporting digital transformation across process industries. The World Economic Forum (WEF) estimates that digital transformation in manufacturing could unlock US$ 3.7 trillion in value by 2025, with sensor-driven monitoring systems forming a critical foundation. Pressure gauges are evolving into connected data nodes that enable remote diagnostics, performance tracking, and system optimization across distributed industrial assets.

Adoption is increasing in industries that are prioritizing high uptime and operational visibility, such as oil and gas, chemical processing, and advanced manufacturing. These sectors are requiring continuous monitoring to minimize unplanned downtime and improve asset utilization. Pressure gauges integrated with IIoT platforms are enabling real-time performance tracking and early fault detection. This capability is supporting operational efficiency and is aligning with broader digital transformation goals across industrial value chains. Manufacturers are responding by offering calibration analytics, condition monitoring, and predictive maintenance platforms delivered through digital interfaces. This shift is creating recurring revenue streams and is improving customer retention through long-term service contracts.

Emerging Market Industrialization and Infrastructure Expansion

Rapid industrialization across India, Southeast Asia, and Africa is driving new installations of pressure monitoring systems in sectors such as water treatment, power generation, and manufacturing. Public investment programs are accelerating infrastructure development and are expanding the installed base of industrial equipment. India’s National Infrastructure Pipeline (NIP) has allocated over US$ 1.4 trillion toward energy, transport, and urban projects, which is increasing demand for instrumentation across project lifecycles. This expansion is creating consistent procurement pipelines for pressure gauges in both greenfield and brownfield facilities.

The massive of scale of urbanization has skyrocketed the demand for HVAC, water distribution, and building automation systems, all of which rely on pressure monitoring for efficient operation. The World Bank projects that urban populations in developing economies will exceed 1.5 billion additional residents by 2035, which will reinforce the demand for infrastructure. These markets are exhibiting high volume potential with strong price sensitivity, which is favoring cost-optimized and durable products. Manufacturers targeting the US$ 20 to US$ 50 price band are capturing the highest demand elasticity and are positioned to unlock an incremental market opportunity of US$ 200 to US$ 300 million by 2033.

Category-wise Analysis

Technology Insights

Mechanical gauges are anticipated to account for approximately 62% of the pressure gauges market revenue share in 2026, supported by their cost efficiency, simple design, and compatibility with legacy systems. Industries such as oil and gas and water treatment are relying on Bourdon tube and diaphragm gauges for routine monitoring where precision requirements remain moderate. These instruments are delivering adequate performance for non-critical applications while maintaining low acquisition and servicing costs. Their widespread installed base is reinforcing steady demand, particularly in replacement-driven procurement cycles.

Digital gauges are poised to emerge as the fastest-growing segment, with an estimated CAGR of 5.2% from 2026 to 2033. Adoption is increasing in sectors such as semiconductor manufacturing, pharmaceuticals, and clean energy, where high accuracy and real-time data access are essential. These environments are requiring precise monitoring to maintain process stability and product quality, which is strengthening demand for advanced instrumentation. These devices are enabling predictive maintenance and are reducing unplanned downtime by providing continuous performance insights. Industrial operators are integrating digital gauges with IIoT platforms to improve asset visibility and operational control. The shift toward hybrid and smart configurations is expanding the role of connected instrumentation, which is increasing value per installation and supporting long-term efficiency improvements across high-value applications.

End-Use Industry Insights

The oil and gas sector is projected to capture an approximate 29% of the pressure gauges market share in 2026, driven by its dependence on pressure monitoring across upstream, midstream, and downstream operations. Pressure gauges are being deployed in pipelines, refineries, and storage infrastructure where maintaining pressure stability is essential for operational safety and efficiency. Aging assets and stricter regulatory requirements are increasing replacement demand, particularly in high-risk environments. Operators are prioritizing reliable instrumentation to meet compliance standards and reduce the likelihood of system failures.

The semiconductor and electronics industry is slated to become the fastest-growing end-user of pressure gauges, likely to record a 2026-2033 CAGR of about 6.1% during the 2026-2033 forecast period. Expansion of fabrication facilities is increasing demand for high-precision pressure gauges used in vacuum environments and gas delivery systems. These processes are requiring strict control over pressure conditions to maintain product quality and yield, which is elevating the importance of advanced instrumentation. Manufacturers are adopting materials and designs that support ultra-clean environments and high accuracy requirements. Digital integration is enabling real-time monitoring and process optimization, which is improving operational efficiency.

Regional Insights

North America Pressure Gauges Market Trends

North America is expected to hold approximately 26% of the pressure gauges market value in 2026, supported by demand from oil and gas, chemical processing, and advanced manufacturing sectors. The United States is leading regional performance due to strong shale gas production and sustained capital expenditure in refining and petrochemical infrastructure. Regulatory authorities such as the OSHA and the United States Environmental Protection Agency (EPA) are known to enforce strict compliance standards, which are increasing the need for reliable pressure monitoring in safety-critical operations. This regulatory environment is strengthening demand for high-quality instrumentation and is encouraging periodic upgrades across industrial facilities.

Digital and smart gauges are gaining traction as industries are integrating automation and predictive maintenance into operational frameworks. Investments in hydrogen infrastructure and carbon capture systems are expanding the need for high-precision pressure monitoring across emerging energy applications. Companies are adopting connected instrumentation to improve system visibility and reduce operational risk. The North America market is projected to grow at a steady CAGR through 2033, supported by replacement demand and gradual adoption of advanced technologies. This trajectory is indicating consistent value creation opportunities for suppliers focusing on compliance-driven and high-accuracy solutions.

Europe Pressure Gauges Market Trends

Europe is anticipated to claim a share of roughly 24% of the global market for pressure gauges in 2026, boosted by stringent regulatory compliance and well-established industrial infrastructure. Germany, France, and the United Kingdom are driving demand across chemical processing and power generation sectors, where operational safety and process control remain critical. The ATEX Directive 2014/34/EU governs equipment used in explosive environments and is enforcing strict certification requirements for pressure monitoring devices. This regulatory framework is ensuring consistent demand for high-quality gauges and is encouraging manufacturers to align product specifications with safety and performance standards.

The region is prioritizing sustainability and energy efficiency, which is accelerating the adoption of advanced instrumentation across industrial systems. European Union (EU) policies focused on emissions reduction and energy optimization are pushing industries to adopt precise monitoring solutions to improve operational efficiency. Companies are investing in digital and high-accuracy gauges to support process optimization and regulatory reporting. The market here is expected to grow at a slightly lower CAGR than that of North America, but the growth trajectory is likely to steady on account of ongoing modernization initiatives and steady replacement demand. This environment is creating opportunities for suppliers offering compliant, energy-efficient, and technologically advanced solutions.

Asia Pacific Pressure Gauges Market Trends

Asia Pacific is expected to account for approximately 34% of the pressure gauges market share in 2026, and is projected to register the fastest growth, with a CAGR of 4.2% through 2033. China and India are driving regional expansion through rapid industrialization, large-scale infrastructure development, and strong manufacturing output. Government programs such as Make in India and China’s industrial modernization initiatives are increasing deployment of pressure monitoring systems across sectors such as power generation, water treatment, and heavy manufacturing. This environment is strengthening demand across both new installations and replacement cycles.

The region is also establishing itself as a global manufacturing hub for pressure gauges, supported by cost-efficient production and strong export capabilities. Urbanization is accelerating demand for systems such as HVAC, water distribution, and building automation, which are requiring reliable pressure monitoring. Investments in semiconductor fabrication and clean energy projects are increasing demand for high-precision and digital gauges. Manufacturers are leveraging regional cost advantages to scale production while targeting export markets, which is enhancing competitive positioning and supporting long-term market expansion.

Competitive Landscape

The global pressure gauges market is exhibiting a moderately fragmented structure, with the top ten players accounting for approximately 50% of the total revenue share. Leading companies are strengthening their positions through product innovation, digital integration, and geographic expansion. Firms such as WIKA Alexander Wiegand, Ashcroft, and Emerson Electric are leveraging diversified portfolios and established distribution networks to maintain market presence across multiple industries. Mid-tier manufacturers are competing on cost efficiency and regional reach, particularly in Asia Pacific, where local production advantages are influencing procurement decisions.

Competitive differentiation is shifting toward performance attributes such as accuracy, durability, and digital functionality. Companies are investing in research and development (R&D) to introduce smart and connected gauges that align with IIoT adoption trends. Strategic collaborations and acquisitions are enabling firms to expand technological capabilities and access new markets. This competitive environment is encouraging consolidation in high-value segments while sustaining price competition in standardized product categories.

Key Industry Developments

- In February 2026, Titan introduced its Pressure Perfect (P2) smart tire sensor system, developed with Cerebrum Sensor Technologies, enabling real-time monitoring of tire pressure, temperature, and load. The system integrates with onboard inflation controls to automatically adjust pressure during operation, improving efficiency, reducing soil compaction by up to 35%, and potentially increasing crop yields.

- In December 2025, BHEL Haridwar issued a global tender via the Government e-Marketplace (GeM) for the procurement of 65 industrial pressure gauges for an energy project. The tender specifies high-precision stainless steel Bourdon tube gauges with strict vendor approval, quality certification, and Make in India compliance requirements, highlighting increasing localization and quality standards in public sector procurement.

- In September 2025, ABB introduced its P-300 pressure transmitter series in the United States, offering high accuracy of around 0.055% across a wide pressure range and targeting industries such as petrochemical, power, and pulp and paper. The product integrates features such as a backlit human-machine interface (HMI) display and QR-enabled digital diagnostics, enabling easier maintenance and improved operational efficiency.

Companies Covered in Pressure Gauges Market

- WIKA Alexander Wiegand SE & Co. KG

- Ashcroft Inc.

- Emerson Electric Co.

- Honeywell International Inc.

- ABB Ltd.

- Siemens AG

- AMETEK Inc.

- Baker Hughes Company

- Badotherm Group B.V.

- Winters Instruments

- OMEGA Engineering Inc.

- Kobold Messring GmbH

- Dwyer Instruments, LLC

- NOSHOK, Inc.

- AFRISO-EURO-INDEX GmbH

Frequently Asked Questions

The global pressure gauges market is projected to reach US$ 1.5 billion in 2026.

The mandating of real-time pressure monitoring and equipment integrity validation across hazardous industrial environments by regulatory bodies is primarily driving the market.

The market is poised to witness a CAGR of 3.4% from 2026 to 2033.

The integration of pressure systems with IIoT and the critical requirement of continuous monitoring to minimize unplanned downtime and improve asset utilization across industries such as oil & gas and power generation are key market opportunities.

WIKA Alexander Wiegand, Ashcroft, Emerson Electric, Honeywell International, and ABB are few of the key players in the market.