- Specialty & Fine Chemicals

- Polyvinylpyrrolidone Market

Polyvinylpyrrolidone Market Size, Share, and Growth Forecast 2026 - 2033

Polyvinylpyrrolidone Market by Grade (PVP K-15, PVP K-30, PVP K-60), Application (Adhesives, Pharmaceutical, Cosmetics, Food and Beverage), and Regional Analysis, 2026 - 2033

Polyvinylpyrrolidone Market Size and Trends Analysis

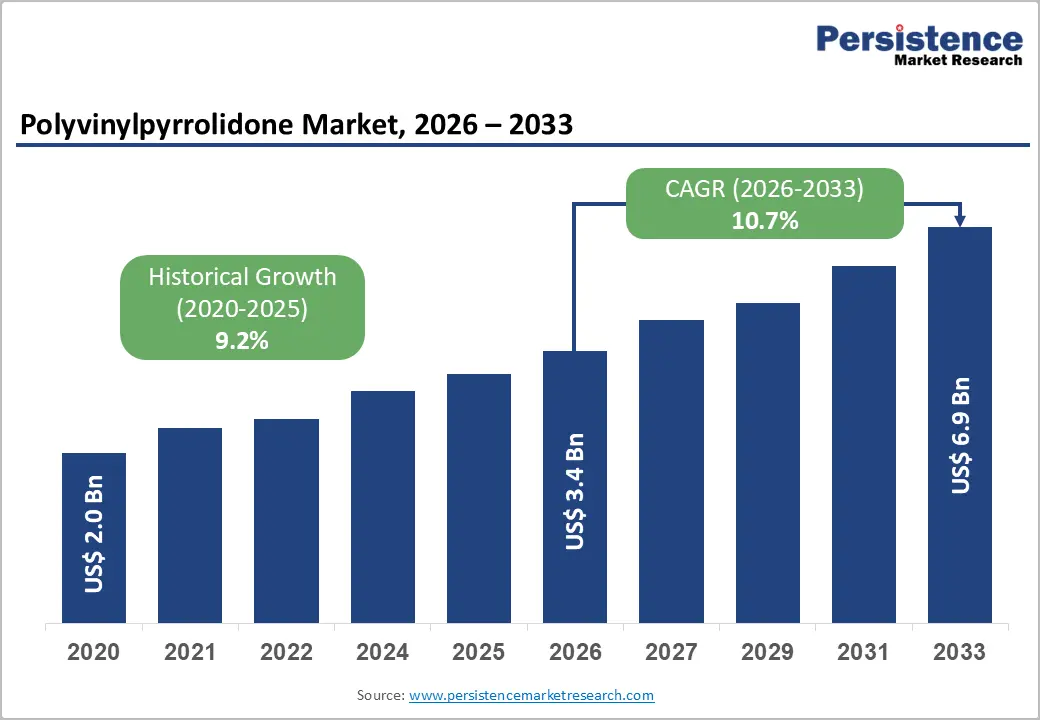

The global polyvinylpyrrolidone market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$6.9 billion by 2033, growing at a CAGR of 10.7% during the forecast period from 2026 to 2033, driven by the rising use of polyvinylpyrrolidone (PVP) as a key excipient in solid oral dosage formulations and fast-growing demand for binder and stabilizer solutions in pharmaceutical manufacturing. Increasing adoption in personal care and cosmetics, especially in hair styling polymers, is further boosting growth.

Key Industry Highlights:

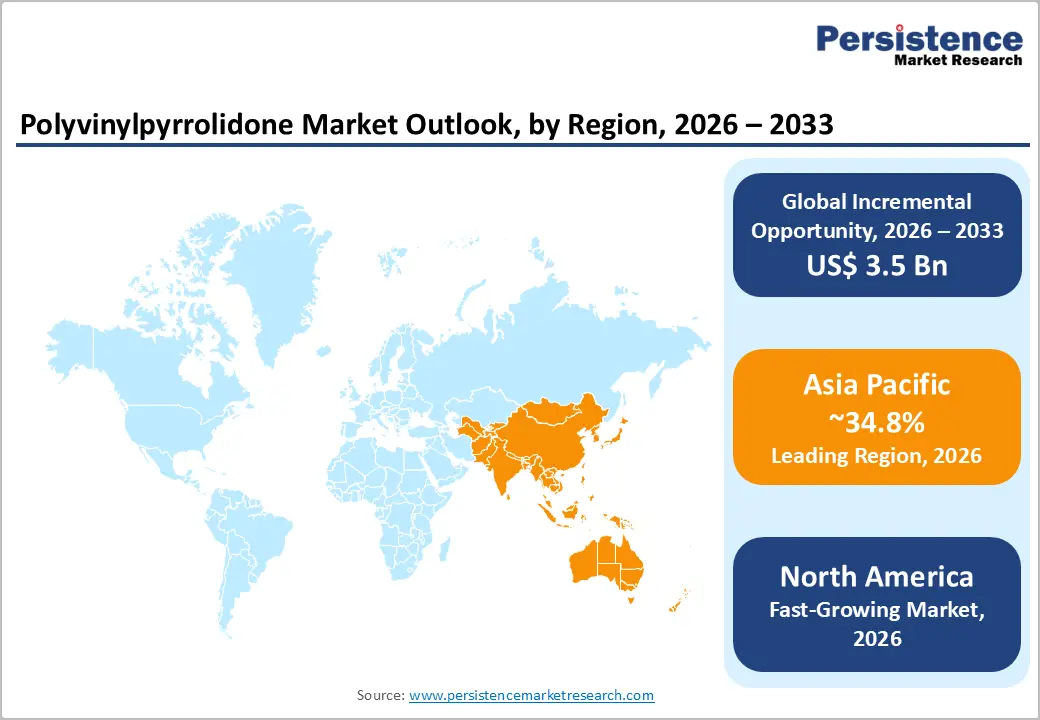

- Leading Region: Asia Pacific, with about a 34.8% share in 2026, owing to its massive pharmaceutical and specialty chemical manufacturing base.

- Fast-growing Region: North America, spurred by rising demand for advanced drug formulations.

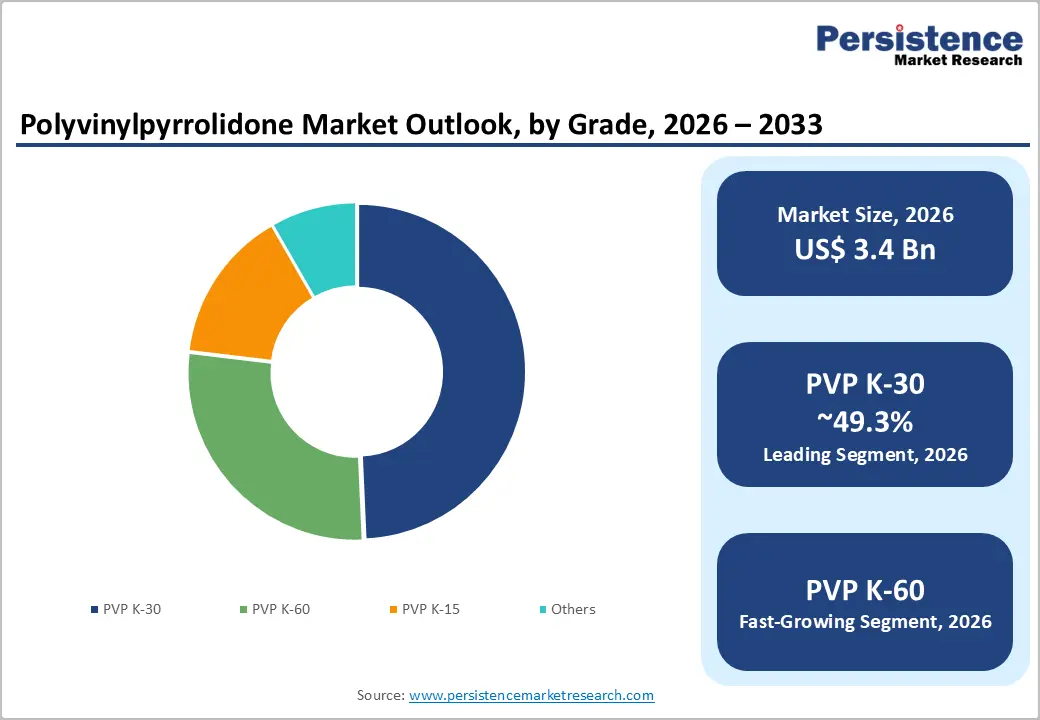

- Leading Grade: PVP K-30, approximately 49.3% share in 2026, as it functions effectively as a binder, film former, solubilizer, and dispersant.

- Dominant Application: Pharmaceuticals, nearly 62.4% in 2026, as PVP is widely used as a binder, coating agent, stabilizer, and solubilizer in oral solid dosage forms.

- Latest Development: In February 2025, BASF highlighted advancements in its Kollidon polyvinylpyrrolidone portfolio for pharmaceutical applications, emphasizing formulation support, excipient innovation, and oral dosage technologies. The company reaffirmed its position as the original developer of PVP and continued investment in high-performance pharmaceutical excipients.

DRO Analysis

Driver - Demand for Pharmaceutical-Grade Excipients in Solid Oral Drug Formulations

Regulatory tightening is influencing how drug makers select binders and solubilizers. Under ICH Q3C guidelines, residual solvent limits in excipients are now non-negotiable, pushing formulators toward high-purity PVP grades that meet United States Pharmacopeia (USP) and Good Manufacturing Practices (GMP) standards. Contract Development and Manufacturing Organizations (CDMOs) in India and China expand output to supply biosimilars and high-potency oral solids.

India is a key example of this pull. The country commissioned 25 new tablet-compression lines between 2024 and 2025 and remains the fastest-growing importer of pharmaceutical-grade PVP. High-viscosity K-90 and K-120 grades, used to engineer extended-release profiles, are finding rising acceptance as brands seek to extend drug lifecycle without reformulating the active compound.

Increasing Use of PVP in Hair-Styling and Personal Care Products

PVP's film-forming ability makes it a preferred fixative in aerosol sprays, hair gels, and wet-look styling products, roles that synthetic alternatives rarely replicate at comparable cost. PVP/VA copolymer is a preferred choice for film forming and as a hair-styling agent, and is suitable for formulations targeting film-forming viscosity. Hair gels, aerosol gas sprays, and wet-look sprays are anticipated to pose new growth opportunities.

Premium positioning is pushing this demand. In December 2024, Brazil-based hair care brand Beox Professional entered India’s market with its premium range providing solutions for coloring, treatments, smoothening, curls, and finishing products. Such launches require performance-stable film formers such as PVP. The global PVP-in-cosmetics market is anticipated to be driven by rising consumer demand for high-performance products and booming online beauty platforms.

Restraint - Instability in N-Vinylpyrrolidone Monomer Pricing

PVP's production begins with N-vinylpyrrolidone (NVP), a monomer built from petrochemical feedstocks, and that dependency creates a persistent cost problem. NVP manufacturing cost is susceptible to fluctuations in its primary raw material, specifically butyraldehyde. Any fluctuation in butyraldehyde pricing can directly affect manufacturing charges for producers. Geopolitical disruptions compound this. Europe's limited domestic NVP production capacity compels reliance on imports from Asia, primarily China and South Korea, exposing the supply chain to logistical barriers and trade policy shifts.

The price swings are measurable. Vinylpyrrolidone monomer experienced 15 to 20% price volatility in recent years due to global supply chain disruptions. Geopolitical factors are affecting petrochemical feedstock, and transportation logistics are creating uncertainty in raw material procurement. For pharmaceutical manufacturers, this unpredictability makes long-term contract pricing difficult to lock in. To mitigate this challenge, manufacturers may implement hedging strategies or seek long-term supply agreements with reliable suppliers. Investment in alternative raw materials or production processes could also help reduce dependence on volatile inputs.

Opportunity - PVP as a Dispersant in Lithium-Ion Battery Slurry

Battery slurry quality is a make-or-break factor in electrode performance. Poorly dispersed cathode materials result in uneven coatings, reduced energy density, and manufacturing rejects. PVP solves this. Its molecular structure carries both polar lactam groups and nonpolar backbone chains, enabling it to coat carbon nanotube and cathode particles and reduce agglomeration. Every ton of carbon nanotube conductive agent requires 12.5 kg of PVP as a dispersant. Increasing demand for PVP dispersants for carbon nanotube conductive agents shows how central PVP has become to battery electrode processing.

Recycling processes are now adding a second demand channel. Battery-grade PVP development and qualification moved closer to end-use needs, especially slurry handling and electrode processing. It is supported by product-specific guidance showing how nonionic dispersant functionality translates into improved stability and manufacturing reliability. Suppliers are already responding. Henan Pengfei New Materials detailed how PVP grades such as K30 were used to optimize slurry behavior and electrode performance, positioning PVP as an enabling component for advanced battery technology.

Adoption of PVP-Based Adhesives in Sustainable Flexible Electronics

The flexible electronics sector is under pressure to replace conventional adhesives with materials that are water-soluble, recyclable, and mechanically reliable under repeated bending. PVP is emerging as a functional base polymer in this transition. A self-healable and recyclable PVP-based ionogel was developed through a one-pot photoinitiated polymerization process. The ionogel exhibited transparency, superior mechanical strength, and excellent ionic conductivity in a single material. A wearable resistive sensor demonstrated an accurate response to human body motion, and a flexible light-emitting device maintained electroluminescence even under bending deformation.

Published in RSC Advances (2024), this work underlines how PVP's nonionic character and solubility profile make it compatible with green processing routes. A parallel shift is happening in foldable display assembly. Sustainable acrylic optically clear adhesives for foldable displays are being developed by incorporating UV-triggered debondability and bio-based degradability, as published in Advanced Materials (2025). PVP's water solubility and film-forming behavior position it as a natural fit for these next-generation adhesive systems where end-of-life disassembly is a design requirement.

Category-wise Analysis

Grade Insights

PVP K-30 is predicted to lead with a share of approximately 49.3% in 2026, as it delivers the most balanced combination of binding strength, solubility, viscosity, and processing ease. Its strong regulatory acceptance is also projected to boost demand. PVP K-30 has been used in pharmaceutical products for decades and appears in various approved drug formulations worldwide. Leading suppliers such as BASF deliver multiple K-30 variants, including low-peroxide and low-nitrite grades, to meet modern pharmaceutical requirements related to formulation stability and nitrosamine risk management.

The PVP K-60 segment is estimated to be the fastest-growing in the forecast period, owing to its expanding applications outside traditional pharmaceuticals. High-molecular-weight PVP grades are now used in battery materials, specialty coatings, and industrial formulations where superior dispersing and stabilizing performance is required. As industries seek materials that can improve particle dispersion and product durability, demand for high-performance PVP grades such as K-60 is rising.

Application Insights

Pharmaceuticals are anticipated to dominate with a share of nearly 62.4% in 2026, as PVP performs several critical functions in a single ingredient. It acts as a binder, solubilizer, crystallization inhibitor, film former, and stabilizer. Few excipients provide such a broad range of functionalities while maintaining a strong safety and regulatory profile. This versatility allows manufacturers to simplify formulations and improve drug performance. BASF identifies povidones as among the most widely used excipients for solid oral dosage forms.

The food and beverage segment is expected to remain in the second position in 2026, as PVP is constantly used as a stabilizing, clarifying, and complexing agent in beverage processing. One of its most valuable properties is its ability to bind polyphenols and other compounds that can cause haze, discoloration, or instability in beverages. This helps manufacturers improve product appearance and shelf stability without significantly affecting flavor.

Regional Insights

Asia Pacific Polyvinylpyrrolidone Market Trends

Asia Pacific is anticipated to dominate in 2026 with a share of nearly 34.8%, as it has become the world's largest pharmaceutical manufacturing hub. China and India account for a significant share of global generic drug production and Active Pharmaceutical Ingredient (API) manufacturing. Since PVP is widely used as a binder, solubilizer, and stabilizer in medicines, growth in pharmaceutical production increases demand for the polymer. The region is also attracting increasing investments in biologics, specialty drugs, and advanced formulations that require high-performance excipients.

China Polyvinylpyrrolidone Market Trends

China will likely lead in Asia Pacific in 2026 with a share of around 42.6%, as it possesses one of the world's largest pharmaceutical and specialty chemical industries. The country has extensive production capacity for APIs, excipients, and fine chemicals, creating a superior domestic customer base for PVP manufacturers. Local companies also benefit from integrated supply chains that allow them to produce raw materials and finished polymers efficiently. China's leadership is further supported by government-backed pharmaceutical modernization programs and investments in healthcare infrastructure.

India Polyvinylpyrrolidone Market Trends

In 2026, India is projected to account for a share of approximately 20.7%, owing to its expanding pharmaceutical manufacturing sector. The country is often called the pharmacy of the world due to its large-scale generic drug exports. As production volumes rise, demand for pharmaceutical excipients, including PVP, continues to increase. Government initiatives are also strengthening the market. Programs focused on domestic API production, pharmaceutical infrastructure development, and supply-chain resilience are encouraging local manufacturing.

North America Polyvinylpyrrolidone Market Trends

North America is predicted to be the fastest-growing region in 2026 with a share of approximately 26.8%, as pharmaceutical companies are constantly developing complex drugs that require advanced excipients. Modern biologics, injectable therapies, and poorly soluble drugs often require functional polymers such as PVP to improve stability and bioavailability. Demand is hence shifting from basic excipients toward higher-value materials. Another growth driver is the increasing focus on domestic pharmaceutical manufacturing. Companies are investing heavily in U.S.-based production facilities to improve supply-chain security and reduce dependence on overseas suppliers.

U.S. Polyvinylpyrrolidone Market Trends

A share of nearly 50.4% is expected to be held by the U.S. in 2026, owing to its leadership in innovative pharmaceuticals, biologics, and specialty medicines. The country remains home to many of the world's key pharmaceutical companies and research organizations. As drug developers focus on complex formulations and personalized medicines, demand for multifunctional excipients such as PVP is predicted to increase. The U.S. government is also encouraging domestic drug manufacturing. In 2025, the FDA introduced initiatives aimed at boosting reviews for domestically manufactured generic drugs.

Europe Polyvinylpyrrolidone Market Trends

Europe will likely see decent growth in the forecast period, with a share of nearly 19.7% in 2026, as it remains a prominent center for pharmaceutical innovation and high-quality drug manufacturing. The region has a strong presence in specialty medicines, biosimilars, and advanced drug delivery technologies, all of which rely heavily on functional excipients. Local pharmaceutical companies also maintain strict quality standards, supporting demand for premium-grade PVP products. The continent’s aging population is increasing demand for medicines used to treat chronic diseases. This trend is encouraging pharmaceutical companies to broaden production of oral and injectable therapies.

Germany Polyvinylpyrrolidone Market Trends

Germany will likely register a substantial share of approximately 33.5% in 2026, as it hosts renowned pharmaceutical producers, research institutions, and specialty chemical companies. These strengths help sustain demand for pharmaceutical-grade PVP despite challenges faced by parts of the broad chemical industry. While Germany's chemical sector has experienced pressure from high energy costs and weak industrial demand, industry associations expect the pharmaceutical segment to remain comparatively resilient. This resilience supports continued investment in pharmaceutical production and specialty excipients.

U.K. Polyvinylpyrrolidone Market Trends

A share of around 18.2% is predicted to be held by the U.K. in 2026, supported by its well-established life sciences sector and research-driven pharmaceutical industry. The country remains a key center for drug discovery, clinical research, and biopharmaceutical development. These activities generate demand for advanced excipients used in innovative formulations. The outlook is also supported by increasing investments in biologics, cell and gene therapies, and complex drug delivery technologies. As pharmaceutical companies move toward more sophisticated formulations, the demand for high-performance excipients such as PVP is predicted to increase.

Competitive Landscape

The global polyvinylpyrrolidone market is moderately concentrated, with a handful of multinational specialty chemical companies controlling much of the pharmaceutical-grade and high-purity PVP supply. Competition is led by leading producers such as BASF, Ashland, Nippon Shokubai, and Boai NKY Pharmaceuticals, which compete primarily on pharmaceutical compliance, product purity, formulation support, and supply reliability rather than price alone. Pharmaceutical customers require USP, EP, and other regulatory-compliant grades, creating high entry barriers and giving established suppliers a competitive advantage.

China-based manufacturers are becoming more influential by extending production capacity and improving quality standards. Companies such as Boai NKY are investing in pharmaceutical-grade production facilities, regulatory certifications, and battery-material applications to move beyond traditional commodity PVP markets. The company also secured EXCiPACT GMP certification for its excipient manufacturing operations, improving its competitiveness in regulated pharmaceutical markets.

Key Industry Developments:

- In September 2025, PharmaExcipients AG investigated the reprocessing potential of polyvinylpyrrolidone (PVP) K-25 across different concentration levels. The study focused on evaluating the physical characteristics of the blends and the resulting paracetamol tablets, with findings confirming PVP K-25’s effectiveness as a binder due to the uniform properties observed in both the mixtures and the final tablet formulations.

- In May 2025, BASF continued expanding the commercialization of Kollidon 90 Evo, a high-purity povidone grade engineered with reduced impurity levels for pharmaceutical formulations. The product was positioned to address increasingly stringent quality requirements for excipients used in oral drug delivery systems.

- In April 2025, BASF introduced Verdessence Maize at in-cosmetics Global 2025 as a plant-based and readily biodegradable styling polymer designed as an alternative to conventional PVP and VP/VA polymers used in personal care formulations. The launch reflects the industry's increasing focus on sustainable and bio-based substitutes for synthetic film-forming polymers.

Companies Covered in Polyvinylpyrrolidone Market

- Ashland

- BASF

- Boai NKY Pharmaceuticals Ltd.

- Glide Chem Private Limited

- Hangzhou Motto Science & Technology Co., Ltd.

- JH Nanhang Life Sciences Co., Ltd.

- NIPPON SHOKUBAI CO., LTD.

- Shanghai Qifuqing Material Technology Co., Ltd.

- Shanghai Yuking Water Soluble Material Tech Co., Ltd.

- Sichuan Lutianhua Co., Ltd

- Thermo Fisher Scientific Inc.

- Sigma-Aldrich Co. LLC (Merck)

Frequently Asked Questions

The global polyvinylpyrrolidone market is projected to be valued at US$3.4 billion in 2026.

The polyvinylpyrrolidone market is expected to reach US$6.9 billion by 2033.

Key market trends include increasing demand for low-impurity pharmaceutical-grade PVP and expansion of pharmaceutical manufacturing in Asia Pacific.

PVP K-30 is expected to be the leading grade with a share of nearly 49.3% in 2026 because its medium molecular weight provides an optimal balance of solubility and binding strength.

The polyvinylpyrrolidone market is expected to grow at a CAGR of 10.7% from 2026 to 2033.

Ashland, BASF, and Boai NKY Pharmaceuticals Ltd. are a few key market players.