- Smart Packaging

- Algae-Based Bioplastics Market

Algae-Based Bioplastics Market Size, Share, and Growth Forecast, 2026 - 2033

Algae-Based Bioplastics Market by Polymer Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Others), Application (Packaging, Automotive, Others), Production Process, and Regional Analysis for 2026 - 2033

Algae-Based Bioplastics Market Size and Trends Analysis

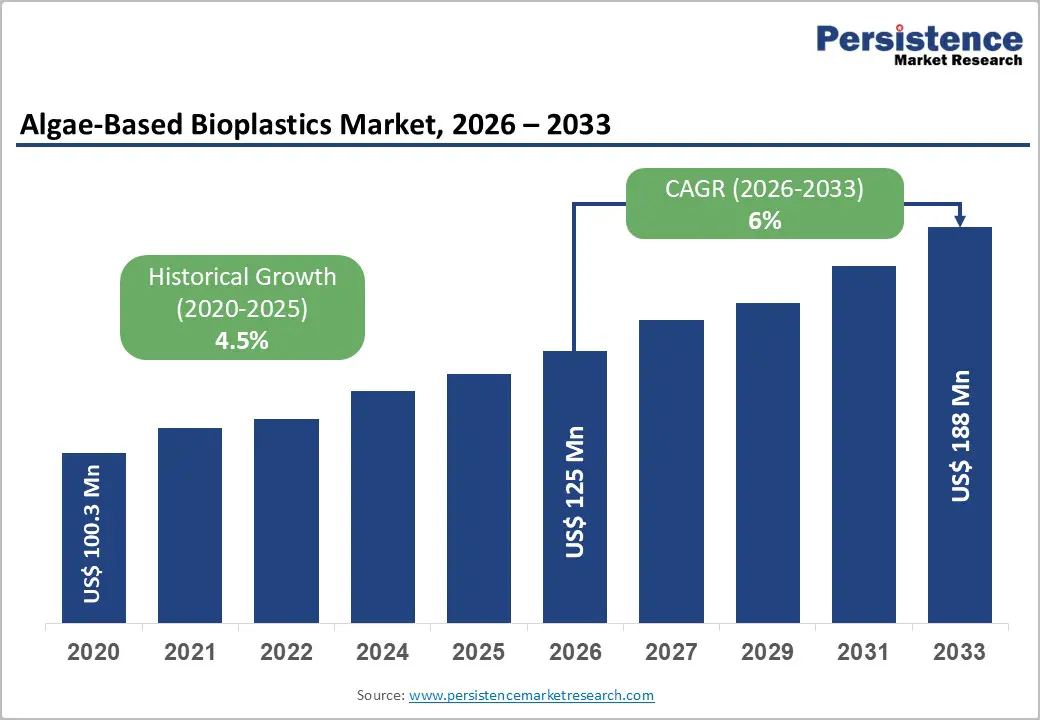

The global algae-based bioplastics market size is likely to be valued at US$ 125 million in 2026 and is expected to reach US$ 188 million by 2033, growing at a CAGR of 6.0% between 2026 and 2033, driven by regulatory pressure to reduce fossil-based single-use plastics, rising corporate sustainability procurement, and measurable performance improvements in algae-derived polymers such as PHA and PLA blends.

Production scale-up across marine and freshwater algae cultivation, combined with advances in extraction and fermentation, is improving feedstock economics. Policy alignment, pilot-to-commercial capacity investments, and partnerships between biopolymer producers and polymer formulators will define the competitive landscape through 2033.

Key Industry Highlights:

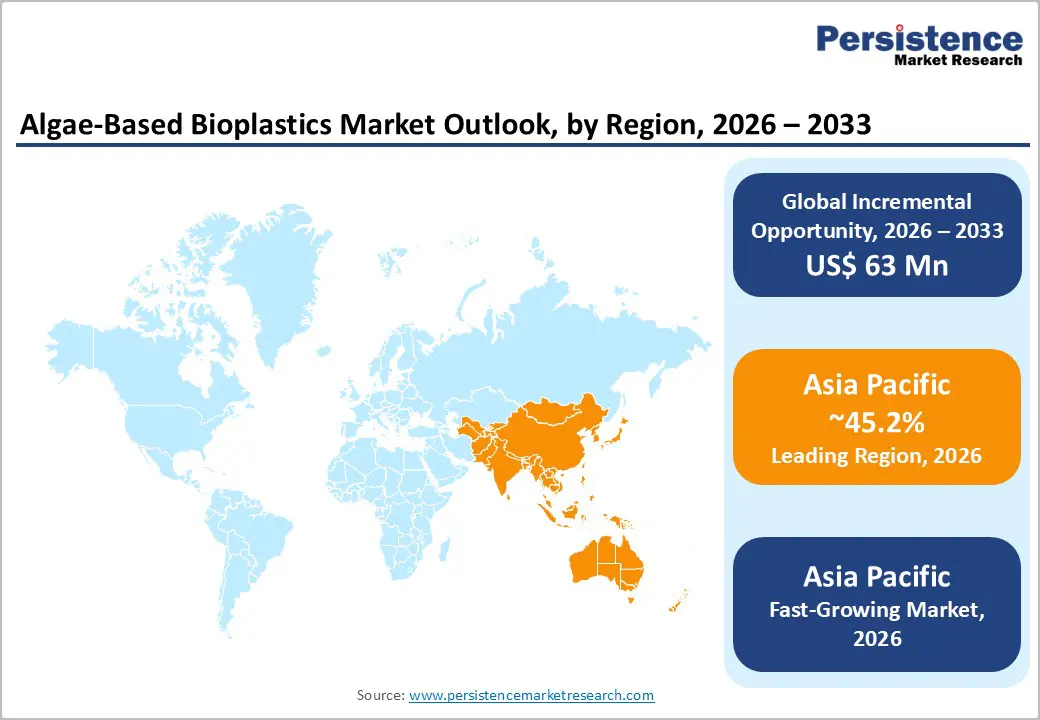

- Leading Region: Asia Pacific is projected to hold approximately 45.2% market share, driven by large-scale manufacturing capacity in China, advanced marine-biodegradable polymer innovation in Japan, and expanding packaging demand across India and Southeast Asia.

- Fastest-growing Region: Asia Pacific is supported by extensive seaweed cultivation, vertically integrated production models, and cost-competitive high-volume packaging grades.

- Investment Plans: Capital allocation is concentrated on fermentation scale-up facilities, vertically integrated algae cultivation-to-polymer extraction infrastructure, and high-volume packaging resin expansion, particularly in the U.S., Germany, China, and Japan.

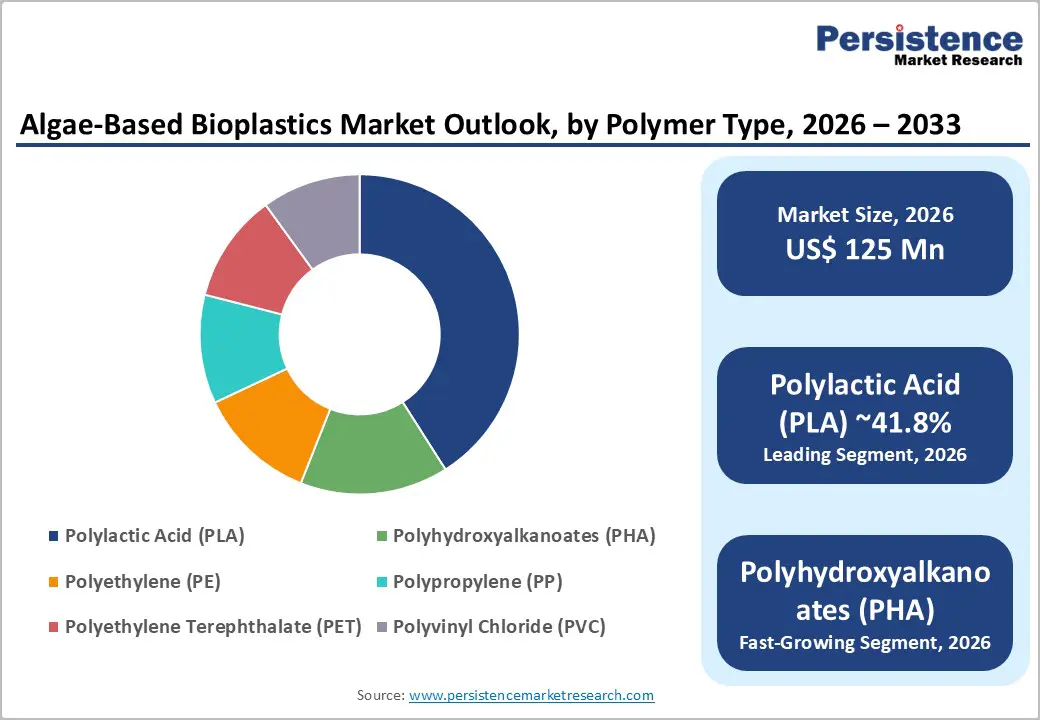

- Dominant Polymer Type: Polylactic Acid (PLA) is anticipated to account for 41.8% of the market share within polymer type segment, supported by established industrial processing compatibility and scalable integration of algae-derived fillers.

- Leading Application: Packaging is anticipated to hold 44.7% of market share, driven by regulatory substitution mandates, high material turnover rates, ESG-linked procurement programs, and rapid adoption in flexible films and thermoformed containers.

| Key Insights | Details |

|---|---|

| Algae-Based Bioplastics Market Size (2026E) | US$125 Mn |

| Market Value Forecast (2033F) | US$188 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory and Policy Tightening Favoring Compostable and Biobased Materials

Global regulatory frameworks aimed at reducing plastic waste are accelerating the adoption of compostable and biobased alternatives. Policies targeting single-use plastics, extended producer responsibility (EPR) modernization, and mandatory recycled or renewable content requirements are reshaping procurement strategies across the packaging and consumer goods industries. In Europe and North America, regulatory structures increasingly require verifiable labeling, compostability standards, and lifecycle transparency. Regulatory clarity reduces adoption risk for brand owners and stimulates demand in food-contact and short-life packaging applications. As compliance requirements intensify, producers of algae-based polymers benefit from stronger offtake visibility and enhanced pricing power in regulated segments.

Technical Maturation and Yield Improvements

Advances in algal strain optimization, photobioreactor engineering, and downstream extraction technologies are lowering the cost per kilogram of biomass while improving polymer yield efficiency. Process intensification in microbial fermentation has strengthened PHA productivity and improved molecular weight control, enabling better mechanical and thermal performance. Lifecycle and techno-economic assessments indicate gradual convergence in performance between algae-derived polymers and certain petrochemical counterparts. Blending technologies now permit drop-in substitution across thermoforming, injection molding, and coating applications. Improved material performance and production efficiency reduce historical adoption barriers. Investors and manufacturers now observe clearer pathways from R&D to commercial-scale production, supporting capacity expansion and long-term margin realization.

Corporate Procurement and Sustainability Commitments

Large consumer goods companies, food service operators, and retail groups are implementing measurable sustainability targets, including Scope 3 emissions reduction and packaging recyclability or compostability commitments. These organizations increasingly engage in joint development agreements with algae-material producers to validate supply chains and material performance. In several cases, brands provide pre-commercial purchase guarantees or premium pricing structures to accelerate commercialization. Early procurement commitments reduce commercialization risk and shorten capital recovery timelines for producers. Co-development of application-specific grades, such as barrier-coated paperboard and flexible films, accelerates route-to-market execution.

Barrier Analysis - Unit Economics and Feedstock Cost Volatility

Algae cultivation remains more capital-intensive than conventional crop-based feedstocks. Nutrient inputs, photobioreactor infrastructure, harvesting systems, and energy usage contribute to elevated production costs. Seasonal variability and biomass yield fluctuations can produce price instability. Techno-economic analyses frequently indicate a cost differential versus commodity polyethylene and polypropylene that remains significant without policy incentives or premium positioning.

End-of-Life Infrastructure and Standards Alignment

Compostability claims require access to industrial composting infrastructure and compliance with recognized certification standards. In regions lacking adequate organics processing capacity, biodegradable materials may not realize their intended environmental benefit. Labeling inconsistencies and limited consumer awareness may contaminate recycling streams or reduce sorting efficiency.

Opportunity Analysis - PHA Commercialization for Compostable Packaging

Polyhydroxyalkanoates (PHA) represent one of the most promising growth pathways within algae-based bioplastics. Fully compostable and capable of biodegradation in soil and marine environments, PHA materials meet increasing regulatory and brand requirements for sustainable packaging. Fermentation scale-up partnerships and licensing agreements are enabling larger production capacities, positioning PHA for broader penetration into trays, films, molded containers, and barrier coatings. Companies investing in industrial-scale fermentation infrastructure and application development will capture premium market segments and differentiated margins.

Seaweed-Derived Coatings and Functional Additives

Algae extracts such as polysaccharides, proteins, and pigments offer value beyond polymer feedstock. These compounds can function as barrier coatings, antimicrobial additives, and UV stabilizers. Integrating these outputs into a multi-product biorefinery model improves overall economics by diversifying revenue streams. Co-location with nutraceutical or food processing facilities can optimize resource utilization. Vertical integration and co-product monetization significantly enhance return on investment and reduce effective feedstock cost per polymer-equivalent kilogram.

Category-wise Analysis

Polymer Type Insights

Polylactic Acid (PLA) is anticipated to account for approximately 41.8% of market share in 2026, maintaining its leadership position within algae-based polymer blends. Its dominance stems from a well-established global production ecosystem and strong compatibility with conventional processing techniques such as thermoforming, injection molding, extrusion, and blown film manufacturing. This allows manufacturers to integrate algae-derived fillers or biomass co-feedstocks without major capital modifications to existing lines. In commercial applications, algae-enhanced PLA blends are widely used in rigid food containers, compostable cups, fresh-produce trays, and flexible packaging films. For example, algae-infused PLA compounds are increasingly utilized in sustainable takeaway packaging and retail clamshells where higher biobased content improves brand sustainability metrics while preserving clarity and stiffness. Given PLA’s industrial-scale output and mature supply chain, it remains the primary volume and revenue contributor within the segment.

Polyhydroxyalkanoates (PHA) are expected to exhibit the strongest projected growth rate among polymer categories, driven by superior biodegradability and expanding fermentation-based production capacity. Unlike PLA, PHA can biodegrade in marine and soil environments, positioning it favorably in regions implementing stringent single-use plastic regulations. Continuous advances in strain engineering and downstream processing have improved polymer consistency, melt stability, and compatibility with film extrusion and coating technologies. PHA is increasingly adopted in compostable flexible films, coated paperboard for food service, and agricultural mulch films. Several pilot projects in Europe and North America have demonstrated PHA-algae composite films for snack packaging and single-use cutlery applications. As regulatory frameworks increasingly prioritize compostability and extended producer responsibility (EPR) compliance, PHA’s functional and environmental profile supports accelerated adoption across highly regulated packaging segments.

Application Insights

Packaging is anticipated to account for approximately 44.7% of market share in 2026, making it the largest application segment. Strong regulatory momentum toward biobased and compostable materials, combined with high material turnover rates, supports rapid substitution opportunities. Flexible films, thermoformed containers, coated paperboard, rigid trays, and single-use food service items represent the primary demand clusters driving segment growth. Algae-integrated materials are particularly attractive in secondary and tertiary packaging formats, where mechanical performance requirements are moderate and sustainability branding is highly visible. Retail-ready packaging, e-commerce mailers, and quick-service restaurant containers increasingly incorporate algae-based blends to enhance renewable content claims and support ESG disclosures. The relative ease of material substitution in packaging compared to structural applications accelerates commercialization timelines and volume scalability.

Automotive applications represent the fastest-growing segment, supported by OEM strategies focused on lightweighting and carbon footprint reduction. Algae-derived composites, fillers, and reinforced biopolymer panels are being evaluated for interior trim components, door panels, dashboards, and seat-back structures. These materials contribute to vehicle mass reduction and support lifecycle emission targets aligned with global decarbonization policies. Although total volume remains lower than packaging, automotive applications deliver higher per-unit value and benefit from multi-year supply contracts once qualified. For example, algae-based thermoplastic composites are being piloted in interior panels and decorative trim elements where aesthetic differentiation and sustainability credentials enhance brand positioning. This combination of premium pricing, innovation-driven adoption, and regulatory alignment supports a comparatively higher CAGR within the automotive segment.

Regional Insights

North America Algae-Based Bioplastics Market Trends - Venture-Backed Commercial Scale-Up, EPR Policy Support, and Marine-Biodegradable Polymer Commercialization

North America represents a strategically significant market characterized by early commercial adoption among multinational brand owners and a mature venture capital ecosystem supporting bio-based materials innovation. The U.S. leads regional demand due to its large-scale packaging industry, advanced converting infrastructure, and strong corporate sustainability procurement programs. Major consumer goods companies such as PepsiCo and Coca-Cola have publicly committed to increasing renewable and compostable content in packaging portfolios, reinforcing demand for next-generation biopolymers, including algae-integrated blends.

Growth momentum is reinforced by state-level Extended Producer Responsibility (EPR) frameworks, particularly in California, Oregon, and Colorado, which mandate producer accountability and encourage compostable alternatives. Federal initiatives led by the U.S. Environmental Protection Agency emphasize waste reduction, recyclability labeling clarity, and lifecycle emissions accounting, influencing certification and material qualification pathways.

Companies such as Danimer Scientific have expanded PHA production capacity in Kentucky, while Loliware has commercialized seaweed-derived resins for single-use applications. These developments accelerate pilot-to-commercial transitions and validate marine-biodegradable polymer models. Investment is increasingly concentrated in fermentation scale-up infrastructure, regional biomass sourcing, and strategic collaborations linking algae cultivators with compounders and packaging converters. Canada complements regional growth with coastal cultivation potential in British Columbia and Nova Scotia, supported by targeted bioeconomy incentives and ocean-based innovation programs.

Europe Algae-Based Bioplastics Market Trends - Green Deal-Funded Biorefinery Expansion, EN 13432 Certification Alignment, and Vertically Integrated Compostable Value Chains

Europe demonstrates advanced regulatory alignment, established organic waste collection systems, and strong policy-driven demand for compostable and biobased materials. EU directives targeting single-use plastics and packaging waste reduction have created a stable substitution environment. Germany and France lead in biorefinery projects and industrial pilots, supported by funding mechanisms under the European Green Deal and Horizon Europe programs. German chemical majors such as BASF have strengthened their compostable polymer portfolio through products like ecovio®, while French materials producer TotalEnergies Corbion has expanded PLA production capacity in Europe to meet rising regional demand. These expansions directly improve supply reliability for converters integrating algae-based fillers into PLA matrices. In France, public-private consortia are advancing microalgae biorefinery pilots aimed at extracting lipids and biopolymers for packaging and specialty films. The U.K. hosts innovative seaweed-material startups such as Notpla, which has commercialized seaweed-based coatings and takeaway packaging solutions adopted at large-scale events and food-service chains. Spain benefits from favorable coastal cultivation conditions in Galicia and Andalusia, supporting macroalgae feedstock development for biopolymer extraction and composite applications.

EU-wide harmonized certification frameworks, including EN 13432 compliance for compostability, reduce cross-border compliance uncertainty and facilitate trade of certified materials. Investment trends increasingly emphasize vertically integrated value chains, from algae cultivation to polymer compounding, supported by publicly funded scale-up programs. Europe remains a benchmark region for regulatory-driven demand and infrastructure readiness, though long-term competitiveness will depend on improving cost parity with fossil-based plastics and securing consistent raw material scaling.

Asia Pacific Algae-Based Bioplastics Market Trends - Seaweed Feedstock Abundance, Cost-Competitive Biopolymer Manufacturing, and High-Volume Marine-Degradable Packaging Growth

Asia Pacific leads the algae-based bioplastics market with approximately 45.2% share and remains the fastest-growing region through the forecast period. The region benefits from large-scale manufacturing capacity, extensive aquaculture infrastructure, and competitive labor and processing costs. China plays a central role due to its dominant packaging production base and strong domestic consumption. Major packaging converters and material suppliers such as Kingfa Sci. & Tech. have expanded biopolymer compounding capabilities, integrating renewable fillers to serve both domestic and export markets. Japan emphasizes high-performance and precision-engineered applications. Companies like Kaneka Corporation have commercialized marine-biodegradable PHA polymers under the PHBH™ brand, supporting adoption in flexible packaging and consumer goods. Japan’s focus on marine pollution reduction aligns strongly with algae-integrated and ocean-degradable material innovation.

India demonstrates rapid uptake in agricultural mulch films, compostable carry bags, and cost-sensitive packaging formats, supported by national bans on certain single-use plastics. Domestic manufacturers are exploring algae-blended compounds to reduce resin costs while increasing renewable content. Southeast Asia, particularly Indonesia and the Philippines, provides extensive seaweed cultivation capacity, reinforcing feedstock security for regional processors. Regional governments are advancing bioeconomy strategies and plastic waste reduction roadmaps, stimulating investments in vertically integrated cultivation-to-extraction models and export-oriented production hubs. Asia Pacific’s structural cost advantages, large-scale seaweed farming base, and integrated manufacturing ecosystem provide durable regional leadership through 2033, particularly in high-volume packaging and marine-biodegradable polymer applications.

Competitive Landscape

The global algae-based bioplastics market exhibits moderate concentration, combining specialized algae-material innovators with larger biopolymer producers and formulation companies. Startups dominate early-stage seaweed packaging innovation, while established polymer companies provide scale, distribution, and licensing frameworks. The industry is transitioning from fragmented pilot activity to structured licensing and capacity consolidation as commercial volumes increase.

Key competitive strategies include partnered scale-up, licensing-based fermentation expansion, co-development with brand owners, and vertically integrated biorefinery models. Companies differentiate through IP strength, feedstock security, and application-specific formulation expertise.

Key Industry Developments

- In September 2025, Sulzer and TripleW jointly announced a collaboration to produce the world’s first polylactic acid (PLA) bioplastic made entirely from food waste, enabling a pilot project to transition into industrial-scale production using food industry side streams as raw material.

- In November 2025, P2 Science and Algenesis announced a strategic partnership to develop and commercialize 100% biobased, biodegradable polyurethanes derived from algae, expanding algae feedstock use beyond traditional polymers into high-performance elastomers and coatings.

Companies Covered in Algae-Based Bioplastics Market

- Danimer Scientific

- Kaneka Corporation

- TotalEnergies Corbion

- BASF

- Kingfa Sci. & Tech.

- NatureWorks

- Loliware

- Notpla

- RWDC Industries

- Cargill

- Corbion

- CJ Biomaterials

- Algix

- Green Dot Bioplastics

- Toray Industries

- Mitsubishi Chemical Group

- Biome Bioplastics

- Ecovative

Frequently Asked Questions

The global market size is estimated at US$125 billion in 2026.

The market is projected to reach US$188 billion by 2033.

Key trends include increasing integration of algae-derived fillers into PLA and PHA matrices, expansion of marine-biodegradable polymer production, vertically integrated cultivation-to-polymer models in Asia Pacific, and regulatory-driven packaging substitution in North America and Europe.

Packaging is the leading application segment, accounting for approximately 44.7% share, driven by regulatory mandates, high material turnover, and corporate sustainability procurement programs.

The market is expected to grow at a CAGR of 6% between 2026 and 2033.

Major players include Danimer Scientific, Kaneka Corporation, TotalEnergies Corbion, BASF, and NatureWorks.