- Smart Packaging

- Bees Wax Wrap Market

Bees Wax Wrap Market Size, Share, and Growth Forecast, 2026 - 2033

Bees Wax Wrap Market by Product Type (Sheets, Pouches/Bags, Others), End-user (Household/Residential Consumers, Commercial Establishments/Food Service, Others), Distribution Channel and Regional Analysis for 2026 - 2033

Bees Wax Wrap Market Size and Trends Analysis

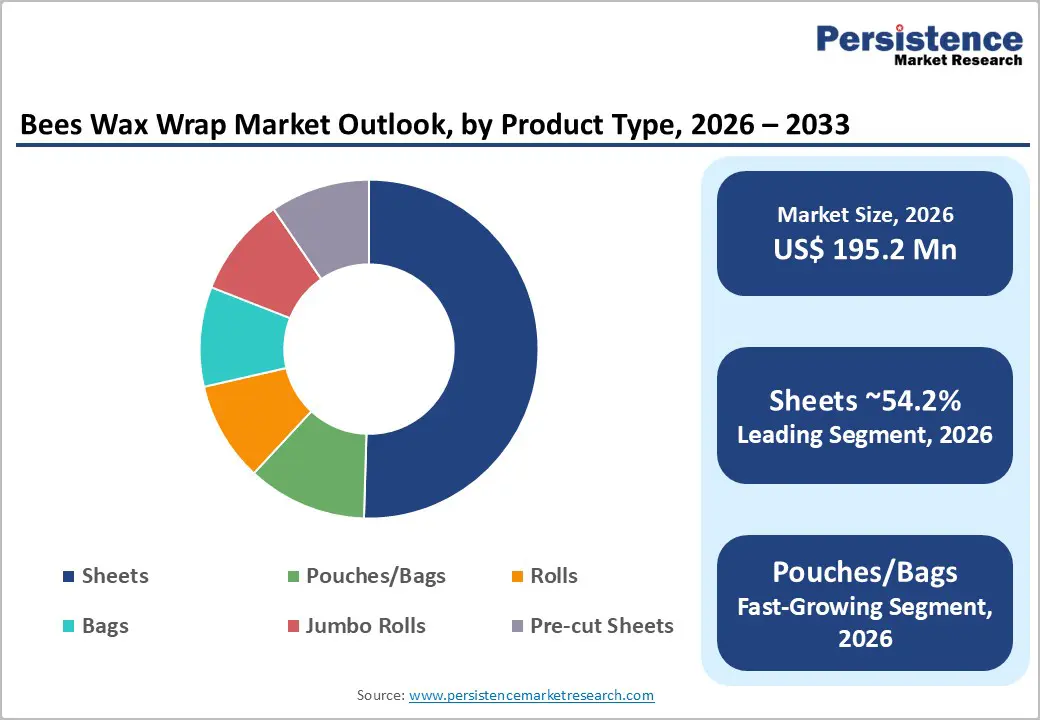

The global bees wax wrap market size is likely to be valued at US$195.2 million in 2026 and is expected to reach US$303.3 million by 2033, growing at a CAGR of 6.5% between 2026 and 2033, driven by regulatory pressure on single-use plastics, rising consumer demand for reusable and low-waste kitchen solutions, and rapid expansion of online and direct-to-consumer (DTC) distribution models.

The market is transitioning from niche eco-conscious adoption to broader mainstream retail integration. Product innovation, including vegan wax alternatives and enhanced durability formulations, is improving lifetime value and repeat purchase rates. Key risks include raw material volatility in beeswax supply, competitive substitution from silicone and polymer-based reusable wraps, and evolving food-contact compliance standards in regulated markets.

Key Industry Highlights:

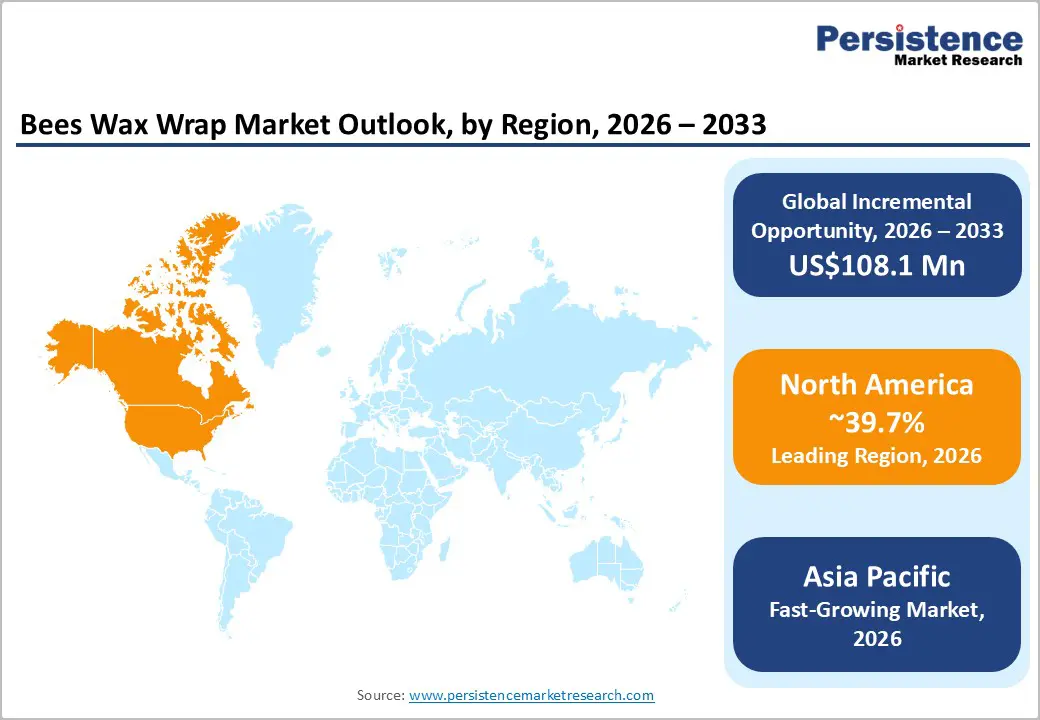

- Leading Region: North America is projected to account for approximately 39.7% of market share, driven by strong DTC penetration, established reusable wrap brands, and supportive state-level sustainability regulations.

- Fastest-Growing Region: Asia Pacific is supported by urbanization, manufacturing scalability, and rising adoption in China and India.

- Investment Plans: Focus on DTC expansion, subscription-based models, regional manufacturing hubs in Asia Pacific, and private-label partnerships across Europe and North America to strengthen recurring revenue streams.

- Dominant Product Type: Sheets are anticipated to hold 54.2% of market share, supported by standardized sizing, multipack formats, and broad household compatibility.

- Leading End-User: Household/Residential Consumers are anticipated to account for 63.4% of market share, driven by zero-waste lifestyle adoption, gifting trends, and repeat purchase cycles.

| Key Insights | Details |

|---|---|

| Bees Wax Wrap Market Size (2026E) | US$195.2 Mn |

| Market Value Forecast (2033F) | US$303.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 1.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory and Policy Pressure on Single-Use Plastics

Governments across North America, Europe, and parts of Asia Pacific continue tightening regulations on single-use plastics and packaging waste. Legislative frameworks targeting waste reduction, recyclability, and extended producer responsibility (EPR) are increasing compliance requirements for retailers and food service operators. As a result, reusable food storage alternatives such as beeswax wraps are gaining institutional and household traction. Regulatory measures are reshaping procurement priorities in food retail and hospitality sectors. Businesses seeking alignment with sustainability commitments increasingly evaluate reusable wrapping materials as substitutes for plastic cling film. This regulatory push directly expands the addressable market and supports above-historical growth rates through 2033.

Consumer Sustainability Preferences and Health Awareness

Consumers demonstrate growing concern regarding plastic waste, microplastic contamination, and exposure to synthetic food-contact materials. This shift in behavior supports premium positioning for natural, reusable wraps composed of cotton, beeswax, and plant-based resins. Urban households, particularly among millennials and Gen Z demographics, are driving trial and adoption rates. The economic argument further strengthens adoption. Many consumers calculate cost parity or savings within months compared to continuous purchases of disposable plastic wraps. Improved product durability and expanded size assortments enhance convenience and reduce replacement frequency. As sustainability transitions from lifestyle choice to purchasing expectation, beeswax wraps benefit from structural demand support.

Channel Expansion through E-commerce and DTC Models

Online retail and direct-to-consumer sales models reduce distribution layers, improving margin retention and enabling rapid product iteration. Subscription programs, bundle offerings, and cross-selling strategies increase average order value and customer lifetime value. Digital channels also allow smaller manufacturers to scale without incurring traditional retail listing costs. This democratization of distribution has expanded the competitive landscape while accelerating geographic penetration. As e-commerce penetration continues rising globally, beeswax wrap brands benefit from broader visibility and repeat-purchase automation mechanisms.

Barrier Analysis - Beeswax Supply Volatility and Cost Sensitivity

Beeswax production is dependent on agricultural cycles, climate conditions, and colony health. Variability in honey production and environmental disruptions can lead to price fluctuations. A 20-30% increase in beeswax input costs can elevate finished product manufacturing costs by approximately 8-12%, depending on formulation composition. Smaller manufacturers with limited sourcing diversification are particularly exposed. To mitigate risk, companies are adopting blended wax formulations and expanding supplier networks. Nevertheless, raw material volatility remains a structural vulnerability within the value chain.

Competitive Substitution and Performance Perception

Silicone food covers, reusable plastic containers, and heat-sealable alternatives present competitive substitution risks. Some consumers perceive beeswax wraps as less durable in high-moisture or raw-protein applications. Where longevity is prioritized over compostability, alternative products may capture share. Without continued innovation and education regarding appropriate usage, penetration growth in certain demographics could lag by 5-8 percentage points relative to forecast expectations. Addressing performance perception remains critical for sustained adoption.

Opportunity Analysis - Development of Vegan and Plant-Based Alternatives

The introduction of plant-based wax formulations expands addressable consumer segments, including vegans and allergy-sensitive buyers. These alternatives reduce reliance on beeswax supply while improving regulatory acceptance in certain markets. Strategically, manufacturers can leverage R&D investments to differentiate through proprietary blends and enhanced durability. Capturing even a modest percentage of conventional plastic wrap spending in developed markets represents substantial incremental revenue potential over the forecast period.

Foodservice and Institutional Adoption

Commercial kitchens, cafés, bakeries, and catering operations present high-volume purchasing potential. Reusable wrapping systems tailored for institutional environments can generate recurring contract revenue. As foodservice operators seek visible sustainability initiatives, beeswax wraps offer branding alignment and regulatory compliance benefits. Industrial-grade roll formats and standardized sanitation protocols could accelerate institutional penetration.

Circular Economy and Composting Integration

Implementing take-back programs and certified composting solutions enhances brand credibility. Clear end-of-life guidance improves consumer confidence and strengthens sustainability positioning. Companies integrating circular economy models can justify premium pricing and improve repeat purchase frequency. Trust and traceability mechanisms are expected to increase retention rates by 10-15% among sustainability-focused consumers.

Category-wise Analysis

Product Type Insights

Sheets are anticipated to account for approximately 54.2% of market share in 2026, maintaining their position as the dominant product format. Their versatility in covering bowls, produce, baked goods, and leftovers makes them the preferred entry-level solution across both online and offline retail channels. Multipack offerings, often sold in assorted sizes, drive higher transaction values while simplifying inventory management for supermarkets and specialty eco-stores. Standardized sizing reduces manufacturing complexity and improves supply chain efficiency, allowing brands such as reusable wrap specialists to scale production with lower SKU variability. Sheets also form the core component of DTC starter kits, where brands bundle small, medium, and large formats to encourage trial and repeat usage. Their broad compatibility with household containers reinforces long-term adoption and category leadership.

Pouches and bags represent the fastest-growing product category, supported by strong consumer demand for portability and structured storage. Unlike flat sheets, pouch formats incorporate reinforced seams and fold-over or button closures, improving usability for packed lunches, snack storage, and on-the-go consumption. These design enhancements position them as a functional upgrade for school-aged children and office workers. Adoption within meal-prep routines and school lunch programs continues to accelerate growth above the market average. Retailers experimenting with branded reusable packaging concepts, including private-label eco-bags, are contributing incremental demand. Hospitality chains and boutique bakeries are also testing reusable pouch formats for takeaway orders, strengthening their commercial viability and expanding the addressable market.

End-user Insights

Households are anticipated to account for approximately 63.4% of market share in 2026, forming the foundational demand base for the industry. Growth stems from rising urban sustainability awareness, eco-conscious gifting trends, and integration into zero-waste lifestyle practices. Consumers increasingly replace single-use plastic wraps with durable, washable alternatives, particularly in metropolitan markets with strong environmental advocacy. Repeat purchase cycles remain stable when durability and maintenance instructions are clearly communicated. Social media demonstrations and influencer-led sustainability campaigns further reinforce product education and trial. Subscription-based refill or accessory programs, such as wrap conditioners and cleaning solutions, also support recurring revenue within the residential segment.

Commercial establishments represent the fastest-growing end-user segment, driven by regulatory pressure on single-use plastics and corporate sustainability commitments. Cafés, bakeries, catering services, and boutique hospitality operators are piloting reusable wrap programs to reduce packaging waste and enhance brand positioning. Higher-volume procurement contracts and predictable replenishment cycles make this segment strategically important for scalability. Foodservice chains implementing ESG reporting frameworks are increasingly incorporating reusable packaging solutions into measurable waste-reduction targets, accelerating institutional adoption and creating long-term growth momentum.

Regional Insights

North America Bees Wax Wrap Market Trends - Premium Retail Penetration, ESG-Driven Merchandising Expansion, and Stable Replacement Demand

North America accounts for approximately 39.7% of market share in 2026, maintaining its position as the leading regional market. The U.S. contributes the largest share, supported by high e-commerce penetration, widespread adoption of sustainable household products, and the strong presence of established reusable food wrap brands such as Bee's Wrap and Abeego. Distribution through platforms such as Amazon and natural grocery chains including Whole Foods Market enhances product accessibility and supports premium positioning. Retail sustainability initiatives reinforce category stability. Major retailers such as Walmart and Target Corporation have expanded shelf space for reusable kitchen alternatives as part of broader ESG commitments. Although federal single-use plastic restrictions remain limited, state-level policies, such as plastic bag bans in California and New York, encourage consumer behavioral shifts toward reusable solutions. Clear guidance from the U.S. Food and Drug Administration on food-contact materials provides regulatory certainty for manufacturers, reducing compliance risk and facilitating product innovation. Investment activity across the region centers on DTC expansion, subscription replenishment programs, and product-line extensions such as reusable sandwich bags and storage kits. Crowdfunding platforms have also supported smaller sustainability-focused startups entering the market. Given relatively high household penetration rates, North America is expected to function as a stable revenue anchor through 2033, with growth primarily driven by premiumization and product upgrades rather than first-time adoption.

Europe Bees Wax Wrap Market Trends - Policy-Led Market Structuring, Private-Label Growth, and Regulatory-Aligned Retail Expansion

Europe represents a substantial share of global demand, underpinned by harmonized sustainability legislation and strong consumer environmental awareness. Countries such as Germany and the U.K. were early adopters of zero-waste kitchen products, supported by specialty retailers and eco-focused chains. Retailers including Tesco and Carrefour have expanded reusable household product assortments in response to regulatory and consumer pressure. Independent European brands such as Bienenwachstuch have gained regional visibility through online marketplaces and sustainable living stores.

Policy frameworks play a defining role in market expansion. The European Commission implemented the Single-Use Plastics Directive, which restricts specific disposable plastic products and sets broader waste-reduction targets. This regulatory clarity encourages retailers to prioritize reusable packaging alternatives and integrate them into sustainability roadmaps. France’s anti-waste legislation, including phased packaging restrictions in food retail, has also stimulated consumer awareness and category trial. Private-label introductions are a notable regional trend, as supermarkets seek to improve margins while aligning with regulatory obligations. Regional manufacturing investments, particularly in Eastern Europe, help reduce logistics costs and carbon footprints. While pricing competition remains strong due to the presence of multiple eco-brands, Europe benefits from predictable policy direction, making it one of the most structurally supported markets globally.

Asia Pacific Bees Wax Wrap Market Trends - Scalable Manufacturing Leadership, Urban Consumption Growth, and Export-Oriented Supply Chain Development

Asia Pacific is the fastest-growing regional market, driven by rapid urbanization, expanding middle-class populations, and scalable manufacturing capabilities. China and India represent long-term volume opportunities due to large household bases and increasing environmental awareness. Japan, meanwhile, maintains premium positioning supported by stringent food-safety oversight and high consumer standards for product quality. Manufacturing advantages significantly influence regional dynamics. China serves as a major production hub for reusable food storage products, supplying both domestic demand and export markets. E-commerce platforms such as Alibaba Group facilitate rapid distribution across urban centers, accelerating consumer access. In India, policy initiatives led by the Ministry of Environment, Forest, and Climate Change, including nationwide single-use plastic bans, have heightened awareness of reusable alternatives. Japan’s retail ecosystem, including chains such as MUJI, has promoted minimalist and sustainable kitchen solutions, indirectly supporting adoption of reusable wrap formats. Meanwhile, regional export partnerships enable private-label supply agreements with Western retailers, strengthening Asia Pacific’s role as both a production base and a high-growth consumption market. Localization of production facilities in Southeast Asia further reduces logistics costs and supports competitive pricing, positioning the region as a central growth engine through the forecast period.

Competitive Landscape

The global bees wax wrap market is moderately fragmented, consisting of specialized eco-focused brands alongside private-label entrants. Market concentration is higher in North America and Europe, while Asia Pacific remains more distributed among smaller manufacturers. Competitive differentiation centers on material quality, durability, certification, and brand storytelling. Innovation and supply chain transparency serve as primary value drivers. Leading companies emphasize product innovation, omnichannel distribution, and supply chain resilience. Premium brands differentiate through certification and traceability, while emerging players compete through price competitiveness and localized production efficiency.

Key Industry Developments:

- In May 2025, Bee’s Wrap secured a nationwide retail partnership with Target, placing its sustainable bees wax wraps in over 550 stores across the U.S. after using advanced data analytics to align its direct-to-consumer demand with Target’s shopper profiles.

Companies Covered in Bees Wax Wrap Market

- Bee's Wrap

- Abeego

- Etee Inc.

- SuperBee Wax Wraps

- The Beeswax Wrap Co.

- Bee Green Wraps

- Khala & Co.

- Meli Wraps

- Beeswax Wraps Australia

- LilyBee Wrap

- Eco Living International

- Wrappa Reusable Food Wraps

- Bee Eco Wraps

- Nature Bee

- Goldilocks Wraps

- BeeBee & Leaf

- Bee Food Wraps

- Gaia Beeswax Wraps

Frequently Asked Questions

The global bees wax wrap market is estimated to be valued at US$195.2 million in 2026.

The bees wax wrap market is projected to reach US$303.3 million by 2033.

Key trends include growing zero-waste lifestyle adoption, premiumization of eco-friendly kitchen products, expansion of DTC subscription models, and rising private-label participation by retailers. Product innovation in reinforced pouches and improved sealing mechanisms is also strengthening repeat purchase rates.

By product type, sheets lead with an anticipated 54.2% market share, owing to versatility and standardized sizing. By end user, household/residential consumers dominate with an anticipated 63.4% revenue share, forming the primary demand base of the market.

The bees wax wrap market is expected to grow at a CAGR of 6.5% from 2026 to 2033.

Major players include Bee's Wrap, Abeego, Etee Inc., SuperBee Wax Wraps, and The Beeswax Wrap Co.