- Biotechnology

- Organoids Market

Organoids Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Organoids Market by Product (Organoid Models, Reagents & Kits, Media & Supplements), Organ Type (Intestinal, Liver, Brain, Kidney, Lung, Pancreatic, Others), Source (Pluripotent Stem Cells, Adult Stem Cells, Primary Tissues), Application (Drug Discovery & Development, Drug Toxicity & Efficacy Testing, Disease Modeling, Personalized Medicine, Regenerative Medicine & Tissue Engineering, Developmental Biology, Others), and Regional Analysis from 2026 to 2033

Organoids Market Share and Trends Analysis

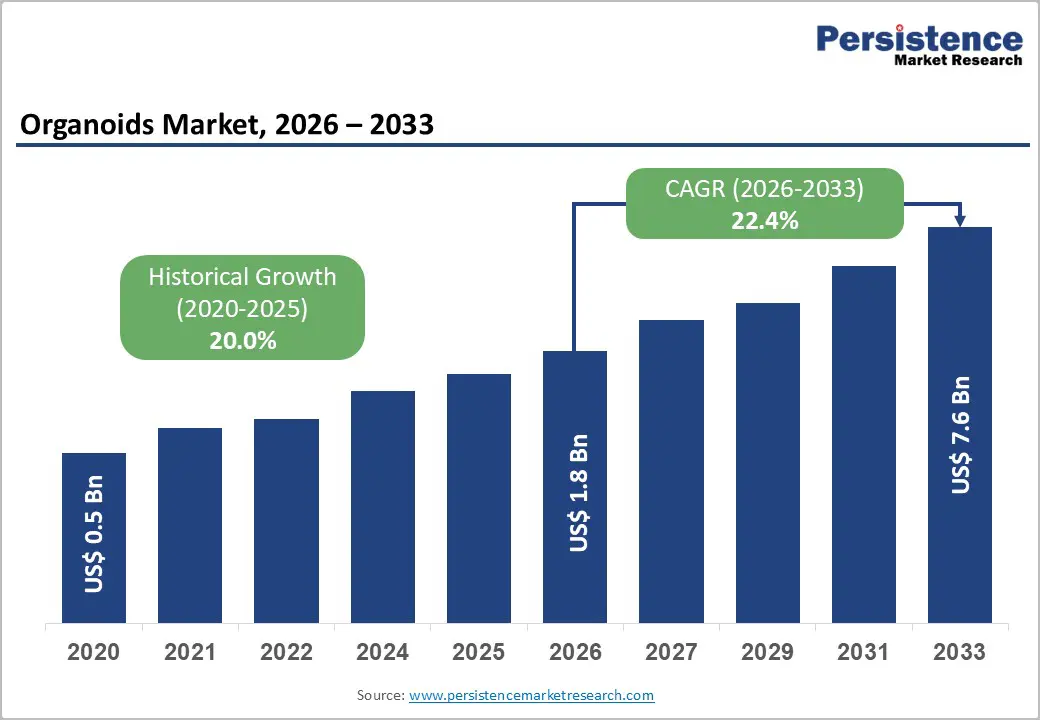

The global organoids market size is likely to value at US$ 1.8 billion in 2026 and reach US$ 7.6 billion by 2033, growing at a CAGR of 22.4% during the forecast period from 2026 to 2033. The global organoids market is growing steadily, fueled by rising research adoption, demand for disease modeling, and drug screening applications.

Increasing investments in biotech, advancements in 3D cell culture technologies, and expanding pharmaceutical R&D further drive growth. North America dominates, while Asia-Pacific shows rapid expansion due to growing life sciences research and biotech infrastructure.

Key Industry Highlights

- Dominant Segment: Intestinal Organoids account for 29.3% of the organoids market in 2025, driven by high demand for disease modeling, drug discovery, and toxicology studies. Increasing adoption in pharmaceutical R&D, academic research, and personalized medicine applications contributes to sustained segment dominance globally.

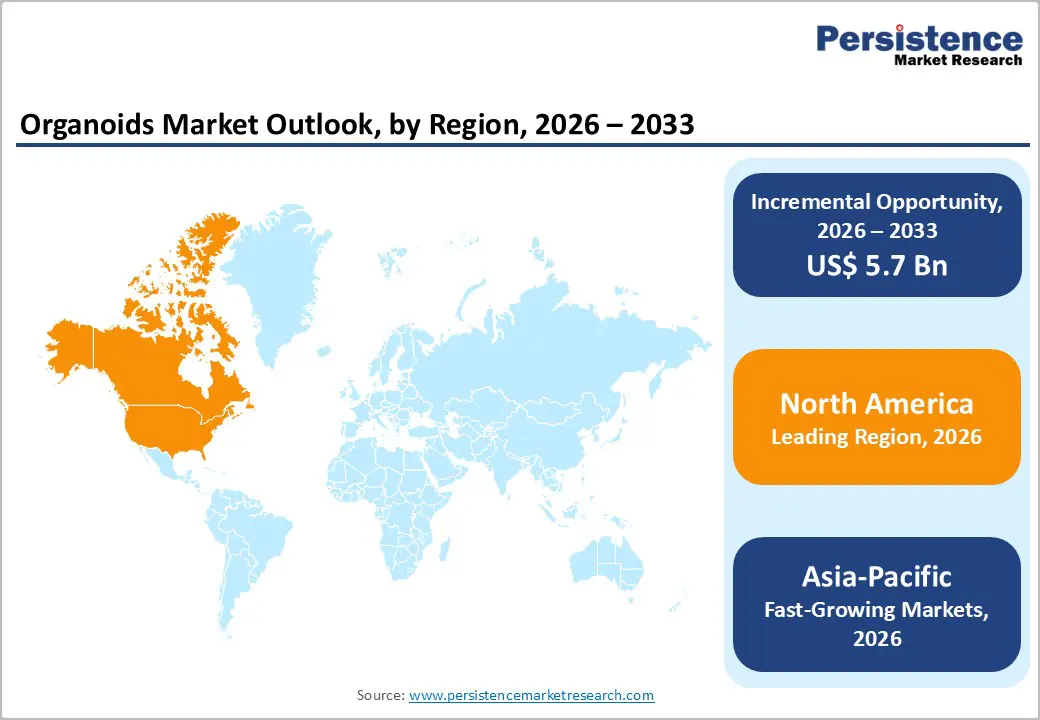

- Dominant Region: North America leads the organoids market in 2025 with 45.0% share, supported by strong research infrastructure, high biotech investment, and widespread adoption of organoid-based platforms. Meanwhile, the Asia-Pacific is the fastest-growing region, driven by rising life sciences investment, increasing pharma R&D, and the expansion of biotechnology labs.

- Growth Indicators: Growing demand for advanced 3D models in drug discovery, personalized medicine applications, disease modeling, toxicity testing, stem cell research, and regenerative medicine. Increased funding, technological innovation, and preference for alternatives to animal testing are key factors driving market growth.

- Key Opportunity: Opportunities include development of organ-specific and patient-derived organoid models, expansion through CRO partnerships and academic collaborations, rising adoption in emerging markets, innovation in culture media and supplements, and strategic collaborations with pharmaceutical and biotechnology companies for high-throughput screening and precision medicine applications.

| Key Insights | Details |

|---|---|

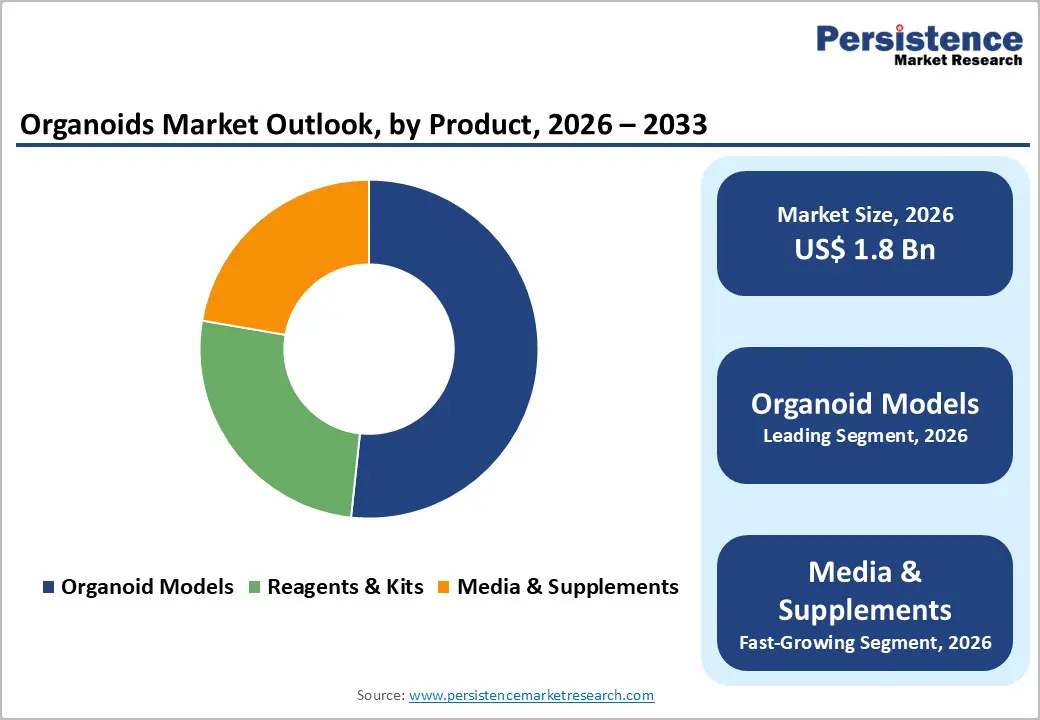

| Global Organoids Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 7.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 22.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 20.0% |

Market Dynamics

Driver: Rising adoption of organoids in drug discovery and toxicity testing

Organoids are three-dimensional, human-derived mini-organ models that more closely replicate human tissue architecture and function than traditional 2D cell cultures or many animal systems. Their use in drug discovery and toxicity testing has expanded rapidly: published research shows organoid platforms can predict drug responses with high accuracy, with some tumor organoids matching patient therapeutic responses with sensitivities and specificities above ~80-90% in cancer drug testing settings. These findings demonstrate that organoids can improve early decisions in drug development by identifying effective or toxic compounds more reliably than older models.

Government-backed initiatives further illustrate this adoption. In 2025, the U.S. National Institutes of Health (NIH) awarded $87 million to establish the Standardized Organoid Modeling (SOM) Center, explicitly to accelerate organoid use in preclinical research, including drug screening and safety testing, and to replace less predictive animal models with human-relevant systems. This federal investment underscores organoids’ increasing role in drug discovery pipelines and translational science.

Restraints: Limited standardization and reproducibility across laboratories

Despite their scientific promise, organoids face significant reproducibility challenges that restrain widespread adoption in industry and regulatory science. A major limitation is the lack of standardized protocols and quality measures: variations in source cells, culture conditions, extracellular matrices, and growth environments produce significant differences in organoid structure, gene expression, and drug responses even when generated from the same patient sample. This variability complicates cross-laboratory comparisons and undermines confidence in organoid data.

A key federal response highlights this problem: the NIH’s newly launched Standardized Organoid Modeling Center is designed specifically to address reproducibility by creating robust, standardized organoid protocols and models accessible to researchers nationwide. The center’s mission reflects a recognized barrier in current organoid research inconsistent outcomes hinder not only academic studies but also regulatory acceptance and industrial deployment of organoids as reliable preclinical tools.

Opportunity: Development of organ-specific and patient-derived organoids for precision medicine

One of the most compelling opportunities in the organoids market lies in patient-derived organoids (PDOs), organoids formed from an individual’s own cells that faithfully recapitulate that person’s tissue biology. These PDOs facilitate precision medicine by enabling clinicians and researchers to test multiple therapies in vitro and identify the most effective treatment for a specific patient before administering therapy in vivo. Clinical research shows that PDOs can model tumor sensitivity with high predictive power, demonstrating strong correlation between organoid drug response and patients’ actual clinical outcomes in cancer settings.

Beyond oncology, PDOs are being used to evaluate responses to a range of drugs and conditions, and clinical trial databases list dozens of organoid-related trials, predominantly initiated within the past five years, underscoring rapid momentum. This trend creates a substantial opportunity to integrate organoid platforms into personalized therapeutic strategies, reduce costly trial-and-error in treatment selection, and accelerate precision medicine adoption in mainstream clinical practice.

Category-wise Analysis

By Product Insights

Organoid Models occupies 51.7% share of the global market in 2025, because they best replicate human physiology in vitro, offering structural and functional features of real organs that traditional 2D cultures lack. Organoid models are three-dimensional systems derived from stem cells that self-organize into mini-organ structures, retaining key genetic and cellular characteristics of the source tissue. This makes them far more predictive for drug screening, disease modeling, and therapeutic evaluation than simple cell lines. Importantly, patent analyses show that over ~76% of organoid technology patents target organoid construction itself, highlighting that creation of reliable organoid models is the principal focus of innovation in this field rather than ancillary reagents or tools.

Because these models can be generated from human tissue samples, including biopsies, and used to study disease mechanisms and drug responses with high physiological relevance, researchers and biotech companies increasingly invest in organoid model platforms solidifying this product category as the dominant revenue contributor across applications.

By Organ Type Insights

Intestinal organoids are among the most widely used organoid types because they closely mimic the structural and cellular complexity of the gastrointestinal epithelium and can be derived from routine clinical tissue samples through minimally invasive procedures unlike some other organ systems. They contain all major intestinal cell types and replicate crypt-villus architecture, making them highly relevant for drug absorption, metabolism, toxicity testing, and disease modeling.

Their suitability for modeling gastrointestinal infections, host-pathogen interactions (e.g., SARS-CoV-2, norovirus), and conditions such as inflammatory bowel disease further expands their utility across infectious disease, pharmacology, and nutritional research. Because intestinal diseases (including colorectal cancer) are among the most prevalent health concerns globally with very high incidence and mortality there is strong scientific demand for accurate human intestine models. This broad applicability and accessibility underpin intestinal organoids’ leading share in organoid market research and application.

Regional Insights

North America Organoids Market Trends

North America dominates the global organoids market primarily due to its substantial investment in life sciences, leading research infrastructure, and concentration of biotech and pharmaceutical firms. In 2025, North America accounted for 45.0% of global organoid market activity, supported by over 1,200 active organoid research projects spanning disease modeling, drug screening, and regenerative applications far more than any other region. The United States, in particular, benefits from consistent federal funding through agencies like the National Institutes of Health (NIH) and its targeted programs in precision and regenerative medicine, which propel adoption of organoid technologies. This concentration of funding, combined with advanced laboratory infrastructure and regulatory support for innovative preclinical models, solidifies North America’s leadership position in both research and commercialization of organoid platforms.

Europe Organoids Market Trends

Europe is a pivotal region for the organoids market because of its strong academic research base, collaborative funding initiatives, and supportive policy environment that facilitate adoption of organoid technologies. In 2025, Europe contributed around 29.3% of global organoid market activity, representing the second largest regional share globally. Major research hubs in Germany, the United Kingdom, and France lead numerous organoid projects focused on personalized medicine and translational research, often under public-private consortia and EU-backed programs. Additionally, European governments provide significant funding for stem cell and organoid research such as Horizon Europe framework investments, which strengthen collaborative networks between industry and academia. These factors make Europe an important driver of innovation and application for organoid models in drug discovery and regenerative medicine.

Asia Pacific Organoids Market Trends

Asia Pacific is gaining rapid momentum in the organoids market due to expanding biotechnology infrastructure, growing governmental support, and increasing healthcare R&D expenditure. Though it currently represents a smaller share globally, the region is forecasted to exhibit higher growth rates than North America and Europe. Countries such as China, Japan, South Korea, and India have collectively launched hundreds of organoid research initiatives, with life sciences spending exceeding USD 15 billion in 2024, a significant portion directed toward advanced biomedical research and drug discovery. In addition, governments in the region are actively promoting translational research and academic-industry collaborations, accelerating the adoption of organoid technologies. These factors combined position Asia Pacific as the fastest-growing region in the global organoids market.

Competitive Landscape

The organoids market is highly competitive, led by major life sciences and biotechnology companies such as Thermo Fisher Scientific, Merck KGaA, Corning Incorporated, STEMCELL Technologies, and Emulate Inc. Competition centers on advanced 3D culture technologies, proprietary media formulations, organ-specific model development, strategic pharma collaborations, and continuous innovation in precision medicine and drug discovery applications.

Key Industry Developments:

- In October 2025, Merck announced that it had partnered with Promega Corporation to accelerate the development and adoption of advanced 3-D cell-based drug discovery technologies. The collaboration aimed to integrate Merck’s expertise in cell culture reagents and biomaterials with Promega’s assay development and detection platforms to enhance the efficiency and reliability of 3-D cell and organoid research.

- In January 2025, Merck announced that it had acquired HUB Organoids Holding B.V., a Netherlands-based pioneer in organoid technology, to strengthen its next-generation biology portfolio. HUB Organoids was widely recognized for its advanced adult stem cell-derived organoid platforms, which are used in disease modeling, drug screening, and personalized medicine research.

Companies Covered in Organoids Market

- STEMCELL Technologies Inc.

- Synthecon Inc.

- Promega Corporation

- Merck KGaA

- Nortis Bio

- PromoCell GmbH

- AxoSim Inc.

- Crown Biosciences

- Corning Incorporated

- Thermo Fisher Scientific Inc.

- Reprocell Inc.

- DefiniGEN Limited

- Lena Biosciences Inc.

- Nanofiber Solutions

- Alveolix AG

- UPM Biomedicals

- Nuvisan GmbH

- Charles River Laboratories

- CELLphenomics GmbH

- 3D Biotek LLC

- Others

Frequently Asked Questions

The global organoids market is projected to be valued at US$ 1.8 Bn in 2026.

Rising demand for advanced drug discovery, personalized medicine, and human-relevant disease modeling.

The global organoids market is poised to witness a CAGR of 22.4% between 2026 and 2033.

Expansion in precision medicine, organ-specific models, CRO partnerships, and emerging biotech markets.

STEMCELL Technologies Inc., Synthecon Inc., Promega Corporation, Merck KGaA, Nortis Bio, PromoCell GmbH.