- Food Ingredients & Additives

- Organic Cocoa Market

Organic Cocoa Market Size, Share, and Growth Forecast 2026 - 2033

Organic Cocoa Market by Product Type (Organic Cocoa Powder, Organic Cocoa Butter, Organic Cocoa Beans, Organic Cocoa Liquor, Others), by Application (Confectionery, Bakery Products, Food & Beverages, Cosmetics & Personal Care, Others), by Distribution Channel (Supermarkets/Hypermarkets, Specialty Organic Stores, Online Retail/E-commerce, Convenience Stores, Others), by Regional Analysis, 2026 - 2033

Organic Cocoa Market Size and Trend Analysis

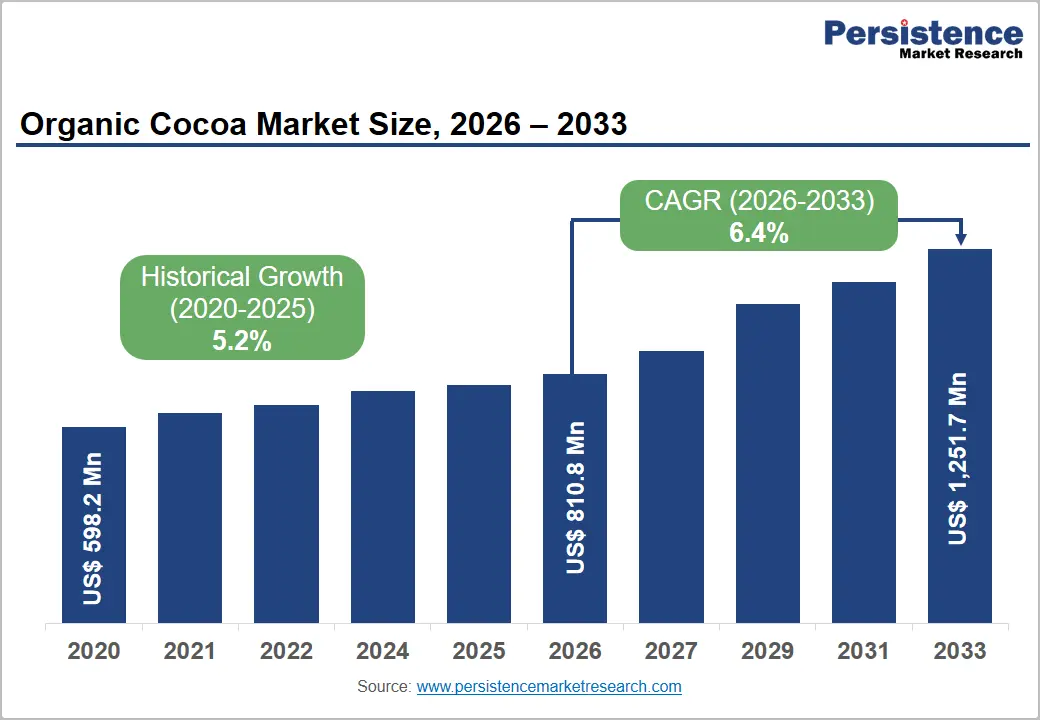

The global organic cocoa market size is expected to be valued at US$ 810.8 million in 2026 and projected to reach US$ 1,251.7 million, growing at a CAGR of 6.4% between 2026 and 2033. This sustained growth is propelled by a decisive global consumer shift toward clean-label, sustainably sourced food ingredients, with organic cocoa at the forefront of the premium chocolate and natural food ingredients movement.

The Organic Trade Association (OTA) reported that U.S. organic food sales surpassed USD 67.6 billion in 2023, reflecting mainstream normalization of organic purchasing behavior. Simultaneously, expanding applications of organic cocoa in cosmetics and personal care, where consumers demand chemical-free, naturally derived ingredients, and the rapid premiumization of global confectionery and artisan chocolate categories are generating strong, diversified demand across food, beverage, and beauty industries throughout the forecast period.

Key Market Highlights

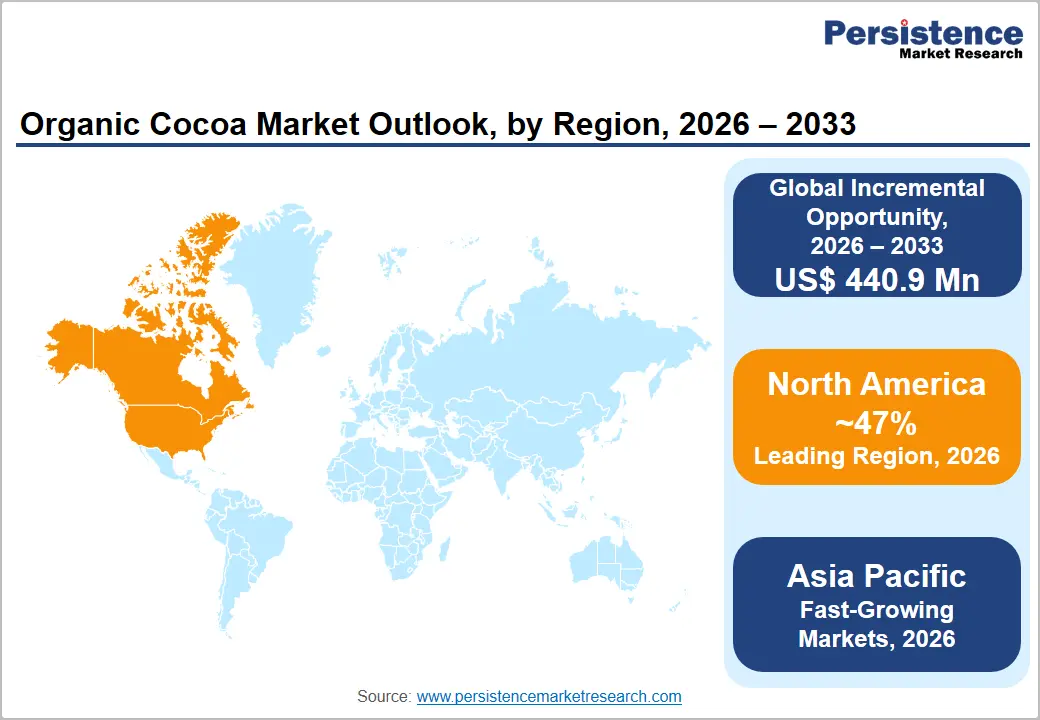

- Leading Region: North America leads the global Organic Cocoa market with approximately 47% revenue share in 2026, anchored by US$ 67.6 billion in total U.S. organic food sales (OTA, 2023), a thriving craft chocolate ecosystem of 200+ bean-to-bar makers, and strong USDA NOP certification-driven consumer trust.

- Fast-growing Market: Asia Pacific is the fast-growing regional market through 2033, driven by rising health consciousness in China, Japan, and India, expanding premium chocolate gifting culture, and ASEAN-based organic cocoa cultivation investment in Indonesia and Vietnam targeting premium export market pricing.

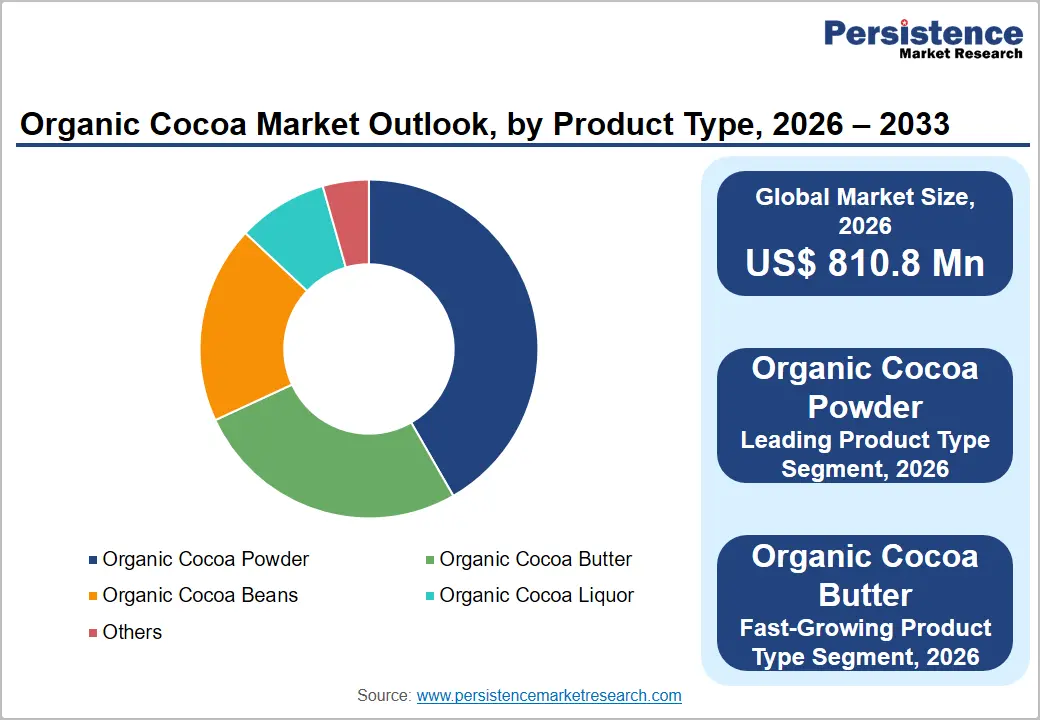

- Leading Product: Organic cocoa powder dominates the product type category with approximately 42% share in 2026, underpinned by its broad application across confectionery, bakery, functional food, and beverage formulations and growing clean-label demand certified under USDA NOP and EU Organic standards.

- Organic Cocoa Butter represents the fastest-growing product segment through 2032, propelled by booming natural beauty sector adoption by brands including L'Oréal and Burt's Bees under Cosmos Organic certification and craft chocolate premiumization commanding 30-50% price premiums over commodity cocoa butter.

- Opportunity: The online retail/e-commerce channel represents the highest-growth distribution opportunity, with U.S. online food and beverage sales growing at CAGR exceeding 15% since 2020, enabling organic cocoa brands to build direct-to-consumer subscription models with superior margins versus traditional specialty retail channels.

Market Dynamics

Drivers - Surging Consumer Demand for Clean-Label and Sustainably Sourced Cocoa Products

The global consumer shift toward transparency in food sourcing and clean-label ingredient standards is a major driver. According to the International Cocoa Organization (ICCO), global cocoa demand has been growing steadily, with premium and specialty organic segments outperforming conventional cocoa categories by a significant margin. A 2023 survey by the Hartman Group found that over 60% of U.S. consumers actively check food labels for organic certification before purchasing chocolate and cocoa-based products.

The USDA National Organic Program (NOP) certification and the EU's EU Organic Regulation (2018/848) provide internationally recognized quality assurance frameworks that drive consumer trust and brand premium positioning, reinforcing consistent demand growth for certified organic cocoa ingredients across food manufacturing and retail channels globally.

Expanding Organic Cocoa Applications in Cosmetics and Functional Food Segments

The diversification of organic cocoa usage beyond traditional confectionery into high-growth cosmetics, personal care, and functional food categories is significantly broadening the addressable market. Organic cocoa butter valued for its emollient, antioxidant, and skin-nourishing properties is increasingly specified as a preferred ingredient in premium skincare formulations by brands committed to natural and organic beauty standards.

The Natural & Organic Products Europe trade association reports that the European natural and organic beauty market exceeded EUR 4.5 billion in annual sales, with cocoa butter featuring prominently in certified organic moisturizers, lip balms, and hair care products. Simultaneously, the functional food trend driven by the growing body of clinical evidence supporting cocoa flavanols' cardiovascular and cognitive health benefits documented in journals including the American Journal of Clinical Nutrition is expanding organic cocoa powder adoption in health-oriented food and beverage formulations.

Restraints - Supply Chain Vulnerabilities and Climate-Driven Production Volatility in Cocoa Growing Regions

Organic cocoa supply is disproportionately concentrated in a small number of tropical producing countries primarily Côte d'Ivoire, Ghana, Ecuador, Peru, and the Dominican Republic that are highly vulnerable to climate variability, crop disease, and agronomic challenges. The ICCO documented that cocoa bean production declined significantly in West Africa during the 2023-2024 crop year due to adverse weather patterns including El Niño-driven dry spells and increased Black Pod Disease incidence.

For certified organic cocoa specifically, yield constraints are more acute as growers cannot use synthetic pesticides or fertilizers, creating supply tightness that drives price premiums that can, at high levels, dampen demand from cost-sensitive buyers in price-competitive confectionery manufacturing segments.

High Certification Costs and Lengthy Organic Transition Periods Limiting Farmer Adoption

The barriers to organic certification for smallholder cocoa farmers who constitute the backbone of global cocoa supply are substantial and create structural supply constraints in the organic cocoa market. Achieving USDA NOP or EU Organic certification requires a 3-year chemical-free transition period during which farmers bear organic production costs without receiving organic price premiums.

Certification fees, documentation requirements, and third-party audits impose additional financial burdens that are prohibitive for subsistence-level smallholders in producing countries. The Fairtrade International network estimates that fewer than 5% of global cocoa farmers are currently certified organic, highlighting the significant structural gap between existing certified supply and growing global demand.

Opportunities - Organic Cocoa Butter: Fast-Growing Product Segment Driven by Natural Beauty and Food Premiumization

Organic Cocoa Butter represents the fastest-growing product segment within the organic cocoa market, positioned at the intersection of two powerful macro trends: the explosive growth of natural and organic beauty products and the premiumization of artisan and craft chocolate manufacturing. Global demand for organic cocoa butter in cosmetics and personal care is accelerating as major beauty brands including L'Oréal, The Body Shop, and Burt's Bees transition formulations toward certified organic ingredients to meet consumer expectations and comply with evolving regulatory standards in the EU and U.K. under Cosmos Organic and NATRUE certification frameworks.

In the food sector, craft chocolate makers' emphasis on single-origin, minimally processed organic cocoa butter for high-cacao content chocolate is creating a premium price tier that commands 30-50% premiums over commodity cocoa butter benchmarks, generating attractive margins for certified organic cocoa processors.

Online Retail and E-commerce Channel: Accelerating Direct-to-Consumer Organic Cocoa Distribution

The online retail/e-commerce distribution channel represents the fastest-growing route to market for organic cocoa products, disrupting traditional specialty store-dependent distribution models and enabling organic cocoa brands to reach health-conscious consumers directly at national and international scale. The U.S. Census Bureau reports that U.S. e-commerce food and beverage sales have grown at a CAGR exceeding 15% since 2020, with organic and specialty food categories demonstrating above-average online channel penetration.

Global platforms including Amazon, Thrive Market, and iHerb have established dedicated organic food sections with strong organic cocoa powder and chocolate product assortments, while direct-to-consumer craft chocolate brands are building subscription and gifting models that generate superior customer lifetime value versus physical retail. This channel shift is particularly beneficial for smaller certified organic cocoa brands that lack resources for traditional retail shelf-space competition.

Category-wise Analysis

Product Type Insights

Organic cocoa powder dominates the organic cocoa market by product type, commanding approximately 42% of global share in 2026. This leadership reflects the ingredient's extraordinarily broad application base spanning hot chocolate beverages, baking mixes, confectionery coatings, protein supplements and functional food formulations that generate consistent high-volume demand across both industrial food manufacturing and retail consumer channels. The rise of health-focused food culture has particularly amplified organic cocoa powder demand, as consumers and food formulators leverage the ingredient's natural flavanol content, certified organic credentials, and clean-label appeal in everything from artisan brownies to organic protein powders.

The Rainforest Alliance and USDA Organic dual-certified organic cocoa powders offered by suppliers including Valrhona, Guittard, and Barry Callebaut's organic lines command meaningful price premiums that drive category revenue leadership disproportionate to pure volume.

Application Insights

The confectionery segment leads the organic cocoa market by application, accounting for approximately 48% of global revenues in 2026. Organic cocoa's central role in premium and artisan chocolate manufacturing where certified organic sourcing is a core brand value proposition for a growing segment of craft chocolate makers and mainstream premium confectionery brands anchors this segment's leadership position.

Switzerland, Belgium, and U.S.-based craft chocolate producers have been significant catalysts for organic cocoa premiumization, with organizations such as the Fine Chocolate Industry Association (FCIA) advocating for transparent, sustainably sourced cacao as a baseline standard. The Cocoa Barometer 2022, published by a coalition of NGOs monitoring the cocoa sector, confirms that premium and sustainable cocoa segments, including organic, are the primary growth segments within the broader confectionery-grade cocoa market.

Distribution Channel Insights

Supermarkets and Hypermarkets represent the leading distribution channel for organic cocoa products, holding approximately 38% of global distribution revenues in 2026. The mainstreaming of organic food retailing within conventional grocery and hypermarket formats led by major retailers including Whole Foods Market (Amazon), Costco, Carrefour, Tesco, and Rewe has dramatically expanded consumer accessibility to certified organic cocoa products beyond specialty health food stores.

Dedicated organic sections within mainstream supermarket formats normalize organic cocoa purchasing as part of routine grocery shopping behavior, reaching a far broader consumer demographic than specialty organic retailers alone. Nielsen IQ retail panel data for 2023 confirmed that organic food categories achieved their highest-ever penetration in conventional grocery channels, with organic chocolate and cocoa products among the top-performing organic segments in both U.S. and European supermarket formats.

Regional Insights

North America Organic Cocoa Market Trends and Insights

North America accounted for nearly 45.8% of the global organic cocoa market revenue in 2026, supported by strong consumer preference for premium organic confectionery, established organic certification systems, and growing ethical sourcing awareness. The region benefits from high penetration of clean-label chocolate products across retail and foodservice channels. Rising demand for sustainably sourced cocoa ingredients and expanding organic snack categories continue to support market expansion. The regional market is projected to register a CAGR of 8.9% through 2032, driven by premiumization trends and increasing adoption of organic-certified bakery and beverage ingredients.

U.S. Organic Cocoa Market Share and Trends Analysis

The U.S. dominates the North American Organic Cocoa market with over 78.4% regional share in 2026. Growth is fueled by rising consumption of organic chocolate, functional beverages, and plant-based desserts. Increasing consumer willingness to pay premium prices for USDA-certified organic and fair-trade cocoa products has accelerated adoption among mainstream retailers and artisanal chocolate brands. Expansion of bean-to-bar chocolate manufacturing and strong e-commerce penetration are further strengthening domestic demand for organic cocoa ingredients.

Canada Organic Cocoa Market Trends and Insights

Canada represents approximately 14.7% of the North American Organic Cocoa market and is anticipated to grow at a CAGR of 8.1% in the coming years. Demand is being supported by increasing health-conscious consumer spending and expanding organic product shelf space across premium supermarkets. Canadian consumers are showing greater interest in clean-label confectionery and sustainably sourced cocoa products. Government-backed organic labeling standards and rising imports of certified organic cocoa ingredients are contributing to continued market expansion across the country.

Europe Organic Cocoa Market Trends and Insights

Europe captured around 31.6% of the global organic cocoa market in 2026, supported by strong organic food consumption patterns, strict sustainability regulations, and high per-capita chocolate intake. Demand for ethically sourced cocoa ingredients continues to rise across premium confectionery, bakery, and beverage applications. The region benefits from advanced retail distribution networks and consumer preference for organic-certified food products. Increasing focus on carbon-neutral supply chains and traceable cocoa sourcing is expected to support a CAGR of 7.8% through 2032 across the European organic cocoa industry.

Germany Organic Cocoa Market Trends and Insights

Germany is likely to account for 24.9% of the European organic cocoa market revenue in 2026, making it the leading country within the region. The country’s strong organic retail infrastructure and rising demand for premium dark chocolate products are driving market growth. German consumers increasingly prefer sustainably sourced cocoa ingredients with EU Organic certification. The expansion of organic private-label confectionery ranges and growing vegan chocolate consumption are further contributing to rising organic cocoa demand.

UK Organic Cocoa Market Trends and Insights

The UK is likely to register approximately 18.2% of the regional market in 2026 and is projected to expand at a CAGR of 7.5% in the forecast period. Rising consumer focus on clean-label snacks, organic bakery products, and premium gifting chocolates is supporting market growth. The country’s established specialty retail network and increasing demand for ethically traded cocoa products continue to strengthen sales of certified organic cocoa ingredients across confectionery and beverage applications.

Asia Pacific Organic Cocoa Market Trends and Insights

Asia Pacific is projected to witness the fastest growth in the organic cocoa market, registering a CAGR of 10.6%. The region accounted for nearly 16.9% of global revenue in 2025, driven by increasing disposable incomes, rapid urbanization, and rising awareness regarding organic food consumption. Expanding premium chocolate culture and growing westernization of dietary habits are accelerating demand for organic cocoa across confectionery and beverages. E-commerce expansion, imported organic food availability, and increasing investment in sustainable cocoa sourcing are expected to further strengthen regional market growth.

China Organic Cocoa Market Trends and Insights

China represented around 29.3% of the Asia-Pacific Organic Cocoa market in 2025 and continues to emerge as a high-growth consumer market for premium organic chocolate products. Rising middle-class spending and growing preference for imported clean-label confectionery are boosting organic cocoa demand. Online retail platforms and premium gifting trends are encouraging greater penetration of organic chocolate brands across urban consumer segments.

India Organic Cocoa Market Trends and Insights

India is poised for nearly 18.6% of the regional market in 2026 and is forecast to reach a CAGR of 11.8% in the years ahead. Rising demand for premium chocolates, organic beverages, and artisanal cocoa products is driving market expansion. Domestic chocolate manufacturers are increasingly incorporating certified organic cocoa ingredients to cater to health-conscious consumers. Growth in organized retail channels and government support for organic agricultural practices are further contributing to the country’s market development.

Competitive Landscape

The global organic cocoa market is moderately fragmented, with a blend of large multinational ingredient suppliers and specialized organic-focused processors competing across different product tiers. Barry Callebaut AG, Olam International, and Cargill, Inc. dominate the industrial supply segment through scale, global supply chain infrastructure, and certified organic procurement programs. Key differentiators include Rainforest Alliance, USDA NOP, and Fairtrade multi-certification capabilities, single-origin traceability platforms, and direct farmer partnership programs.

Emerging competitive strategies include blockchain-enabled supply chain transparency, regenerative organic agriculture investment programs, and direct-to-consumer brand development. Mid-size specialty players including Valrhona, Guittard, and Republica del Cacao compete through artisan product quality, origin differentiation, and premium food service and craft chocolate market positioning.

Key Developments:

- In March 2024, Swiss-based organic cocoa processor YACAO announced that it became the first supplier in Latin America to achieve Regenerative Organic Certified (ROC) status, reinforcing its commitment to sustainable and regenerative cocoa production practices.

- In December 2022, Indian craft chocolate brand Kocoatrait launched its sustainable Bean-to-Bar 64% Plum Cake Dark Chocolate developed using organic cocoa beans sourced from India. Created by certified chocolate taster Poonam Chordia, the vegan and gluten-free dark chocolate bar was infused with warm spices, dried fruits, and roasted almonds, reflecting the growing demand for premium organic and artisanal cocoa-based confectionery products.

Companies Covered in Organic Cocoa Market

- MIMEDX Group, Inc.

- BioTissue, Inc.

- Organogenesis Holdings Inc.

- Integra LifeSciences Corporation

- Smith & Nephew plc

- Celularity Inc.

- Amnio Technology, LLC

- NuVision Biotherapies Ltd

- Tides Medical, LLC

- Corza Health, Inc.

- Merakris Therapeutics, Inc.

- Skye Biologics, Inc.

- StimLabs, LLC

- Sanara MedTech Inc.

- Applied Biologics, LLC

- Others

Frequently Asked Questions

The global organic cocoa market is estimated to reach US$ 810.8 million in 2026, growing from US$ 598.2 million in 2020 at a historical CAGR of 5.2%. The market is projected to expand to US$ 1,251.7 million by 2033 at a forecast CAGR of 6.4%, driven by clean-label consumer trends, expanding organic confectionery and cosmetics applications, and growing certified organic supply chain investment from major cocoa ingredient processors.

Rising consumer preference for organic, clean-label, and ethically sourced food products, particularly premium chocolates, bakery items, and functional beverages, is significantly driving demand for organic cocoa globally.

North America leads with approximately 47% of global revenues in 2025, driven by the United States' status as the world's largest organic food consumer market. The OTA reported USD 67.6 billion in U.S. organic food sales, a 200+ bean-to-bar craft chocolate ecosystem tracked by the Fine Chocolate Industry Association, and the robust USDA NOP regulatory framework all underpin North America's dominant position in both organic cocoa ingredient procurement and finished premium chocolate product consumption.

Expanding adoption of organic cocoa in emerging Asia-Pacific markets and increasing use in premium cosmetics, plant-based foods, and sustainable confectionery products present major growth opportunities for the market.

The leading companies in the global Organic Cocoa market include Barry Callebaut AG, Olam International Limited, Cargill, Incorporated, Valrhona S.A.S., Guittard Chocolate Company, Republica del Cacao, Organic Valley, Divine Chocolate Limited, Theo Chocolate, Inc., Pacari Chocolate, Equal Exchange, Inc., Dr. Bronner's, and Cao Chocolates, among other specialty organic cocoa processors and craft chocolate manufacturers operating across global supply and distribution networks.