- Medical Devices

- Tinnitus Masker Market

Tinnitus Masker Market Size, Share and Growth Forecast, 2026 - 2033

Tinnitus Masker Market by Application (Conventional Hearing Aids, Others), Distribution Channel (Retail pharmacy, E-commerce, Hospital), Product Type (In Ear Tinnitus Maskers, Behind Ear Tinnitus Masker), and Regional Analysis for 2026 - 2033

Tinnitus Masker Market Size and Trends Analysis

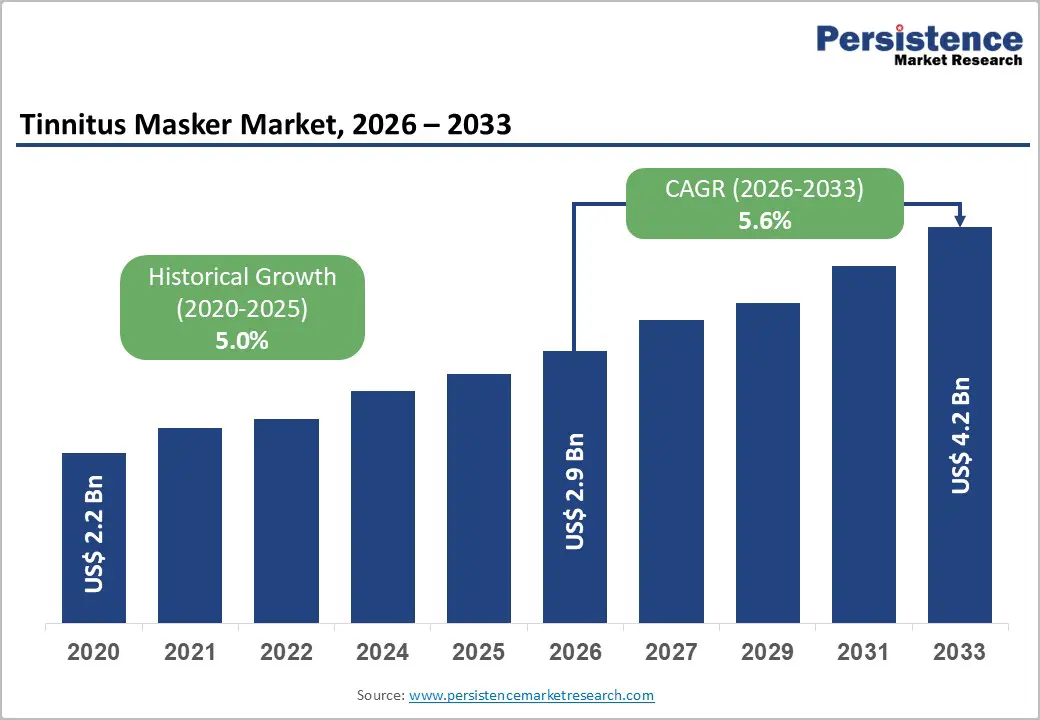

The global tinnitus masker market size is likely to be valued at US$2.9 billion in 2026 and is projected to reach US$4.2 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026 - 2033, driven by the increasing prevalence of tinnitus and hearing loss, particularly among aging populations, along with the rising adoption of hearing healthcare devices and advancements in digital hearing aid technology.

Greater awareness of tinnitus management, expanding availability of personalized sound therapy solutions, and improved access to audiology services are supporting market growth. Additionally, the integration of AI-enabled hearing devices, smartphone connectivity, and favorable reimbursement policies in developed markets is driving sustained demand for tinnitus masking devices.

Key Industry Highlights:

- Dominant Application Segment: Conventional hearing aids are set to lead with around a 48% share in 2026, while tinnitus instruments are expected to grow the fastest, driven by personalized sound therapy and connected hearing technologies.

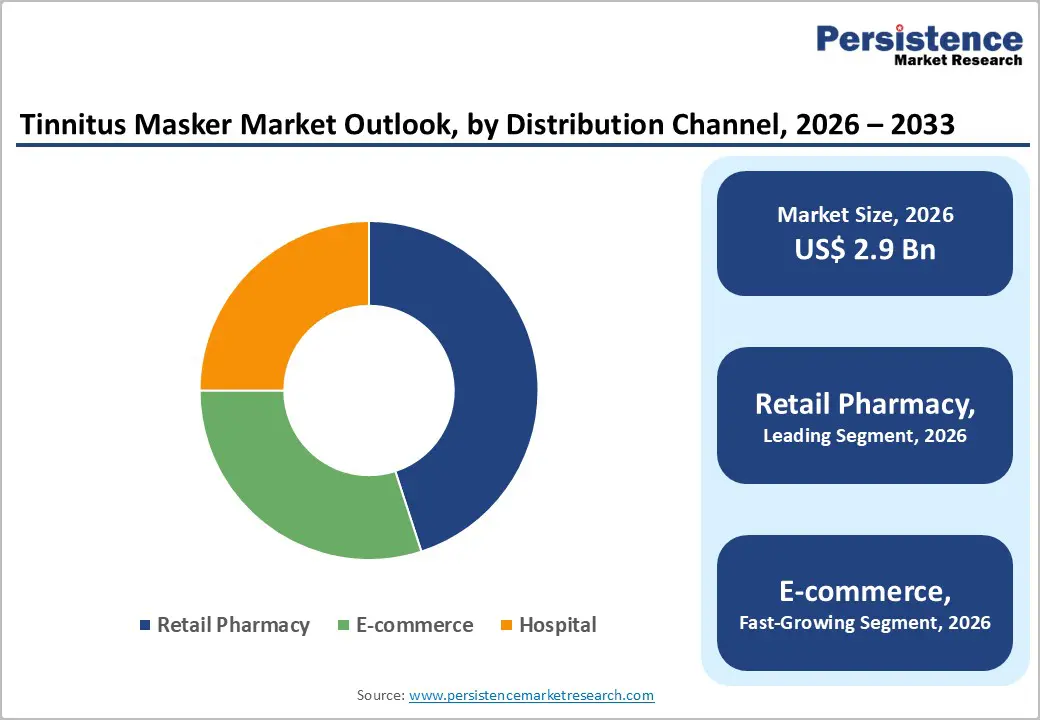

- Distribution Channel Trends: Retail pharmacies are likely to dominate in 2026, whereas e-commerce is projected to be the fastest-growing channel through 2033 due to digital adoption and tele-audiology expansion.

- Product Type Leadership: Behind-ear tinnitus maskers are expected to hold nearly 60% share in 2026, while in-ear devices are anticipated to grow fastest due to demand for discreet, smart-connected solutions.

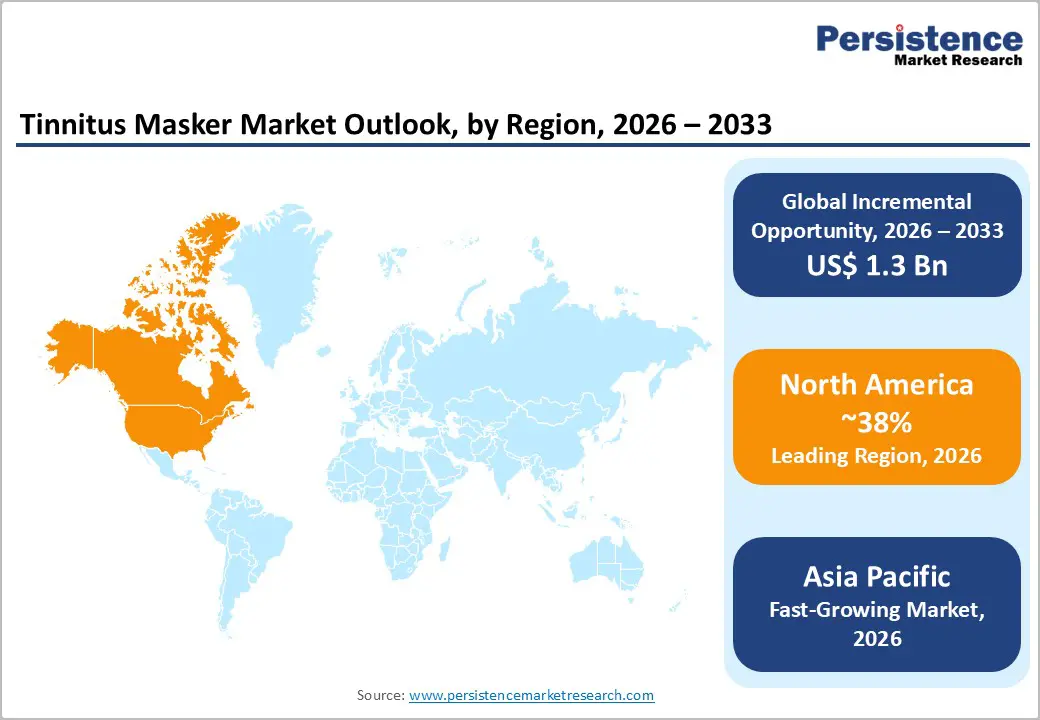

- Regional Leadership: North America is projected to lead with about a 38% share in 2026, while Asia Pacific is expected to register the fastest growth through 2033 on the back of rising prevalence and healthcare access.

- Competitive Environment: Market players are focusing on AI-enabled hearing solutions, digital therapeutics, and geographic expansion to strengthen their presence across developed and emerging markets.

DRO Analysis

Driver - Rising Global Burden of Hearing Loss and Tinnitus Driving Demand for Advanced Tinnitus Management Solutions

The increasing prevalence of tinnitus remains the primary growth driver for the Tinnitus Masker Market. According to the World Health Organization (WHO), more than 1.5 billion people globally experience some degree of hearing loss, while approximately 430 million individuals require rehabilitation services for disabling hearing impairment. The U.S. National Institute on Deafness and Other Communication Disorders (NIDCD) estimates that nearly 10-15% of adults experience tinnitus symptoms, with around 20 million Americans affected by chronic tinnitus.

Aging demographics further amplify demand, as tinnitus prevalence increases significantly among individuals aged above 60 years. Simultaneously, prolonged exposure to occupational and recreational noise is contributing to rising cases among younger populations. These trends are encouraging greater adoption of digital hearing aids, sound therapy devices, and tinnitus masking technologies, prompting manufacturers to invest heavily in product innovation, wireless connectivity, and personalized treatment capabilities.

Restraint - High Treatment Costs and Limited Reimbursement Coverage Restrict Market Expansion

Despite growing demand, the market faces challenges associated with device affordability and reimbursement limitations. Advanced tinnitus maskers integrated into premium hearing aids often require significant out-of-pocket expenditure, particularly in developing economies where hearing healthcare reimbursement remains limited.

According to the WHO World Report on Hearing, nearly 80% of individuals with hearing loss live in low- and middle-income countries, yet access to hearing care services remains substantially underserved. Furthermore, hearing aid adoption rates remain below 30% in many regions due to affordability concerns and social stigma. Clinical variability in tinnitus symptoms also complicates treatment outcomes, resulting in inconsistent patient satisfaction and longer evaluation periods before device adoption. These barriers can delay purchasing decisions and limit penetration of sophisticated tinnitus management devices, particularly in price-sensitive healthcare markets.

Opportunity - Digital Therapeutics and Smart Hearing Technologies Create Significant Growth Potential

The tinnitus masker market is expanding due to rising global hearing loss, with the WHO projecting 2.5 billion people affected by 2050, including nearly 700 million requiring rehabilitation. This is driving adoption of AI-enabled hearing devices, digital therapeutics, and connected tinnitus maskers, supported by regulatory developments such as the U.S. FDA approval of OTC hearing aids (2022), which has improved access to smart hearing solutions with app-based and remote features.

Tele-audiology is also gaining momentum, with the American Academy of Audiology (AAA) reporting sustained growth in remote hearing care adoption post-pandemic. This is enabling broader use of cloud-based monitoring and personalized sound therapy platforms, reducing reliance on in-clinic consultations. In addition, WHO data indicates that over 1 billion young people globally are at risk of noise-induced hearing loss, strengthening long-term demand for preventive and therapeutic hearing solutions, particularly in emerging markets such as India, China, and Brazil.

Category-wise Analysis

Application Insights

Conventional hearing aids are estimated to lead the tinnitus masker market with a 48% share in 2026, primarily due to the strong clinical overlap where nearly 70-80% of tinnitus cases are associated with hearing loss, making amplification-based therapy a widely adopted first-line intervention. The segment’s growth is further supported by regulatory and access expansion, including the U.S. FDA OTC hearing aid framework (2022), which is estimated to have significantly widened consumer entry points, while aging demographics in regions such as Japan and Western Europe continue to sustain high baseline demand for hearing rehabilitation solutions.

Tinnitus instruments are estimated to be the fastest-growing application segment through 2033, driven by increasing clinical preference for personalized sound therapy and neuromodulation-based treatment approaches in chronic tinnitus cases. Devices such as bimodal stimulation systems, including platforms such as Lenire (Neuromod Devices), evaluated in clinical studies showing measurable symptom improvement in a significant proportion of patients, are estimated to be accelerating physician adoption, while rising integration of app-based therapy and tele-audiology support is expected to further enhance long-term growth momentum.

Distribution Channel Insights

Retail pharmacies are estimated to lead the distribution channel with approximately a 45% share in 2026, supported by their role as the primary access point for over-the-counter hearing solutions and early tinnitus-related consultations. The segment is estimated to have gained additional traction following the FDA OTC hearing aid approval (2022), which enabled direct retail availability through large pharmacy networks such as CVS and Walgreens, while similar pharmacy-led distribution structures in Europe are expected to continue supporting high-volume adoption of basic tinnitus masking devices.

E-commerce is estimated to be the fastest-growing distribution channel through 2033, driven by increasing digital healthcare adoption and the expansion of direct-to-consumer hearing device sales enabled by regulatory shifts such as the FDA OTC rule (2022). Online platforms, including major marketplaces and specialized audiology portals, are estimated to be gaining share due to rising demand for price transparency, home delivery, and remote fitting services, while growth in emerging markets such as India is further supported by increasing tele-audiology penetration and smartphone-based healthcare access.

Product Type Insights

Behind-ear tinnitus maskers are estimated to dominate the market with nearly 60% revenue share in 2026, primarily due to their superior amplification capacity, longer battery life, and stronger suitability for moderate-to-severe hearing loss cases. The segment is estimated to benefit from widespread clinical preference in aging populations, particularly in countries such as Japan and Germany, where hearing impairment prevalence is high, while continuous product upgrades by leading manufacturers such as Sonova and GN Store Nord are expected to further strengthen adoption through enhanced connectivity and adaptive sound processing features.

In-ear tinnitus maskers are estimated to be the fastest-growing product category through 2033, driven by rising consumer preference for discreet, lightweight, and cosmetically appealing hearing solutions. Growth is further supported by increasing adoption of AI-enabled miniaturized devices from companies such as Starkey and Widex, which offer real-time sound adjustment and smartphone integration, while demand is estimated to be particularly strong among working professionals and younger users in urban markets where invisible and wearable health technologies are gaining rapid acceptance.

Regional Analysis

North America Tinnitus Masker Market Trends

North America is estimated to hold around a 38% share of the global tinnitus masker market in 2026, driven by a high clinical detection rate of tinnitus cases and early adoption of digital-first hearing care ecosystems. The region shows stronger penetration of AI-enabled hearing aids and OTC hearing solutions compared to other geographies, supported by established insurance-linked audiology pathways and high consumer awareness. Growth is also influenced by rising workplace noise exposure in manufacturing and service sectors, alongside increasing integration of telehealth in ENT care delivery.

U.S. Tinnitus Masker Market Trends

The U.S. is estimated to contribute 87% of the regional market in 2026, supported by a tinnitus-affected population of nearly 25-30 million adults and rapid commercialization of hearing technologies post FDA OTC hearing aid approval (2022). A key trend is the shift toward self-fitting hearing devices and app-based sound therapy platforms, which have expanded entry points beyond clinical settings. Pharmacy chains and digital retail platforms are increasingly acting as primary distribution hubs, accelerating adoption in early-stage hearing loss and tinnitus management.

Canada Tinnitus Masker Market Trends

Canada is estimated to account for 13% of the regional market in 2026, with growth shaped less by population size and more by structured public healthcare coverage and expanding remote care delivery. Adoption of tele-audiology is notably higher in rural provinces, where specialist density is low, creating reliance on hybrid digital-clinic models. Provincial hearing support programs and increasing use of remote device tuning services are gradually improving treatment adherence for chronic tinnitus patients.

Europe Tinnitus Masker Market Trends

Europe is estimated to represent around 30% of the global market in 2026, supported by standardized hearing care pathways, strong audiology regulation, and high penetration of prescription hearing devices in diagnosed patients. Unlike North America, growth here is more policy-driven, with reimbursement structures and clinical validation requirements shaping device adoption. Demand is also influenced by rising tinnitus cases linked to industrial noise exposure and long-term occupational hearing damage across urban populations.

Germany Tinnitus Masker Market Trends

Germany is estimated to hold 28% of the Europe market in 2026, making it the regional leader due to high hearing aid adoption rates and structured reimbursement systems covering a large portion of diagnosed patients. Penetration of hearing devices exceeds 35% among eligible users, reflecting strong clinical acceptance. A notable trend is the increasing shift toward AI-supported audiology fitting systems and remote calibration tools, which are reducing dependency on in-person clinic adjustments and improving long-term device optimization.

U.K. Tinnitus Masker Market Trends

The U.K. is estimated to account for 20% of the regional market in 2026, with demand heavily influenced by NHS-based audiology services and long patient waiting times for specialist consultations. Tinnitus prevalence is estimated at 10-15% of adults, but diagnosis rates remain uneven, creating latent demand for self-managed solutions. Expansion of community-based audiology services and tele-audiology integration within NHS frameworks is gradually improving access and reducing diagnostic bottlenecks.

Asia Pacific Tinnitus Masker Market Trends

Asia Pacific is estimated to account for approximately 24% of the global market in 2026, but is the fastest-growing region, driven by a combination of rising urban noise exposure, increasing industrial workforce size, and rapidly improving access to audiology care. Unlike mature markets, growth here is strongly volume-driven, supported by large untreated populations and increasing affordability of digital hearing solutions. Smartphone penetration is also accelerating adoption of app-connected tinnitus management devices across urban centers.

China Tinnitus Masker Market Trends

China is estimated to hold 40% of the Asia Pacific market in 2026, which translates into a very large absolute patient base due to population scale. Urban environmental noise and industrial exposure remain key drivers, particularly in manufacturing-heavy provinces. A defining trend is the rapid expansion of hospital-based AI diagnostic systems and ENT infrastructure in tier-1 and tier-2 cities, improving early detection and shifting treatment from reactive to preventive audiology care.

Japan Tinnitus Masker Market Trends

Japan is estimated to account for 22% of the regional market in 2026, with demand strongly concentrated in the elderly segment where tinnitus prevalence reaches 18.6% among adults aged 65+. However, unlike other regions, severity and chronicity are higher due to stress sensitivity and long life expectancy. Market adoption is being shaped by advanced integration of AI-enabled hearing aids and precision sound therapy systems in geriatric care, supported by highly developed audiology infrastructure and high healthcare utilization rates.

Competitive Landscape

The global tinnitus masker market is moderately consolidated, with leading players such as Sonova, Demant, GN Store Nord, Starkey, and WS Audiology collectively estimated to hold a significant share of global revenues. These companies maintain strong dominance through established audiology networks, deep relationships with ENT clinics, and integrated product portfolios combining hearing aids and tinnitus masking solutions. Their leadership is further reinforced by continuous investments in AI-based sound processing, Bluetooth-enabled devices, and app-connected hearing platforms, strengthening product differentiation in premium segments.

Regional and niche players, including innovators in digital therapeutics and neuromodulation-based tinnitus solutions, are expanding their presence through targeted clinical offerings and OTC-enabled products. While regulatory approvals, clinical validation requirements, and audiology licensing create high entry barriers, the rise of tele-audiology, direct-to-consumer channels, and software-driven hearing care is gradually improving market accessibility. The competitive landscape is expected to evolve toward increased consolidation, with established players expanding through acquisitions and partnerships focused on digital hearing ecosystems and personalized tinnitus management solutions.

Key Industry Developments:

- In December 2025, Sonova expanded its tinnitus portfolio by integrating the SilentCloud digital tinnitus therapy platform, combining sound therapy and CBT-based digital interventions into its hearing care ecosystem. The move signals a shift toward scalable, app-based tinnitus management solutions and strengthens Sonova’s hybrid digital-clinical strategy.

- In April 2025, WS Audiology expanded its India operations by establishing a commercial and production hub in Bangalore, strengthening its footprint in a high-growth APAC hearing care market. The expansion improves access to hearing aids and tinnitus solutions through enhanced local manufacturing, distribution, and service capabilities.

Companies Covered in Tinnitus Masker Market

- Sonova Holding AG

- Demant A/S

- GN Store Nord A/S

- WS Audiology

- Starkey Laboratories

- Cochlear Limited

- MED-EL

- Widex

- Rexton

- Miracle-Ear

- Beltone

- Audina Hearing Instruments

- Arphi Electronics

- Puretone Ltd

- Neuromod Devices

Frequently Asked Questions

The global tinnitus masker market is projected to reach US$2.9 billion in 2026.

The tinnitus masker market is driven by rising tinnitus prevalence, increasing hearing loss cases, and growing adoption of digital hearing care solutions.

The tinnitus masker market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

Key opportunities lie in AI-enabled hearing devices, tele-audiology expansion, and digital sound therapy integration.

Key players include Sonova, Demant, GN Store Nord, Starkey, and WS Audiology.