- Oil & Gas

- Oil and Gas Lubricants Market

Oil and Gas Lubricants Market Size, Share, and Growth Forecast, 2026 - 2033

Oil and Gas Lubricants Market by Sector (Upstream, Midstrea, Others), Product Type (Hydraulic Oil, Synthetic-based, Others), Base Oil, Application, and Regional Analysis for 2026 - 2033

Oil and Gas Lubricants Market Size and Trends Analysis

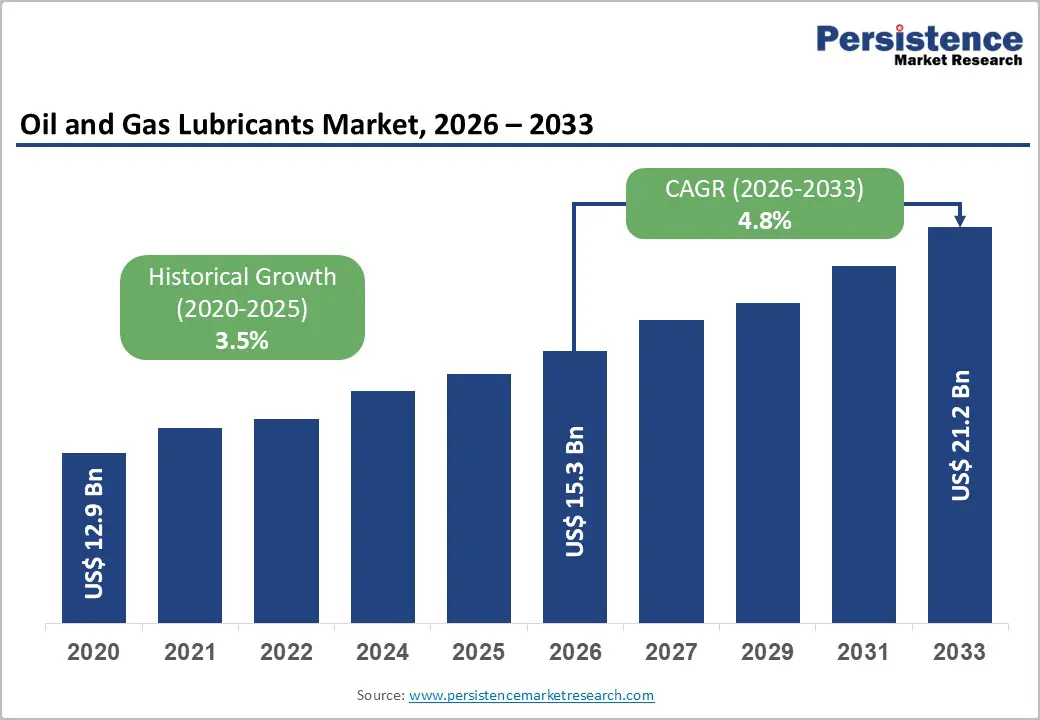

The global oil and gas lubricants market size is likely to be valued at US$15.3 billion in 2026 and is expected to reach US$21.2 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by sustained upstream capital expenditure, expansion of offshore and deepwater operations, and rising demand for high-performance lubricants under extreme operating conditions. Increasing environmental regulations are accelerating the transition toward synthetic and bio-based lubricants with improved efficiency, lower emissions, and extended service life.

Key Industry Highlights:

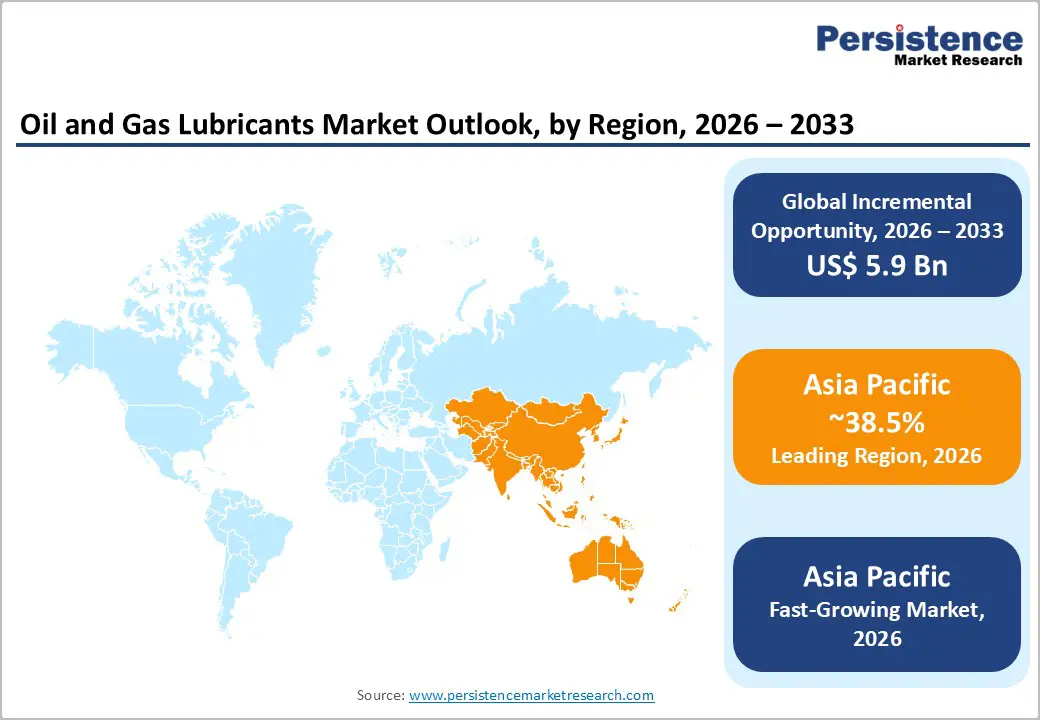

- Leading Region: Asia Pacific is projected to account for approximately 38.5% of the market share, supported by strong industrial growth, expanding refining capacity, and increasing upstream and downstream investments across China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, with a projected growth rate exceeding the global average, driven by rising energy demand, infrastructure expansion, and increasing adoption of high-performance lubricants in emerging economies.

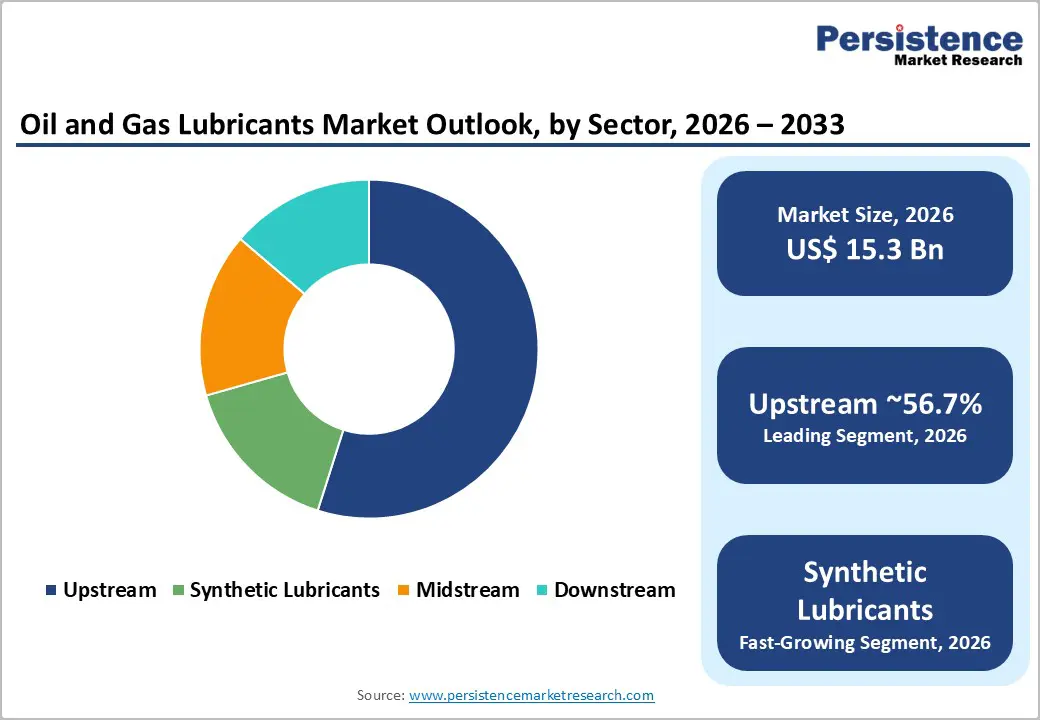

- Dominant Sector: The upstream sector is anticipated to dominate, holding approximately 56.7% of market share, due to the high intensity of drilling, extraction, and production activities requiring continuous lubrication under extreme operating conditions.

- Leading Product Type: Hydraulic oil is estimated to lead, accounting for around 38.9% share, owing to its extensive use in drilling rigs, production systems, and pipeline operations where consistent performance and equipment reliability are critical.

| Key Insights | Details |

|---|---|

| Oil and Gas Lubricants Market Size (2026E) | US$15.3 Bn |

| Market Value Forecast (2033F) | US$21.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

DRO Analysis

Driver Analysis - Sustained Upstream Investment Driving Core Demand

Upstream oil & gas activities continue to represent the backbone of lubricant consumption due to the high intensity of mechanical operations involved. Continuous drilling, well maintenance, and production optimization require extensive use of lubricants across rigs, pumps, compressors, and rotating equipment. A significant portion of global upstream investments is directed toward offsetting natural decline rates of existing fields, ensuring consistent operational activity. This structural dependency creates stable demand for lubricants, even during periods of moderate oil price volatility. As operators focus on maximizing recovery rates and improving efficiency, the need for high-quality lubricants with superior wear protection and thermal stability continues to increase.

Expansion of Offshore and Deepwater Exploration

The increasing number of offshore and deepwater projects is significantly influencing lubricant demand patterns. These environments expose equipment to high pressure, temperature fluctuations, salinity, and continuous operational stress. Such conditions require advanced lubricant formulations capable of maintaining viscosity, resisting oxidation, and reducing equipment wear over extended intervals. The commissioning of new offshore fields and subsea installations has increased the adoption of premium lubricants, including synthetic hydraulic oils, compressor oils, and greases. This shift toward technically advanced lubricants is improving equipment reliability and reducing maintenance frequency, which is critical for cost-intensive offshore operations.

Stringent Environmental and Performance Regulations

Regulatory frameworks are becoming increasingly stringent, particularly in regions with strong environmental oversight. Regulations governing lubricant toxicity, biodegradability, and emissions are encouraging the use of environmentally acceptable lubricants. Industry standards are also evolving to require higher performance levels, including improved fuel efficiency, reduced sludge formation, and enhanced oxidation stability. These regulatory developments are pushing manufacturers to innovate and develop advanced formulations. As a result, synthetic and bio-based lubricants are gaining traction, particularly in offshore, marine, and environmentally sensitive applications.

Restraint Analysis - Oil Price Volatility Impacting Procurement Cycles

Fluctuations in crude oil prices directly influence upstream investment decisions and operational budgets. During periods of declining prices, operators often reduce capital expenditures and delay maintenance activities to control costs. This leads to extended lubricant replacement cycles and lower short-term demand. While the installed equipment base remains intact, procurement volumes may decline due to inventory optimization and cost containment strategies. This cyclical behavior introduces uncertainty in demand forecasting for lubricant manufacturers and suppliers.

Cost and Recycling Challenges for Advanced Lubricants

High-performance lubricants, particularly synthetic and bio-based variants, come with higher production and procurement costs compared to conventional mineral oils. These costs can be a barrier in price-sensitive markets or in operations with tight budget constraints. In addition, the disposal and re-refining of used lubricants containing complex additive packages or bio-based components present technical challenges. These factors increase the total cost of ownership and may limit the widespread adoption of advanced lubricants, especially in regions with less developed waste management infrastructure.

Opportunity Analysis - Asia Pacific as a High-Growth Demand Center

Asia Pacific represents the most significant growth opportunity, with an estimated 38.5% share of the global market and the fastest growth rate. Rapid industrialization, expanding energy demand, and increasing investments in oil and gas infrastructure are driving lubricant consumption across the region. Countries such as China, India, and those in Southeast Asia are witnessing growth in refining capacity, petrochemical production, and exploration activities. This creates sustained demand for both conventional and high-performance lubricants across upstream, midstream, and downstream sectors.

Rising Adoption of Bio-Based and Environmentally Acceptable Lubricants

The growing emphasis on sustainability and environmental protection is creating opportunities for bio-based lubricants. These products offer advantages such as biodegradability, lower toxicity, and compliance with environmental regulations. Their adoption is particularly strong in offshore operations, marine environments, and ecologically sensitive areas. As regulatory pressure increases and technological advancements improve performance characteristics, bio-based lubricants are expected to gain a larger share of the market.

Shift toward Service-Oriented Business Models

Lubricant manufacturers are increasingly offering value-added services such as oil condition monitoring, predictive maintenance, and technical support. These services help operators optimize lubricant usage, extend equipment life, and reduce downtime. The shift toward service-based offerings allows companies to differentiate themselves in a competitive market while creating recurring revenue streams. This trend is particularly relevant in the oil and gas sector, where equipment reliability and operational efficiency are critical to profitability.

Category-wise Analysis

Sector Insights

The upstream sector is anticipated to remain the leading segment, accounting for approximately 56.7% of market share in 2026, due to the intensive use of drilling and production equipment. Operations in this segment involve continuous mechanical activity, including drilling, well completion, and extraction processes. Equipment such as mud pumps, compressors, top drives, and drilling rigs requires high-performance lubricants to withstand extreme pressure, temperature variations, and abrasive environments. For instance, offshore rigs in deepwater basins such as the Gulf of Mexico and Brazil’s pre-salt fields rely heavily on advanced hydraulic oils and greases to maintain operational continuity. The high frequency of maintenance cycles and the critical nature of equipment uptime further reinforce the dominance of upstream applications in overall lubricant consumption.

Synthetic lubricants are the fastest-growing segment, anticipated to be driven by the increasing adoption across upstream and midstream operations, particularly in technically demanding environments. These lubricants offer superior thermal stability, oxidation resistance, and performance under extreme loads, making them suitable for deepwater exploration, LNG facilities, and gas compression systems. For example, synthetic compressor oils are increasingly used in natural gas processing plants to ensure longer service intervals and reduced downtime. As oil and gas companies prioritize cost optimization, asset longevity, and operational efficiency, the demand for synthetic lubricants is expected to grow steadily, especially in high-value and remote installations.

Product Type Insights

Hydraulic oil is anticipated to lead, accounting for approximately 38.9% of market share in 2026, driven by its extensive use across drilling rigs, production facilities, and pipeline operations. Hydraulic systems are integral to lifting, control, and power transmission functions in oilfield equipment, requiring lubricants that provide consistent viscosity, anti-wear protection, and resistance to contamination. For example, hydraulic oils are widely used in blowout preventers (BOPs), offshore cranes, and subsea control systems, where reliability is critical for safety and operational efficiency. The widespread deployment of hydraulic systems across upstream, midstream, and downstream sectors ensures sustained and stable demand for these lubricants.

The fastest-growing product category is anticipated to be synthetic-based lubricants, supported by their superior performance characteristics. These products offer enhanced thermal stability, oxidation resistance, and extended service life compared to conventional mineral oils. They are increasingly used in high-performance applications such as gas turbines, compressors, and critical rotating equipment in refineries and LNG terminals. For instance, synthetic turbine oils are gaining traction in power generation units within refineries due to their ability to maintain efficiency under high temperatures. The transition toward synthetic lubricants is being driven by the need for improved operational reliability, reduced maintenance frequency, and compliance with evolving environmental and performance standards.

Regional Insights

North America Oil and Gas Lubricants Market Trends - Offshore and Shale-Driven Demand for High-Performance and Synthetic Lubricants

North America represents a mature yet technologically advanced market for oil and gas lubricants, anticipated to account for a significant share of global demand driven by high-value upstream and offshore operations. The region benefits from extensive exploration and production activities, particularly in the Gulf of Mexico, where deepwater projects continue to require high-performance lubricants for drilling rigs, subsea systems, and floating production units. Companies such as ExxonMobil and Chevron Corporation maintain strong operational footprints in this region, supporting consistent lubricant consumption through their upstream and integrated operations. Stable production levels and continued investment in shale and offshore assets ensure a steady demand base for hydraulic oils, compressor oils, and greases.

Regulatory frameworks in North America emphasize environmental protection and operational efficiency, driving the adoption of environmentally acceptable lubricants in offshore and marine applications. For instance, Shell plc has expanded its portfolio of high-performance synthetic lubricants tailored for extreme offshore conditions, while Chevron Corporation continues to develop premium lubricant formulations under its industrial brands. The region also acts as a hub for innovation, with significant investments in R&D and digital monitoring solutions such as predictive maintenance and oil condition analysis. These developments are reinforcing North America’s leadership in high-spec lubricant adoption and technological advancement.

Europe Oil and Gas Lubricants Market Trends - Sustainability-Led Shift toward Biodegradable and Premium Lubricant Solutions

The oil and gas lubricants market in Europe is characterized by strict environmental regulations and a strong focus on sustainability, with anticipated steady value growth driven by premium and eco-friendly lubricant adoption. Regulatory frameworks are encouraging the transition toward low-toxicity, biodegradable, and energy-efficient lubricant formulations. Countries such as Germany, the U.K., France, and Spain play a significant role in market development, supported by strong industrial bases and advanced manufacturing capabilities. Companies such as FUCHS SE and BP p.l.c. (through its Castrol brand) are actively investing in sustainable lubricant technologies, including bio-based and low-emission products.

The market is increasingly shifting toward premium products with higher performance standards. For example, TotalEnergies SE has expanded its range of marine and industrial lubricants designed to meet stringent environmental requirements in European waters. Similarly, Exxon Mobil Corporation continues to maintain a strong lubricant presence in Europe despite restructuring parts of its downstream operations, highlighting the strategic importance of the lubricant segment. These developments are accelerating the transition toward high-value lubricant products, where performance, compliance, and sustainability drive purchasing decisions more than volume alone.

Asia Pacific Oil and Gas Lubricants Market Trends - Rapid Industrial Expansion Fueling High-Volume Growth in Oil and Gas Lubricants

Asia Pacific is the largest and fastest-growing region, accounting for approximately 38.5% of the global market in 2026, driven by rapid industrialization, rising energy demand, and expanding oil and gas infrastructure. Countries such as China, India, and Japan are leading contributors, supported by investments in refining, petrochemicals, and upstream exploration. National oil companies like Sinopec and Indian Oil Corporation play a crucial role in driving regional lubricant demand through their extensive refining and distribution networks. These companies also produce and market a wide range of industrial lubricants, strengthening local supply chains.

The region benefits from cost advantages, large-scale manufacturing, and a rapidly growing industrial base. For instance, TotalEnergies SE has expanded its lubricant product offerings in India with next-generation engine oils, while Shell plc continues to invest in blending plants and distribution networks across Southeast Asia. Demand is increasing across upstream, midstream, and downstream sectors, including LNG terminals, pipelines, and refining complexes. The adoption of advanced lubricants is also rising as operators seek to improve efficiency, reduce downtime, and meet evolving environmental standards. This combination of strong volume growth and increasing penetration of premium products positions Asia Pacific as the primary growth engine for the global oil and gas lubricants market.

Competitive Landscape

The global oil and gas lubricants market is fragmented to moderately consolidated, with a mix of global leaders and regional players. Large multinational companies dominate in terms of product innovation, brand recognition, and global distribution networks. However, regional and local manufacturers maintain a strong presence by offering cost-competitive solutions and localized services. Competitive differentiation is based on product performance, technical support, and supply chain efficiency.

Key players are focusing on innovation, sustainability, and service integration. Strategies include developing advanced formulations, expanding distribution networks, and offering value-added services such as condition monitoring. Companies are also investing in environmentally friendly products to align with regulatory requirements and evolving customer preferences.

Key Industry Developments:

- In May 2025, Lubrication Engineers announced the acquisition of RSC Bio Solutions, a company specializing in biodegradable and environmentally acceptable lubricants, to strengthen its portfolio of sustainable lubrication technologies and expand its presence in eco-friendly industrial applications.

- In November 2025, Whitmore Manufacturing (Jet-Lube brand) acquired ProAction Fluids, expanding its portfolio to include drilling fluids and strengthening its position in oilfield service lubrication and specialty chemicals.

Companies Covered in Oil and Gas Lubricants Market

- Shell plc

- Exxon Mobil Corporation

- Chevron Corporation

- TotalEnergies SE

- BP p.l.c.

- Sinopec

- FUCHS SE

- Idemitsu Kosan Co., Ltd.

- Phillips 66

- Valvoline Inc.

- Indian Oil Corporation

- PetroChina Company Limited

- Petrobras

- Lukoil

- ENEOS Corporation

- Petronas

Frequently Asked Questions

The oil and gas lubricants market is estimated to be valued at US$15.3 billion in 2026.

The oil and gas lubricants market is projected to reach US$21.2 billion by 2033.

Key trends include the increasing adoption of synthetic and bio-based lubricants, rising demand for high-performance formulations in extreme environments, and the growing use of condition monitoring and predictive maintenance services to enhance operational efficiency.

The upstream sector is the leading segment, accounting for approximately 56.7% of market share, due to the high intensity of drilling and production activities.

The oil and gas lubricants market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Some of the major players include Shell plc, Exxon Mobil Corporation, Chevron Corporation, TotalEnergies SE, and BP p.l.c..