- Oil & Gas

- Wellhead Components Market

Wellhead Components Market Size, Share, and Growth Forecast 2026 - 2033

Wellhead Components Market by Product Type (Hangers, Flanges, Master Valve, Casing Head, Casing Spools, Others), by Application (Onshore, Offshore), and Regional Analysis for 2026 - 2033

Wellhead Components Market Size and Trend Analysis

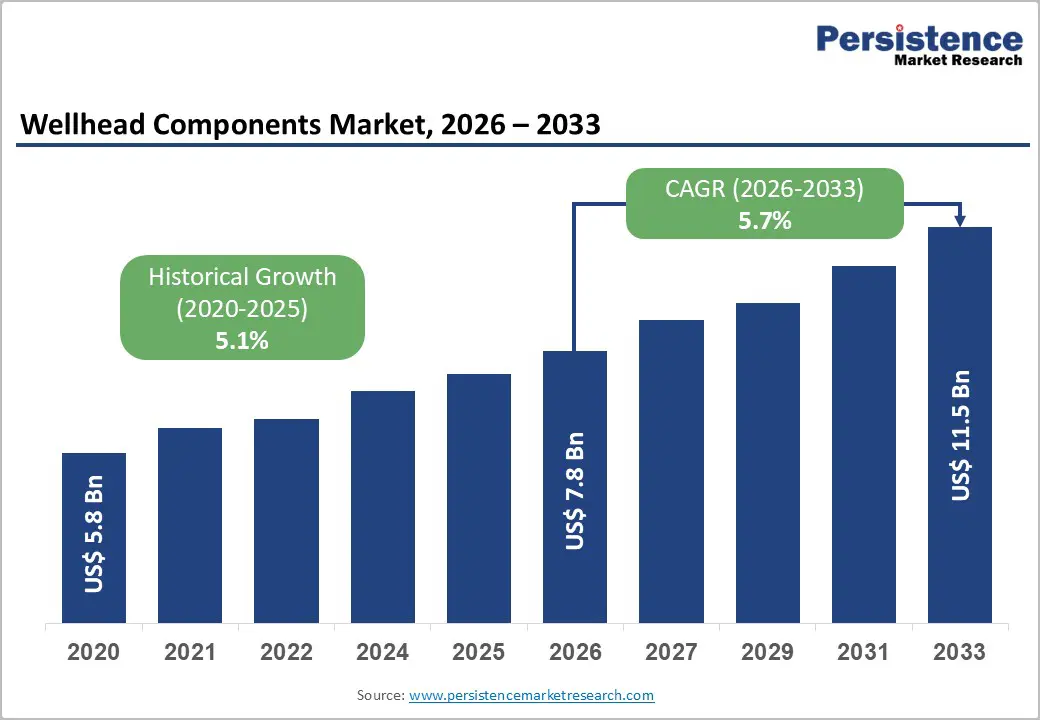

The global Wellhead Components market size is supposed to be valued at US$ 7.8 Billion in 2026 and is projected to reach US$ 11.5 Billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The market's sustained and accelerating growth trajectory is fundamentally anchored in the global energy sector's continued reliance on hydrocarbon production to meet rising baseload energy demand, coupled with expanding upstream capital expenditure across conventional and unconventional oil and gas plays. Approximately 95,000 new wells are drilled each year globally, according to available industry data, ensuring a persistent and large-volume procurement pipeline for casing heads, master valves, hangers, flanges, and casing spools that are indispensable at every new well completion.

Key Market Highlights

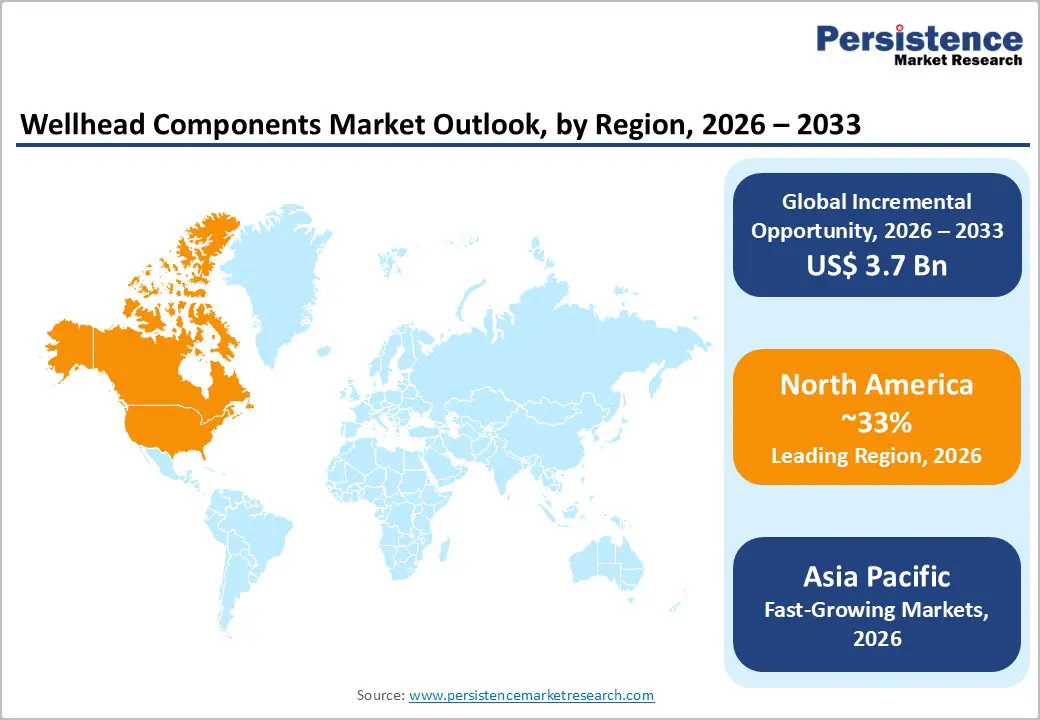

- Dominant Region: North America leads the global Wellhead Components market, underpinned by the U.S.'s record crude oil production of 13.3 million barrels per day in 2024 as reported by the EIA, and the Permian Basin's continuous high-volume shale drilling activity, sustaining the highest annual wellhead component procurement volumes of any single national market globally.

- Growing Region: Asia Pacific is the fastest-growing region for wellhead components, driven by China's NEA domestic gas expansion targets under the 14th Five Year Plan, India's ONGC KG-DWN-98/2 deepwater program, and ASEAN LNG infrastructure development, generating accelerating subsea and onshore wellhead procurement demand.

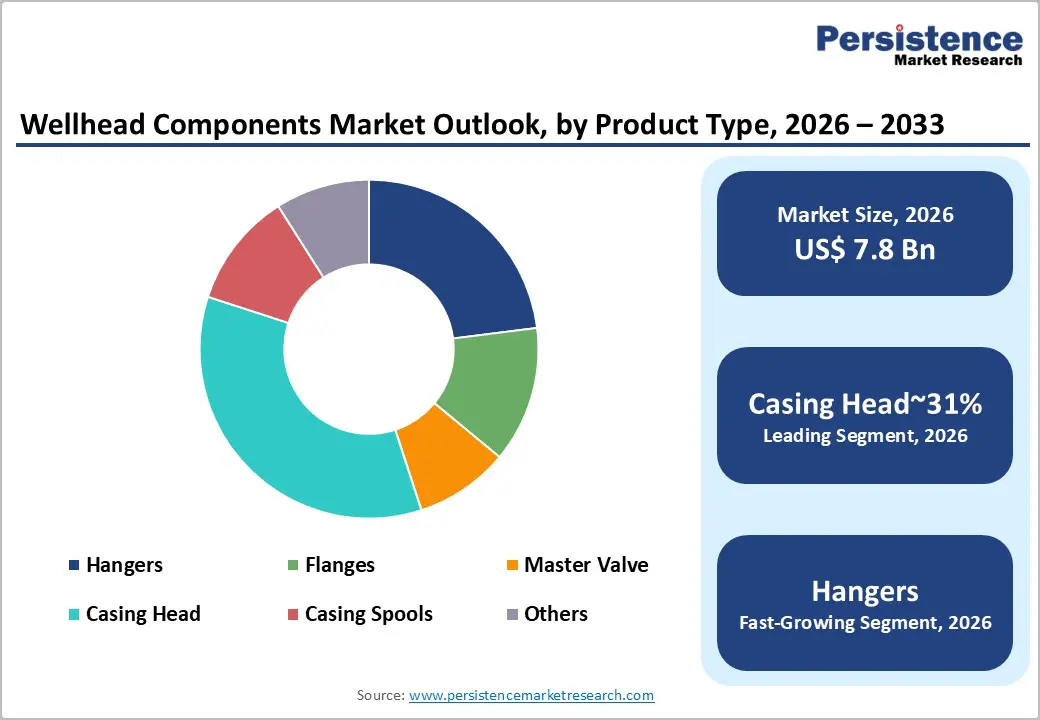

- Dominant Product Type: Casing Heads dominate the Product Type segment with approximately 31% revenue share in 2026, reinforced by their mandatory installation in every oil and gas well globally, foundational structural role in all wellhead assembly configurations, and universal procurement requirement across 95,000 new wells drilled annually worldwide.

- Growing Application: Offshore wellhead components are the fastest-growing Application segment, driven by floating rig utilization exceeding 90% globally in 2024 per IADC data and Petrobras's US$ 100 billion pre-salt development investment through 2028, generating accelerating demand for premium-specification subsea and HPHT wellhead assemblies.

- Opportunity: Smart wellhead technology and CCS-ready wellhead component development represent the key market opportunity, with the U.S. IRA's 45Q tax credit of US$ 85 per tons and IEA's CCS 20-fold capacity expansion requirement by 2030 creating structurally new procurement demand for digitally integrated and CO2-service-rated wellhead assemblies commanding 20–30% price premiums over conventional products.

| Key Insights | Details |

|---|---|

|

Wellhead Components Market Size (2026E) |

US$ 7.8 Billion |

|

Market Value Forecast (2033F) |

US$ 11.5 Billion |

|

Projected Growth CAGR (2026–2033) |

5.7% |

|

Historical Market Growth (2020–2025) |

5.1% |

Market Dynamics

Drivers - Recovering Global Upstream Capital Expenditure and Rising Drilling Activity Sustaining Wellhead Demand

The sustained recovery of global upstream oil and gas capital expenditure since 2022 is the most powerful structural driver of wellhead component demand worldwide. The IEA's World Energy Investment Report 2024 confirmed that global upstream oil and gas investment reached approximately US$ 530 billion in 2024, a multi-year high, reflecting the oil and gas industry's commitment to maintaining and expanding production capacity in response to persistent global energy demand growth. The U.S. Energy Information Administration (EIA) reported that the U.S. rig count, a leading indicator of drilling activity and wellhead component procurement, stabilized at approximately 590 active rigs in late 2024, with continued activity in the Permian Basin, Eagle Ford, and Haynesville Shale plays sustaining large-volume orders for onshore wellhead assemblies.

Internationally, OPEC+ producers including Saudi Arabia, the UAE, and Iraq have committed to substantial upstream expansion programs targeting long-term production capacity maintenance, generating consistent procurement demand for wellhead components across conventional high-volume reservoir development projects in the Middle East and Africa region.

Deepwater and Ultra-Deepwater Exploration Expansion Driving Premium Offshore Wellhead Demand

The accelerating global shift toward deepwater and ultra-deepwater oil and gas exploration, particularly in Brazil's pre-salt Santos Basin, the Gulf of Mexico, West Africa, and Southeast Asia, is generating disproportionately high demand for advanced, high-pressure high-temperature (HPHT) rated subsea wellhead systems. The International Association of Drilling Contractors (IADC) has reported a sustained uptick in offshore rig utilization rates, with floating rig utilization exceeding 90% globally in 2024, a near-decade high, reflecting the depth and breadth of offshore development commitments by major operators.

Deepwater wellhead assemblies require specialized high-alloy steel casings, precision-engineered flanges and hangers rated for pressures exceeding 15,000 psi, and corrosion-resistant coatings qualified to stringent API 6A and API 17D standards. The Brazilian National Petroleum Agency (ANP) has confirmed Petrobras's continued investment in pre-salt development exceeding US$ 100 billion through 2028, directly sustaining a large multi-year procurement pipeline for offshore wellhead components. TechnipFMC and SLB are actively expanding their subsea wellhead technology capabilities to address this high-value growth segment.

Restraints - Volatility in Global Oil Prices Creating Capital Expenditure Uncertainty

The wellhead components market remains highly sensitive to cyclical fluctuations in global crude oil and natural gas prices, which directly govern upstream operator capital expenditure decisions and, by extension, drilling activity volumes. The IEA has documented that every sustained US$ 10 per barrel decline in crude oil prices historically translates into a meaningful reduction in global upstream drilling budgets, with smaller independent operators disproportionately cutting exploration and development spending.

During the 2015–2016 oil price downturn, global upstream investment declined by approximately 44% over two years, severely contracting wellhead component demand. While prices have stabilized in the US$ 70–80 per barrel range in 2024–2025, ongoing geopolitical uncertainties and energy transition concerns continue to suppress the long-cycle investment commitments that drive the largest wellhead procurement programs.

Stringent API and ISO Certification Requirements Increasing Compliance Costs for Manufacturers

Wellhead components are subject to some of the most demanding quality and safety certification requirements in the industrial manufacturing sector, governed by API 6A (for surface wellhead equipment), API 17D (for subsea wellhead equipment), ISO 10423, and NACE MR0175 corrosion resistance standards. These certifications require manufacturers to maintain extensive quality management systems, conduct rigorous third-party material testing and pressure qualification, and implement detailed traceability documentation across all production processes, compliance costs that can represent 15–20% of total manufacturing overhead for specialized wellhead component producers.

For smaller regional manufacturers lacking the scale to amortize these certification costs efficiently, compliance requirements effectively create a structural barrier to competing in specification-driven international tender markets dominated by certified global players.

Opportunities - Smart Wellhead Technologies and Digital Integration Unlocking High-Value Product Differentiation

The integration of digital monitoring, automation, and Industrial Internet of Things (IIoT) capabilities into wellhead component systems represents one of the most commercially significant and rapidly expanding technology-driven growth opportunities in the global wellhead components market. The oil and gas industry's accelerating digitalization agenda, driven by operator mandates for production optimization, real-time safety monitoring, and operational cost reduction, is creating sustained procurement demand for smart wellhead assemblies equipped with embedded pressure and temperature sensors, automated choke control systems, and cloud-connected data transmission capabilities. Aker Solutions announced a strategic partnership in 2024 to develop a next-generation digital wellhead control system, reflecting the industry's growing investment in intelligent surface equipment.

The American Petroleum Institute (API) has been developing updated standards to incorporate smart well technology performance criteria, further institutionalizing digital wellhead procurement specifications across major operator supply chains. Manufacturers that can deliver API 6A-certified wellhead components with integrated digital monitoring architectures will command meaningful price premiums, estimated at 20–30% above conventional wellhead pricing, and gain preferred supplier status with technology-forward operators pursuing zero-unplanned-downtime operational objectives in critical production environments.

Carbon Capture and Storage (CCS) and Geothermal Well Infrastructure Creating New Application Frontiers

Beyond traditional hydrocarbon applications, the global expansion of Carbon Capture and Storage (CCS) projects and the accelerating development of geothermal energy infrastructure are creating structurally new and high-growth demand frontiers for specialized wellhead component manufacturers. Governments across Europe, North America, and Asia Pacific have committed substantial capital to CCS deployment under national decarbonization strategies, the U.S. Inflation Reduction Act (IRA) expanded the 45Q tax credit to up to US$ 85 per metric tonne of CO2 permanently stored, catalyzing a wave of new CCS injection well projects that require purpose-engineered CO2-service-rated wellhead assemblies with enhanced corrosion resistance to carbonic acid environments.

The IEA projects that global CCS capacity must grow 20-fold by 2030 under Net Zero scenarios, implying substantial new wellhead component procurement demand from this emerging application. Concurrently, geothermal wellhead components, rated for high-temperature steam and mineral-laden brines, are experiencing double-digit demand growth, supported by government renewable energy mandates in Iceland, Indonesia, Kenya, and the United States.

Category-wise Insights

By Product Type

Casing head leads the global market by product type, capturing approximately 31% of total product type segment revenue in 2026, as supported by available industry data confirming casing heads' 31.2% dominant share in 2024. Casing heads serve as the foundational structural component of every wellhead assembly, providing the primary load-bearing attachment point for all subsequent casing strings, isolating the well from surface contamination, and establishing the pressure integrity baseline for the entire wellhead system. Their mandatory installation in every oil and gas well, from shallow conventional wells to ultra-deepwater subsea completions, ensures the highest procurement frequency and volume of any single wellhead component category.

The API 6A standard governing casing head design and pressure ratings provides a rigorous specification framework that virtually all major operators worldwide reference in procurement contracts, ensuring sustained demand for API-certified casing heads across all geographies and well types. Master Valve components represent the second-largest segment, while Casing Spools held approximately 25.7% market share in 2024, reflecting their critical role in multi-string well architecture across complex reservoir developments.

By Application

The Onshore application segment dominates the global Wellhead Components market, commanding approximately 74% of total application segment revenue in 2026, directly corroborated by market data showing onshore applications capturing 73.9% share in the wellhead system market and approximately 80% share in the wellhead components segment specifically, as reported by Persistence Market Research. Onshore wellhead components' enduring dominance reflects the sheer volume of active land-based oil and gas wells globally, with the U.S. Permian Basin alone accounting for over 5,000 active drilling locations at any given time, combined with the significantly lower per-unit installation complexity, faster project turnaround, and more accessible maintenance practices of land-based operations compared to offshore environments. Unconventional resource development programs in the United States, Canada, China, and Argentina's Vaca Muerta formation sustain continuous high-volume casing head, hanger, and flange procurement for onshore well completions.

The Offshore segment, while smaller in volume share, generates significantly higher per-unit revenue, particularly for subsea and HPHT wellhead systems, and is the fastest-growing application segment, driven by expanding deepwater investment programs across Brazil, West Africa, the North Sea, and Southeast Asia.

Regional Insights

North America Wellhead Components Market Trends

North America is the global leader in wellhead component demand, anchored by the United States' unrivalled position as the world's largest oil and gas producer, with the U.S. EIA reporting crude oil production exceeding 13.3 million barrels per day in 2024, a new historical record, and the country's prolific shale and tight oil development activity that drives the highest per-annum wellhead component procurement volumes of any single national market. The Bureau of Land Management (BLM) and Bureau of Safety and Environmental Enforcement (BSEE) regulatory frameworks establish rigorous wellhead equipment performance standards for onshore federal land and offshore U.S. operations respectively, effectively mandating premium-specification components from certified suppliers across major development programs.

Canada contributes meaningfully to North American wellhead demand through Alberta oil sands thermal well programs and Atlantic offshore developments managed by the Canada-Newfoundland and Labrador Offshore Petroleum Board (CNLOPB). The U.S. Pipeline and Hazardous Materials Safety Administration (PHMSA) regulations on wellhead integrity requirements further elevate procurement specification standards across the U.S. market. North American technology leaders including Halliburton and SLB maintain dominant positions through integrated wellhead component supply, installation engineering, and digital well monitoring service offerings that create high switching costs and strong customer retention, cementing the region's commercial and technological leadership in the global wellhead components market.

Europe Wellhead Components Market Trends

Europe's wellhead components market is defined by the technically demanding offshore operating environments of the North Sea, encompassing Norwegian, British, and Danish sectors, where high-pressure, sub-zero temperature, and highly corrosive subsea conditions mandate the industry's most advanced and rigorously certified wellhead component specifications. Norway's Norwegian Petroleum Directorate (NPD) has confirmed that over 90 active fields operate on the Norwegian Continental Shelf (NCS), with continuous well maintenance, infill drilling, and new tieback developments sustaining consistent wellhead component demand. Equinor ASA, TotalEnergies, and Aker BP are the dominant operators driving procurement of advanced subsea and surface wellhead assemblies compliant with NORSOK standards, some of the world's most stringent petroleum equipment technical specifications.

The United Kingdom North Sea Transition Authority (NSTA), formerly the Oil and Gas Authority (OGA), has issued production efficiency directives that actively encourage infill drilling and late-life field rejuvenation on the United Kingdom Continental Shelf (UKCS), generating incremental wellhead component replacement and upgrade demand. Germany and the Netherlands contribute to European onshore wellhead demand through conventional gas production, while Spain and France participate through their national energy companies' international upstream portfolios. The EU's stringent environmental regulations, including the EU Offshore Safety Directive 2013/30/EU, mandate comprehensive wellhead integrity management programs that require regular component inspection, testing, and replacement, sustaining a durable aftermarket demand stream for wellhead component suppliers operating in European waters.

Asia Pacific Wellhead Components Trends

Asia Pacific is the fastest-growing regional market for wellhead components globally, propelled by China's domestic gas production expansion through tight sandstone plays, India's deepwater development programs in the KG Basin, and accelerating LNG infrastructure investment across Australia, Indonesia, and Vietnam. China's National Energy Administration (NEA) has set ambitious domestic gas production targets aligned with the country's 14th Five Year Plan, requiring rapid deployment of quick-install wellhead systems optimized for the country's "factory drilling" unconventional well development model, where hundreds of standardized wells are drilled and completed in rapid sequence using repeatable wellhead assembly configurations. CNOOC, PetroChina, and SINOPEC collectively drive enormous wellhead component procurement volumes across Chinese domestic upstream programs.

India's Oil and Natural Gas Corporation (ONGC) is advancing development of the KG-DWN-98/2 deepwater cluster in the Bay of Bengal, triggering procurement orders for thermally and mechanically demanding subsea wellhead systems capable of withstanding hydrate inhibition cycles in deepwater high-pressure environments. Indonesia's SKK Migas has committed to maintaining national oil production at one million barrels per day, driving ongoing wellhead equipment procurement across Sumatra and Kalimantan onshore blocks. Australia's offshore LNG development programs, managed under the regulatory oversight of the National Offshore Petroleum Safety and Environmental Management Authority (NOPSEMA), sustain demand for advanced offshore wellhead assemblies engineered for the region's challenging cyclone-prone marine environments. The region's growing domestic manufacturing capabilities, particularly in China and India, are also enabling cost-competitive regional wellhead component production that serves both domestic demand and export markets across Southeast Asia and Africa.

Competitive Landscape

The global wellhead components market is moderately consolidated at the premium technology tier, with large integrated oilfield services leaders, Halliburton, SLB (Schlumberger), Baker Hughes, and TechnipFMC, commanding significant share through their combined wellhead technology, installation engineering, and digital well management capabilities. These global players differentiate through API 6A and API 17D certification breadth, proprietary HPHT-rated material technologies, and service-bundled supply models that deliver higher customer lifetime value.

Emerging business model trends include digital wellhead-as-a-service offerings and wellhead component rental programs for shorter-life unconventional wells. Mid-tier specialists including Valveworks USA, TSI Flow Products, and Apache Pressure Products compete effectively in the onshore North American market through rapid order fulfillment, competitive pricing, and broad in-stock component availability that major multinational suppliers cannot match at the field procurement level.

Key Developments:

- In January 2026, SLB advanced its asset-light strategy in the global land rig market, finalizing portfolio transitions that sharpen its focus on high-margin wellhead technology and digital well management services, reinforcing its strategic positioning across North American and international upstream markets.

- In November 2024, Aker Solutions announced a strategic partnership to co-develop a next-generation digital wellhead control system integrating real-time pressure monitoring, automated choke management, and cloud-based production optimization for deepwater and harsh-environment offshore operations.

- In October 2023, TechnipFMC secured a major long-term contract for the supply of subsea wellhead systems for a significant deepwater development project in the Gulf of Mexico, leveraging its Unitized Wellhead System (UWS) technology platform to address ultra-deepwater HPHT operational requirements.

Companies Covered in Wellhead Components Market

- Halliburton

- SLB

- G.B. Industry Co.

- Apache Pressure Products

- Hartmann Valves GmbH

- Acteon Group Operations (UK) Limited

- INTEGRATED

- Dawsons-Tech Components LLP

- Singoo

- DKG Valve Manufacturing LLC

- Valveworks USA

- TSI Flow Products

- Canary, LLC

- Baker Hughes Company

- TechnipFMC plc

- NOV Inc.

Frequently Asked Questions

The global Wellhead Components market is estimated to be valued at US$ 7.8 Billion in 2026 and is projected to reach US$ 11.5 Billion by 2033, registering a forecast CAGR of 5.7% over the period 2026 to 2033. The market recorded a historical growth rate of 5.1% CAGR between 2020 and 2025, supported by consistent global upstream oil and gas investment recovery.

The primary growth drivers are the recovery of global upstream oil and gas capital expenditure to over US$ 530 billion in 2024 as reported by the IEA, sustaining approximately 95,000 new well completions annually, and the accelerating expansion of deepwater and ultra-deepwater drilling programs in Brazil, the Gulf of Mexico, and West Africa, where floating rig utilization exceeded 90% globally in 2024 per IADC data.

Casing heads lead the product type category with approximately 31% revenue share in 2026, supported by industry data confirming their 31.2% dominant share in 2024. Their leadership is driven by mandatory installation in every oil and gas well completion globally, foundational structural function in all wellhead assembly configurations, and universal specification under the API 6A standard across all major operator procurement frameworks worldwide.

North America leads the global Wellhead Components market, anchored by the United States' record crude oil production exceeding 13.3 million barrels per day in 2024 as confirmed by the U.S. EIA, and the Permian Basin's continuous high-volume shale drilling activity. North American regulatory bodies, BSEE and BLM, mandate rigorous wellhead certification standards that further concentrate procurement within the region's premium-specification supply ecosystem.

The most significant growth opportunity lies in smart wellhead technologies and CCS-ready wellhead components. The U.S. Inflation Reduction Act's 45Q tax credit of US$ 85 per tonne of stored CO₂ and the IEA's mandate for 20-fold CCS capacity expansion by 2030 are creating structurally new procurement demand for digitally integrated and corrosion-resistant CO₂-service-rated wellhead assemblies that command estimated 20–30% price premiums over conventional product lines.