- Oil & Gas

- Well Cementing Market

Well Cementing Market Size, Share, and Growth Forecast, 2026 - 2033

Well Cementing Market by Product Type (Primary Cementing, Remedial Cementing, Others), Well Location (Onshore Cementing, Offshore Cementing, Others), Well Type, Cement Class, and Regional Analysis for 2026 - 2033

Well Cementing Market Size and Trends Analysis

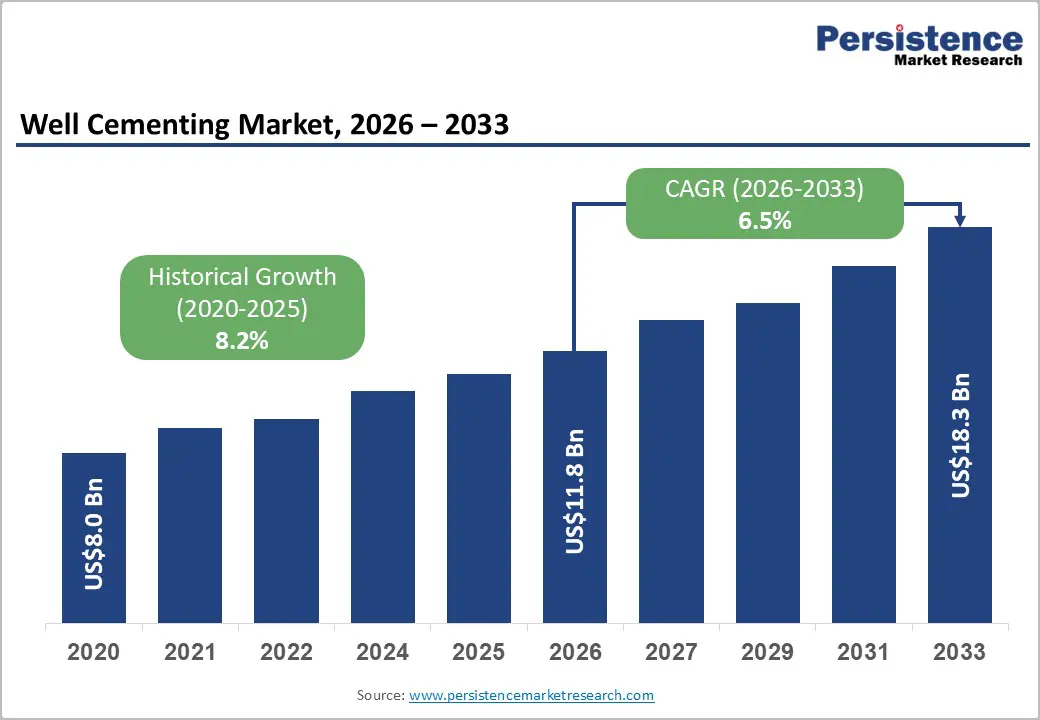

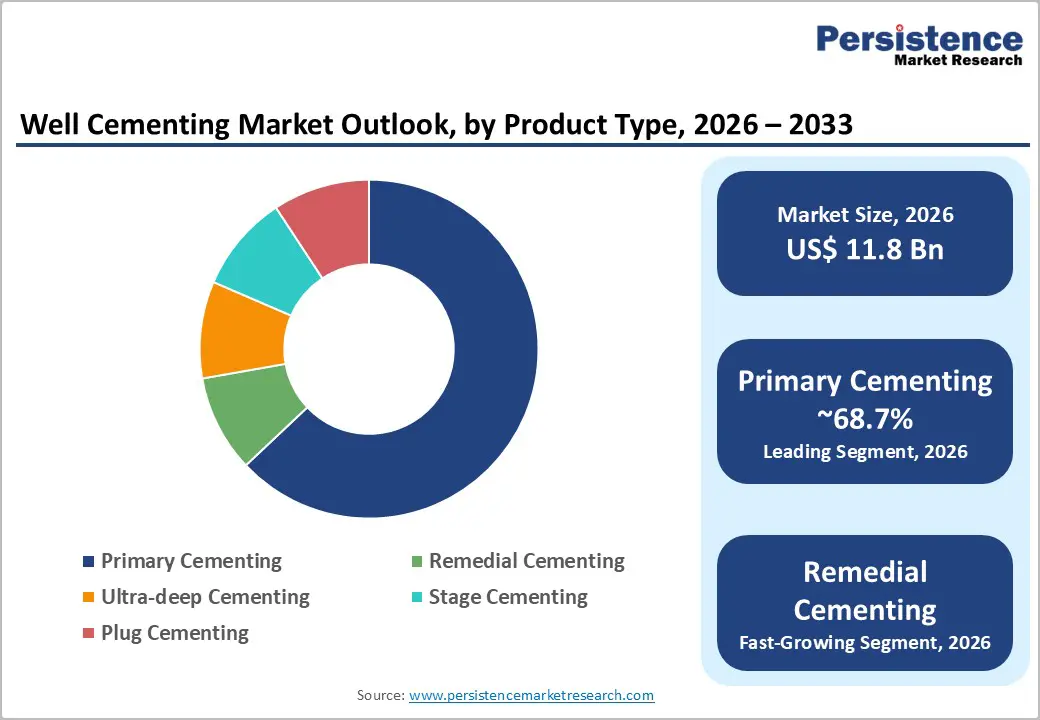

The global well cementing market size is likely to be valued at US$11.8 billion in 2026 and is expected to reach US$18.3 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033, driven by upstream drilling intensity, increasing well complexity, and stringent well integrity requirements.

Rising horizontal drilling activity and multi-well pad development are increasing cementing demand, while offshore expansion and carbon storage projects are introducing higher-specification cementing solutions. Despite some softening in upstream investment, structural demand for reliable zonal isolation continues to sustain long-term growth.

Key Industry Highlights:

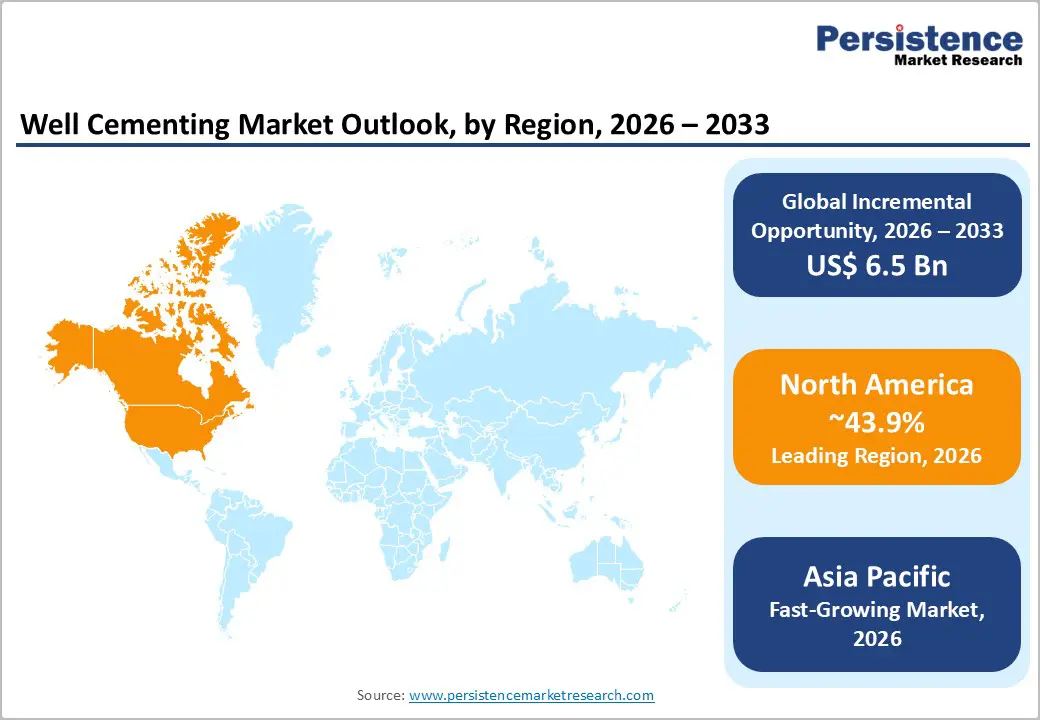

- Leading Region: North America is projected to hold approximately 43.9% market share, driven by high shale drilling activity, advanced oilfield infrastructure, and strong adoption of digital cementing technologies.

- Fastest-growing Region: Asia Pacific projected to grow at the highest CAGR, supported by rising upstream investments, offshore developments, and increasing energy demand in China and India.

- Investment Plans: Increasing investments in offshore deepwater projects and CCUS infrastructure, with upstream oil and gas spending remaining around US$420 billion (2025), alongside growing allocation toward digital cementing and well integrity solutions.

- Dominant Product Type: Primary cementing is anticipated to account for approximately 68.7% of the market share, driven by its essential role in all well construction activities and consistent demand across onshore and offshore drilling operations.

- Leading Well Type: Oil wells are estimated to represent approximately 54.8% market share, driven by sustained global crude oil demand and ongoing investments in conventional and offshore oilfield developments.

| Key Insights | Details |

|---|---|

| Well Cementing Market Size (2026E) | US$11.8 Bn |

| Market Value Forecast (2033F) | US$18.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.2% |

DRO Analysis

Driver Analysis - Increasing Well Completion Intensity and Horizontal Drilling Expansion

The rapid expansion of horizontal drilling and multi-well pad development is significantly increasing cementing demand. Over the past decade, the number of wells completed per location has more than doubled, reflecting a shift toward operational efficiency and cost optimization. Horizontal wells, which now account for a growing share of total production, require more complex cementing due to extended lateral lengths and higher pressure zones. This trend increases the need for advanced cement formulations, precise placement techniques, and faster execution. As operators continue to optimize drilling productivity, cementing services are becoming more critical to ensure well integrity and minimize non-productive time.

Growth in Offshore and Deepwater Exploration

Offshore and deepwater exploration activities are a major driver for high-value cementing services. These wells operate under extreme pressure and temperature conditions, requiring specialized cement systems capable of maintaining long-term structural integrity. Recent offshore project approvals and multi-year contracts indicate sustained investment in deepwater assets, particularly in regions such as Latin America and Southeast Asia. Offshore wells typically involve higher capital expenditure, making cementing quality critical to avoid costly failures. This drives demand for premium cementing solutions, including advanced slurry designs and real-time monitoring technologies.

Rising Focus on Well Integrity, Abandonment, and CCUS Applications

Well integrity has become a central concern due to environmental regulations and aging well infrastructure. Cementing plays a critical role in isolating zones, preventing fluid migration, and ensuring long-term stability. Increasing decommissioning activities and plug-and-abandonment requirements are expanding the scope of remedial cementing services. Carbon capture, utilization, and storage (CCUS) projects are also creating new demand for corrosion-resistant cement systems designed for CO2 injection wells. These applications require enhanced durability and long-term performance, positioning cementing as a key enabler of energy transition initiatives.

Restraint Analysis - Volatility in Oil Prices and Upstream Investment Cycles

Fluctuations in oil and gas prices directly influence upstream capital expenditure, which in turn impacts cementing demand. Periods of declining investment often lead to reduced drilling activity, delayed projects, and pricing pressure on service providers. Cost inflation in drilling and completion operations further compounds this challenge. Smaller service providers are particularly vulnerable due to limited financial flexibility, while larger players are forced to adopt integrated service models to maintain margins. This cyclical nature of the industry creates uncertainty in revenue streams and limits long-term planning.

Regulatory Complexity and Supply Chain Constraints

Stringent regulatory requirements, particularly in offshore environments, increase operational complexity and project timelines. Compliance with safety standards, environmental guidelines, and well integrity protocols adds to the cost of cementing operations. Supply chain challenges, including rising material costs for steel and specialized equipment, further impact profitability. Since cementing relies heavily on casing and tubular infrastructure, any disruption in material availability or pricing can significantly affect project economics. These factors collectively act as barriers to market expansion, especially in cost-sensitive regions.

Opportunity Analysis - Expansion in Asia Pacific Energy Markets

Asia Pacific presents a significant growth opportunity due to rising energy demand and increasing domestic production initiatives. Countries such as China and India are investing heavily in upstream exploration to reduce import dependency. Offshore gas developments and onshore unconventional resource exploration are driving cementing demand across the region. The combination of growing consumption and supportive government policies is expected to sustain long-term market expansion. Service providers that establish strong regional presence and localized supply chains will be well-positioned to capitalize on this growth.

Digitalization and Automation in Cementing Operations

Technological advancements are transforming cementing operations through automation and digital monitoring. Real-time data analytics, predictive maintenance, and automated execution systems are improving efficiency and reducing operational risks. These innovations enable better control over cement placement, enhance equipment reliability, and minimize downtime. As operators prioritize cost efficiency and performance optimization, digital cementing solutions are gaining traction. Companies investing in advanced technologies are likely to achieve competitive differentiation and higher market share.

Growth in CCUS and Mature Field Services

The increasing adoption of carbon capture and storage projects is creating new demand for specialized cementing solutions. These applications require cement systems that can withstand chemical exposure and maintain integrity over extended periods. In parallel, aging oilfields are driving demand for remedial cementing and well abandonment services. Operators are allocating more resources to maintain existing assets and meet regulatory requirements. This shift from exploration to lifecycle management is expanding the addressable market for cementing services.

Category-wise Analysis

Product Type Insights

Primary cementing dominates the market and is anticipated to account for approximately 68.7% of the market share over the forecast period. This segment forms the foundation of well construction, ensuring effective zonal isolation, structural integrity, and protection of groundwater resources. Every drilled well, whether onshore shale or offshore deepwater, requires primary cementing, making it a consistent and high-volume segment globally. Its dominance is reinforced by increasing drilling activity and the growing complexity of well architectures. For instance, in U.S. shale basins such as the Permian, multi-stage horizontal wells require precise primary cementing to support hydraulic fracturing operations. Similarly, offshore projects in Brazil’s pre-salt fields rely on advanced primary cementing systems to withstand high-pressure and temperature conditions. The segment benefits from scalability and repeatability, particularly in pad drilling environments.

Remedial cementing is anticipated to be the fastest-growing segment. Growth is driven by aging well infrastructure, stricter regulatory requirements, and increasing focus on well integrity management. This segment includes squeeze cementing, plug cementing, and corrective zonal isolation treatments. As global well inventories mature, operators are allocating more resources to maintenance and repair activities. For example, North Sea operators are investing heavily in plug-and-abandonment programs, while U.S. shale operators frequently perform remedial jobs to address casing leaks and cement bond failures. Carbon capture and storage (CCUS) projects require high-performance remedial cementing to ensure long-term containment of CO2. Compared to primary cementing, these services demand higher technical expertise, customized slurry design, and advanced diagnostics, positioning remedial cementing as a high-value, growth-oriented segment.

Well Type Insights

Oil wells are anticipated to remain the leading segment, accounting for approximately 54.8% of the market share in 2026. This dominance reflects the continued reliance on crude oil as a primary energy source across global markets. Oil well cementing plays a critical role in both exploration and production phases, ensuring well integrity and preventing fluid migration. The segment is supported by sustained investments in major oil-producing regions such as North America, the Middle East, and offshore Latin America. For example, large-scale developments in the Permian Basin and offshore Brazil require extensive cementing operations to support production efficiency and reservoir management. Enhanced oil recovery (EOR) projects often involve recompletion and cementing activities, further reinforcing demand in this segment.

Horizontal wells are anticipated to be the fastest-growing segment, driven by the rapid expansion of unconventional oil and gas resources. These wells require advanced cementing techniques to ensure effective zonal isolation across extended lateral sections, which can span several thousand feet. The increasing adoption of shale and tight gas extraction methods is significantly boosting demand for stage cementing, plug-and-perf systems, and high-performance cement formulations. For instance, in U.S. shale plays such as the Eagle Ford and Bakken, horizontal drilling has become the standard approach, requiring precise cement placement to support multi-stage hydraulic fracturing. Similarly, China’s shale gas development is accelerating the use of horizontal wells, further contributing to segment growth. As operators continue to prioritize production efficiency and recovery rates, horizontal drilling is expected to increase both the technical complexity and overall volume of cementing operations.

Regional Insights

North America Well Cementing Market Trends - Shale-Driven High-Intensity Drilling with Digital Cementing Adoption

North America dominates the market and is anticipated to hold approximately 43.9% of the global market share in 2026, driven by high drilling intensity, advanced oilfield infrastructure, and strong technological adoption. The U.S. leads the region with robust oil and gas production and widespread deployment of horizontal drilling and multi-well pad development, particularly in shale basins such as the Permian and Bakken. These developments significantly increase the frequency and complexity of cementing operations, reinforcing steady demand.

Recent industry developments further highlight regional strength. Companies such as Halliburton have introduced digital cementing solutions, including automated monitoring systems that improve job accuracy and reduce downtime. Similarly, Baker Hughes has secured integrated well construction contracts in the Gulf of Mexico, emphasizing bundled services that include cementing. SLB continues to deploy advanced cement evaluation technologies across North American operations. These innovations are improving efficiency and lowering operational risks. At the same time, strict regulatory oversight focused on groundwater protection and well integrity ensures consistent demand for high-quality cementing solutions, positioning North America as both a volume and technology leader.

Europe Well Cementing Market Trends - Decommissioning and CCUS-Focused Cementing in Regulated Offshore Markets

Europe represents a mature, compliance-driven market where growth is closely tied to regulatory frameworks and sustainability initiatives. Countries such as the U.K., Norway, and Germany play important roles in offshore operations and energy policy development. While exploration activity is relatively limited compared to other regions, demand for cementing services is sustained by well maintenance, decommissioning, and integrity management, particularly in the North Sea.

Recent developments illustrate this transition. Weatherford secured a multi-year integrated completions contract in Denmark, highlighting continued offshore activity in mature basins. In parallel, Baker Hughes has been actively involved in carbon capture and storage (CCUS) initiatives across Europe, deploying specialized cement systems designed for long-term CO2 containment. These developments align with the region’s broader energy transition goals, where decommissioning of aging wells and investment in carbon storage infrastructure are becoming key demand drivers. As a result, Europe is evolving from a traditional drilling market into a hub for advanced, regulation-driven cementing applications.

Asia Pacific Well Cementing Market Trends - Energy Security-Driven Drilling Expansion with Advanced Cementing Uptake

Asia Pacific is anticipated to be the fastest-growing regional market, supported by rising energy demand, increasing upstream investments, and strong government initiatives to enhance energy security. Major economies such as China, India, and Indonesia are expanding both onshore and offshore exploration activities, driving significant demand for cementing services. Offshore gas developments in Southeast Asia and unconventional resource projects in China are key growth contributors.

Recent developments reinforce the region’s momentum. SLB has secured offshore drilling and completions contracts in China and Indonesia, supporting complex well construction projects that require advanced cementing technologies. In India, national oil companies are increasing drilling activity to reduce import dependency, creating opportunities for both domestic and international service providers. Halliburton has also expanded its regional footprint by deploying digital cementing solutions tailored to high-volume onshore operations. These developments demonstrate how Asia Pacific is not only growing in volume but also adopting advanced technologies. Combined with cost advantages and expanding industrial capabilities, the region presents a strong growth opportunity for cementing service providers.

Competitive Landscape

The global well cementing market is moderately consolidated, with a few global players dominating high-value projects while regional companies compete in localized markets. Large service providers offer integrated solutions, combining drilling, completion, and cementing services. Smaller players focus on cost efficiency and regional expertise. Competition is based on technology, service quality, and operational efficiency. Key strategies include technology innovation, service integration, and expansion into emerging markets. Leading companies are focusing on digital solutions, high-performance materials, and lifecycle services to enhance competitiveness and capture long-term contracts.

Key Industry Developments:

- In November 2025, Halliburton launched its LOGIX™ unit vitality system, an AI-powered solution designed to monitor cementing equipment in real time, improve operational readiness, and reduce non-productive time, strengthening its digital cementing capabilities.

- In March 2026, Halliburton collaborated with ExxonMobil to achieve the world’s first fully closed-loop automated geological well placement in Guyana, advancing automation in well construction processes that directly support precision cementing applications.

Frequently Asked Questions

The global well cementing market is estimated to be valued at US$11.8 billion in 2026.

The well cementing market is projected to reach US$18.3 billion by 2033, driven by increasing drilling activity and well integrity requirements.

Key trends include rising horizontal drilling activity, growth in offshore and deepwater projects, increasing adoption of digital cementing technologies, and expanding applications in CCUS and well abandonment services.

Primary cementing is the leading segment, accounting for approximately 68.7% of the market share, due to its essential role in all well construction activities.

The well cementing market is expected to grow at a CAGR of 6.5% from 2026 to 2033.

Some of the major players with strong portfolios include Halliburton, SLB, Baker Hughes, Weatherford, and NOV.