- Oil & Gas

- Oil Condition Monitoring Services Market

Oil Condition Monitoring Services Market Size, Share, and Growth Forecast 2026 - 2033

Oil Condition Monitoring Services Market by Product Type (Turbines, Compressors, Engines, Gear Systems, Hydraulic Systems), Sampling Type (On-site, Off-site), End-User (Transportation: Road, Rail, Aviation; Oil and Gas; Industrial Manufacturing; Mining; Power Generation; Marine; Aerospace and Defense; Renewable Energy: Wind, Solar Thermal), and Regional Analysis for 2026 - 2033

Oil Condition Monitoring Services Market Size and Trend Analysis

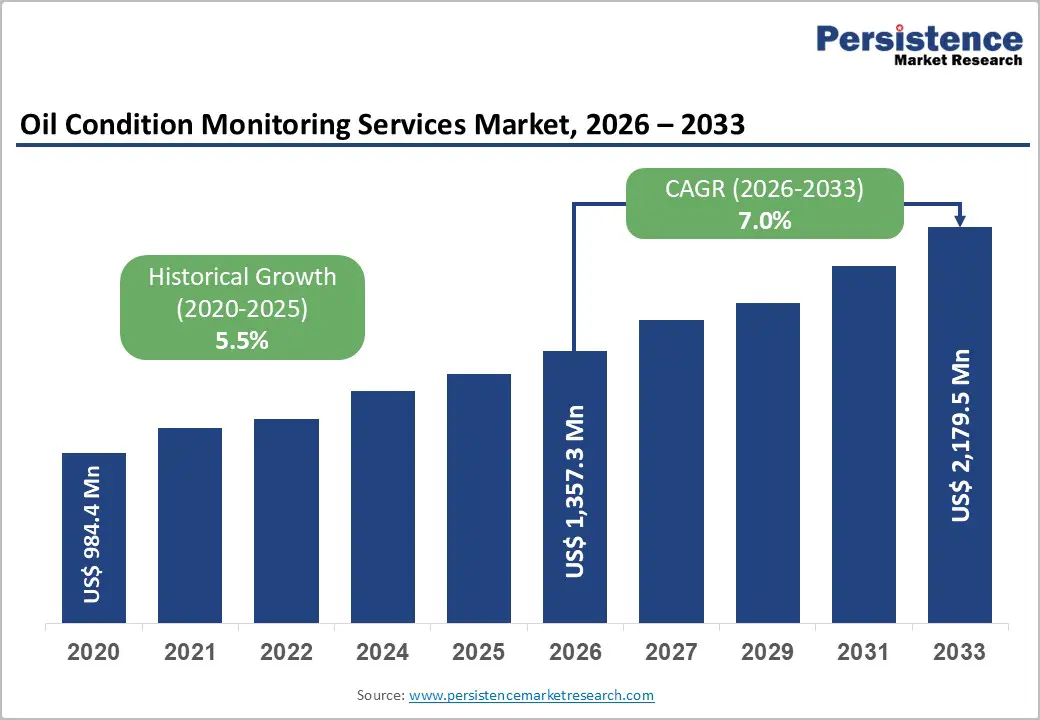

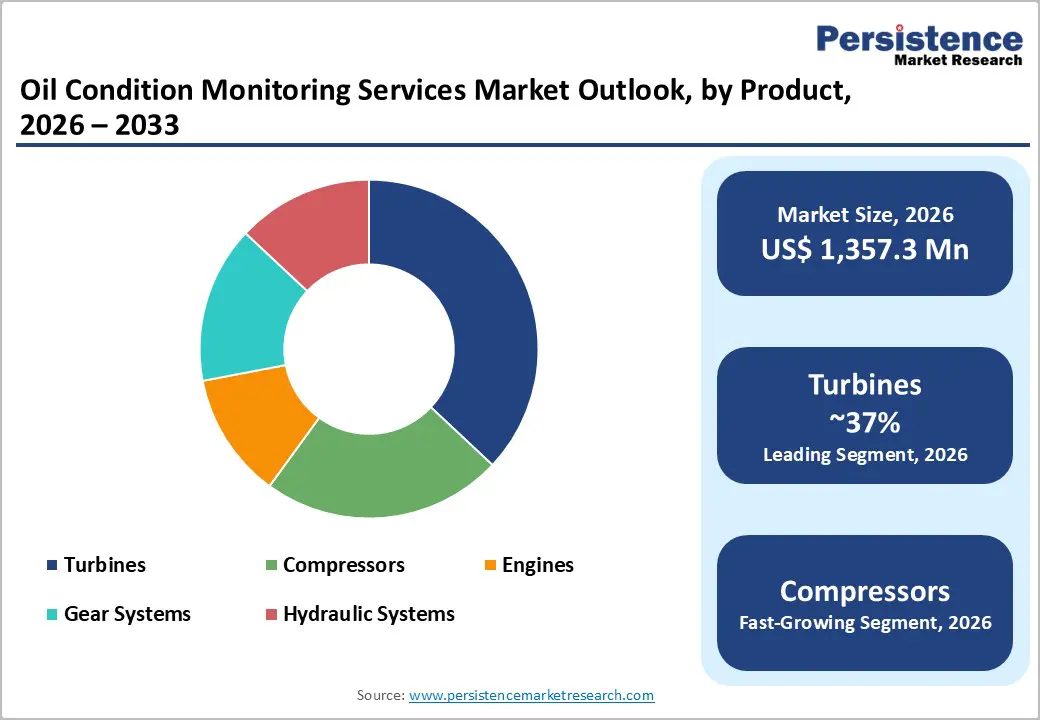

The global oil condition monitoring services market size is valued at US$ 1,357.3 Mn in 2026 and is projected to reach US$ 2,179.5 Mn by 2033, growing at a CAGR of 7.0% between 2026 and 2033.

The market's accelerating growth is primarily fueled by the rapid industrial adoption of predictive maintenance strategies, which leverage real-time lubricant diagnostics to prevent unplanned equipment failures and reduce operational costs alongside the integration of IoT-enabled sensors and AI-driven analytics platforms.

Key Market Highlights

- Leading Region: North America leads with the highest per-capita adoption of oil condition monitoring services, driven by the U.S. DoD's Joint Oil Analysis Program (JOAP), EPA waste oil regulations, and early-adopter predictive maintenance culture in energy and defense sectors.

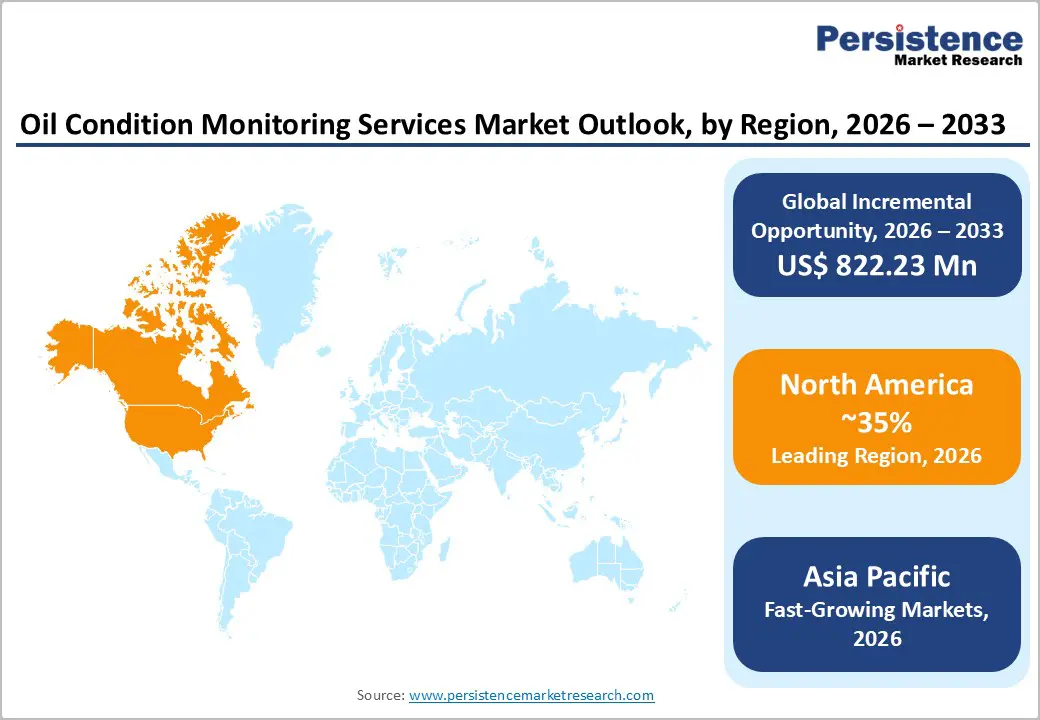

- Fastest Growing Region: Asia Pacific is both the largest and fastest growing region, holding approximately 50% market share in 2026, fueled by China's 3.2 million+ industrial enterprises, India's US$ 1.4 Tn National Infrastructure Pipeline, and Industry 4.0 digital maintenance initiatives.

- Dominant Segment: The Transportation end-user segment dominates with approximately 40% revenue share, driven by road fleet operators increasing oil monitoring adoption by 35% in 2025-2026 and mandatory aviation engine oil analysis under FAA and EASA maintenance regulations.

- Fastest Growing Segment: The Renewable Energy (Wind) end-user sub-segment is the fastest-growing application, driven by over 680 GW of new wind capacity additions projected between 2024 and 2028 (GWEC), each turbine requiring mandatory gearbox oil analysis to prevent failures costing €250,000-€400,000 per incident.

- Key Market Opportunity: AI-powered cloud-based digital oil analysis platforms (Monitoring-as-a-Service) and dedicated wind turbine gearbox monitoring programs represent the two highest-growth commercial opportunities, supported by developments such as Tan Delta Systems' SENSE-2 and Rexnord PMC's Smart Condition Monitoring System 1030.

| Key Insights | Details |

|---|---|

| Oil Condition Monitoring Services Market Size (2026E) | US$ 1,357.3 Mn |

| Market Value Forecast (2033F) | US$ 2,179.5 Mn |

| Projected Growth CAGR (2026 - 2033) | 7.0% |

| Historical Market Growth (2020 - 2025) | 5.5% |

Market Dynamics

Drivers - Accelerating Industry 4.0 Adoption and IoT-Enabled Predictive Maintenance

The global transition to Industry 4.0 manufacturing paradigms is fundamentally reshaping maintenance strategies across asset-intensive industries, and oil condition monitoring services are a direct beneficiary of this structural shift. The adoption of Industrial Internet of Things (IIoT) sensor networks enabling continuous, real-time lubricant diagnostics including viscosity, contamination, oxidation, and wear particle measurement is replacing scheduled oil sampling intervals with data-driven condition-based maintenance protocols. Industry data indicates that IoT-enabled sensor-based continuous oil monitoring adoption rose by approximately 29% between 2023 and 2025. The predictive maintenance market, which encompasses oil condition monitoring as a core component, is projected to reach US$ 12.3 Bn by 2025 at a CAGR of 28.1%. In April 2024, Parker Hannifin Corporation launched a new IoT-enabled oil condition monitoring sensor system, reinforcing the accelerating pace of embedded real-time diagnostics integration across industrial equipment fleets globally.

Stringent Environmental Regulations Driving Mandatory Lubricant Compliance Programs

Growing regulatory pressure from environmental and safety authorities worldwide is compelling asset operators across oil and gas, transportation, and industrial manufacturing to implement formalized oil condition monitoring programs to ensure regulatory compliance. The U.S. Environmental Protection Agency (EPA) has explicitly noted that improper oil disposal can cause significant environmental damage, mandating lubricant management practices that require continuous condition assessment to identify when oil requires disposal or recycling. In the European Union, the EU Methane Emissions Reduction Regulation that entered force in 2024 institutionalizes facility-wide leak detection and equipment performance monitoring programs across oil and gas assets, creating new compliance-driven demand for certified oil analysis services.

Restraints - High Initial Implementation Costs and Technical Complexity of Advanced Monitoring Systems

Despite strong demand momentum, the high capital expenditure required to deploy sophisticated oil condition monitoring systems encompassing sensors, data acquisition hardware, connectivity infrastructure, and analytical software platforms remains a significant barrier for small-to-medium enterprises and operators in developing economies. Advanced on-site monitoring platforms can carry implementation costs of US$ 50,000 to US$ 250,000 per installation for industrial facilities, creating a return-on-investment calculation that is difficult to justify for operators with limited asset portfolios or lower-margin operations. The technical complexity of interpreting multi-parameter lubricant diagnostics requiring specialized expertise in tribology, ferrography, and spectral analysis further constrains market penetration among end-users without dedicated maintenance engineering resources, limiting adoption beyond tier-1 industrial operators.

Lack of Standardization Across Monitoring Protocols and Diagnostic Parameters

A significant structural challenge impeding broader adoption of oil condition monitoring services is the absence of universally standardized testing protocols, diagnostic thresholds, and condition alarm criteria across different equipment types, lubricant grades, and industry verticals. The ASTM International and ISO Technical Committee 28 maintain lubricant testing standards, but the translation of laboratory test results into actionable maintenance decisions remains inconsistent across service providers. This lack of standardization reduces confidence in third-party laboratory reports among end-users, creates interoperability barriers for integrated monitoring platforms, and complicates benchmarking of oil condition data across multi-site industrial operations collectively limiting the pace at which organizations scale oil condition monitoring from pilot programs to enterprise-wide deployment.

Opportunities - Renewable Energy Wind Turbine Gearbox Monitoring as a High-Growth End-Market

The rapid global expansion of onshore and offshore wind power generation is creating a substantial new demand stream for oil condition monitoring services specifically targeting wind turbine gearbox lubricants technically demanding and commercially high-value application. Wind turbine gearboxes operate under highly variable load conditions, with lubricant degradation accelerated by contamination from metallic wear particles, water ingress from marine environments, and thermal cycling. Gearbox failure in offshore wind turbines can cost between €250,000 and €400,000 per incident, including crane mobilization and component replacement. Globally installed wind capacity reached approximately 1,100 GW by the end of 2023, according to the International Energy Agency (IEA), with the Global Wind Energy Council (GWEC) projecting additions of over 680 GW between 2024 and 2028.

AI-Powered Digital Oil Analysis Platforms and Cloud-Based Monitoring as a Service

The convergence of artificial intelligence (AI), machine learning, and cloud computing with traditional oil condition monitoring laboratory workflows is creating a transformative commercial opportunity for monitoring-as-a-service (MaaS) business models that deliver predictive lubricant diagnostics through subscription-based digital platforms. By embedding AI algorithms trained on decades of historical lubricant test data, these platforms can correlate viscosity degradation, wear particle profiles, and contamination markers with specific failure modes, generating automated maintenance recommendations without requiring on-site tribology expertise. In February 2024, Tan Delta Systems launched its SENSE-2 oil condition monitoring kit, providing continuous real-time oil quality data to optimize maintenance schedules and reduce operating costs.

Category-wise Analysis

Product Type Insights

The Turbines segment leads the oil condition monitoring services market's product type category, accounting for approximately 37% of total market revenue. Turbines, including gas turbines in power generation, steam turbines in industrial facilities, and wind turbine gearboxes, are among the highest-value, most failure-sensitive rotating assets in operation globally, making oil condition monitoring a critical maintenance investment. Turbine lubricant degradation, contamination, or the presence of wear metals serves as an early warning of bearing or seal failures that can result in unplanned outages costing operators hundreds of thousands of dollars per incident. The IEA reports that power generation turbines represent one of the most asset-intensive equipment categories globally.

Sampling Type Analysis

The Off-site sampling segment currently holds the dominant position in the oil condition monitoring services market by sampling type, representing approximately 59% of total revenue. Off-site laboratory analysis, which involves collecting lubricant samples from equipment and transporting them to certified testing laboratories for comprehensive multi-parameter analysis, has established its leadership by virtue of the depth and accuracy of diagnostic data it provides. Accredited off-site laboratories equipped with inductively coupled plasma (ICP) spectrometers, ferrographic analyzers, and FTIR spectrometers can identify wear metals at parts-per-billion concentrations, a resolution impossible to replicate with on-site sensors.

End-user Insights

The Transportation end-user segment, encompassing road, rail, and aviation, is the dominant end-use application in the oil condition monitoring services market, commanding approximately 40% of total market revenue. Fleet operators for road transport (trucks, buses, and commercial vehicles), rail operators, and aviation maintenance organizations are among the most systematic and high-frequency consumers of oil analysis services globally. Between 2024 and 2025, fleet operators increased their use of oil condition monitoring services by approximately 35% as maintenance strategies shifted toward predictive schedules, reducing unscheduled maintenance and associated downtime costs. For aviation specifically, both FAA (Federal Aviation Administration) and EASA (European Union Aviation Safety Agency) regulations mandate regular oil analysis as part of engine health monitoring programs for commercial aircraft, creating a compliance-driven, recurring revenue base that is structurally independent of economic cycles and provides oil condition monitoring service providers with predictable, multi-year demand from aviation customers.

Regional Insights

North America Oil Condition Monitoring Services Market Trends

North America holds the largest regional market share in oil condition monitoring services, driven by its concentration of asset-intensive industries including oil and gas extraction, power generation, defense, and aviation all of which operate under stringent regulatory frameworks mandating systematic equipment health monitoring. The U.S. market alone accounted for approximately US$ 251.61 Mn in 2025, reflecting early and widespread adoption of predictive maintenance protocols across transportation, energy, and industrial sectors.

The region's innovation ecosystem is a defining competitive advantage. Parker Hannifin Corporation launched its advanced IoT-enabled oil condition monitoring system in April 2024, while Rexnord PMC's Smart Condition Monitoring System 1030 (June 2024) introduced multi-parameter gear drive monitoring combining oil quality, vibration, and temperature diagnostics. The U.S. Department of Defense (DoD) mandates oil analysis programs for military aircraft, ground vehicles, and naval vessels under Joint Oil Analysis Program (JOAP) standards, providing a structurally stable government procurement channel that insulates the North American market from broader economic downturns.

Europe Oil Condition Monitoring Services Market Trends

Europe represents the second-largest regional market for oil condition monitoring services, underpinned by rigorous regulatory standards, a mature industrial manufacturing base, and rapidly expanding renewable energy infrastructure requiring turbine lubricant monitoring. Germany, the United Kingdom, and France are the three dominant national demand centres, driven by their aerospace, automotive, and heavy engineering sectors.

Europe's offshore wind expansion, with a 300 GW target by 2050 and over 32 GW installed capacity in 2023, is generating substantial incremental demand for wind turbine gearbox oil monitoring services across the North Sea, Baltic Sea, and Atlantic offshore wind zones. Bureau Veritas, headquartered in France, operates one of Europe's most comprehensive oil and gas laboratory networks accredited under ISO 9001, ISO 14001, and ISO/IEC 17025 at every major shipping port and petroleum terminal hub.

Asia Pacific Oil Condition Monitoring Services Market Trends

Asia Pacific is both the largest regional market by volume share, accounting for approximately 50% of global oil condition monitoring market revenue in 2026, and the fastest-growing region, driven by the rapid industrialization of China, India, and Southeast Asia. China's manufacturing sector, which encompasses over 3.2 million industrial enterprises according to the National Bureau of Statistics of China (NBS), represents an enormous installed base of turbines, compressors, hydraulic systems, and gear drives requiring systematic lubricant monitoring.

Japan, South Korea, and Australia are mature sub-markets within Asia Pacific, characterized by high predictive maintenance adoption in precision manufacturing, mining, and energy sectors. ASEAN nations, including Indonesia, Thailand, and Malaysia, are emerging demand centres, with expanding automotive manufacturing clusters and oil and gas upstream operations creating growing needs for engine and hydraulic system oil monitoring services.

Competitive Landscape

The global oil condition monitoring services market is moderately fragmented, with a two-tier structure comprising large multinational Testing, Inspection, and Certification (TIC) firms, including Bureau Veritas, SGS SA, Intertek Group plc, and Element Materials Technology, and a broad base of specialized regional oil analysis laboratories. The top five players account for approximately 40% of global revenue. Market leaders differentiate through ISO/IEC 17025-accredited global laboratory networks, multi-parameter analytical instrumentation, digital reporting platforms, and integrated LIMS (Laboratory Information Management Systems).

Key Developments:

- In March 2025, Cambridge Applied Systems launched the SPL571 viscometer for real-time oil viscosity monitoring, enabling dashboard-based condition assessment that captures transient chemistry changes impossible to detect through traditional sampling methods. The technology is being tested by major engine manufacturers and offers significant advantages in reducing new model development times while improving oil change recommendation accuracy.

- In January 2025, Kongsberg Digital expanded its digital twin platform capabilities for midstream oil and gas operations, introducing enhanced real-time monitoring and predictive analytics features that create integrated data management solutions for pipeline operators. The platform integrates 12,000 data points per facility to enable single-operator management of complex industrial installations.

Companies Covered in Oil Condition Monitoring Services Market

- Bureau Veritas SA

- Condition Monitoring Services, Inc.

- Eastway Services

- Element Materials Technology

- Exxon Mobil Corporation

- Intertek Group plc

- SGS SA

- Shell plc

- Veritas Petroleum Services

- Vickers Oils

Frequently Asked Questions

The global Oil Condition Monitoring Services market is valued at US$ 1,357.3 Mn in 2026 and is projected to reach US$ 2,179.5 Mn by 2033, growing at a CAGR of 7.0%.

The primary demand drivers include, the global adoption of Industry 4.0 and IIoT-enabled predictive maintenance, with IoT-enabled oil monitoring adoption rising by approximately 29% between 2023 and 2025, and regulatory compliance requirements from U.S. EPA, FAA, EASA, and the EU Methane Regulation (2024) mandating oil monitoring; and

The Transportation end-user segment (Road, Rail, Aviation) dominates with approximately 40% of total market revenue. Fleet operators increased oil monitoring adoption by approximately 35% in 2025-2026.

North America holds the largest revenue share among mature markets due to early predictive maintenance adoption, the U.S. DoD's Joint Oil Analysis Program (JOAP), and EPA compliance mandates. Asia Pacific is simultaneously the largest volume market (approximately 50% global share in 2024) and the fastest-growing region, driven by China's massive industrial base of over 3.2 million industrial enterprises and India's US$ 1.4 Tn National Infrastructure Pipeline.

The key market participants include Bureau Veritas SA (France), SGS SA (Switzerland), Intertek Group plc (U.K.), Element Materials Technology (U.K.), Exxon Mobil Corporation (U.S.), Shell plc (U.K./Netherlands), Veritas Petroleum Services (Netherlands), Vickers Oils (U.K.), Condition Monitoring Services, Inc. (U.S.), and Eastway Services (U.K.), among others including emerging innovators Tan Delta Systems, Parker Hannifin, and ALS Limited.