- Automotive

- Off-highway Vehicle Market

Off-highway Vehicle Market Size, Share, and Growth Forecast 2026 - 2033

Off-highway Vehicle Market by Vehicle Type (Construction Vehicles, Agricultural Machinery, Mining Vehicles, Forestry Equipment, Others), by Propulsion Type (Diesel, Gasoline/Petrol, Electric/Hybrid), Power Output (Up to 100 HP, 100-200 HP, 200-400 HP, 400+ HP), by Distribution Channel (Dealers & Distributors, Rental & Leasing, Direct/OEM Sales, Online/E-commerce), End-user, and Regional Analysis, 2026 - 2033

Off-highway Vehicle Market Size and Trend Analysis

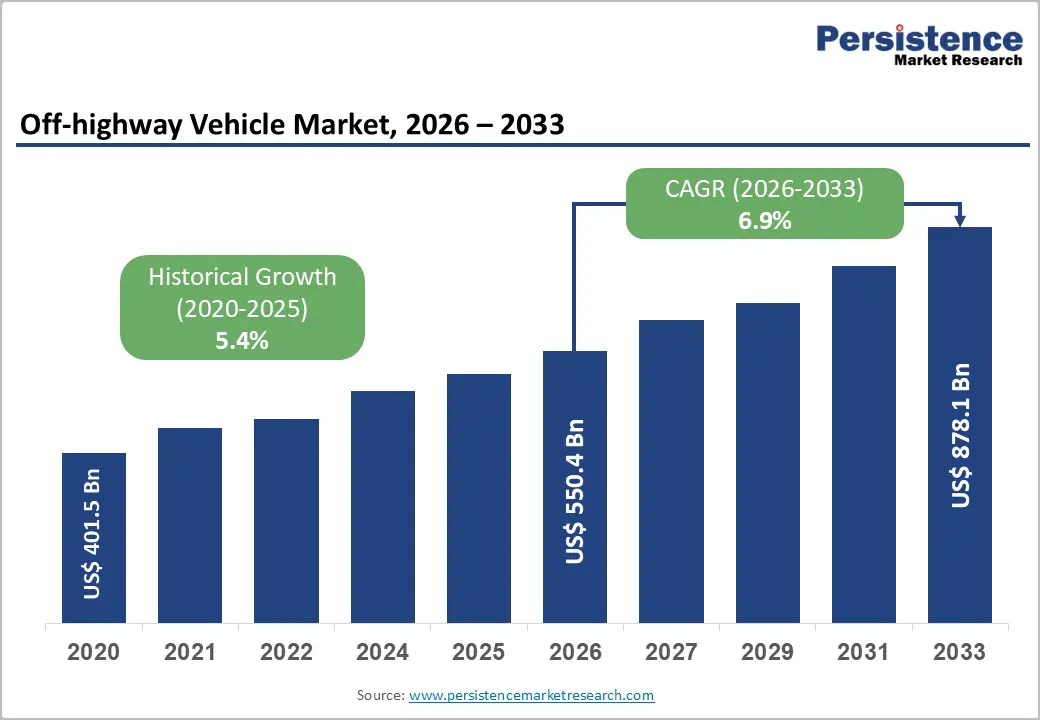

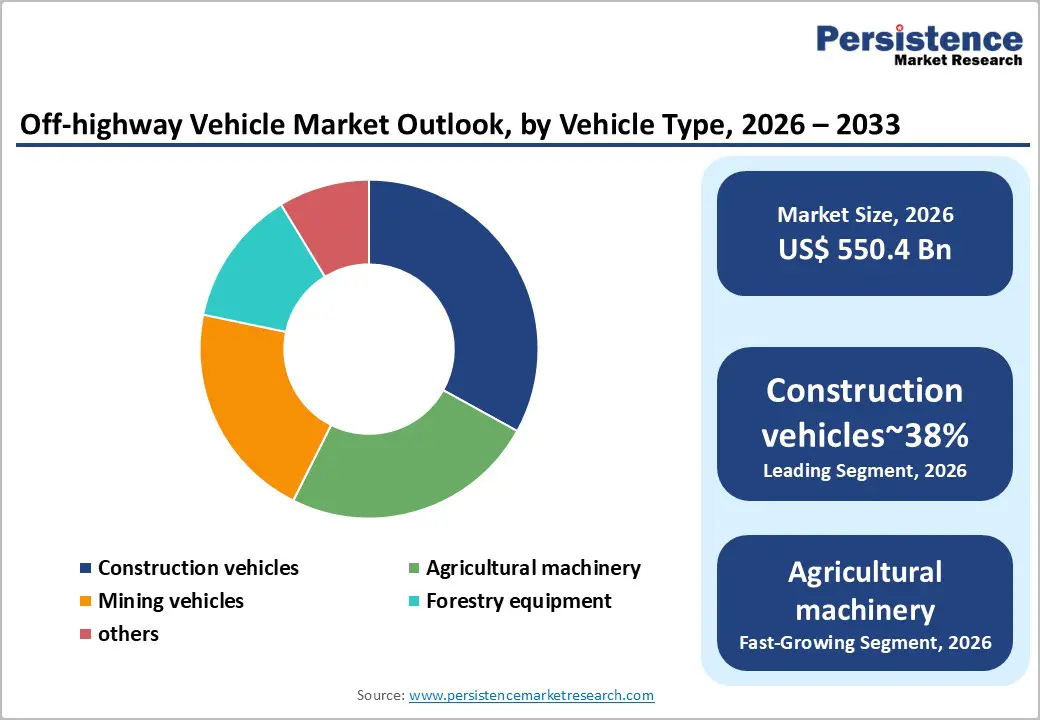

The global off-highway vehicle market size is likely to be valued at US$ 550.4 Billion in 2026 and is expected to reach US$ 878.1 Billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033.

The market's robust trajectory is fundamentally driven by escalating global infrastructure investment, accelerating agricultural mechanization across emerging economies, and a rapidly expanding mining sector.

Key Industry Highlights:

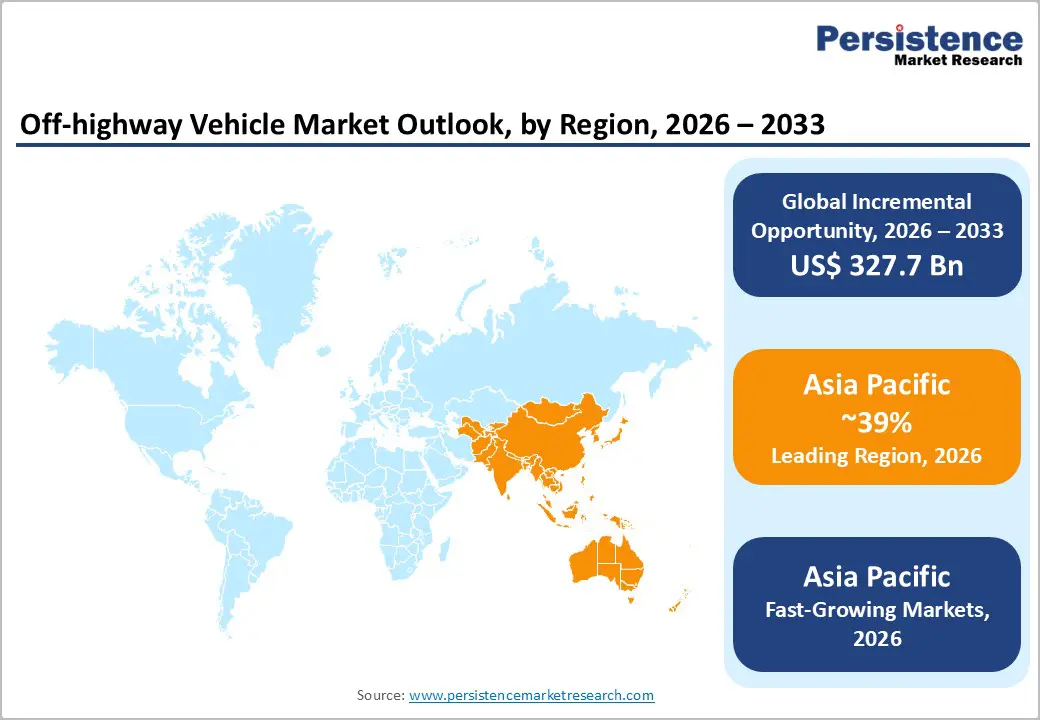

- Leading Region: Asia Pacific leads the global off-highway vehicle market holding 39% share, driven by China's infrastructure megaprojects, India's PM Gati Shakti initiative, and ASEAN's accelerating industrial build-out, collectively making it the dominant revenue-generating region.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region with rising CAGR of 8.3%, propelled by surging agricultural mechanization in India and Vietnam, urban construction expansion, and competitive local manufacturing by XCMG Group and SANY Group.

- Leading Segment: Construction vehicles represent the dominant segment by vehicle type with approximately 38% market share, supported by multi-trillion-dollar global infrastructure programs under the IIJA, EU Cohesion Fund, and China's 14th Five-Year Plan.

- Fastest-Growing Segment: Electric and hybrid propulsion is the fastest-growing propulsion segment, driven by EU Stage V NRMM regulatory revisions, corporate net-zero pledges, and rapidly improving battery energy density, making electric off-highway equipment commercially viable.

- Key Opportunity: Electrification of heavy equipment fleets and integration of autonomous haulage systems in mining represent the most compelling market opportunities, as operators globally pursue zero-emission targets and AI-driven productivity improvements through smart fleet management.

| Key Insights | Details |

|---|---|

| Off-highway Vehicle Market Size (2026E) | US$ 550.4 Billion |

| Market Value Forecast (2033F) | US$ 878.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 5.4% |

Market Dynamics

Drivers - Unprecedented Global Infrastructure Investment Fueling Equipment Demand

Global infrastructure investment has reached historic levels, creating strong and sustained demand across all categories of off-highway construction equipment. The Infrastructure Investment and Jobs Act (IIJA) in the United States has committed approximately US$ 1.2 trillion toward roads, bridges, airports, railways, and utilities, and this large-scale program is expected to support construction equipment demand well into the early 2030s. According to the Global Infrastructure Hub, global infrastructure investment needs are projected to reach nearly US$ 94 trillion by 2040, with an estimated annual funding gap of about US$ 15 trillion.

Meanwhile, China’s 14th Five-Year Plan has allocated significant funding for transportation, water management, and energy infrastructure projects. Similarly, India’s PM Gati Shakti National Master Plan is integrating multimodal infrastructure projects such as highways, ports, and logistics corridors. The International Road Federation reports that global road construction spending has been growing at approximately 4-5% annually, directly increasing the use of excavators, graders, compactors, and loaders across construction sites worldwide.

Agricultural Mechanization Surge Across Developing Economies

Agricultural mechanization is rapidly accelerating across developing economies, driven by government initiatives, rising farm labor costs, and increasing food security concerns. The Food and Agriculture Organization estimates that mechanization levels in regions such as sub-Saharan Africa and South Asia remain below 30%, highlighting a large untapped opportunity for tractors, combine harvesters, and other modern farming equipment. In India, the Sub-Mission on Agricultural Mechanization (SMAM) has provided financial support to millions of smallholder farmers to adopt mechanized equipment.

According to the Tractors and Mechanization Association, India records annual tractor sales of over 900,000 units, making it one of the world’s largest tractor markets. In Southeast Asia, governments in countries such as Vietnam and Indonesia are actively encouraging mechanization to reduce post-harvest losses and improve farm productivity. This ongoing transition from manual labor to machine-driven farming practices is expected to remain a long-term growth driver for the off-highway agricultural machinery market.

Restraints - Rise in Compliance Costs from Tightening Emission Regulations

Strict emission regulations worldwide are significantly increasing manufacturing and compliance costs for off-highway vehicle manufacturers. Standards such as the EPA Tier 4 Final introduced by the United States Environmental Protection Agency and the European Union Stage V emission standard represent some of the most stringent non-road emission rules ever implemented. These regulations require the integration of advanced after-treatment technologies such as selective catalytic reduction (SCR), diesel particulate filters (DPF), and exhaust gas recirculation (EGR) systems.

As a result, equipment manufacturers often experience cost increases of 15-20% per unit, placing pressure on pricing strategies and reducing affordability for smaller fleet operators. In addition, different regions follow different regulatory timelines and technical requirements, which makes it more challenging for global OEMs to standardize product designs. This fragmentation increases engineering complexity and supply chain costs, forcing manufacturers to invest more heavily in compliance management and product adaptation.

High Capital Expenditure and Extended Asset Lifecycle Limiting Fleet Renewal

Off-highway vehicles are among the most expensive capital assets used in industrial operations, making fleet upgrades financially challenging for many operators. Heavy mining haul trucks and large hydraulic excavators can cost between US$ 500,000 and US$ 5 million per unit, while even mid-range agricultural machinery typically ranges from US$ 150,000 to US$ 400,000. These high acquisition costs often discourage frequent equipment replacement, especially for small and medium-sized operators. Furthermore, most off-highway vehicles have long operational lifecycles of approximately 10-15 years, which naturally slows fleet renewal cycles.

This trend is particularly evident in mature markets such as North America and Western Europe. In the mining industry, fluctuations in commodity prices also influence purchasing decisions. During periods of low commodity prices, companies typically delay capital expenditure for two to four years, resulting in temporary demand slowdowns that directly affect equipment sales and overall market growth.

Opportunities - Electrification of Off-highway Equipment, Transformative Long-Term Growth Potential

The electrification of off-highway vehicles is gradually shifting from experimental development to commercial deployment, opening significant long-term growth opportunities for equipment manufacturers. Policy initiatives such as the Fit for 55 package introduced by the European Commission are expected to accelerate the adoption of zero-emission equipment in urban construction zones across the European Union by the early 2030s. Leading equipment manufacturers are already investing heavily in this transition.

Caterpillar Inc. has announced plans to expand its portfolio of electric and hybrid machinery. Similarly, Volvo Construction Equipment has successfully launched fully electric compact excavators and wheel loaders that are gaining popularity among European contractors. Continuous improvements in battery technology, including higher energy density and faster charging capabilities, are also helping reduce total operating costs. As construction and mining companies pursue net-zero carbon targets by 2050, many are actively evaluating opportunities to electrify their equipment fleets, creating a significant replacement cycle in the coming decade.

Autonomous and Connected Equipment in Smart Mining Operations

The adoption of autonomous technology, telematics, and artificial intelligence in off-highway vehicles is creating a major opportunity, particularly within the mining industry. Advanced automation systems enable equipment to operate with minimal human intervention while improving productivity, safety, and operational efficiency. For instance, Rio Tinto operates one of the world’s largest autonomous haul truck fleets at its Pilbara iron ore mines in Western Australia, reporting productivity gains of more than 15% compared with conventional human-operated vehicles.

Similarly, Komatsu Ltd. has successfully commercialized its FrontRunner autonomous haulage system, which is now deployed across several global mining operations. Equipment manufacturer Epiroc AB is also investing heavily in automated drilling and rock-reinforcement machinery. As the global mining industry moves toward digitalization and smart mine development, operators are increasingly integrating sensors, GPS machine control systems, and IoT connectivity into their fleets. Rising labor costs and stricter safety regulations are further strengthening the economic case for autonomous equipment adoption.

Category-wise Analysis

By Vehicle Type Insights

Construction vehicles hold the leading position in the off-highway vehicle market, accounting for approximately 38% of the total market share. This strong dominance is primarily driven by the rapid expansion of infrastructure development projects worldwide. Excavators, which are among the most versatile and widely used construction machines, play a crucial role in activities such as road construction, trenching for utilities, building foundation preparation, and demolition work.

According to the Committee for European Construction Equipment, construction equipment orders in Europe increased by more than 8% during a recent reporting period, reflecting strong post-pandemic recovery across the sector. Meanwhile, large-scale urban development initiatives in China and India, including smart city programs, affordable housing schemes, and transportation network expansion projects, continue to generate high demand for loaders, cranes, and graders. The wide range of applications for construction vehicles across multiple industries and regions ensures that this segment will maintain its leadership position throughout the forecast period.

By Propulsion Type Insights

Diesel-powered off-highway vehicles dominate the propulsion type segment, accounting for roughly 68% of the total market share. Diesel engines remain the preferred option for heavy-duty applications because of their high torque output, superior fuel energy density, and proven reliability in demanding operating environments. According to the International Energy Agency, diesel engines continue to power the majority of agricultural and construction equipment worldwide, especially in regions where electrical grid infrastructure is limited or unreliable.

In large-scale machinery such as rigid dump trucks used in open-pit mining or combine harvesters operating in remote agricultural areas, diesel fuel provides a clear advantage in terms of operational endurance and energy efficiency. While electric and hybrid propulsion technologies are gaining traction and represent the fastest-growing segment, diesel engines are expected to remain the dominant power source for heavy-duty off-highway equipment until at least 2030 due to their unmatched performance in demanding field conditions.

By Power Output Insights

The 200-400 horsepower power output segment represents the leading category within the off-highway vehicle market, accounting for approximately 34% of total market share. This power range includes a wide variety of versatile mid- to heavy-duty machinery such as large agricultural tractors, mid-sized hydraulic excavators, wheel loaders, and surface mining support vehicles. These machines provide the ideal balance between operational capability, efficiency, and overall cost of ownership, making them highly preferred across multiple industries.

In developed markets such as North America and Europe, commercial-scale farming operations commonly rely on tractors within the 200-350 HP range to handle large-scale field operations efficiently. According to the Association of Equipment Manufacturers, this power category consistently records the highest shipment volumes among all off-highway equipment segments. Additionally, infrastructure construction projects worldwide frequently depend on machines within this power band for tasks such as earthmoving, grading, and large-scale material handling operations.

By Distribution Channel Insights

Dealers and distributors remain the dominant sales channel in the off-highway vehicle market, accounting for nearly 48% of total distribution share. This channel plays a critical role because purchasing off-highway equipment typically involves complex technical evaluations, financing arrangements, warranty management, and long-term service agreements. Localized dealer networks help customers select equipment specifications, provide product demonstrations, and offer maintenance services throughout the equipment lifecycle.

Leading manufacturers such as Caterpillar Inc., Komatsu Ltd., and Deere & Company operate extensive global dealer networks that span hundreds of countries, ensuring strong after-sales support and customer engagement. Dealers also assist with fleet management consulting, trade-in evaluations, and spare parts supply. Meanwhile, the rental and leasing channel is emerging as the fastest-growing distribution model, particularly in North America and Europe, where contractors increasingly prefer flexible equipment access rather than investing in high-cost asset ownership.

By End-user Insights

Construction and infrastructure development represent the largest end-use segment in the off-highway vehicle market, accounting for approximately 36% of total demand. This dominance is driven by massive infrastructure investments being implemented across multiple regions of the world. Major government initiatives such as the Infrastructure Investment and Jobs Act in the United States, infrastructure funding programs under the European Union Cohesion Fund, and development initiatives included in China’s 14th Five-Year Plan have collectively mobilized trillions of dollars for construction projects.

According to the Global Infrastructure Hub, global infrastructure investment requirements could reach US$ 94 trillion by 2040. Large-scale projects including road construction, metro rail expansion, port modernization, airport upgrades, and large residential housing developments are creating continuous demand for excavators, bulldozers, compactors, and aerial work platforms. The scale, geographic reach, and long-term nature of infrastructure investments ensure that construction will remain the primary demand driver in this market.

Regional Insights

North America Off-highway Vehicle Market Trends

North America is one of the leading global markets for off-highway vehicles, with the United States accounting for the majority of regional revenue. A major factor driving equipment demand is the Infrastructure Investment and Jobs Act, which allocates about US$ 1.2 trillion over the next decade for infrastructure development. This funding supports projects such as interstate highway reconstruction, bridge rehabilitation, EV charging infrastructure, and broadband network expansion. These initiatives are increasing the need for advanced construction equipment across the region.

Major manufacturers like Deere & Company and Caterpillar Inc. are investing heavily in next-generation telematics systems and autonomous machinery designed specifically for North American operating conditions. In Canada, the mining sector, particularly oil sands and base metals operations, continues to drive demand for haul trucks, loaders, and drilling equipment. Meanwhile, Mexico’s infrastructure programs and expanding agribusiness sector are also supporting equipment sales. Environmental regulations such as EPA Tier 4 Final and California Air Resources Board emission standards are encouraging fleet modernization toward cleaner and electric equipment, creating a strong replacement cycle across the region.

Europe Off-highway Vehicle Market Trends

Europe’s off-highway vehicle market is shaped by two major forces: strict environmental regulations and ongoing infrastructure development. Key markets in the region include Germany, France, the United Kingdom, and Spain, which together account for a significant share of equipment demand. The EU Stage V non-road emission standard, fully implemented in 2019, has accelerated the replacement of older machinery with cleaner and more efficient equipment. According to Committee for European Construction Equipment, demand for Stage V-compliant machinery continues to grow as contractors upgrade their fleets.

Large infrastructure initiatives such as the Trans-European Transport Network and funding from the EU Cohesion Fund are supporting the expansion of roads, railways, and waterways across Central and Eastern Europe. Leading manufacturers including Volvo Construction Equipment, Liebherr Group, and JCB are introducing electric and hybrid machines to meet Europe’s strict emission targets. Initiatives such as the European Green Deal and REPowerEU are further encouraging electrification of non-road machinery. Major projects like Spain’s high-speed rail expansion and the U.K.’s HS2 railway project continue to support demand for heavy earthmoving equipment.

Asia Pacific Off-highway Vehicle Market Trends

Asia Pacific represents the largest and fastest-growing regional market for off-highway vehicles worldwide. China remains the dominant market, supported by large-scale infrastructure development, urban housing projects, and energy investments under the 14th Five-Year Plan. Domestic manufacturers such as XCMG Group and SANY Group have strengthened their global presence by offering cost-competitive equipment and expanding exports to Africa, Latin America, and Southeast Asia.

India is emerging as one of the region’s fastest-growing markets, supported by national infrastructure initiatives such as PM Gati Shakti National Master Plan, Bharatmala Pariyojana, and AMRUT 2.0, which focus on highways, logistics networks, and urban infrastructure. Japan continues to play a major role as a high-value exporter of construction equipment, with companies such as Komatsu Ltd. and Hitachi Construction Machinery Co., Ltd. reporting strong export performance through the Japan Construction Equipment Manufacturers Association. At the same time, ASEAN economies including Indonesia, Vietnam, and Thailand are increasing investments in road, port, and energy infrastructure, further expanding regional demand.

Competitive Landscape

The global off-highway vehicle market has a moderately consolidated competitive structure, with the top ten companies accounting for nearly 55-60% of total market revenue. Industry leaders such as Caterpillar Inc., Komatsu Ltd., and Deere & Company maintain strong positions through broad product portfolios, extensive global dealer networks, and continuous investment in research and development. These companies are increasingly focusing on electrification, automation, and digital equipment management to improve machine efficiency and productivity. Smart equipment integration, predictive maintenance solutions, and connected telematics platforms are becoming key differentiators in the competitive landscape.

In addition, aftermarket services such as parts, maintenance, and equipment upgrades are becoming an important revenue stream for manufacturers. Mergers and acquisitions are also increasing as large OEMs acquire technology startups to accelerate the development of autonomous systems and advanced telematics capabilities. Meanwhile, Chinese manufacturers like XCMG Group and SANY Group are expanding rapidly through competitive pricing strategies and strong distribution networks in emerging markets, creating increasing pressure on Western manufacturers, particularly in mid-range equipment segments.

Key Developments:

- In March 2025: Caterpillar Inc. unveiled its next-generation battery-electric excavator and wheel loader lineup at CONEXPO-CON/AGG in Las Vegas. The machines feature extended operating range and fast-charging compatibility, supporting large construction projects while reducing emissions and improving jobsite energy efficiency.

- In September 2024: Volvo Construction Equipment partnered with Northvolt to develop high-density battery packs designed for electric wheel loaders and excavators. The collaboration focuses on improving battery durability and performance in demanding Nordic and Alpine climate conditions.

- In January 2024: Komatsu Ltd. completed a commercial pilot of autonomous mining haul trucks at a copper mine in Chile, achieving a 17% improvement in haulage cycle efficiency while also reducing safety incidents compared with conventional human-operated mining fleets.

Companies Covered in Off-highway Vehicle Market

- Caterpillar Inc.

- Komatsu Ltd.

- Deere & Company

- CNH Industrial N.V.

- Hitachi Construction Machinery Co., Ltd.

- Liebherr Group

- Volvo Group

- XCMG Group

- Kubota Corporation

- SANY Group

- J C Bamford Excavators Ltd. (JCB)

- Doosan Corporation

- Sandvik AB

- Epiroc AB

- Terex Corporation

- AGCO Corporation

- Bobcat Company (Doosan Bobcat)

- Wirtgen Group

- Manitou Group

- Hyundai Construction Equipment Co., Ltd.

Frequently Asked Questions

The global Off-highway Vehicle Market is estimated to be valued at US$ 550.4 Billion in 2026 and is projected to reach US$ 878.1 Billion by 2033, expanding at a healthy CAGR of 6.9% over the forecast period.

The market is primarily driven by unprecedented global infrastructure investment, notably the U.S. Infrastructure Investment and Jobs Act (IIJA) committing US$ 1.2 trillion, alongside rapid agricultural mechanization in developing economies such as India, where annual tractor sales surpass 900,000 units, and expanding mining activities worldwide.

Construction vehicles dominate the market by vehicle type, holding approximately 38% of total market share. Their leadership is supported by multi-trillion-dollar infrastructure programs globally, with excavators, loaders, graders, and compactors deployed extensively across road, housing, and utilities construction projects.

Asia Pacific holds the largest regional share in the global Off-highway Vehicle Market, driven by China's massive infrastructure build-out under the 14th Five-Year Plan, India's PM Gati Shakti program, and growing construction and agricultural equipment demand across ASEAN nations.

Electrification of off-highway equipment and adoption of autonomous haulage systems in mining represent the most significant opportunities. Regulatory mandates from the European Commission's Fit for 55 package and corporate net-zero commitments are accelerating replacement of diesel fleets, while autonomous mining vehicles are delivering 15-17% productivity gains at commercial mine sites.

Leading companies operating in the global Off-highway Vehicle Market include Caterpillar Inc., Komatsu Ltd., Deere & Company, CNH Industrial N.V., Volvo Group, Liebherr Group, Hitachi Construction Machinery Co., Ltd., XCMG Group, SANY Group, Kubota Corporation, Epiroc AB, Sandvik AB, and J C Bamford Excavators Ltd. (JCB), among others.