- Automotive

- Car Rental Market

Car Rental Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Car Rental Market by Vehicle Type (Economy Cars, SUVs, Executive Cars, Luxury Cars, MUVs), Application (Local Usage, Airport Transport, Outstation, Others), Booking Mode (Online, Offline/Direct), and Region Analysis for 2026 to 2033

Car Rental Market Trends & Analysis

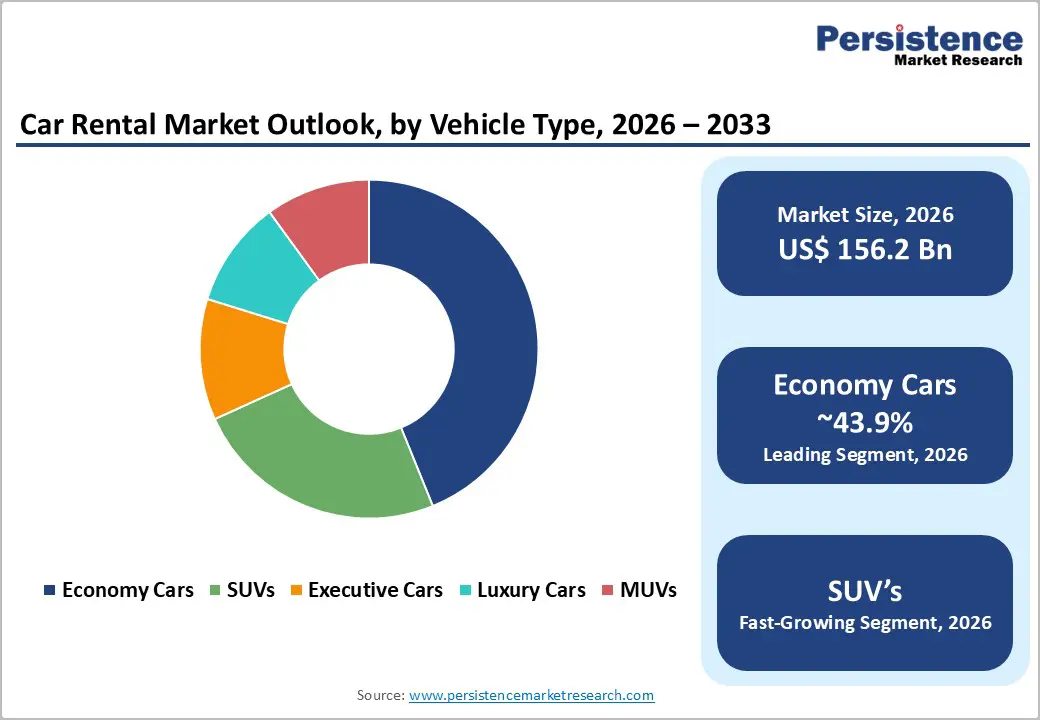

The global car rental market size is anticipated at US$ 156.2 Bn in 2026 and is projected to reach US$ 328.4 Bn by 2033, growing at a CAGR of 11.2% between 2026 and 2033. Global international tourist arrivals recovered to 1.4 billion in 2024 per UNWTO; digital booking platforms achieved 73.8% booking mode share; SUV rental adoption grew 12.5% at CAGR through premium leisure travel; and Asia Pacific's 13.7% CAGR reflects India's four-fold mobility service expansion and China's 14.3 Bn car rental market growth.

Accelerating global tourism recovery, digital platform-driven online booking consolidation, and corporate travel resumption across North America and Asia Pacific are the primary structural growth drivers. The historical 9.1% CAGR from 2020 to 2026 demonstrates the market's strong post-pandemic recovery trajectory, sustained by urbanization, shared mobility adoption, and emerging market travel demand expansion.

Key Industry Highlights:

- Leading Vehicle Type: Economy cars leads at 43.9% share (US$ 68.6 Bn); SUVs grow fastest at 12.5% CAGR, fueled by leisure family travel, adventure outstation demand, and premium fleet expansion at Enterprise and Hertz global networks.

- Leading Application: Airport Transport leads at 38.7% share (US$ 60.5 Bn); Outstation applications are likely to grow fast at a leading CAGR driven by India, China, and ASEAN self-drive platform adoption among urban Millennial leisure travelers.

- Leading Booking Mode: Online dominates at 73.8% share (US$ 115.3 Bn) and grows fastest at 12.4% CAGR, driven by OTA integration, mobile app adoption, and AI-powered dynamic pricing expansion globally through 2033.

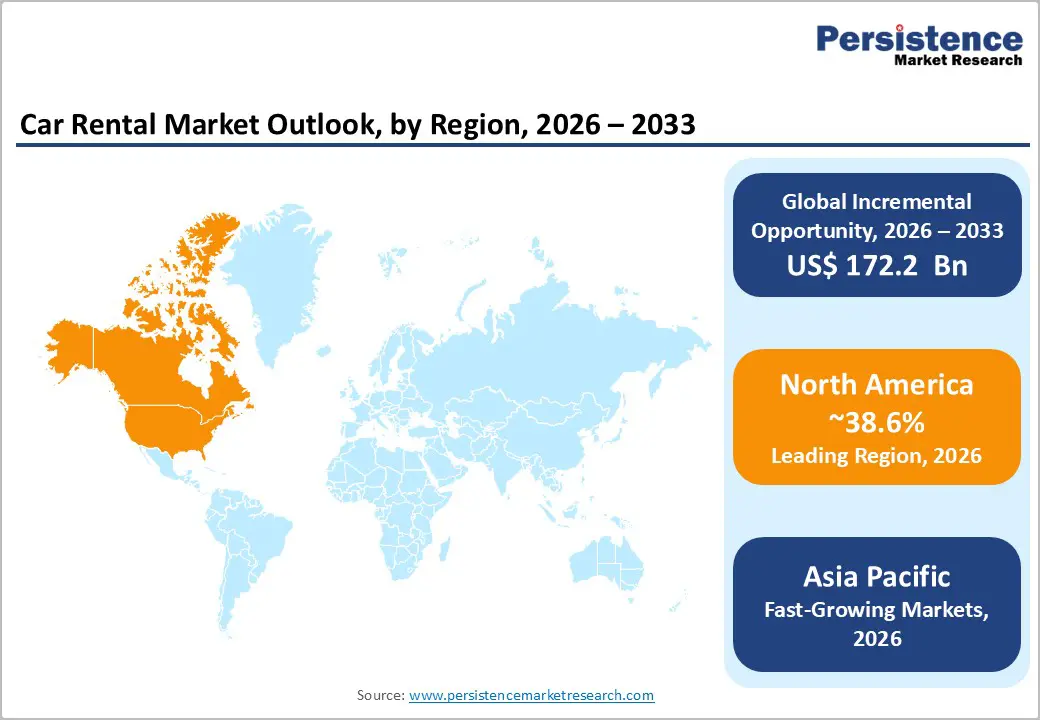

- Regional Leader: North America leads at 38.6% share (U.S. US$ 51.1 Bn); Asia Pacific is likely to achieve a fast-growth at 13.7% CAGR (China US$ 14.3 Bn, India US$ 4.9 Bn), driven by domestic tourism digitization and self-drive platform growth.

- Strategic Milestone: Enterprise's US$ 340 Mn European EV fleet expansion (March 2025) and Avis Budget's Kindred Fleet Management acquisition (November 2024) signal EV fleet transition and subscription mobility consolidation as twin defining strategic themes through 2033.

Market Dynamics Analysis

Drivers - Global Tourism Recovery and Business Travel Expansion Generating Structural Airport and Outstation Car Rental Demand

The UNWTO confirmed global international tourist arrivals reached 1.4 billion in 2024, fully recovering to pre-pandemic 2019 peak levels, with cross-border leisure and business travel combined generating over 2.8 billion airport transit movements globally, each representing a high-conversion airport car rental procurement event at Hertz, Enterprise, Avis, Sixt, and Europcar airport concession locations across 800+ major international gateway airports worldwide. IATA's 2025 airline industry forecast projects global passenger traffic reaching 5.2 billion by 2026, a 12.4% increase versus 2024, directly expanding the airport transport application segment that already commands 38.7% of total car rental market revenue, creating compounding inbound demand growth across global car rental operator airport fleet capacity programs.

Corporate travel management platforms, including CWT and American Express GBT, confirm business travel spend recovered to 95% of 2019 levels by Q1 2025, with corporate account car rental contracting representing high-frequency, multi-day, premium vehicle tier procurement that generates ASPs 35-55% above leisure rental equivalents at executive and SUV vehicle categories. The Global Business Travel Association (GBTA) projects global business travel spend reaching US$ 1.8 Tn by 2027, with car rental representing approximately 8-10% of total business travel expenditure across Fortune 500, FTSE 100, and Nikkei 225 corporate travel program budgets, sustaining premium vehicle tier car rental demand by 2033.

Digital Platform Transformation, App-Based Booking, and AI Fleet Management Driving Online Channel Dominance and Operational Efficiency

Online booking platforms, including Rentalcars.com, Kayak, Booking.com, and direct OTA integrations, processed over 74% of all global car rental transactions in 2025 (Industry Booking Mode Survey, Global Travel Distribution Report), with contactless pickup technologies including keyless entry smartphone digital key solutions reducing average customer wait time by 40% at rental pickup locations while IoT-enabled fleet telematics improving fleet utilization efficiency by 18% across connected fleet management deployments at Hertz, Enterprise, and Sixt major market operators.

Mobile-first booking adoption among Millennial and Gen Z leisure travelers, representing 62% of global car rental bookings in 2024, and app-integrated loyalty program adoption at Enterprise Plus, Hertz Gold, and Avis Preferred are sustaining online channel booking share consolidation from 73.8% toward an estimated 82-85% digital share by 2033.

AI-driven dynamic pricing algorithms, deployed by Avis Budget Group, Sixt SE, and Europcar, enable real-time demand-responsive fleet pricing across 200+ micro-market demand zones at major rental networks, delivering 12-18% revenue per available vehicle uplift versus static pricing models. Subscription-based rental models, monthly corporate vehicle subscription plans, and usage-based insurance integration via vehicle telematics further extend digital monetization beyond transactional one-time rental revenue toward recurring customer value streams that reduce customer acquisition cost dependence and improve fleet return predictability at operating scale.

Restraints - Regulatory Complexity Across Multi-Jurisdiction Insurance, Licensing, and Consumer Protection Frameworks Constraining Cross-Border Rental Expansion

Car rental operators expanding across multiple regulatory jurisdictions face a fragmented regulatory landscape covering minimum age requirements (18-25 years), mandatory third-party liability insurance thresholds, cross-border vehicle permit requirements, and consumer protection disclosure mandates varying significantly across 190+ national markets, with EU Member State transposition of the Consumer Rights Directive (2011/83/EU) alone creating 27 distinct national compliance configurations that constrain standardized fleet deployment and digital booking platform rollout at EU market expansion programs. Operators entering emerging markets including India, Indonesia, and Brazil face additional regional licensing, pollution compliance, and taxi aggregator classification regulatory hurdles that materially extend time-to-revenue at new market launch programs.

Fleet Supply Constraints from Automotive Production Delays and EV Fleet Transition Complexity Limiting Capacity Expansion

Global automotive production disruptions, compounded by semiconductor shortages affecting 2.5-3.0 million vehicle production units annually through 2024 (LMC Automotive Production Report), have constrained new fleet acquisition programs at Hertz, Avis, and Europcar, limiting capacity expansion below demand growth at key airport and metropolitan rental locations.

Hertz's partial EV fleet rollback, retiring 20,000 EVs in early 2024 citing elevated collision repair costs and resale value depreciation versus ICE equivalents, illustrates the operational complexity of fleet electrification at rental scale, constraining EV fleet transition timelines across the industry and limiting sustainability commitments actionable within near-term fleet procurement cycles.

Opportunities - Emerging Market Urbanization and Rising Middle-Class Mobility Demand Expanding Car Rental Addressable Market in Asia Pacific and Latin America

India's Urban population is projected to reach 600 million by 2030 (India Ministry of Housing and Urban Affairs), with rising disposable income driving first-time leisure travel and outstation rental adoption among upper-middle-class households in Tier 2 and Tier 3 Indian cities where car ownership rates remain below 20 vehicles per 1,000 inhabitants, generating demand for flexible short-duration car rental alternatives to ownership across Carzonrent, Zoomcar, and Ola self-drive platform commercial models.

Latin America's Localiza Rent a Car US$ 4.8 Bn annual revenue in 2024 and Brazilian domestic tourism growth of 8.9% YoY in 2024 (EMBRATUR, Brazil Tourism Authority), combined with Mexico's US$ 32 Bn tourism sector and Colombia's rising inbound tourist arrivals, indicate a combined Latin American car rental addressable market of US$ 12-15 Bn by 2030, particularly accessible through digital-first platform entry strategies targeting OTA-integrated booking at price-sensitive leisure and corporate travel segments.

EV and Sustainable Fleet Integration Creating Premium Eco-Rental Positioning and Corporate ESG Mandate Procurement Channels

Corporate sustainability mandates, driven by EU CSRD (Corporate Sustainability Reporting Directive, effective 2024) and SEC climate disclosure rules requiring Scope 3 emissions reduction across corporate supply chains including business travel, are generating structured demand for zero-emission vehicle rental options at Fortune 500 corporate travel programs where sustainability-linked car rental contracts command 8-15% premium pricing above ICE equivalent fleet configurations.

Enterprise Holdings' 50,000 EV fleet deployment target by 2026 and Sixt SE's BMW i-series and Tesla fleet integration across European premium rental locations position early-mover sustainable fleet operators to capture corporate ESG-mandated procurement contracts valued at an estimated US$ 4.2-6.8 Bn globally by 2028.

Category-wise Analysis

Vehicle Type Insights

Economy cars lead the vehicle type segment with a 43.9% market share in 2026, estimated at approximately US$ 68.6 billion, driven by their dominant positioning as the highest-demand rental vehicle tier across airport, leisure, and corporate rental applications where price-sensitive travelers and budget-managed corporate travel programs prioritize fuel efficiency, low daily rental rates, and broad fleet availability over vehicle class.

Economy car dominance reflects the volume tier of global car rental, with budget leisure travelers, short-term urban renters, and corporate policy-managed bookings collectively generating the largest single vehicle class booking volume across all major global rental networks and OTA booking platforms. SUVs are growing faster, but economy car's fundamental volume scale at price-sensitive global rental demand tiers sustains vehicle type segment leadership through 2033.

SUVs are the fast-growing vehicle type at 12.5% CAGR by 2033. Rising family leisure travel, adventure outstation trip demand, and corporate travel upgrading behavior across North America, Europe, and Asia Pacific, combined with SUV fleet expansion at major rental operators targeting premium leisure and outstation application revenue, drive SUV rental market share acceleration globally through 2033.

Application Insights

Airport Transport leads the application segment with a 38.7% share in 2026, estimated at approximately US$ 60.5 billion, anchored by the structural concentration of high-frequency rental transactions at airport concession locations where inbound international travelers generate the highest-value, multi-day rental bookings at Hertz, Enterprise, Avis, and Sixt terminal-embedded rental operations across 800+ major global airport gateways

Airport transport application leadership reflects both the premium booking value and the structurally captive demand of arriving international passengers for whom car rental represents the primary last-mile mobility solution at unfamiliar destinations. Outstation is growing faster, but airport application's premium multi-day rental value at high-volume international gateway locations sustains revenue segment leadership through 2033.

Outstation is the fast-growing application at 12.1% CAGR through 2033. Rising domestic leisure travel, weekend driving tourism, hill station and rural destination accessibility, and Millennial adventure travel behavior across India, China, and Southeast Asia, driving self-drive outstation rental adoption at Zoomcar, Drivezy, and regional platform operators, collectively fuel outstation application market growth acceleration by 2033.

Booking Mode Insights

Online booking leads the booking mode segment with a 73.8% market share in 2026, estimated at approximately US$ 115.3 Bn, driven by OTA platform aggregation, mobile app booking convenience, digital loyalty program integration, and AI-powered dynamic pricing delivering consumer value that has structurally shifted reservation behavior away from walk-up counter and telephonic booking toward mobile-first online transaction completion at Booking.com, Kayak, and direct operator app platforms. Online booking dominance reflects the irreversible digital transformation of car rental distribution, with contactless pickup, digital key delivery, and pre-arrival vehicle selection all requiring online booking origination.

Offline channel retains airport walk-up and corporate negotiated rate transactions, but online's share is trending toward 82-85% by 2033 with no structural reversal risk.

Online booking is simultaneously the fast-growing channel at 12.4% CAGR by 2033. Expanding smartphone penetration across Asia Pacific and Latin American emerging markets, OTA integration at airline booking checkout flows, and subscription-based digital rental platform adoption among urban Millennial and Gen Z consumers collectively drive online booking channel market volume and revenue acceleration globally.

Regional Market Insights

North America Car Rental Market Insights

North America leads the global car rental Market with a 38.6% share in 2026, estimated at approximately US$ 60.3 Bn, driven by the United States' scale of airline passenger volumes, the world's highest per-capita leisure and business travel car rental penetration rates, and a mature OTA and corporate travel management ecosystem sustaining high-frequency premium vehicle rental demand at Enterprise Holdings, Hertz, and Avis Budget Group airport and urban fleet networks across the United States and Canada.

U.S. Car Rental Market: Global Car Rental Capital, OTA Leadership, and EV Fleet Transition

The United States holds approximately US$ 51.1 Bn in 2026, driven by the world's largest airline network at 900 million domestic enplanements in 2024 (U.S. Bureau of Transportation Statistics), GBTA-tracked corporate travel recovery to pre-pandemic spend levels, and Enterprise Holdings' 1.9 million-vehicle global fleet leadership. U.S. DOT regulations and ADA rental fleet compliance standards sustain certification requirements. Canada contributes through tourism and cross-border U.S. travel drive rental demand at Enterprise and Hertz Canadian networks.

North America's leadership is reinforced by U.S. corporate travel demand recovery, premium SUV and executive tier rental ASP growth, and digital loyalty program subscription model expansion, delivering sustained revenue per available vehicle uplift at Enterprise, Hertz, and Avis U.S. fleet networks by 2033.

Europe Car Rental Market Insights

Europe holds a 24.2% share of the global car rental market in 2026, estimated at approximately US$ 37.8 Bn, driven by Schengen Zone cross-border tourism, EU consumer protection-compliant OTA booking platforms, inbound international tourist arrivals at Paris, Rome, Barcelona, and Amsterdam generating premium multi-day car rental demand at Europcar, Sixt, and Hertz European airport and urban station networks.

Germany Car Rental Market: Business Travel, Inbound Tourism, and EV Fleet Integration

Germany holds approximately US$ 8.6 Bn in 2026, anchored by BMW Motorrad, Volkswagen fleet leasing integration with Sixt premium car rental, and Frankfurt and Munich airport concession revenues. The U.K. sustains Enterprise and Hertz premium business travel and leisure rental demand at Heathrow, Gatwick, and Manchester. France drives Europcar home market leadership at CDG and Nice Côte d'Azur airports. Spain benefits from Mallorca and Canary Islands leisure rental demand at record 94 million tourist arrivals in 2024. EU Fit for 55 EV fleet mandate compliance shapes fleet investment planning.

Europe's EU tourism recovery momentum, EV fleet transition investment at premium operator networks, and Schengen cross-border leisure rental demand sustain above-average ASP car rental market revenue growth across European airport and urban station networks through 2033.

Asia Pacific Car Rental Market Share

Asia Pacific is the fast-growing region poised to reach 13.7% CAGR by 2033, commanding an estimated 22.8% of global Car Rental Market share in 2025, expanding rapidly through China's platform-integrated self-drive rental, India's PLI-supported tourism and digitization-driven outstation rental growth, and ASEAN's expanding inbound tourist arrivals generating both airport and outstation car rental procurement demand.

China Car Rental Market: Self-Drive Platform Growth, PLI Tourism Investment, and Airport Rental Expansion

China holds US$ 14.3 Bn in 2026, driven by DiDi Chuxing's self-drive integration, SAIC Mobility's fleet platform, and China Tourism Academy-tracked 5.6 billion domestic tourist trips in 2024. India at US$ 4.9 Bn grows through Carzonrent, Zoomcar, and Ola self-drive rapid urban expansion at 13.5% CAGR, backed by India's National Tourism Policy investment programs. Japan sustains Toyota Rent a Car and Nippon Rent-A-Car at premium inbound tourism tiers. Thailand, Vietnam, and Indonesia generate ASEAN airport rental volume growth.

Asia Pacific's China self-drive platform scale, India outstation digital rental adoption at 13.5% CAGR, and ASEAN inbound tourist arrival growth collectively sustain the region's fastest-growth trajectory and expanding global market share through 2033.

Competitive Landscape

The global car rental market is moderately consolidated at the premium tier, with Enterprise Holdings, Hertz, Avis Budget Group, Sixt SE, and Europcar collectively holding approximately 52-58% of global car rental revenue, while regional platform operators including Localiza, Carzonrent, Zoomcar, and Turo compete across emerging market self-drive, peer-to-peer, and subscription rental segments. Proprietary digital loyalty programs, airport concession exclusivity, and EV fleet differentiation are primary competitive moats.

EV fleet sustainability integration, AI-powered dynamic pricing platform development, subscription-based urban rental model expansion, and Asia Pacific emerging market geographic footprint scaling define the dominant competitive strategic investment themes across all global Car Rental market participants.

Strategic Developments

- In January 2025, Hertz Global Holdings announced a partnership with BP Pulse to deploy EV charging infrastructure at 50 key Hertz U.S. airport rental locations, covering 2,500 EV charging points targeting Tesla, Polestar, and Chevrolet Bolt EV rental fleet vehicles, enhancing Hertz EV rental customer experience and fleet operational readiness.

- In March 2025, Enterprise Holdings expanded its European car rental footprint through a US$ 340 Mn fleet investment across Germany, France, and Italy, adding 22,000 new vehicles including BMW, Mercedes-Benz, and Volkswagen EV models to European corporate travel account fleet programs targeting Sixt and Europcar corporate client acquisition.

- In September 2024, Sixt SE announced a technology partnership with Mercedes-Benz Mobility, integrating Mercedes-Benz digital key technology and over-the-air vehicle software update capability into Sixt's premium rental fleet across 10 European markets, enabling contactless vehicle access and remote feature customization for Sixt premium corporate rental subscribers.

Car Rental Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 92.6 Bn |

| Current Market Value (2026) | US$ 156.2 Bn |

| Projected Market Value (2033) | US$ 328.4 Bn |

| CAGR (2026 - 2033) | 11.2% |

| Leading Region | North America |

| Dominant Booking Mode | Online - 73.8% |

| Top-ranking Vehicle Type | Economy Cars - 43.9% |

| Incremental Opportunity | US$ 172.2 Bn |

Companies Covered in Car Rental Market

- Enterprise Holdings Inc.

- Hertz Global Holdings Inc.

- Avis Budget Group Inc.

- Sixt SE

- Europcar Mobility Group

- Localiza Rent a Car S.A.

- National Car Rental

- Alamo Rent a Car

- Thrifty Car Rental

- Dollar Rent A Car

- Toyota Rent a Car

- Carzonrent India Pvt. Ltd.

- Turo Inc.

- Zipcar

- Zoomcar Holdings Inc.

Frequently Asked Questions

The car rental market is likely to be valued at US$ 156.2 Bn in 2026, projected to reach US$ 328.4 Bn by 2033, delivering an unprecedented incremental opportunity of US$ 172.21 Bn through 2033.

UNWTO-confirmed 1.4 billion global tourist arrivals in 2024 recovering to pre-pandemic peaks, online booking platform dominance at 73.8% transaction share, and Asia Pacific's 13.7% CAGR driven by India and China self-drive platform adoption are the primary growth drivers.

The car rental market is likely to grow at a CAGR of 11.2% from 2026 to 2033 reflecting sustained global tourism and digital platform expansion momentum.

Asia Pacific urbanization-driven self-drive rental opportunity of US$ 28-35 Bn by 2030 and corporate ESG-mandated EV sustainable fleet rental contracts valued at US$ 4.2-6.8 Bn globally by 2028 represent the highest-value strategic market growth opportunities.

Enterprise Holdings, Hertz, Avis Budget Group, Sixt, Europcar, Localiza, National, Alamo, Thrifty, Dollar, Toyota Rent a Car, Carzonrent, Turo, Zipcar, and Zoomcar are the leading global Car Rental market participants.