- Marine

- North America Boat Trailer Market

North America Boat Trailer Market Size, Share, and Growth Forecast 2026 - 2033

North America Boat Trailer Market by Product Type (Bunk Trailers, Roller Trailers, Float-on / Drive-on Trailers, Hybrid Trailers), by Load Capacity (Up to 1,500 kg, 1,500 - 3,000 kg, 3,000 - 4,500 kg, Above 4,500 kg), Distribution Channel (Marine Dealerships, Specialty Trailer Retailers, Online Direct Sales), Technology, End User, and Regional Analysis, 2026 - 2033

North America Boat Trailer Market Size and Trend Analysis

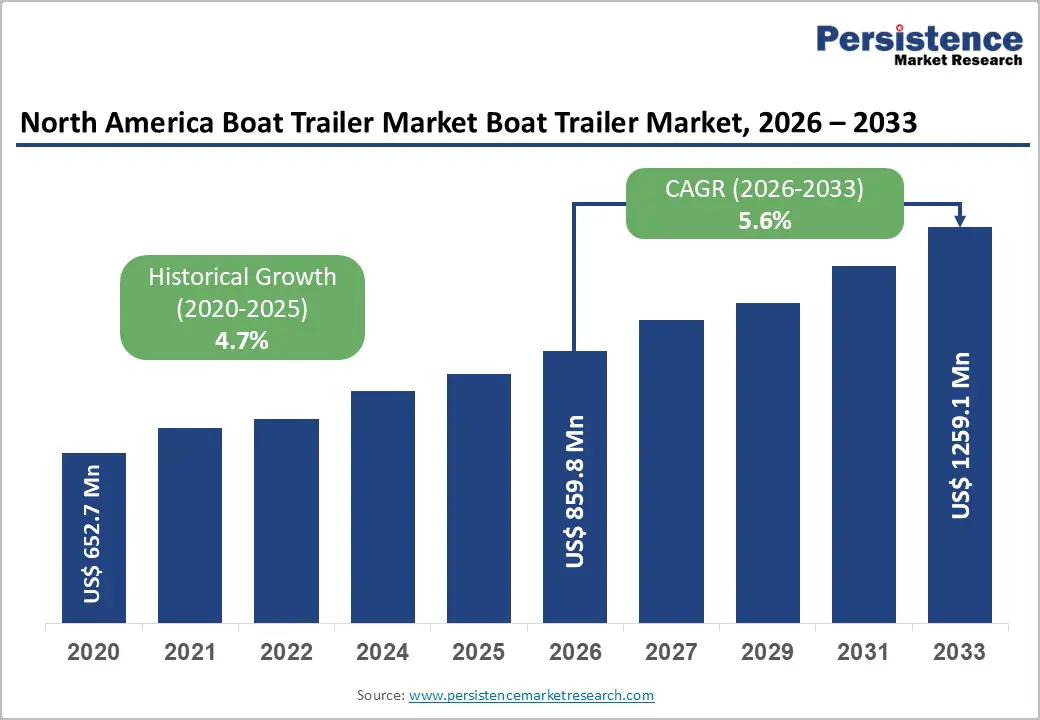

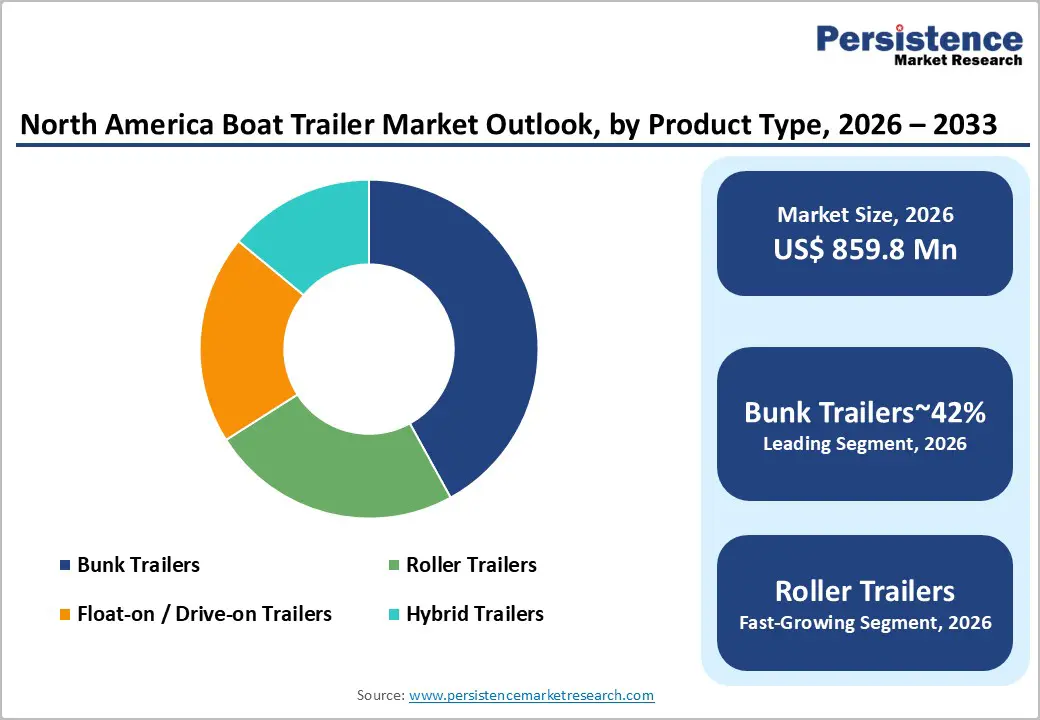

The North America boat trailer market size is likely to be valued at US$ 859.8 million in 2026 and is expected to reach US$ 1,259.1 Million by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033.

Sustained growth in the North America boat trailer market is anchored in the region's deeply embedded recreational boating culture, a large and expanding registered boat fleet, and ongoing investments in marine infrastructure.

Key Market Highlights

- Dominant Segment: Bunk Trailers lead the By Product Type category with approximately 42% market share, favoured for their universal hull compatibility, competitive pricing, and suitability across the broadest range of fiberglass, aluminium, and V-hull recreational boat types.

- Fastest Growing Segment: Corrosion-resistant Coatings within the Technology category is the fastest growing segment, driven by rising saltwater boating participation, consumer demand for long-service-life trailers, and premium pricing power for hot-dipped galvanized and marine-grade aluminium products.

- Key Opportunity: The emerging electric boat market presents a high-value opportunity, with heavier EV battery payloads requiring purpose-built, higher-rated trailer platforms integrated with smart monitoring technology and onboard charging system compatibility for the next generation of watercraft.

| Key Insights | Details |

|---|---|

| North America Boat Trailer Market Size (2026E) | US$ 859.8 Million |

| Market Value Forecast (2033F) | US$ 1,259.1 Million |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 4.7% |

Market Dynamics

Drivers - Strong Recreational Boating Participation and Rising New Boat Sales Drive Consistent Boat Trailer Demand Growth

Recreational boating continues to be one of the most popular outdoor leisure activities in North America, playing a crucial role in sustaining demand for boat trailers. According to the NMMA’s 2023 Recreational Boating Statistical Abstract, new powerboat retail sales in the United States reached approximately 268,600 units in 2022, maintaining strong momentum compared to pre-pandemic levels. Canadian Marine Industries Association reported continued growth in boating activity across Canadian waterways. Notably, nearly 95% of the U.S. recreational boat fleet is classified as trailerable, meaning these boats require highway-rated trailers for transportation. As a result, every new boat purchase almost always leads to a corresponding trailer purchase or upgrade. This strong interdependence between boat and trailer sales creates a stable, volume-driven growth foundation, ensuring consistent demand for trailers across North America over the long term.

Aging Trailer Fleet and Regulatory Compliance Accelerate Replacement Demand, Ensuring Steady Aftermarket Sales Growth

In addition to new boat sales, the replacement cycle of aging boat trailers represents a significant and often overlooked driver of market demand. Typically, boat trailers have an effective service life of 10 to 15 years, depending on maintenance practices, exposure to harsh environments such as saltwater, and frequency of use. Across North America, millions of trailers are currently in operation, many of which were purchased during the early 2000s boating boom and the pandemic-driven surge between 2020 and 2021.

As these units approach or exceed their functional lifespan, replacement becomes inevitable. Furthermore, safety regulations set by the U.S. Department of Transportation, particularly regarding lighting and structural compliance, encourage owners to replace outdated trailers rather than invest in costly repairs, thereby accelerating the replacement cycle and sustaining consistent market demand.

Restraints - Fluctuating Steel and Aluminum Prices Impact Manufacturing Costs, Influencing Pricing Strategies and Consumer Purchase Decisions

Boat trailer manufacturing heavily depends on key raw materials such as galvanized steel and aluminum alloys, both of which are highly sensitive to global price fluctuations. Factors including supply chain disruptions, trade tariffs, and shifts in commodity markets have contributed to significant price volatility in recent years.

The U.S. Bureau of Labor Statistics reported a sharp increase in the Producer Price Index for fabricated structural metal products during 2021 and 2022. These rising input costs have placed pressure on manufacturers’ profit margins, often forcing them to increase product prices. As a result, consumers, particularly in the mid-range segment, may delay purchase decisions due to higher costs. This price sensitivity can slow down overall market growth during periods of instability, making raw material cost fluctuations a key restraint that manufacturers must strategically manage to maintain competitiveness and sustain demand.

Complex State-level Trailer Regulations Create Compliance Challenges, Increasing Costs and Limiting Standardized Product Development Strategies

The regulatory environment for boat trailers in North America is highly fragmented, particularly in the United States, where towing, registration, and safety requirements are governed at the state level. Each state has its own set of rules regarding braking systems, lighting standards, maximum trailer dimensions, and registration procedures. Similarly, Canada follows province-specific regulations, adding another layer of complexity for manufacturers and consumers.

This lack of standardization often creates confusion for buyers who intend to use their trailers across multiple states or regions. Additionally, manufacturers face increased design and compliance challenges, as they must ensure their products meet varying regulatory requirements. In many cases, this leads to additional retrofitting costs and operational inefficiencies. The absence of unified federal standards for lower GVWR trailers further complicates product development, limiting scalability and increasing the overall compliance burden.

Opportunities - Demand for Corrosion-Resistant Materials and Smart Technologies Creates Innovation Opportunities In The Premium Boat Trailer Segment

The rising popularity of saltwater boating along the Gulf Coast, Atlantic, and Pacific regions is creating strong demand for advanced corrosion-resistant boat trailers. Manufacturers are increasingly focusing on premium materials such as marine-grade aluminum, hot-dipped galvanized steel, and durable powder-coated finishes to enhance product longevity and performance. These advanced solutions not only improve durability but also command higher price points, contributing to revenue growth.

In parallel, the integration of smart technologies is transforming the boat trailer landscape. Features such as GPS tracking, wireless tire pressure monitoring systems, LED lighting with diagnostic capabilities, and electric-over-hydraulic braking systems are gaining traction among premium customers. As technology adoption increases, manufacturers have the opportunity to offer connected trailer ecosystems supported by mobile applications. This opens the door to recurring revenue models through subscriptions, while also enabling differentiation in an increasingly competitive market environment.

Growth of Electric Boats Drives Need for High-Capacity, EV-Compatible Trailers, Creating New Market Expansion Opportunities

The emergence of the electric boat market presents a significant growth opportunity for boat trailer manufacturers in North America. Innovative companies such as X Shore, Vita Power, and Candela are introducing electric watercraft, while established players like Mercury Marine and Torqeedo are expanding their electric propulsion offerings. Unlike traditional boats, electric vessels are equipped with heavy battery systems, resulting in higher overall weights during transportation.

This shift creates a need for specially designed trailers with higher load capacities and enhanced structural strength. Additionally, there is growing demand for trailers equipped with integrated electrical systems capable of supporting onboard charging functionalities. As the electric boating market is expected to grow rapidly over the coming decade, manufacturers that invest early in EV-compatible trailer designs can gain a competitive advantage. This segment offers strong potential for innovation, differentiation, and long-term revenue growth in the evolving marine ecosystem.

Category-wise Analysis

By Product Type Insights

Bunk trailers dominate the North American boat trailer market, accounting for approximately 42% of the total market share. These trailers are designed to support the boat hull along its entire length using carpet-covered wooden or composite bunks, ensuring even weight distribution and enhanced protection. They are widely preferred for fiberglass boats, sailboats, and aluminum fishing vessels due to their adaptability to various hull shapes, including flat-bottom, V-hull, and modified-V designs.

Their simple construction makes them cost-effective, which further strengthens their popularity among consumers. Additionally, bunk trailers perform well in varying water depths, making them highly suitable for different types of launch ramps. Leading manufacturers such as Load Rite Trailers Inc. and EZ Loader have developed extensive product portfolios centered around bunk trailer platforms. Their versatility, affordability, and compatibility with a wide range of boats continue to reinforce their position as the most preferred product type.

By Load Capacity Insights

The 1,500 to 3,000 kg load capacity segment leads the North American boat trailer market, representing approximately 38% of the total market share. This segment aligns closely with the most popular recreational boat categories, including 17 to 24-foot fishing boats, bowriders, and deck boats, which dominate new boat sales in the region. These trailers offer an optimal balance between capacity and towing convenience, making them highly practical for everyday use.

They are compatible with commonly used towing vehicles such as half-ton and three-quarter-ton pickup trucks, which are widely owned across North America. This compatibility significantly enhances their market appeal among both individual consumers and dealerships. As a result, trailers in this category are considered highly versatile and commercially viable. Their ability to meet the needs of a broad customer base ensures sustained demand, making this segment a key contributor to overall market growth.

By Distribution Channel Insights

Marine dealerships represent the leading distribution channel in the North American boat trailer market, accounting for approximately 52% of total sales. This dominance is driven by the strong integration between boat and trailer purchases, as most customers prefer to buy both products together as part of a bundled package. Dealerships provide a seamless buying experience by offering tailored trailer options that match specific boat models, ensuring compatibility and performance.

In addition to product sales, dealerships deliver value-added services such as financing options, customization, installation of accessories, and ongoing maintenance support. These services enhance customer convenience and foster long-term relationships. Organizations like the Marine Retailers Association of the Americas support an extensive network of dealerships across the United States and Canada. This well-established infrastructure gives dealerships a significant competitive advantage over independent retailers and online platforms, reinforcing their position as the primary sales channel.

By Technology Insights

Corrosion-resistant coatings are the leading technology segment in the North American boat trailer market, contributing approximately 30% of total technology-related value. Boat trailers are frequently exposed to water, including saltwater environments, which significantly increases the risk of corrosion over time. As a result, durability and resistance to environmental damage are critical factors influencing purchasing decisions. Technologies such as hot-dipped galvanization, marine-grade aluminum construction, and advanced epoxy coatings are widely adopted to extend product lifespan. These solutions not only improve performance but also reduce long-term maintenance costs for users. According to the American Galvanizers Association, galvanized coatings can provide protection for over 50 years under typical atmospheric conditions. This long-term value proposition supports premium pricing and drives strong adoption, particularly in coastal and high-usage regions. As customers increasingly prioritize durability, corrosion-resistant technologies remain a key focus area for manufacturers.

By End-user Insights

Recreational boat owners represent the largest end-user segment in the North American boat trailer market, accounting for approximately 68% of total demand. This dominance reflects the overall structure of the boating industry, where the majority of vessels are privately owned and used for leisure purposes. According to the U.S. Coast Guard, there are over 12 million registered recreational boats across the country, highlighting the scale of this segment.

Individual owners are the primary buyers of both new and replacement trailers, driven by factors such as boat upgrades, wear and tear, and changing usage needs. Their purchasing behavior remains relatively stable, supported by consistent participation in boating activities. This large and active customer base provides a strong foundation for market growth. As recreational boating continues to thrive, this segment is expected to maintain its leading position and drive sustained demand for boat trailers in the region.

Competitive Landscape

The North American boat trailer market is moderately fragmented, with a combination of well-established manufacturers and regional players competing across different segments. Companies such as Load Rite Trailers Inc., EZ Loader, and ShoreLand’r Trailers differentiate themselves through broad product portfolios, strong dealer relationships, and a focus on product quality and durability. Competition is largely driven by factors such as corrosion resistance, customization capabilities, and compatibility with a wide range of boat models.

Manufacturers are increasingly incorporating advanced features such as LED lighting systems, electric braking mechanisms, and model-specific fit designs to enhance product value. While traditional dealership networks remain dominant, direct-to-consumer online sales channels are gradually gaining traction, particularly among price-sensitive buyers. Additionally, premium brands are leveraging lifetime warranties and superior build quality as key differentiators. This dynamic competitive environment encourages continuous innovation and strategic positioning among market participants.

Key Developments:

- In February 2025: Load Rite Trailers Inc. expanded its aluminum trailer portfolio by introducing advanced bunk and roller configurations tailored for electric boats. These models feature reinforced axle capacities and integrated wiring systems compatible with onboard charging, addressing increasing weight and electrical requirements of modern electric marine vessels.

- In September 2024: EZ Loader introduced an upgraded custom-fit trailer program in collaboration with leading boat OEMs, enabling factory-matched trailer specifications for specific boat models. This initiative enhances dealer efficiency, simplifies bundled sales, and improves customer experience by ensuring precise fit, safety, and performance optimization.

- In April 2023: Triton Trailers launched a new aluminum alloy frame series designed with enhanced corrosion resistance, marine-grade welding, and upgraded LED lighting systems. The product targets high-salinity coastal regions, offering improved durability, reduced maintenance, and extended lifespan for trailers used in saltwater environments.

Companies Covered in North America Boat Trailer Market

- Load Rite Trailers Inc.

- Karavan Trailers

- Magic Tilt Trailers

- EZ Loader

- Magnum Trailers Inc.

- Triton Trailers

- ShoreLand'r Trailers

- Continental Trailers

- Venture Trailers

- Yacht Club Trailers

- Amera Trail Inc.

- Boatmate Trailers Inc.

- Marine Master Trailers

- McClain Trailers Inc.

- MYCO Trailers LLC

- Calkins Industries Inc.

- Trailmaster Trailers

- Pacific Coachworks

Frequently Asked Questions

The North America Boat Trailer Market is projected to reach US$ 1,259.1 Million by 2033, growing from an estimated US$ 859.8 Million in 2026, at a CAGR of 5.6% during the 2026-2033 forecast period, underpinned by the region's large registered recreational boat fleet and sustained outdoor recreation spending.

Key growth drivers include the region's vast trailerable recreational boat fleet of over 17 million registered vessels, of which approximately 95% require trailers for transport, combined with the accelerating replacement cycle for aging trailer stock and the post-pandemic surge in recreational boating participation documented by the NMMA.

Bunk Trailers lead the By Product Type segment with approximately 42% market share. Their leadership is driven by universal compatibility with the broadest range of hull configurations, including flat-bottom, V-hull, and modified-V designs, competitive pricing, and adoption by major manufacturers such as Load Rite Trailers Inc. and EZ Loader.

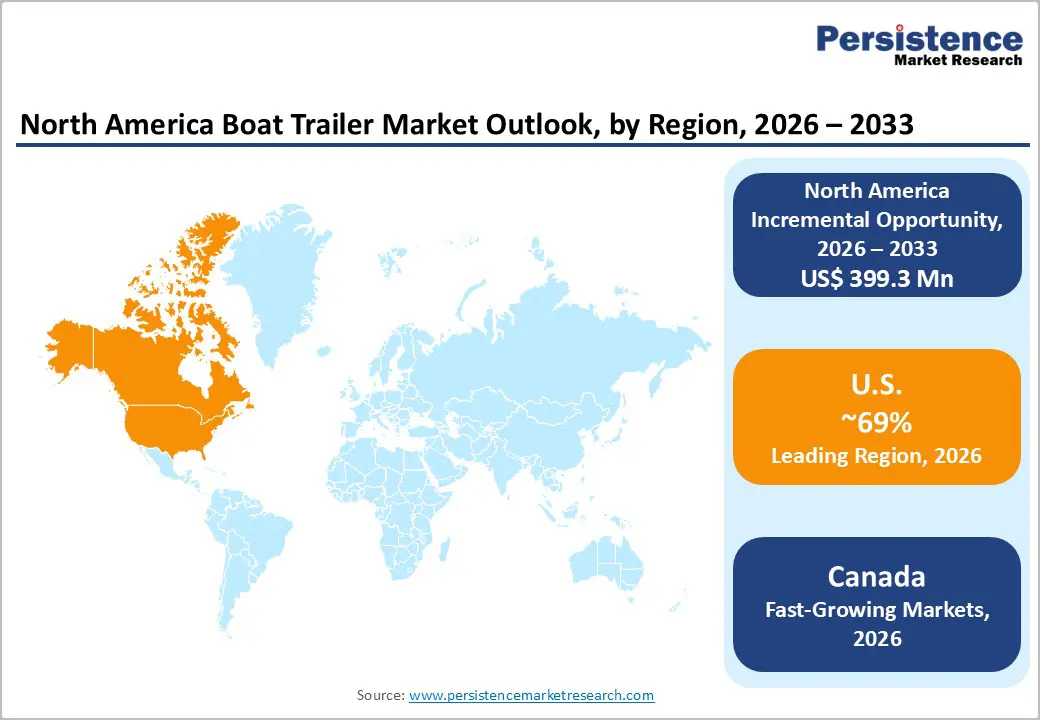

The United States dominates the North America Boat Trailer Market, underpinned by the world's largest recreational boating fleet, over 17 million registered trailerable vessels, deep marine dealer infrastructure, and concentration of demand in high-boating states such as Florida, Texas, and Michigan. Florida alone leads all U.S. states in registered recreational vessels per U.S. Coast Guard data.

Key opportunities include the development of purpose-built, weight-rated trailer platforms for the emerging electric boat market, which features heavier battery payloads requiring upgraded trailer designs, and the integration of smart trailer technologies such as GPS tracking, TPMS, and connected LED diagnostic systems that support premium pricing and new subscription-based service revenue models.

The leading market participants include Load Rite Trailers Inc., Karavan Trailers, Magic Tilt Trailers, EZ Loader, Magnum Trailers Inc., Triton Trailers, ShoreLand'r Trailers, Continental Trailers, Venture Trailers, Yacht Club Trailers, Amera Trail Inc., Boatmate Trailers Inc., Marine Master Trailers, McClain Trailers Inc., and MYCO Trailers LLC.