- Marine

- Marine Ports and Services Market

Marine Ports and Services Market Size, Share and Growth Forecast, 2026 - 2033

Marine Ports and Services Market by Container handling services (Container Handling, Quay‑side Cranes, Others), Ship repair and maintenance services (In‑port ship repair, Dry‑Dock Services, Others), Logistics‑Support Services, and Regional Analysis for 2026 - 2033

Marine Ports and Services Market Share and Trends Analysis

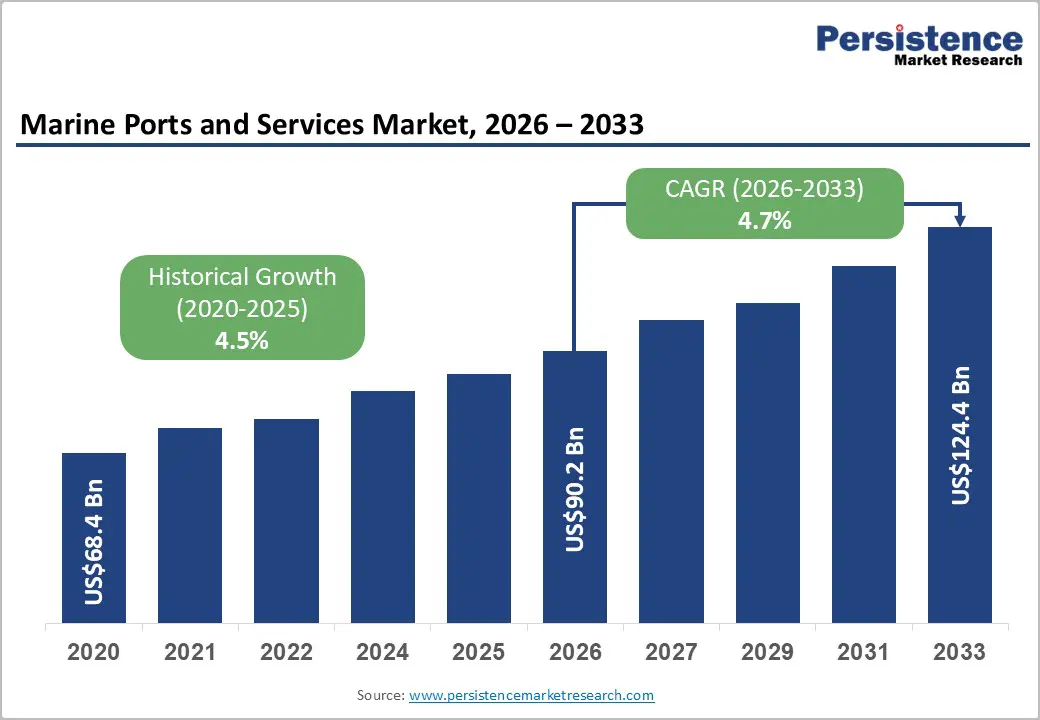

The global marine ports and services market size is likely to be valued at US$ 90.2 billion in 2026 and is projected to reach US$ 124.4 billion by 2033, growing at a CAGR of 4.7% during the forecast period 2026–2033, driven by global trade volumes, which continue to channel approximately 80% of international merchandise through maritime routes.

The proliferation of port automation technologies, including AI-driven cargo handling and IoT-enabled vessel traffic management systems, is fundamentally reshaping operational efficiency benchmarks across major shipping hubs. These converging forces position marine port services as indispensable infrastructure, enabling seamless supply chain operations and sustained economic connectivity across continents.

Key Industry Highlights:

- Dominant Segments: Container handling is estimated to hold 42% share in 2026, while automation is expected to grow the fastest through 2033, driven by efficiency gains.

- Leading Sub-segments: Dry-dock services are projected at 33% share, while IoT in logistics-support is likely to expand at the fastest pace.

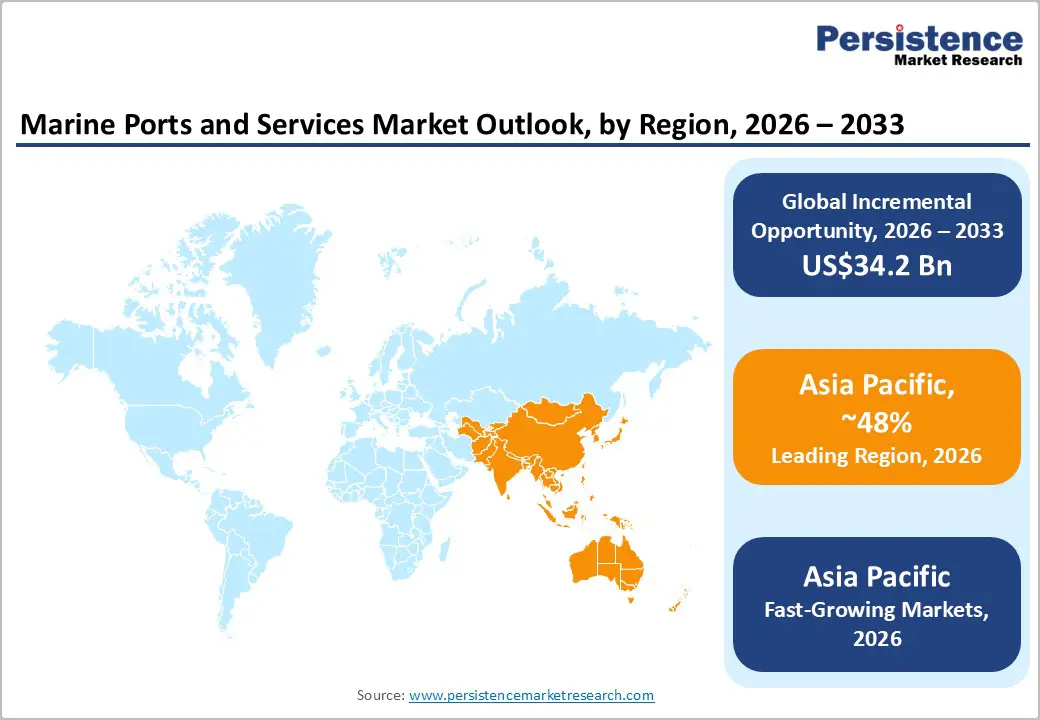

- Regional Leadership: Asia Pacific is expected to lead with 48% share in 2026 and remain the fastest-growing region at 5.2% CAGR.

- Competitive Environment: Market leaders are expected to focus on capacity expansion, strategic partnerships, and digital transformation initiatives, while gradually increasing their presence in high-growth emerging markets.

DRO Analysis

Driver - Global Trade Expansion Powers Port Services Growth

Global seaborne trade exceeded 11 billion tonnes annually per UNCTAD data, with projections indicating continued expansion through 2033. Container shipping dominates manufactured goods movement, with worldwide port throughput recovering to pre-pandemic levels and showing steady year-over-year growth.

Asia Pacific ports handle approximately 65% of global container traffic, establishing the region as the maritime logistics epicenter. This sustained momentum creates strong demand for container handling, vessel pilotage, and integrated logistics solutions. Operators respond with multi-billion-dollar capacity expansion programs to accommodate larger vessels and escalating cargo volumes.

Digitalization and Infrastructure Investments Drive Acceleration

Smart port transformations through automation, IoT, and AI deliver 25–30% productivity improvements while cutting labor costs and handling errors. Digital twin technology provides real-time infrastructure monitoring, complemented by blockchain documentation for streamlined customs clearance.

Government-backed investments exceed hundreds of billions through public-private partnerships worldwide. China's port expansion spans domestic mega-ports and overseas projects across Asia, Africa, and the Middle East. EU's TEN-T framework and the U.S. Infrastructure Act fund major upgrades at key facilities such as Los Angeles and Rotterdam.

Restraint - Regulatory Overhaul and Geopolitical Risks Constrain Growth

IMO’s tightened sulfur rules, including the Mediterranean Sea ECA, and its 2025-approved net-zero framework, raise compliance costs and force ports to invest heavily in shore power, electrification, and alternative-fuel infrastructure. These mandates strain smaller ports lacking scale and divert capital from pure capacity expansion. The UNCTAD’s 2025 outlook notes that geopolitical tensions, new tariffs, and rerouted flows are stalling maritime growth and unsettling investment plans.

The Red Sea and Suez disruptions through 2025–2026 lengthen transit times and raise operating costs, while trade-policy shifts and targeted fees reallocate cargo and cloud long-term commitments. Cyber-threats to port systems further push operators toward resilience spending instead of growth, collectively constraining the pace and geography of port-services expansion.

Opportunity - Greenfield Growth and Sustainable Port Integration Unlock New Revenue Streams

Rapid industrialization in Sub-Saharan Africa and South Asia is driving greenfield port development and integrated logistics hubs, supported by India’s Sagarmala Programme and AfCFTA-linked infrastructure initiatives launched in 2025–2026. Global operators such as DP World have announced multi-billion-dollar expansions in India, Africa, and Europe, including new large-capacity ports and upgraded terminals. These projects create a strong pipeline for marine port services, port-centric warehousing, customs processing, and last-mile distribution aligned with rising e-commerce and regional trade.

Tightening emissions standards and corporate-sustainability targets are accelerating investments in shore power, LNG and hydrogen bunkering, and on-site renewables, with leading ports rolling out zero-emission terminal pilots and green-certification programs. As governments and operators prioritize energy-efficient equipment and digital monitoring, the integration of green technologies and logistics-centric port operations is poised to become a key growth engine for the marine ports and services market through 2033.

Category-wise Analysis

Container Handling Services Insights

The container handling services segment is expected to dominate with 42% revenue share in 2026. The marine ports and services market is supported by sustained growth in containerized trade and rising port throughput volumes. Key sub-segments such as quay-side cranes and yard stacking systems are likely to remain essential for efficient cargo movement, while the shift toward automated terminals is anticipated to accelerate as ports aim to reduce congestion and enhance operational precision through AI and robotics.

In 2026, PSA International is estimated to have expanded automated operations at Tuas Mega Port, scaling autonomous cranes and AGVs to manage higher volumes, while in 2025, the Port of Rotterdam Authority reportedly deployed remote-controlled quay cranes integrated with digital twin technology to improve berth productivity.

The automated terminals sub-segment is projected to be the fastest-growing, driven by labor optimization and efficiency gains. Furthermore, DP World’s 2025 implementation of an AI-based container stacking system at Jebel Ali Port is expected to enhance yard planning and reduce rehandling, reinforcing automation as a key investment trend.

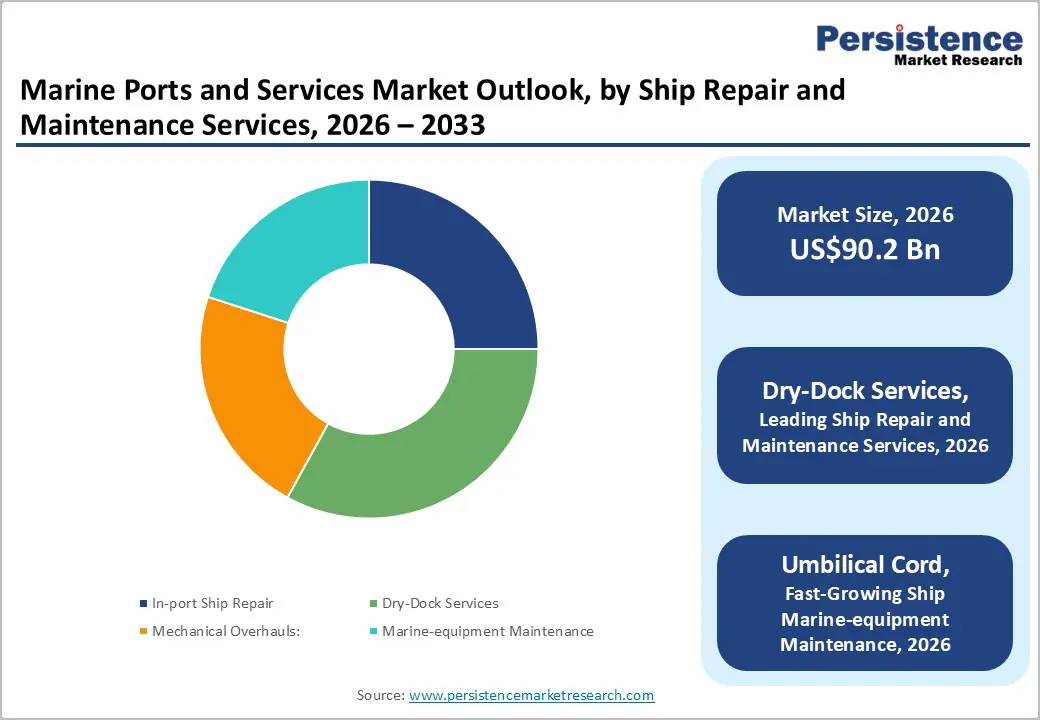

Ship Repair and Maintenance Services Insights

The ship repair and maintenance services segment is expected to grow steadily, with dry-dock services projected to account for approximately 33% of the segment share, maintaining leadership due to their critical role in vessel inspection, retrofitting, and regulatory compliance. Increasing fleet size and aging vessels are anticipated to drive demand for mechanical overhauls and marine equipment maintenance, particularly in ports with specialized infrastructure. In 2025, Keppel Offshore & Marine is estimated to have secured major contracts for LNG vessel upgrades and offshore asset repairs, while in 2026, Sembcorp Marine reportedly advanced capabilities in green retrofitting solutions.

The marine-equipment maintenance sub-segment is projected to be the fastest-growing, supported by environmental mandates and digitalization. Additionally, MAN Energy Solutions’ 2025 rollout of remote monitoring solutions is expected to enhance predictive maintenance and efficiency across marine service operations.

Logistics-Support Services

The logistics-support services segment is projected to maintain strong growth momentum, with vessel navigation expected to hold around 30% of the segment share, driven by its central role in supply chain integration. Ports are increasingly evolving into logistics hubs supporting cargo distribution and real-time tracking.

In 2025, Hamburg Port Authority is estimated to have expanded its smartPORT logistics platform, while in 2026, Busan Port Authority reportedly enhanced its automated logistics network with AI-enabled cargo tracking. The port digitalization and IoT integration sub-segment is anticipated to be the fastest-growing, supported by efficiency gains and visibility improvements. Furthermore, CMA CGM’s 2025 deployment of digital logistics solutions is expected to strengthen connectivity, reinforcing the shift toward smart port ecosystems.

Regional Analysis

North America Marine Ports and Services Market Trends

North America’s marine ports and services market is expected to progress at a steady pace, underpinned by consistent cargo flows and ongoing supply chain realignment. The U.S. clearly anchors the region, contributing more than 80% of total regional revenues, with major ports such as Los Angeles and Long Beach continuing to function as critical gateways for trans-Pacific trade. Growth is supported by resilient import demand and the gradual shift toward nearshoring, which is redistributing cargo volumes across Gulf and East Coast ports.

What distinguishes the region is its strong policy-backed modernization push. Federal funding programs are actively addressing long-standing congestion issues while encouraging the adoption of cleaner technologies such as shore power and low-emission cargo handling systems. The port operators are leaning into automation and digital platforms to improve turnaround efficiency. The competitive environment reflects a balance between public port authorities and private terminal operators, with investment increasingly flowing into smart logistics integration and capacity optimization, rather than just physical expansion.

Europe Marine Ports and Services Market Trends

Europe’s marine ports and services market reflects a mature yet highly adaptive ecosystem, where efficiency and innovation often outweigh capacity expansion. The Netherlands leads the region, contributing roughly 25% of regional market activity, largely due to Rotterdam’s role as a central logistics hub for European trade. The market growth is supported by stable intra-regional trade and strong hinterland connectivity despite spatial and regulatory constraints.

The region’s trajectory is closely tied to its regulatory priorities. Decarbonization goals are not just compliance measures but active drivers of investment, pushing ports toward renewable energy integration, alternative fuel infrastructure, and advanced emission monitoring systems. At the operational level, European ports are early adopters of digital solutions, using AI and data platforms to optimize vessel traffic and cargo flows. Competition is less about scale and more about efficiency, with operators focusing on technology-led differentiation and seamless multimodal connectivity to maintain their global relevance.

Asia Pacific Marine Ports and Services Market Trends

Asia Pacific continues to set the pace for the marine ports and services market, holding over 48% of global share while also emerging as the fastest-growing region with a CAGR of 5.2% through 2033. China remains the central force, accounting for approximately 60% of the regional market, supported by its extensive port network and export-driven economy. The region’s dominance is not just a function of scale but also its deep integration with global manufacturing and trade systems.

Beyond China, the broader region is evolving rapidly. Advanced economies such as Japan and South Korea are pushing the boundaries of automation and port digitalization, while Southeast Asian countries are expanding capacity to capture shifting manufacturing supply chains. Investments are increasingly directed toward handling mega-vessels and building integrated logistics ecosystems that connect ports with inland transport networks. The competitive landscape is dynamic, combining state-backed expansion with private sector innovation, all reinforcing Asia Pacific’s position as both the growth engine and innovation hub of the global maritime industry.

Competitive Landscape

The global marine ports and services market reflects a moderately fragmented to semi-consolidated structure, led by global operators such as A.P. Moller–Maersk (APM Terminals), DP World, PSA International, and Hutchison Ports. These players command a significant share of terminal capacity through long-term concessions and global port networks. Their competitive edge lies in integrated offerings that combine port operations with logistics and digital solutions. Continuous investments in automation, smart port infrastructure, and AI-driven systems are strengthening operational efficiency. This positions them strongly across high-volume international trade routes.

Regional and state-backed operators, including COSCO Shipping Ports and Adani Ports, are expanding through targeted infrastructure investments and geographic diversification. Entry barriers remain high due to capital intensity, regulatory complexity, and land constraints. However, digitalization is opening the door for technology providers, particularly in IoT, analytics, and port management software. Partnerships between port operators and tech firms are becoming more common. Over time, the market is expected to see gradual consolidation alongside rising collaboration in smart port ecosystems.

Key Industry Developments:

- In October 2025, APM Terminals Pipavav signed a ?17,000 crore (~US$2 billion) MoU with the Gujarat Maritime Board to expand port infrastructure, including container terminals, liquid cargo berths, and digital systems, with execution contingent on extending the concession agreement beyond 2028.

- In March 2025, DP World invested approximately US$3.1 billion in capital expenditure, exceeding earlier projections and expanding global port capacity to nearly 109 million TEU, with key upgrades at Jebel Ali (UAE) and London Gateway (UK) to enhance efficiency and throughput.

Companies Covered in Marine Ports and Services Market

- APM Terminals

- DP World

- PSA International

- COSCO Shipping Ports

- China Merchants Port Holdings

- Hutchison Ports

- Terminal Investment Limited

- Hamburger Hafen und Logistik AG

- Shanghai International Port Group

- Port of Rotterdam Authority

- International Container Terminal Services, Inc.

- Georgia Ports Authority

- Ningbo Zhoushan Port Company

- Port of Antwerp-Bruges

Frequently Asked Questions

The global marine ports and services market is projected to reach US$ 90.2 billion in 2026.

Rising global maritime trade, increasing port automation, and expanding logistics integration drive the market.

The market is expected to grow at a CAGR of 4.7% from 2026 to 2033.

Growth in smart ports, emerging trade corridors, and integrated logistics ecosystems creates key opportunities.

A.P. Moller–Maersk, DP World, PSA International, Hutchison Ports, and COSCO Shipping Ports lead the market.