- Hardware & Software IT Services

- Network Repeaters Market

Network Repeaters Market Size, Share, and Growth Forecast 2026 - 2033

Network Repeaters Market by Product Type (Wi-Fi Repeaters, Cellular Repeaters, Signal Repeaters, Bluetooth Repeaters, Optical Repeaters, Others), Deployment (Indoor Repeaters, Outdoor Repeaters, Mobile Repeaters), Technology (Analog Repeater, Digital Repeater, 2G/3G/4G/LTE Repeaters, 5G NR Repeaters, Others), Frequency Band (Low Band Repeaters, Mid Band Repeaters, High Band Repeaters, Others), End-user, and Regional Analysis for 2026 - 2033

Network Repeaters Market Size and Trend Analysis

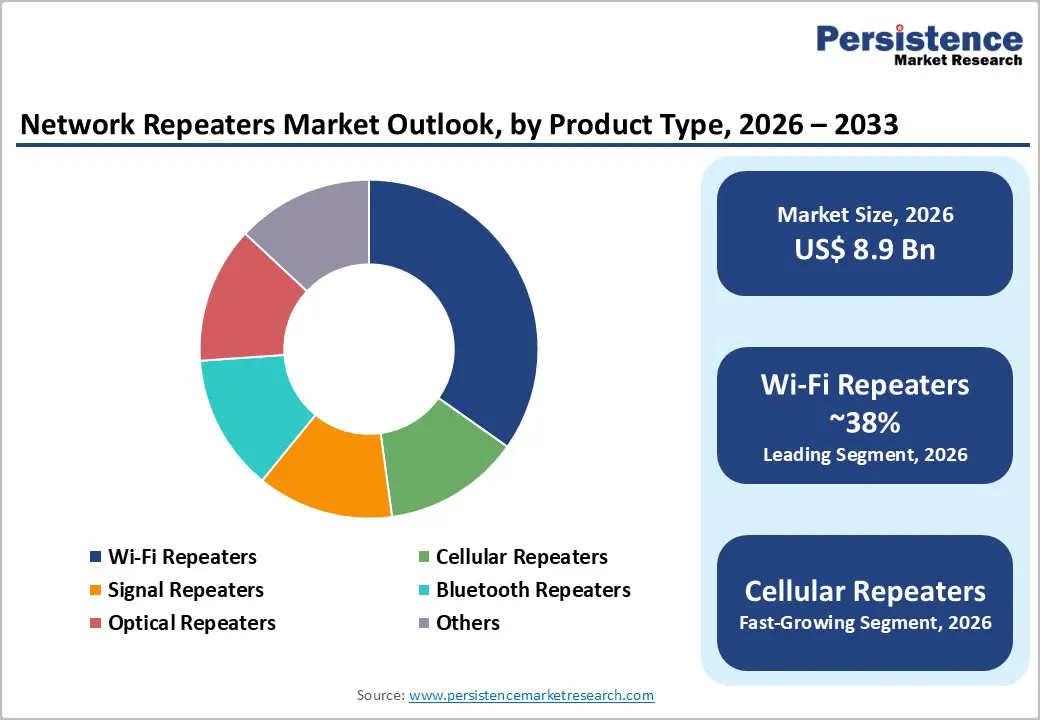

The global network repeaters market is valued at USD 8.9 billion in 2026 and is projected to reach USD 16.9 billion by 2033, expanding at a CAGR of 9.6%. Market growth is primarily driven by rapid 5G deployment, increasing mobile data consumption, and the proliferation of IoT devices requiring seamless connectivity across both urban and rural environments.

According to the International Telecommunication Union, nearly 2.7 billion people remain without internet access, highlighting significant opportunities for repeater infrastructure expansion. Additionally, smart city initiatives and enterprise digital transformation are accelerating demand for advanced signal amplification solutions.

A network repeater is a device that extends network coverage by receiving weak signals and retransmitting them at full strength. It operates across both wired and wireless networks-regenerating electrical or optical signals over long distances in wired systems, and rebroadcasting Wi-Fi signals to eliminate coverage gaps in wireless environments. Governed by standards from IEEE, Repeaters enhance signal quality without filtering or managing data traffic.

Key Industry Highlights:

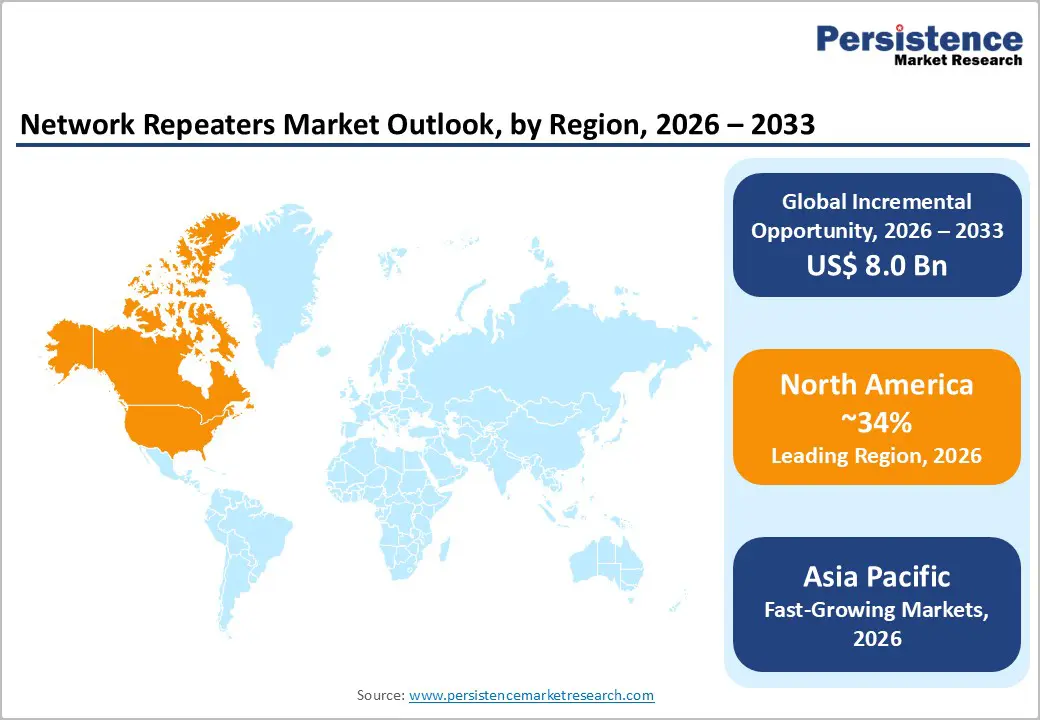

- Leading Region: North America dominates the global network repeaters market with approximately 34% revenue share in 2025, supported by advanced 5G rollouts, federal broadband funding, and mandatory in-building public safety coverage regulations.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, projected at a CAGR of 11.3% through 2033, driven by China's 5G densification, India's BharatNet program, and ASEAN smart city investments that require extensive repeater infrastructure.

- Dominant Segment: Wi-Fi Repeaters lead the Product Type category with approximately 38% market share in 2025, driven by the global proliferation of Wi-Fi 6E/7 devices and enterprise BYOD policies demanding expanded wireless coverage areas.

- Fastest Growing Segment: 5G NR Repeaters are expanding at a CAGR of 22.4% through 2033, the highest across all technology segments, fueled by global 5G network densification programs and private enterprise 5G deployments across industrial sectors.

- Key Market Opportunity: The integration of IoT devices across smart cities, healthcare, and industrial automation is generating substantial connectivity demand in coverage-deficient areas, creating a high-growth opportunity for cost-effective cellular and signal repeater deployments in emerging economies.

Market Dynamics

Drivers - Rapid 5G Network Densification and Infrastructure Expansion

The global rollout of 5G networks stands as the most transformative growth driver for the network repeaters market. Densification of 5G infrastructure inherently requires a significantly higher density of signal amplification and relay equipment to compensate for higher frequency propagation limitations. According to the GSMA, 5G connections are projected to account for approximately 54% of global mobile connections by 2030, up from around 17% in 2023.

The concept of 5G Network Densification necessitates the use of small cells and Repeaters in dense urban corridors, transportation hubs, and commercial complexes where macro cell coverage alone is inadequate. Governments across the U.S., China, South Korea, and the European Union are allocating substantial spectrum and capital for 5G rollout, creating strong institutional demand for advanced repeater infrastructure that can bridge coverage gaps across both frequency bands and deployment scenarios.

Rising Mobile Data Traffic and In-Building Connectivity Demands

Exponential growth in mobile data consumption is generating unprecedented demand for reliable signal amplification. According to Cisco's Annual Internet Report, global mobile data traffic is expected to grow at a CAGR of 26% between 2020 and 2026, placing enormous strain on legacy network infrastructure. The emergence of video streaming, cloud computing, augmented reality, and mission-critical IoT applications has intensified the need for consistent indoor and outdoor connectivity.

In-Building Connectivity has become a priority for enterprises, hospitals, airports, and educational campuses, where signals from macro towers are significantly attenuated by construction materials. Regulatory bodies such as the Federal Communications Commission (FCC) in the U.S. have issued mandates requiring improved in-building cellular coverage in public safety environments, further boosting the adoption of advanced repeater systems that ensure uninterrupted Rising Mobile Data Traffic management.

Restraints - Stringent Regulatory and Certification Requirements

Network Repeaters are subject to rigorous certification and compliance standards from bodies such as the FCC in the United States, the CE marking requirements in Europe, and the Telecom Regulatory Authority of India (TRAI) in Asia Pacific. Unauthorized repeater deployment can cause signal interference, degrading network quality for other users. The compliance burden including testing, certification, and spectrum coordination increases time-to-market and adds substantially to per-unit costs.

Many smaller operators and emerging market players lack the technical expertise or financial resources to navigate these regulatory frameworks, restricting their market participation and dampening broader market penetration, especially in price-sensitive developing regions.

Technical Challenges Related to Signal Interference and Network Compatibility

Network Repeaters, particularly analog variants, can introduce signal interference that degrades overall network quality when improperly configured or deployed in spectrum-dense environments. As mobile operators transition to 5G NR and heterogeneous network (HetNet) architectures, compatibility between legacy Repeaters and next-generation infrastructure becomes a significant challenge.

The 3GPP technical standards require repeater manufacturers to continuously upgrade their product portfolios, increasing research and development (R&D) expenditure. Field deployments in complex RF environments such as dense urban areas or industrial facilities require custom engineering solutions, raising installation costs and extending deployment timelines, thereby restraining the market's speed of adoption.

Opportunities - Growing Adoption of Digital and Smart Repeaters for Next-Generation Networks

The transition from conventional analog systems to Digital & Smart Repeaters presents a high-value opportunity for market participants. Smart Repeaters, equipped with self-optimization capabilities, remote management interfaces, and AI-driven network analytics, are being increasingly adopted by mobile network operators (MNOs) seeking to reduce operational expenditure and improve quality of service (QoS).

According to the European Telecommunications Standards Institute (ETSI), smart repeater architectures aligned with O-RAN specifications enable seamless integration into cloud-native 5G networks. Countries such as South Korea and Japan have already initiated procurement programs for smart repeater solutions as part of their national 5G acceleration plans. This technological shift unlocks recurring revenue streams through software licensing, managed services, and remote diagnostics enabling vendors to build differentiated, high-margin product offerings that go beyond commodity hardware.

IoT Integration and Smart Infrastructure Deployment Across Emerging Economies

The rapid proliferation of IoT devices across sectors such as smart manufacturing, precision agriculture, smart utilities, and connected healthcare is creating a vast and underserved connectivity demand that Repeaters are uniquely positioned to fulfill. The International Data Corporation (IDC) estimates that global IoT connections will exceed 55 billion by 2025, with a significant concentration in emerging economies that still have significant network coverage deficits.

IoT Integration across logistics hubs, remote mining sites, and offshore industrial platforms requires low-latency, reliable wireless connectivity that cannot always be delivered by macro cells alone. Governments in Southeast Asia, Sub-Saharan Africa, and Latin America are investing in rural broadband programs, creating institutional procurement channels for cost-effective cellular and signal repeater solutions that can extend network reach without requiring full tower infrastructure buildout.

Category-wise Analysis

Product Type Insights

Wi-Fi Repeaters represent the leading segment within the Product Type category, commanding approximately 38% of the global network repeaters share in 2025. This dominance is underpinned by the ubiquitous adoption of Wi-Fi-enabled devices across residential, commercial, and enterprise environments. According to the Wi-Fi Alliance, over 5 billion Wi-Fi devices are shipped annually, reflecting the sheer scale of ecosystem demand. The proliferation of remote work, smart home devices, and cloud-based enterprise applications has intensified the need for seamless indoor wireless coverage, with Wi-Fi Repeaters serving as an accessible, cost-effective solution for extending router range.

Additionally, the rollout of Wi-Fi 6E and Wi-Fi 7 standards has spurred demand for next-generation Repeaters capable of operating in the 6 GHz band, further reinforcing the segment's leadership position. Vendor competition has driven down per-unit prices while improving performance, broadening the consumer and enterprise addressable market significantly.

Cellular Repeaters represent the fastest-growing segment within the product type category, projected to expand at a CAGR of approximately 11.2% through 2033. This growth is driven by operator-mandated indoor coverage improvements and the accelerating rollout of 5G NR networks globally. Telecom operators are increasingly deploying cellular Repeaters to enhance signal penetration in dense urban structures, transportation corridors, and large public venues, making this segment a priority investment area for network infrastructure providers.

Deployment Insights

Indoor repeaters hold the dominant position in the Deployment category, accounting for approximately 52% of market share in 2025. Indoor signal amplification is a critical requirement across commercial real estate, healthcare facilities, educational institutions, and enterprise campuses, where reinforced concrete and steel structures substantially attenuate cellular and Wi-Fi signals. The in-building connectivity segment has received a significant boost from regulatory mandates for instance, the FCC's rules requiring public-safety broadband coverage inside large buildings.

Enterprise adoption of BYOD (Bring Your Own Device) policies and the expansion of smart building technologies have further amplified indoor repeater deployments. Major vendors including CommScope and Corning, have developed Distributed Antenna Systems (DAS) and integrated indoor repeater platforms that cater to this high-demand segment, underpinning its sustained market leadership across both developed and emerging economies.

Mobile repeaters are emerging as the fastest-growing deployment segment, projected to grow at a CAGR of 12.1% through 2033. Demand is driven by vehicle-mounted solutions for public safety fleets, emergency response units, and maritime vessels requiring reliable mobile coverage in remote or transit environments. The integration of mobile Repeaters in first-responder vehicles and connected transportation infrastructure is creating a rapidly expanding addressable market.

Technology Insights

4G/LTE Repeaters currently dominate the Technology category, holding approximately 41% of the global market share in 2025. Despite the growing momentum of 5G, LTE remains the predominant mobile technology in large parts of Asia Pacific, Latin America, Africa, and rural North America. According to the GSMA Intelligence database, LTE accounted for approximately 52% of global mobile connections in 2023, and LTE infrastructure will continue to underpin connectivity for billions of users.

Enterprise and government networks in mid-tier economies still heavily rely on LTE for mission-critical communications, driving consistent procurement of 4G/LTE Repeaters for both new deployments and network capacity upgrades. The large installed base of LTE devices further reinforces the longevity of this segment's leadership, as operators seek to maximize return on existing infrastructure investments.

5G NR Repeaters represent the fastest-growing technology segment, with an estimated CAGR of 22.4% through 2033. As operators accelerate mmWave and sub-6 GHz 5G rollouts globally, the need for signal amplification in 5G frequency bands is intensifying rapidly. Government spectrum auctions, Open RAN adoption, and private 5G network deployments across manufacturing and logistics sectors are collectively driving robust demand for this next-generation repeater technology.

Frequency Band Insights

Mid Band Repeaters lead the Frequency Band category, representing approximately 43% of market share in 2025. Mid-band spectrum (typically 1 GHz to 6 GHz) offers an optimal balance between coverage range and data capacity, making it the preferred frequency band for both 4G LTE and 5G deployments by major mobile network operators globally.

The Federal Communications Commission (FCC) in the United States and Ofcom in the United Kingdom have both prioritized mid-band spectrum allocation for 5G services, recognizing its superior propagation characteristics compared to millimeter wave frequencies. This regulatory preference has significantly elevated operator investment in mid-band compatible repeater infrastructure. Key telecom operators such as T-Mobile, Verizon, Vodafone, and Deutsche Telekom have made mid-band deployments central to their 5G strategy, reinforcing demand for mid-band Repeaters across metropolitan and suburban coverage zones.

High Band Repeaters (mmWave) are the fastest-growing segment in the Frequency Band category, projected to grow at a CAGR of 18.9% through 2033. The ultra-high data throughput requirements of applications such as augmented reality, stadium connectivity, and dense urban enterprise environments are driving mmWave repeater adoption, particularly across the U.S., Japan, and South Korea markets, where mmWave spectrum allocations are most advanced.

End-user Insights

Service providers are dominant, accounting for approximately 36% of the global network repeaters market in 2025. Mobile network operators and internet service providers constitute the largest and most consistent buyers of network repeater equipment, driven by their ongoing obligation to maintain and upgrade network coverage and capacity for their subscriber base.

According to GSMA, global telecom operator capital expenditure (capex) exceeded US$ 300 billion in 2023, with a significant portion directed toward network densification and coverage improvement programs that directly drive repeater procurement. The service provider segment benefits from centralized procurement, long-term infrastructure contracts, and government-mandated coverage obligations (such as universal service fund requirements), ensuring a stable and recurring demand pipeline for repeater manufacturers and integrators across all major global markets.

Healthcare facilities represent a high-potential, fast-growing end-use segment, expected to expand at a CAGR of 13.5% through 2033. Hospitals and healthcare campuses are increasingly mandated to maintain uninterrupted in-building connectivity for patient monitoring systems, telehealth applications, and emergency communication networks. Regulatory requirements such as NFPA 72 in the United States mandate reliable in-building public safety communication coverage, accelerating repeater deployments across new and retrofitted healthcare infrastructure globally.

Regional Insights

North America Network Repeaters Trends

North America commands the largest share of the global network repeaters market, accounting for approximately 34% of global revenue in 2025. The region's leadership is anchored in robust 5G infrastructure investment, high enterprise IT spending, and stringent regulatory mandates for in-building public safety communication coverage. T-Mobile, AT&T, and Verizon have collectively invested over US$ 100 billion in 5G network buildout since 2020, generating sustained demand for high-performance repeater solutions across urban, suburban, and rural geographies.

The passage of the Infrastructure Investment and Jobs Act in 2021 allocated US$ 65 billion for broadband expansion across underserved communities, further stimulating repeater deployment in rural and tribal areas. Additionally, the FirstNet public safety broadband network managed by AT&T under a federal contract is driving specialized repeater procurement for first-responder communication systems, reinforcing North America's dominant market position through the forecast period.

- United States Network Repeaters Market Dominance and Growth Trends

The United States holds approximately 78% of the North American network repeaters market, representing a critical revenue concentration for global vendors. The U.S. market is growing at an estimated CAGR of 9.2% through 2033, driven by one of the world's most advanced 5G deployment programs, enterprise in-building connectivity upgrades, and federal mandates for public safety broadband.

The FCC's Citizens Broadband Radio Service (CBRS) band and its ongoing spectrum auctions have enabled enterprise-grade private LTE and 5G networks across manufacturing, logistics, and healthcare sectors, each requiring dedicated repeater infrastructure. U.S. data center expansion, smart stadium projects, and the commercial real estate sector's post-pandemic redevelopment are also creating additional demand vectors. The country's mature regulatory environment and high per-capita IT spending make it the most commercially significant single-country market in the global network repeaters landscape.

Europe Network Repeaters Trends

Europe represents the second-largest regional market, contributing approximately 26% of global network repeaters revenue in 2025. The region's market dynamics are shaped by the European Union's ambitious digital connectivity agenda, including the European Electronic Communications Code (EECC), which harmonizes spectrum regulations across member states and mandates improved indoor coverage standards. The EU's Gigabit Society targets call for all European households to have access to networks delivering at least 1 Gbps by 2030, necessitating significant investments in signal amplification infrastructure.

Germany, the United Kingdom, France, and Spain are the market's primary revenue contributors, with 5G spectrum auctions in each country having already been completed, unlocking major network densification programs. Vodafone, Deutsche Telekom, Orange, and BT Group are among the leading operators actively investing in 5G-capable repeater infrastructure. Europe's focus on sustainable infrastructure has also spurred demand for energy-efficient repeater designs, creating a technological differentiation axis for market participants.

- Germany Network Repeaters Market Driven by Industrial 5G Adoption

Germany holds approximately 22% of the European network repeaters market, growing at an estimated CAGR of 8.9% through 2033. Germany's advanced industrial base, including its globally significant automotive and manufacturing sectors, is a major driver of in-building and private 5G network deployments. The Bundesnetzagentur (Federal Network Agency) has conducted extensive spectrum auctions for industrial 5G deployment, enabling private network growth that directly requires repeater solutions. Deutsche Telekom and Vodafone Germany have both launched major 5G densification campaigns in metropolitan areas, and Germany's stringent building energy efficiency standards are driving demand for smart repeater solutions that minimize power consumption.

- United Kingdom Network Repeaters Market Boosted by Rural Connectivity

The United Kingdom accounts for approximately 19% of the European market, expanding at a CAGR of 9.4% through 2033. Ofcom's Shared Rural Network initiative, backed by government funding of £1 billion, specifically targets coverage in rural and geographic notspots, creating direct institutional demand for outdoor and mobile repeater deployments. BT/EE, Vodafone, and O2 UK are collectively investing in 5G rollout and indoor coverage improvement programs. The UK's post-Brexit independent spectrum policy also provides Ofcom with flexibility to accelerate innovative spectrum sharing models, including CBRS-equivalent frameworks that support private network and repeater deployments.

- France Network Repeaters Market Driven by Strong Regulatory Policies

France contributes approximately 16% of European market revenues, with an estimated CAGR of 8.6% through 2033. Autorité de régulation des communications électroniques (ARCEP) has implemented strict indoor coverage obligations for mobile operators, directly stimulating in-building repeater investments. France's 5G rollout accelerated following spectrum auctions in 2020 and 2021, with operators Orange, SFR, Bouygues Telecom, and Free Mobile committing to national coverage targets. France's healthcare infrastructure modernization programs and smart city initiatives in cities like Paris and Lyon are additional demand drivers for advanced repeater deployments.

- Italy Network Repeaters Market Growth Supported by Infrastructure Investments

Italy accounts for approximately 14% of the European network repeaters market, growing at a CAGR of 9.1% through 2033. Italy's National Recovery and Resilience Plan (PNRR) allocates over €6.7 billion for digital infrastructure and connectivity, including broadband expansion in underserved areas. TIM (Telecom Italia), Vodafone Italy, and WindTre are accelerating 5G deployments across major Italian cities. Italy's tourism infrastructure, including historic buildings that are notoriously challenging for signal penetration, is creating a unique niche demand for specialized indoor repeater systems designed for heritage architectural environments.

Asia Pacific Network Repeaters Trends

Asia Pacific represents the fastest-growing regional market for network repeaters, accounting for approximately 28% of global revenue in 2025 and projected to expand at the highest regional CAGR of 11.3% through 2033. The region's growth is powered by China's massive 5G deployment program, India's rapidly digitizing economy, South Korea's advanced telecom ecosystem, and ASEAN's emerging market expansion. According to GSMA Intelligence, Asia Pacific accounted for over 50% of all global 5G connections in 2023, reflecting the region's outsized role in driving next-generation wireless infrastructure adoption.

Manufacturing advantages in China, Taiwan, and South Korea have enabled regional players to offer cost-competitive repeater solutions that are increasingly exported to emerging markets globally. Government-backed rural broadband programs in India, Indonesia, Vietnam, and the Philippines are creating additional institutional demand channels, further reinforcing the region's leading growth trajectory. The ASEAN Smart Cities Network initiative is also driving urban infrastructure modernization across Southeast Asia, stimulating demand for advanced in-building and outdoor repeater deployments.

- China Network Repeaters Market Leads Regional Market Share Growth

China dominates the Asia Pacific market with approximately 41% regional share, growing at an estimated CAGR of 10.8% through 2033. China has deployed the world's largest 5G network, with over 3.6 million 5G base stations as of 2024, according to the Ministry of Industry and Information Technology (MIIT). This densification program requires extensive repeater deployments to ensure seamless indoor and outdoor coverage. Leading domestic players, including Huawei, ZTE, and Comba Telecom, are deeply embedded in the national supply chain. China's dual-use strategy for 5G covering both commercial and public safety applications further amplifies repeater procurement volumes.

- India Network Repeaters Market Exhibits Highest Growth Potential Globally

India holds approximately 18% of the Asia Pacific market, projected to grow at one of the highest country-level CAGRs of 14.2% through 2033. India's 5G rollout, which began in 2022 following spectrum auctions by DoT (Department of Telecommunications), is being led by Reliance Jio and Bharti Airtel. The government's BharatNet program aims to connect over 600,000 villages with high-speed broadband, creating extensive demand for rural repeater deployments. India's large population of digitally underserved communities and rapidly expanding smartphone penetration present a generational opportunity for network repeater manufacturers, particularly those offering cost-optimized solutions for price-sensitive market segments.

- South Korea Network Repeaters Market Driven by Advanced 5G Ecosystem

South Korea accounts for approximately 12% of Asia Pacific market revenue, with a CAGR of 9.8% projected through 2033. As the world's first country to commercially launch 5G networks in 2019, South Korea has developed a highly mature and sophisticated network repeater ecosystem. SK Telecom, KT Corporation, and LG Uplus are investing in 5G standalone (SA) network upgrades and mmWave indoor coverage solutions for enterprise and industrial use cases. South Korea's strong electronics manufacturing base supports a domestic supply chain for high-quality repeater components, while the government's focus on smart factories under the Korean New Deal is driving enterprise private network deployments that require specialized repeater solutions.

Competitive Landscape

The global network repeaters market exhibits a moderately consolidated structure, with a handful of large multinational corporations, including CommScope, Huawei, ZTE, and Ericsson, commanding significant market influence through their scale, technology portfolios, and deep operator relationships. These leaders differentiate through proprietary signal processing algorithms, interoperability with open RAN architectures, and end-to-end managed service capabilities.

Simultaneously, a fragmented mid-tier and regional vendor ecosystem competes on price, customization, and rapid deployment capabilities. Key strategic trends include partnerships with MNOs for joint network optimization, acquisition of software-defined networking (SDN) capabilities, and investment in AI-powered self-optimizing repeater platforms. Emerging business models centered on repeater-as-a-service (RaaS) are gaining traction, enabling operators to shift from capital expenditure to operational expenditure models.

Key Developments:

- January 2025: CommScope announced the expansion of its ION-E indoor cellular solution portfolio to natively support 5G NR standalone deployments, targeting large enterprise and healthcare campus customers across North America and Europe.

- September 2024: Huawei unveiled its MetaAAU intelligent active repeater at MWC Shanghai, featuring AI-driven beam management and support for both sub-6 GHz and mmWave 5G frequencies, designed for dense urban environments.

- March 2024: Corning Incorporated completed its acquisition of a minority stake in a smart DAS startup, reinforcing its in-building connectivity strategy and accelerating the integration of AI analytics into its enterprise repeater product line.

Network Repeaters Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.4 Bn |

| Current Market Value (2026) | US$ 8.9 Bn |

| Projected Market Value (2033) | US$ 16.9 Bn |

| CAGR (2026 - 2033) | 9.6% |

| Leading Region | North America, 34% |

| Dominant Segment | Wi-Fi Repeaters (Product Type), 38% |

| Top-ranking Segment | Indoor Repeaters (Deployment), 52% |

| Incremental Opportunity (2033 minus 2026) | US$ 8.0 Bn |

Companies Covered in Network Repeaters Market

- Advanced Design Network Repeaters & Signs

- KE Outdoor Design

- markilux GmbH + Co. KG

- Marygrove Network Repeaters

- Schmitz-Werke

- ShadeFX

- Somfy Systems Inc.

- Sunesta LLC

- SunSetter Products LP

- Warema Renkhoff SE

Frequently Asked Questions

The global Network Repeaters market is valued at US$ 8.9 Bn in 2026 and is projected to reach US$ 16.9 Bn by 2033, expanding at a CAGR of 9.6% during the forecast period 2026 - 2033. Historically, the market grew at a CAGR of 8.7% between 2020 and 2025.

The primary demand drivers include the global rollout of 5G networks requiring dense signal amplification infrastructure, surging mobile data traffic driven by video streaming and IoT applications, and government mandates for improved in-building public safety broadband coverage across commercial and institutional buildings.

Wi-Fi Repeaters hold the leading position in the Product Type category with approximately 38% market share as of 2025. This dominance is attributed to the widespread global adoption of Wi-Fi-enabled consumer and enterprise devices and the accelerating rollout of Wi-Fi 6E and Wi-Fi 7 standards requiring advanced signal extension solutions.

North America leads the global market, commanding approximately 34% of revenue in 2025. The region benefits from advanced 5G infrastructure investment by major operators, substantial federal broadband funding through the Infrastructure Investment and Jobs Act, and robust regulatory mandates for in-building coverage improvement.

The integration of IoT across smart cities, industrial automation, precision agriculture, and healthcare presents a high-growth opportunity. The IDC estimates global IoT connections will exceed 55 billion by 2025, creating extensive connectivity demand in areas underserved by macro cellular infrastructure, directly driving repeater adoption.

Key players in the global Network Repeaters market include CommScope Holding Company, Huawei Technologies, ZTE Corporation, Ericsson, Nokia Corporation, Corning Incorporated, Wilson Electronics (weBoost), SureCall Technologies, Nextivity Inc. (Cel-Fi), Comba Telecom Systems Holdings, and Kathrein Solution.