- Hardware & Software IT Services

- Data Center Rack Market

Data Center Rack Market Size, Share, and Growth Forecast 2026 - 2033

Data Center Rack Market by Rack Type (Open Frame Rack, Cabinet, Others), Height (Below 42 U, 42 U, above 42 U), Width (19 Inch, 23 Inch, Others), Vertical (BFSI, Government & Défense, Healthcare, IT & Telecom, Energy, Retail, Others), and Regional Analysis for 2026 - 2033

Data Center Rack Market Size and Trend Analysis

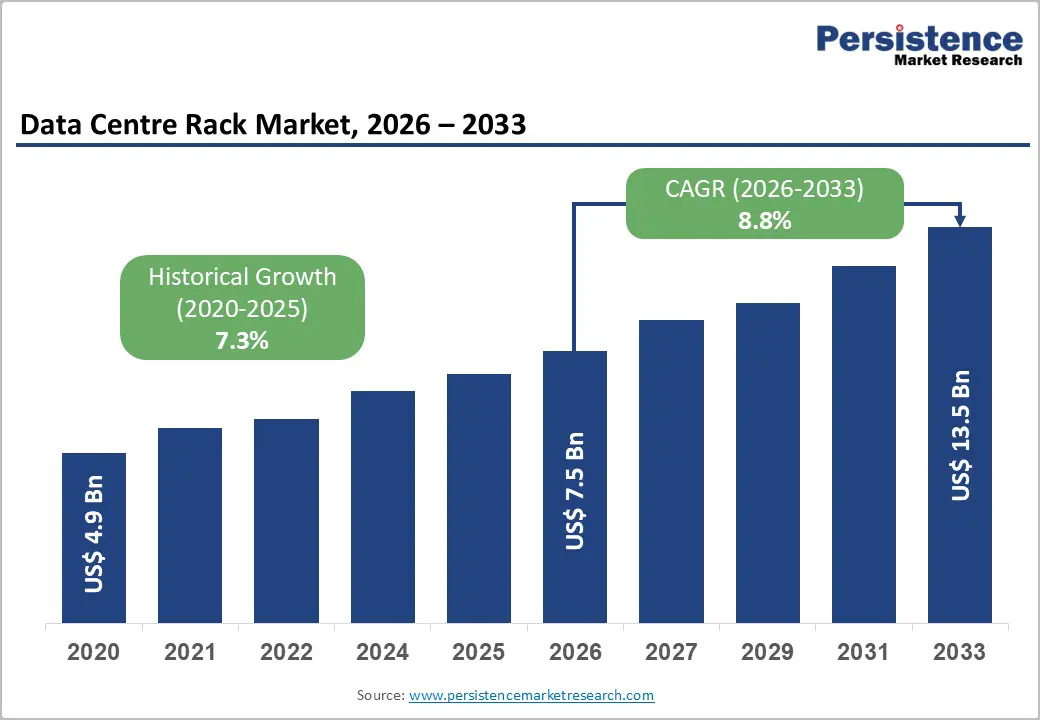

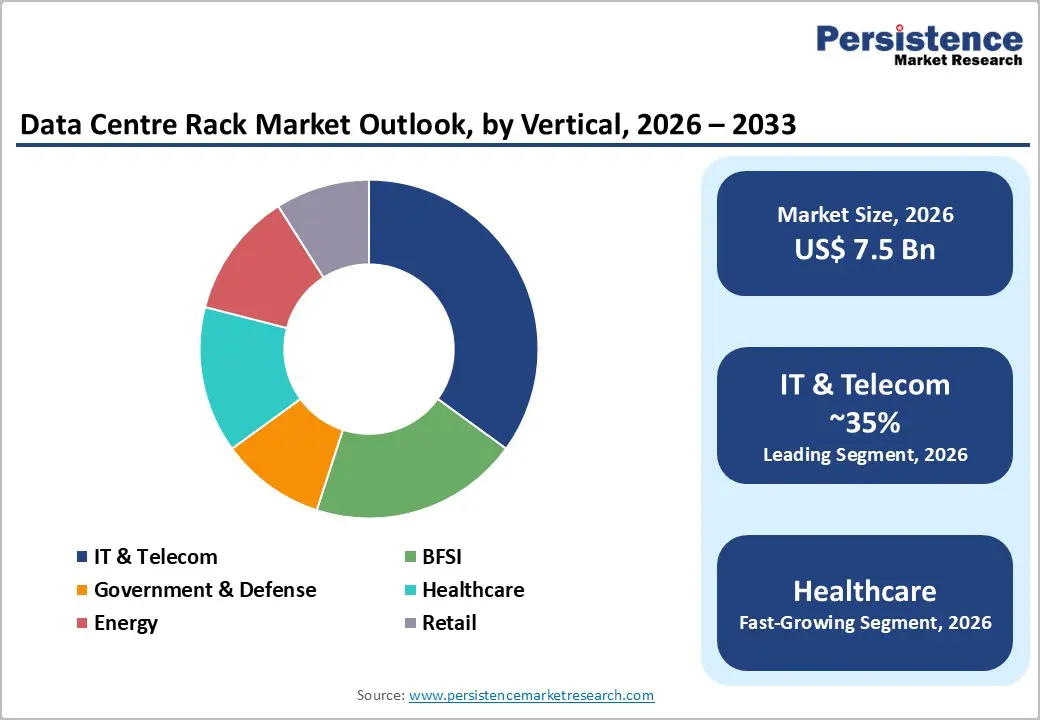

The global data center rack market size is expected to be valued at US$ 7.5 billion in 2026 and is projected to reach US$ 13.5 billion by 2033, growing at a CAGR of 8.8% between 2026 and 2033. This robust growth is driven by an unprecedented global surge in hyperscale data center construction, accelerating enterprise IT infrastructure modernization, and exponential growth in cloud computing and AI workload deployments that require dense, high-power rack configurations.

The market grew from US$ 4.9 billion in 2020 at a historical CAGR of 7.3%, underpinned by rapid digital transformation across all industry verticals, the COVID-19 pandemic's acceleration of remote work and cloud adoption, and the proliferation of IoT-connected devices.

Key Industry Highlights:

- Leading Region - North America leads the global data center rack market, driven by the world's largest hyperscale cloud operator concentration, U.S. government FedRAMP IT modernization mandates, and massive AWS, Microsoft Azure, and Google Cloud campus expansions consuming tens of thousands of racks per facility.

- Fastest Growing Region - Asia Pacific is the fastest growing market fueled by China's Eastern Data Western Computing initiative, India's Digital India data center policy, and combined multi-billion-dollar AWS, Microsoft, and Google cloud infrastructure investments across Indian metropolitan markets.

- Dominant Segment - Cabinet racks held 62% share in 2025, dominating through superior physical security, integrated cable management, and compliance with TIA-942 Tier III/IV specifications, making them the default specification for enterprise, hyperscale, and colocation data center deployments globally.

- Fastest-Growing Segment - Above-42 U racks are the fastest-growing height segment, driven by NVIDIA DGX AI supercomputer racks consuming 100+ kW, which demand taller, reinforced enclosures with liquid-cooling integration that exceed conventional 42 U rack height and structural load specifications.

- Opportunity - Schneider Electric, Rittal, and Vertiv's AI-optimized rack enclosures with integrated liquid cooling represent the highest-margin opportunity, as NVIDIA DGX GB200 deployments consuming 120 kW per rack require purpose-built enclosures incompatible with standard air-cooled data center rack infrastructure.

DRO Analysis

Drivers - Hyperscale Data Center Construction Boom Driven by Cloud and AI Workload Demand

The global acceleration of cloud computing adoption and artificial intelligence workload deployment is driving an unprecedented construction wave of hyperscale data center facilities requiring massive quantities of high-density rack infrastructure. The Synoptics Research and Data Center World reports document record capital expenditure commitments from hyperscale operators, including Microsoft Azure, Amazon Web Services (AWS), and Google Cloud, which collectively announced over US$ 200 billion in combined data center investment commitments in 2024 alone.

Each hyperscale facility requires thousands of standardized racks to house compute, storage, and networking equipment. The International Data Corporation (IDC) forecasts global data creation and replication to reach 175 zettabytes by 2025, continuously expanding the infrastructure footprint requirement. High-density AI GPU clusters consuming 30-100+ kW per rack versus traditional 5-10 kW per rack are particularly driving demand for reinforced, high-weight-capacity cabinet racks.

Enterprise Digital Transformation and Edge Computing Expansion Across Industry Verticals

Beyond hyperscale cloud operators, enterprise digital transformation programs across the BFSI, healthcare, manufacturing, and government sectors are driving significant investment in rack infrastructure for on-premises, colocation, and edge deployments. The U.S. Federal Government's Cloud Smart Strategy and FedRAMP framework are driving federal agency IT modernization with compliant rack-mounted server infrastructure.

The proliferation of edge computing, where data processing occurs close to the source rather than in centralized cloud data centers, is creating millions of new small-footprint rack deployment points across retail, manufacturing, and telecom environments. Ericsson estimates that 5G network densification will require hundreds of thousands of edge data center nodes globally by 2030, each requiring standardized rack enclosures for organized, remotely manageable compute and networking infrastructure deployment.

Market Restraints

High Capital and Operational Costs for Premium High-Density Rack Infrastructure

High-density rack cabinets engineered for AI GPU cluster workloads, featuring reinforced structures, liquid-cooling compatibility, advanced power distribution units (PDUs), and intelligent monitoring systems, command 3-8 times the cost of standard commodity open-frame racks.

For enterprise and colocation operators managing capital expenditure discipline, this cost differential creates procurement friction and can delay rack fleet upgrades. Small and mid-market enterprises with constrained IT budgets may defer investment in premium rack infrastructure, opting instead for lower-specification alternatives that can limit long-term scalability.

Floor Space Constraints and Power Density Limitations in Legacy Data Center Facilities

A significant proportion of installed data center capacity globally operates in legacy facilities designed for 5-10 kW per rack power densities, which are structurally and electrically incapable of supporting the 30-100 kW per rack requirements of modern AI and high-performance computing workloads.

The Uptime Institute's Global Data Center Survey consistently identifies power density limitations as a primary operational constraint for many enterprise data center operators. Retrofitting legacy facilities for high-density rack deployment requires costly electrical and cooling infrastructure upgrades, deterring operators from investing in rack refreshes and slowing overall market growth in the enterprise colocation segment.

Opportunities - AI-Optimized High-Density Rack Cabinets with Integrated Liquid Cooling Systems

The explosion of AI inference and training workloads, driven by the rapid commercial deployment of large language models (LLMs), generative AI platforms, and autonomous systems, is creating an urgent need for next-generation high-density rack cabinets with integrated direct liquid cooling (DLC) or rear-door heat exchanger systems. NVIDIA's DGX GB200 NVL72 AI supercomputer rack consumes up to 120 kW per rack, far exceeding the capacity of conventional air-cooled data center rack infrastructure.

Schneider Electric, Rittal GmbH & Co. KG, and Vertiv Group have all introduced dedicated AI-optimized rack enclosure product lines with integrated liquid cooling manifolds. The Uptime Institute projects that liquid-cooled racks will account for a rapidly growing share of new data center capacity by 2026, representing a premium, high-margin product category opportunity for rack manufacturers with early integration capabilities for liquid cooling.

Edge Data Center and Telecom 5G Infrastructure: Massive Distributed Rack Deployment Opportunity

The convergence of 5G network rollout, IoT device proliferation, and the deployment of latency-sensitive applications is creating a structural demand for compact, ruggedized rack enclosures in edge computing environments. Ericsson's Mobility Report forecasts approximately 5.6 billion 5G subscriptions by 2029, with associated network densification requiring distributed edge compute nodes at cell towers, manufacturing floors, retail locations, and transportation hubs.

Governments, including the U.S. (CHIPS and Science Act) and the EU (Digital Decade Policy Program) are investing in domestic digital infrastructure that includes edge data center deployments. Companies including Chatsworth Products, Panduit Corp., and Legrand are developing specialized compact and wall-mount rack products targeting the edge and telecom infrastructure segment, which is projected to be among the fastest-growing rack verticals through 2033.

Category-wise Analysis

Rack Type Insights

Cabinet racks (enclosed rack enclosures) dominate the Rack Type segment with approximately 62% market share in 2025. Cabinet racks are the preferred choice for enterprise and hyperscale data center deployments due to their superior physical security, preventing unauthorized access to critical IT equipment, and integrated cable management, blanking panels, and PDU mounting capabilities that support structured, high-density deployments.

The TIA-942 Telecommunications Infrastructure Standard for Data Centers and ANSI/EIA-310 standards specify enclosed cabinet racks as the default for Tier III and Tier IV data center designs, where security, organization, and thermal management are paramount. Leading manufacturers, including Rittal GmbH & Co. KG and Schneider Electric, maintain extensive cabinet rack product portfolios with optional integrated cooling, intelligent PDUs, and remote monitoring capabilities that further differentiate cabinets from open-frame alternatives.

Height Insights

The 42 U (unit) height specification is the dominant standard in the Height segment, holding approximately 58% market share in 2025. The 42 U racks standing approximately 2,000 mm in height have been the global industry standard for data center rack infrastructure since their adoption in EIA-310-D and IEC 60297 standards. This standardization ensures universal compatibility with the vast majority of rack-mounted server, storage, networking, and power distribution equipment from all major vendors, including Dell Inc., Hewlett Packard Enterprise, and Cisco Systems, Inc.

The 42 U format balances equipment hosting capacity with practical accessibility for technician maintenance and cable management. Above-42 U racks are gaining share in hyperscale deployments requiring maximum equipment density per floor tile, but the installed base and procurement standard for 42 U remains overwhelmingly dominant across enterprise and colocation markets globally.

Width Insights

The 19-inch rack width is the dominant Width specification, accounting for approximately 78% market share in 2025. The 19-inch rack width has been the universal standard for IT equipment mounting since it was established by ANSI/EIA-310 and subsequently adopted by IEC 60297 and DIN 41494. Virtually all rack-mounted server, storage, network switch, patch panel, and UPS products from vendors including IBM, Cisco, and Fujitsu are designed to the 19-inch mounting standard.

The 23-inch width maintains a niche presence in telecommunications central office environments where legacy telco equipment requires wider mounting, but the near-universal adoption of 19-inch racks across enterprise IT ensures its continued commanding dominance in the global data center rack market.

Vertical Insights

IT & Telecom is the dominant Vertical segment, accounting for approximately 35% of the total data center rack market share in 2025. The IT & Telecom vertical encompasses cloud service providers, managed service providers, internet service providers, and telecommunications operators collectively operating the world's largest data center footprints and consuming the highest volumes of rack infrastructure.

The International Telecommunication Union (ITU) reports that global internet traffic continues growing at double-digit annual rates, requiring continuous data center capacity expansion. Hyperscale cloud operators, including AWS, Microsoft Azure, and Google Cloud, represent the highest individual procurement volumes per buyer for standardized rack cabinet orders, with new hyperscale facilities consuming tens of thousands of racks per deployment. This concentration of demand in IT & Telecom buyers reinforces the segment's dominant revenue share.

Regional Analysis

North America Data Center Rack Market Trends & Analysis

North America leads the global data center rack market, supported by the world's highest concentration of hyperscale data centers, active enterprise IT modernization programs, and the largest cloud computing market globally. The U.S. Department of Energy estimates that U.S. data centers consume approximately 200 TWh of electricity annually, reflecting the immense scale of installed compute infrastructure driving rack demand. Major hyperscale campus expansions in Virginia, Texas, Arizona, and Nevada are sustaining multi-year rack procurement pipelines for leading suppliers.

U.S. Data Center Rack Market Size

The United States accounts for approximately 80% of North American data center rack market revenue in 2025, representing the world's single largest national market. The U.S. hosts the largest concentration of hyperscale data centers globally, with Northern Virginia being the world's densest data center market per CBRE Research data. Federal IT modernization under FedRAMP compliance and the CHIPS and Science Act's digital infrastructure investments sustain institutional procurement of compliant rack enclosures at scale.

Europe Data Center Rack Market Trends, Drivers & Insights

Europe is a mature and sustainability-regulated data center rack market, shaped by the EU Green Deal, European Green Deal Digital Strategy, and the EU Code of Conduct on Data center Energy Efficiency, mandating PUE improvements across European data center operators. Frankfurt, Amsterdam, London, and Dublin, collectively known as the FLAP-D markets, remain the continent's primary data center deployment hubs, driving concentrated rack procurement from both hyperscale and colocation operators.

Germany Data Center Rack Market Size

Germany holds approximately 25% of European data center rack market revenue in 2025. Frankfurt is Europe's largest data center market by capacity, hosting major AWS, Microsoft, and Google cloud regions alongside leading colocation providers. Rittal GmbH & Co. KG's German headquarters and manufacturing base reinforce the country's role as both a key demand market and a leading rack production center, with domestic market knowledge informing product development for European enterprise customers.

U.K. Data Center Rack Market Size

The United Kingdom represents approximately 19% of European data center rack market revenue in 2025. London's Docklands and Slough corridors host Europe's second-largest data center cluster, with active AWS, Microsoft Azure, and Google Cloud regions driving hyperscale rack procurement. Post-Brexit regulatory independence has not diminished the UK's appeal as a data center investment destination, with UK Government's designation of data centers as critical national infrastructure supporting continued sector investment.

France Data Center Rack Market Size

France accounts for approximately 13% of the European data center rack market revenue in 2025. Paris is a significant European data center market, with Microsoft's French cloud region and growing colocation operator investment driving rack procurement. France's Strategies Nationales pour le Cloud and government-sponsored Campus Cyber cybersecurity infrastructure are driving public-sector data center investment, including standardized rack enclosure procurement for secure government and Défense IT infrastructure.

Asia Pacific Data Center Rack Market Drivers & Analysis

Asia Pacific is the fastest-growing regional data center rack market, driven by massive digital infrastructure investment across China, India, Japan, Singapore, and Australia. China alone accounts for approximately 38% of the Asia Pacific demand, with domestic hyperscale operators including Alibaba Cloud, Tencent Cloud, and Huawei Cloud expanding national data center footprints at scale. China's 14th Five-Year Plan and Eastern Data Western Computing initiative are directing massive investment in data center infrastructure across multiple provinces.

China Data Center Rack Market Size

China accounted for approximately 38% of the Asia-Pacific data center rack market revenue in 2025. China's Eastern Data Western Computing project, connecting eastern demand centers with western renewable energy sources, is driving the construction of large-scale data centers in multiple provinces, each requiring tens of thousands of racks. Domestic manufacturers, including Inspur Group and H3C Group, supply the majority of China's rack enclosure demand alongside international brands.

India Data Center Rack Market Size

India represents approximately 15% of the Asia Pacific data center rack market revenue in 2025 and is growing rapidly. India's Digital India program and the National Data Center Policy are stimulating domestic data center investment, with Mumbai, Chennai, Pune, and Hyderabad emerging as major hubs. Amazon Web Services, Microsoft, and Google have announced combined multi-billion-dollar investments in Indian cloud infrastructure that are driving sustained demand for rack procurement.

Japan Data Center Rack Market Size

Japan contributes approximately 13% of the Asia Pacific data center rack market revenue in 2025. Japan's advanced enterprise IT sector, anchored by NTT Data Corporation, Fujitsu, and Hitachi, drives consistent high-quality cabinet rack procurement for enterprise and government data centers. Japan's strict seismic safety requirements mandate robust, earthquake-rated rack enclosures across all data center deployments, sustaining premium product specification and supporting Rittal and Schneider Electric's premium market positions in the Japanese data center sector.

Competitive Landscape

The global data center rack market exhibits a moderately consolidated competitive structure, with multinational infrastructure companies including Schneider Electric, Rittal GmbH & Co. KG, Legrand, and Eaton competing alongside IT OEM rack solutions from Hewlett Packard Enterprise, Dell Inc., and Cisco Systems, Inc.

Key differentiators include intelligent rack monitoring via integrated PDUs and environmental sensors, AI-optimized liquid cooling compatibility, modular design for rapid deployment, and compliance with TIA-942, ANSI/EIA-310, and regional seismic standards. Emerging trends include integrated rack-level liquid cooling solutions, as-a-service rack lifecycle management models, and digital twin software for rack capacity planning.

Key Developments:

- In June 2025, Schneider Electric announced the launch of data center solutions to meet the difficulties of high-density AI (artificial intelligence) and fast-tracked compute implementations. New rack systems and rack PDUs (Power Distribution Units) are being developed for increased weight capacity and larger sizes, featuring direct-to-chip liquid cooling.

- In July 2025, Vertiv announced the acquisition Great Lakes Data Racks & Cabinets group of enterprises (combinely “Great Lakes”) for USD 200 million. The incorporation of Great Lakes’ expertise with Vertiv's current offering is expected to offer substantial customer benefits through combined infrastructure sourcing and pre-engineered solutions.

Companies Covered in Data Center Rack Market

- AMCO Enclosures

- Belden Inc.

- Chatsworth Products

- Cisco Systems Inc.

- Dell Inc.

- Eaton Corporation

- Fujitsu

- Hewlett Packard Enterprise

- IBM

- Legrand

- Panduit Corp.

- Rittal GmbH & Co. KG

- Schneider Electric

- Vertiv Group Holdings

Frequently Asked Questions

The global data center rack market is projected to reach US$ 13.5 billion by 2033, growing from an estimated US$ 7.5 billion in 2026 at a CAGR of 8.8%.

Primary demand drivers include hyperscale cloud operator capital expenditure with AWS, Microsoft, and Google announcing over US$ 200 billion in combined 2024 data center investment commitments and AI workload density growth, with NVIDIA DGX GPU racks consuming 30-120 kW per rack versus standard 5-10 kW.

Cabinet racks are the leading segment with approximately 62% market share in 2025. Their dominance reflects superior physical security, structured cable management, integrated PDU and cooling accessory compatibility, and compliance with TIA-942 Tier III/IV data center standards.

North America leads the global data center rack market, anchored by the U.S. which holds approximately 80% of North American market revenue. The world's largest concentration of hyperscale cloud data centers in Northern Virginia, Texas, and Arizona, combined with FedRAMP federal IT modernization mandates and the CHIPS and Science Act digital infrastructure investment, sustain North America's dominant market position through the forecast period.

Leading companies include Schneider Electric, Rittal GmbH & Co. KG, Eaton Corporation, Legrand, Vertiv Group Holdings, Panduit Corp., Chatsworth Products, Belden Inc., Dell Inc., Hewlett Packard Enterprise, Cisco Systems, Inc., and IBM.