- Advanced Materials

- Natural Rubber Market

Natural Rubber Market Size, Share, and Growth Forecast 2026 - 2033

Natural Rubber Market by Product Type (RSS Grade, Latex Concentrate, Solid Block Rubber, Others), by Application (Auto-Tire Sector, Gloves, Footwear, Latex Products, Others), and Regional Analysis for 2026 - 2033

Natural Rubber Market Size and Trend Analysis

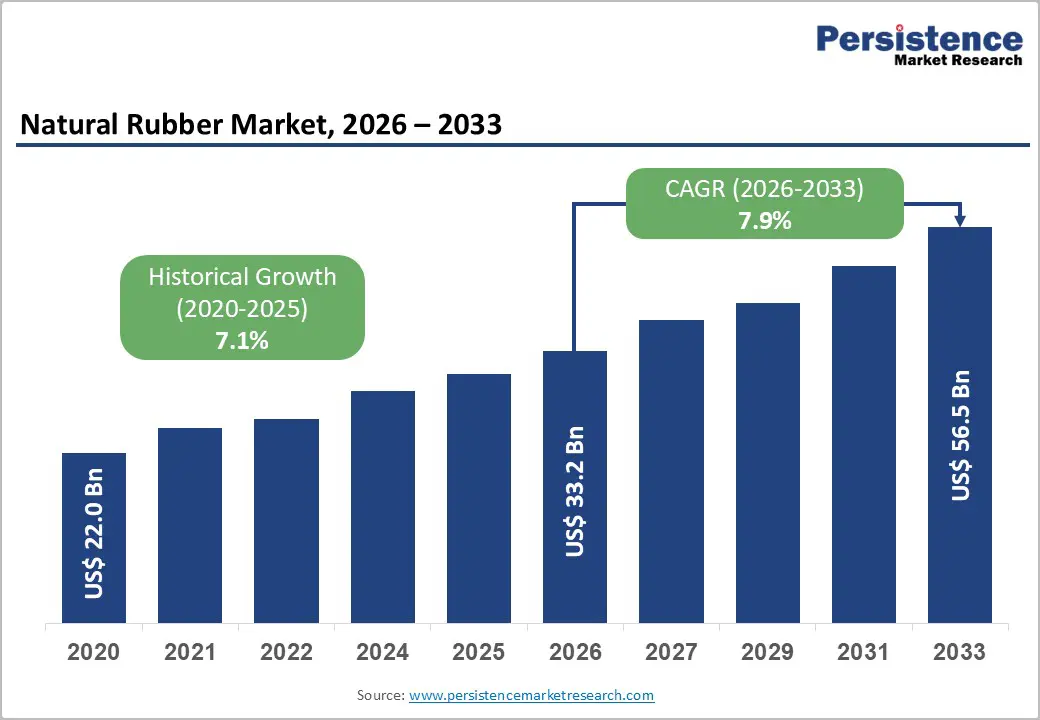

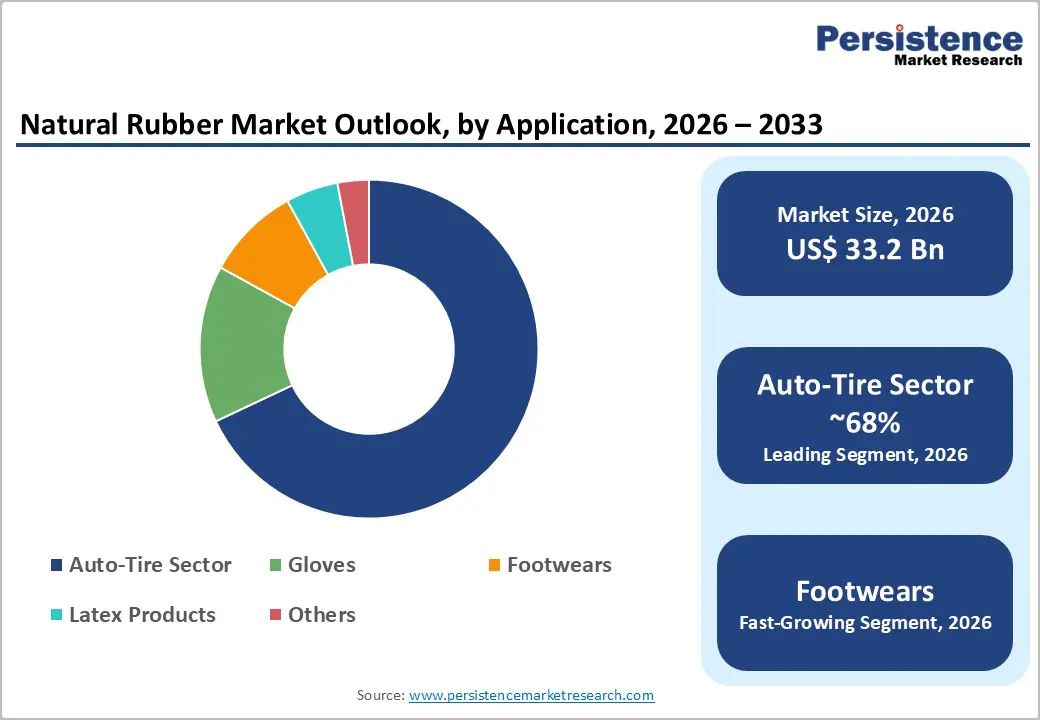

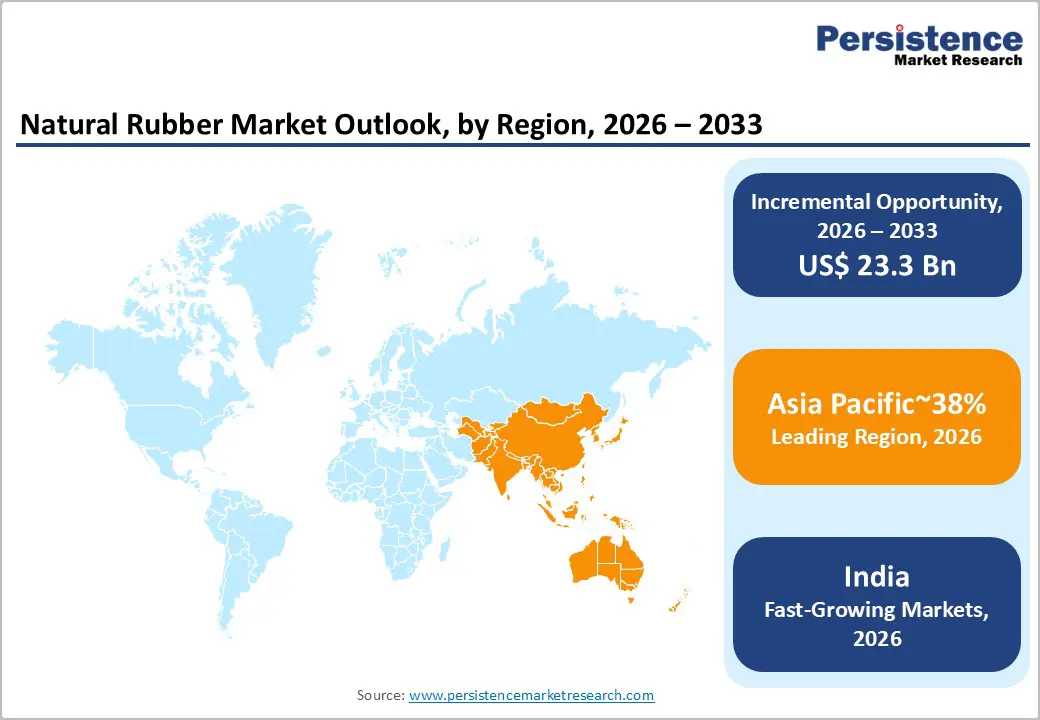

The global Natural Rubber market size is supposed to be valued at US$ 33.2 Billion in 2026 and is projected to reach US$ 56.5 Billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

The global Natural Rubber market is experiencing structurally reinforced growth, driven by the irreplaceable functional properties of natural rubber in high-performance tire manufacturing, the global medical glove sector's post-pandemic demand normalization at an elevated baseline, and the accelerating automotive and industrial production recovery across Asia Pacific and emerging market economies that sustain above-average natural rubber procurement volumes.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the global Natural Rubber market as both dominant production and consumption geography, with Thailand's OAE documenting 4.5–5.0 million tonnes annual production, ANRPC's documented 85%+ global supply from Asia Pacific, Sri Trang's 1.5 million tonne processing capacity, and China's position as the world's largest natural rubber importing and tire manufacturing economy sustaining structural regional market leadership.

- Fastest Growing Country: India is the fastest-growing consumption market, driven by India's Rubber Board documented domestic consumption growth, ASEAN automotive and medical glove manufacturing expansion.

- Dominant Product Type: Solid Block Rubber dominates the Product Type segment with approximately 46% revenue share, anchored by ISO 2000 Technically Specified Rubber (TSR 20/SIR 20) as the global tire manufacturer standard procurement grade, Sri Trang and Thai Hua massive solid block processing and export volumes.

- Dominant Application: The Auto-Tire sector is the dominant Application segment with approximately 68% revenue share, confirmed by IRSG's documented tire industry 70% global natural rubber consumption share, OICA's 85 million unit annual global vehicle production, Bridgestone's ¥4.68 trillion FY2023 tire revenues, and the irreplaceable role of high-cis natural rubber in high-performance radial tire compound formulations driving consistent structural procurement growth.

- Key Market Opportunity: EUDR-compliant sustainable rubber supply chain certification and diversification into specialty non-tire industrial rubber applications represent the dual key market opportunities, with EU Deforestation Regulation mandatory due diligence mandates creating premium value for GPSNR-certified processors, Michelin's 100% sustainable sourcing commitment, seismic bearing and medical device demand growth, and APICCAPS' 22 billion pair global footwear production sustaining natural rubber specialty grade diversification revenue growth through 2033.

| Key Insights | Details |

|---|---|

|

Natural Rubber Market Size (2026E) |

US$ 33.2 Billion |

|

Market Value Forecast (2033F) |

US$ 56.5 Billion |

|

Projected Growth CAGR (2026–2033) |

7.9% |

|

Historical Market Growth (2020–2025) |

7.1% |

DRO Analysis

Drivers - Global Automotive Production and Tire Manufacturing Scale Driving Structural Natural Rubber Demand Growth

The global automotive tire industry is the single most commercially dominant demand driver for the natural rubber market, with the International Rubber Study Group (IRSG) documenting that the tire sector accounts for approximately 70% of total global natural rubber consumption, reflecting the irreplaceable role of high-cis polyisoprene natural rubber in high-performance radial tire sidewall and bead area compound formulations where its superior tensile strength, tear resistance, and heat build-up management properties cannot be fully replicated by synthetic rubber alternatives.

The International Organization of Motor Vehicle Manufacturers (OICA) documents global vehicle production exceeding 85 million units annually, with each passenger car tire set requiring approximately 7–10 kg of natural rubber per vehicle and commercial truck and off-highway tires requiring 50–100 kg or more per unit, collectively sustaining multi-million tonne annual natural rubber procurement from tire manufacturers. Bridgestone Corporation, the world's largest tire manufacturer by revenue, and Michelin Group, are among the largest single institutional natural rubber procurement entities globally, with combined annual natural rubber sourcing volumes representing a structurally significant share of global supply that creates long-term supply chain partnership relationships with major plantation and processing conglomerates including Sri Trang Agro-Industry Plc and Thai Hua Rubber Public Company Limited.

Global Medical Glove Sector Structural Demand Elevation Post-Pandemic Sustaining Latex Concentrate Natural Rubber Consumption

The global medical examination and surgical glove sector, transformed by the COVID-19 pandemic into one of the highest-profile natural rubber latex demand drivers, has sustained post-pandemic consumption at structurally elevated levels above pre-2020 baselines, driven by healthcare infection control standard upgrades, mandatory personal protective equipment (PPE) stockpile regulations implemented by health ministries across the U.S., EU, India, and other major healthcare systems, and the expanding global healthcare infrastructure investment in emerging economies. The World Health Organization (WHO) has consistently emphasized hand hygiene and examination glove use as foundational infection prevention practices, reinforcing institutional healthcare procurement of latex examination gloves as a standard and recurrent medical supply category.

Malaysian Rubber Board (MRB), the government agency overseeing Malaysia's natural rubber industry, documents that Malaysia remains the world's dominant latex concentrate and latex glove manufacturing geography, with Thai Rubber Latex Group Public Company Limited and Von Bundit Co. Ltd. supplying concentrated latex to glove manufacturers across Malaysia, Thailand, and globally. The Association of Natural Rubber Producing Countries (ANRPC) annual natural rubber demand data confirms latex-based products as the second-largest natural rubber consumption category after tires, sustaining above-average revenue growth through the forecast period.

Restraints - Price Volatility of Natural Rubber Driven by Climate Events and Speculative Trading Constraining Supply Chain Stability

Natural rubber commodity prices, traded on the Tokyo Commodity Exchange (TOCOM), Singapore Exchange (SGX), and Shanghai Futures Exchange (SHFE), are subject to significant inter-year and seasonal price volatility driven by Southeast Asian plantation yield fluctuations from El Niño and La Niña climate events, speculative financial trading activity, and demand-side automotive production cycle changes that collectively create procurement cost unpredictability for tire manufacturers and latex product producers.

The International Rubber Study Group (IRSG) has documented natural rubber price fluctuations spanning from approximately US$ 1.0/kg to US$ 4.5/kg within single decade periods, a volatility range that creates serious revenue planning and margin management challenges for natural rubber processors and downstream product manufacturers dependent on stable input cost environments for profitable operations.

Land Availability Constraints and Hevea Plantation Disease Risk Limiting Supply Expansion Capacity

Global natural rubber supply expansion is constrained by the geographic concentration of viable Hevea brasiliensis cultivation across a relatively narrow tropical equatorial belt spanning 15 degrees north and south of the equator, limiting new plantation development to Thailand, Indonesia, Vietnam, Cambodia, Myanmar, and parts of West Africa where suitable soil, rainfall, and temperature conditions exist.

The Food and Agriculture Organization (FAO) has documented growing land use competition between rubber plantations and food crop production, palm oil, and conservation forest in Southeast Asian growing regions, while the recurring threat of South American Leaf Blight (SALB) caused by the fungal pathogen Microcyclus ulei represents a potentially catastrophic biological risk to global Hevea plantation productivity if it spreads from Latin America to Asian growing regions, as documented in research published by the CGIAR Research Program on Roots, Tubers and Bananas.

Opportunities - Sustainable and Deforestation-Free Natural Rubber Supply Chain Certification Creating Premium Market Differentiation Opportunity

The global tire and natural rubber consuming industries are undergoing a structural transformation driven by the European Union Deforestation Regulation (EUDR), which came into effect and requires companies placing natural rubber, timber, palm oil, soy, cattle, cocoa, and coffee-derived products on the EU market to demonstrate that their supply chains are deforestation-free and compliant with producing country land-use laws. The EUDR's natural rubber provisions directly mandate due diligence and geolocation documentation for all rubber plantation areas supplying EU-bound tire and latex product manufacturers, creating a premium commercial opportunity for certified sustainable natural rubber producers and processors who invest in Rainforest Alliance, Forest Stewardship Council (FSC), or Sustainable Natural Rubber Initiative (SNR-i)-compliant supply chain traceability platforms.

Halcyon Agri Corporation Limited, one of the world's largest natural rubber supply chain integration companies, has been actively developing its Corrie MacColl certified sustainable natural rubber supply platform directly targeting EUDR-compliant supply chain requirements from European tire and automotive OEM customers. The Global Platform for Sustainable Natural Rubber (GPSNR), a multi-stakeholder industry initiative supported by Bridgestone, Michelin, and Continental, is developing shared due diligence tools and supplier certification systems that create a structured commercial advantage for plantation operators and processors investing in documented sustainable rubber supply chain compliance ahead of EUDR enforcement timelines.

Growing Demand for Natural Rubber in Non-Tire Industrial Applications, Including Seismic Bearings, Medical Devices, and Sustainable Footwear, Diversifying Revenue Base

Beyond the traditionally dominant tire and glove end-use categories, natural rubber is experiencing accelerating demand growth in diversified industrial and specialty application segments that offer above-average margin potential and supply chain resilience benefits for natural rubber processors investing in application-specific product development. Seismic isolation bearings for earthquake-resistant building and bridge construction, manufactured using high-grade natural rubber compounds, represent a growing institutional procurement category in seismically active geographies including Japan, China's infrastructure development programs, India's national infrastructure pipeline, and Southeast Asian construction markets.

Sri Trang Agro-Industry Plc, the world's largest natural rubber processor and exporter by volume, and Southland Rubber Company Limited are among the natural rubber processors actively diversifying their product portfolios toward specialty compound grades serving industrial vibration isolation, healthcare, and high-performance footwear application segments. The World Footwear Yearbook published by APICCAPS documents that global footwear production exceeds 22 billion pairs annually, with natural rubber outsole and midsole specification sustaining consistent demand from premium footwear, safety boot, and sports shoe manufacturers globally where natural rubber's grip, flexibility, and wear resistance properties sustain its preferred material status versus synthetic rubber alternatives.

Category-wise Analysis

By Product Type Insights

Solid Block Rubber (SBR/TSR Grade) leads the global Natural Rubber market by product type, commanding approximately 46% of total product type segment revenue in 2026, a dominant position anchored in its status as the primary processing form in which Thailand Standard Rubber (TSR), Indonesian Standard Rubber (SIR), and Technically Specified Rubber (TSR 20) grade natural rubber is processed, baled, and exported from major producing countries to tire manufacturers globally. The Association of Natural Rubber Producing Countries (ANRPC) documents that Technically Specified Rubber in solid block form, standardized under ISO 2000 international quality grading, accounts for the majority of natural rubber trade volume between producing country processors and tire industry consumers, as its standardized dry rubber content (DRC), dirt content, ash content, and plasticity retention specifications enable consistent compound formulation by tire manufacturers.

Sri Trang Agro-Industry Plc and Thai Hua Rubber Public Company Limited are among the world's largest solid block rubber processors and exporters serving Bridgestone, Michelin, and Sinochem Group tire manufacturing procurement programs. RSS (Ribbed Smoked Sheet) Grade holds approximately 24% of product type revenue, primarily serving specialty industrial and export markets. Latex Concentrate holds approximately 22%, dominated by Malaysian and Thai latex processing for global glove manufacturer supply chains.

By Application Insights

Auto-Tire Sector leads the global Natural Rubber market by application, commanding approximately 68% of total application segment revenue in 2026, confirmed by the International Rubber Study Group (IRSG) documenting the tire sector's approximately 70% share of global natural rubber consumption, reflecting the automobile and commercial vehicle tire industry's foundational and irreplaceable dependence on natural rubber's unique combination of high tensile strength (25–30 MPa), excellent tear resistance, and low heat build-up during dynamic flexing that synthetic polyisoprene rubber cannot fully replicate in demanding tire compound formulations.

Bridgestone Corporation's FY2023 revenues of approximately ¥4.68 trillion (approx. US$ 31 billion) and Michelin Group's FY2023 revenues of approximately €28.3 billion confirm the tire sector's immense scale as a natural rubber procurement driver, with each company's compound laboratory specifying natural rubber sourcing requirements that shape global TSR 20 and SVR 20 grade procurement from processors including Sri Trang, Thai Hua, and Von Bundit. Gloves hold the second-largest application share at approximately 14%, driven by medical latex examination gloves sustaining post-pandemic elevated procurement volumes. Footwear holds approximately 8%, serving both premium natural rubber sole manufacturing and mass-market footwear.

Regional Analysis

North America Natural Rubber Trends & Insights

The United States leads North American Natural Rubber market consumption, anchored by its position as one of the world's largest automotive tire manufacturing and consumption markets, with the Rubber Manufacturers Association (RMA) and its successor U.S. Tire Manufacturers Association (USTMA) documenting consistent domestic tire shipment volumes exceeding 300 million passenger and light truck tires annually. North American tire plants operated by Bridgestone, Michelin, Goodyear, and Continental collectively procure multi-hundred-thousand-tonne volumes of natural rubber annually from Southeast Asian processors, sustaining the U.S. as the world's third-largest natural rubber import destination after China and EU. The EUDR-analogous sustainability sourcing pressure from U.S. automaker corporate sustainability commitments is driving natural rubber supply chain transparency investments among North American tire producers.

Canada and Mexico contribute secondary but commercially meaningful North American natural rubber consumption, with Mexico's OICA-documented vehicle manufacturing production exceeding 3.5 million vehicles annually sustaining domestic tire compound and rubber product natural rubber procurement. The U.S. International Trade Commission (USITC) monitors natural rubber import trade flows confirming Thailand, Indonesia, and Vietnam as the dominant natural rubber supplying countries to the North American market. The Guayule (Parthenium argentatum) domestic natural rubber research program, funded by the USDA Agricultural Research Service (ARS) as a strategic alternative domestic natural rubber source, represents North America's long-term supply chain resilience investment that could partially reduce import dependency for natural rubber in future decades.

Europe Natural Rubber Trends & Insights

Europe is the world's most sustainability-regulation-active natural rubber consuming geography, with the European Union Deforestation Regulation (EUDR) directly mandating deforestation-free supply chain due diligence for natural rubber placed on EU markets, creating the world's most stringent institutional natural rubber sourcing compliance framework that is progressively reshaping European tire manufacturer and latex product producer supply chain investment priorities toward certified sustainable sourcing platforms. Germany, France, Spain, and the UK collectively represent Europe's largest natural rubber consuming economies, anchored by tire manufacturing plants operated by Continental AG, Michelin Group, and Bridgestone European manufacturing facilities that together procure substantial annual natural rubber volumes from Southeast Asian processors.

The European Tyre and Rubber Manufacturers Association (ETRMA) actively participates in the Global Platform for Sustainable Natural Rubber (GPSNR) alongside major European tire manufacturers, coordinating industry-wide responses to EUDR compliance requirements, developing shared smallholder farmer support programs for GPSNR-certified sustainable rubber production, and communicating European industry's commitment to deforestation-free rubber supply chains to producing country governments and EU regulators. Halcyon Agri Corporation's Corrie MacColl certified sustainable rubber supply chain platform is particularly commercially relevant to European buyers, serving as a certification-compliant supply channel for EU-market-bound natural rubber volumes from Halcyon's West African and Southeast Asian plantation and processing operations.

Asia Pacific Natural Rubber Trends & Insights

Asia Pacific is both the world's dominant natural rubber production geography and the largest consumption market, anchored by Thailand's status as the world's largest natural rubber producer with the Office of Agricultural Economics (OAE) of Thailand's Ministry of Agriculture and Cooperatives documenting annual rubber production of approximately 4.5–5.0 million tonnes, Indonesia's second-largest global producer position documented by Indonesia's Ministry of Agriculture (Kementan), and China's position as the world's largest natural rubber importing and consuming country where tire manufacturing, latex gloves, and industrial rubber products sustain multi-million tonne annual import procurement volumes.

The Association of Natural Rubber Producing Countries (ANRPC) documents Thailand, Indonesia, Vietnam, Cambodia, and Myanmar collectively contributing over 85% of global natural rubber production, confirming Asia Pacific's structural dominance of the global natural rubber supply chain.

Sri Trang Agro-Industry Plc (headquartered in Bangkok, Thailand), the world's largest natural rubber processor by volume with annual processing capacity exceeding 1.5 million tonnes, and Thai Hua Rubber Public Company Limited, Von Bundit Co. Ltd., and Thai Rubber Latex Group Public Company Limited represent Thailand's four most commercially significant natural rubber processing and export conglomerates serving global tire manufacturer supply chains.

India's Rubber Board of India, the statutory body under the Ministry of Commerce and Industry governing India's natural rubber sector, documents India as both the world's fourth-largest natural rubber producer (Kerala accounting for approximately 80% of domestic production) and one of the fastest-growing natural rubber consuming economies, with Apcotex Industries Limited (headquartered in Mumbai, Maharashtra, India) serving India's latex and synthetic rubber downstream industries.

Competitive Landscape

The global Natural Rubber market is moderately consolidated at the primary processing and export level, with Sri Trang Agro-Industry Plc, Halcyon Agri Corporation, Thai Hua Rubber, and Von Bundit collectively accounting for a dominant share of global processed natural rubber export volumes from Southeast Asian producing countries. The downstream tire and latex consuming industry is highly consolidated, with Bridgestone, Michelin, Continental, and Goodyear collectively purchasing the majority of global natural rubber trade volumes.

Key differentiators include GPSNR sustainable sourcing certification, EUDR-compliant traceability platforms, processing grade quality consistency, and integrated plantation-to-processing vertical ownership. Emerging business model trends include blockchain-enabled supply chain traceability, direct smallholder farmer sustainability partnerships, and sustainability-linked supply agreements with European tire OEM customers.

Key Developments:

- In January 2025, Sri Trang Agro-Industry Plc expanded its EUDR-compliant geolocation traceability platform, covering over 500,000 smallholder rubber farmer plots in Thailand and Indonesia, positioning itself as Asia Pacific's most EUDR-prepared natural rubber exporter targeting European tire manufacturer customers facing imminent deforestation regulation compliance deadlines.

- In September 2024, Halcyon Agri Corporation Limited announced a strategic sustainability partnership with a leading European tire manufacturer through its Corrie MacColl certified sustainable natural rubber supply chain, providing fully traceable, deforestation-free natural rubber volumes from West African and Southeast Asian operations certified under GPSNR and Rainforest Alliance frameworks.

- In March 2024, Michelin Group published its updated Sustainable Natural Rubber Policy committing to 100% verified sustainable natural rubber sourcing by 2050 with interim 2025 milestones, reinforcing the structural commercial advantage for GPSNR-certified rubber processors including Sri Trang, Thai Hua, and Von Bundit in European and global tier-1 tire manufacturer supply chain qualification programs.

Companies Covered in Natural Rubber Market

- Apcotex Industries Limited

- Bridgestone Corporation

- Halcyon Agri Corporation Limited

- Michelin Group

- Sinochem Group

- Southland Rubber Company Limited

- Sri Trang Agro-Industry Plc

- Thai Hua Rubber Public Company Limited

- Thai Rubber Latex Group Public Company Limited

- Von Bundit Co. Ltd.

- Continental AG

- Goodyear Tire & Rubber Company

Frequently Asked Questions

The global Natural Rubber market is estimated to be valued at US$ 33.2 Billion in 2026 and is projected to reach US$ 56.5 Billion by 2033, registering a forecast CAGR of 7.9% from 2026 to 2033.

The primary drivers are the IRSG-documented tire sector's 70% share of global natural rubber consumption, sustained by OICA's global 85 million unit annual vehicle production and Bridgestone and Michelin's multi-hundred-thousand-tonne annual TSR procurement, and the WHO-reinforced healthcare examination glove procurement growth driving latex concentrate demand elevation at structurally above-pre-pandemic baseline levels across U.S., EU, and emerging market healthcare systems through the 2026–2033 forecast period.

Solid Block Rubber leads the Product Type segment with approximately 46% revenue share in 2026, anchored by ISO 2000 Technically Specified Rubber (TSR 20/SIR 20) as the global tire manufacturer standard procurement form, Sri Trang Agro-Industry Plc's world-leading 1.5 million tonne annual processing capacity in solid block rubber, and ANRPC trade data confirming solid TSR/SIR block rubber as the dominant natural rubber trade form shipped from Thailand, Indonesia, and Vietnam to global tire manufacturing supply chains.

Asia Pacific leads the global Natural Rubber market, anchored by Thailand's OAE documented 4.5–5.0 million tonnes annual rubber production, ANRPC's confirmed 85%+ global supply contribution from Asian producers, Sri Trang Agro-Industry Plc's Bangkok-headquartered world-largest natural rubber processing operations, China's position as the world's largest natural rubber consumer, and India's Rubber Board documented domestic natural rubber production and consumption growth across Kerala plantation and downstream industrial rubber sectors.

The most significant opportunity is EUDR-compliant sustainable natural rubber supply chain certification, with EU Deforestation Regulation mandatory deforestation-free due diligence requirements, Michelin's commitment to 100% sustainable rubber sourcing by 2050, GPSNR platform expansion, Halcyon Agri's Corrie MacColl certified supply chain, and Sri Trang's 500,000+ smallholder farmer geolocation traceability platform collectively creating a premium commercial advantage for certified sustainable processors targeting European and sustainability-mandating global tire OEM procurement programs through 2033.

The leading companies include Sri Trang Agro-Industry Plc Halcyon Agri Corporation Limited Bridgestone Corporation, Michelin Group, Thai Hua Rubber Public Company Limited, Rubber Latex Group Public Company Limited, Von Bundit Co. Ltd., Sinochem Group, Southland Rubber Company Limited, and Apcotex Industries Limited spanning world-leading natural rubber processors and exporters, global tire manufacturer institutional consumers, and specialty latex product supply chain operators serving the full global Natural Rubber value chain.