- Processed Food

- Mulching Materials Market

Mulching Materials Market Size, Share, and Growth Forecast, 2026 - 2033

Mulching Materials Market by Product Type (Organic, Plastic Films, Others), Material (Wood, Chips, Others), Application, Form, and Regional Analysis for 2026 - 2033

Mulching Materials Market Size and Trends Analysis

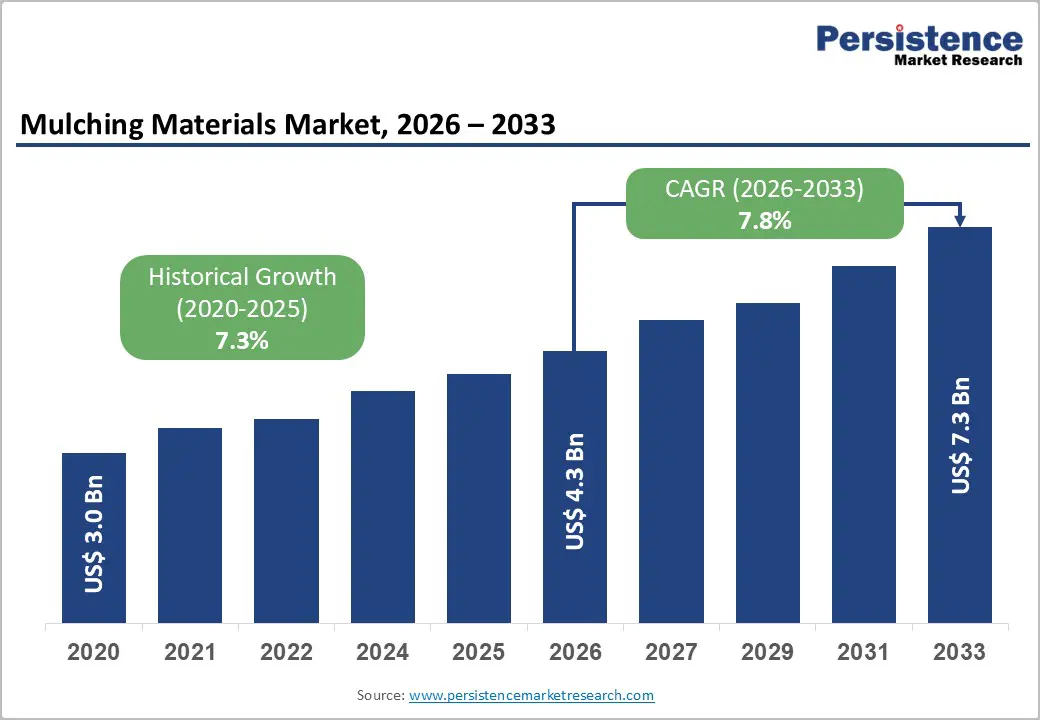

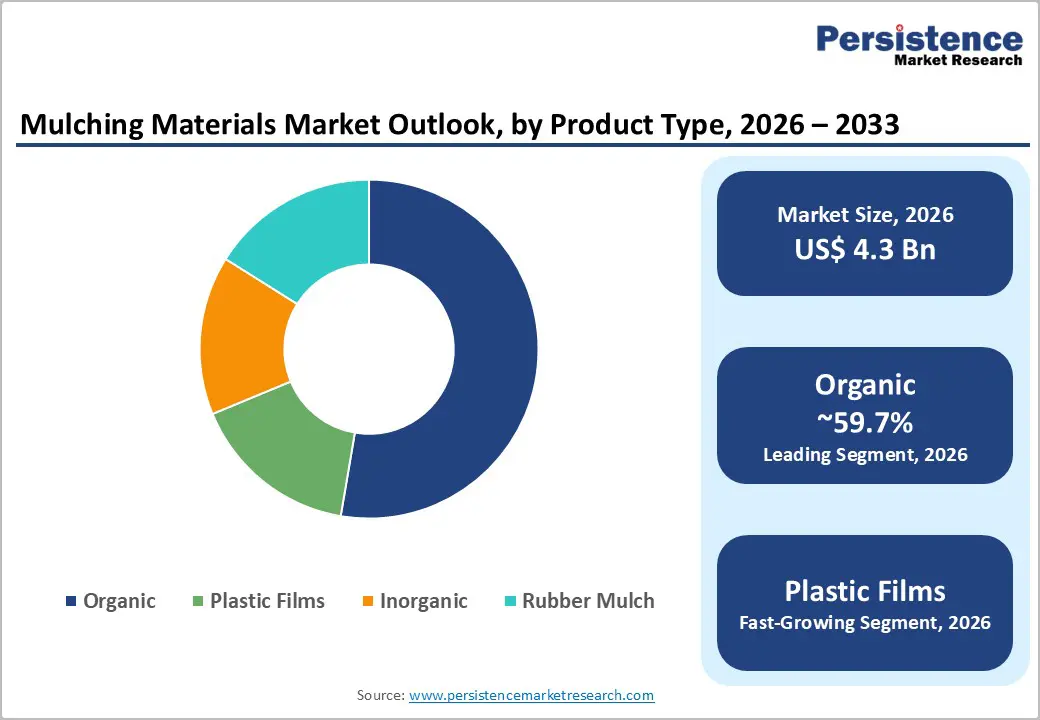

The global mulching materials market size is likely to be valued at US$4.3 billion in 2026 and is expected to reach US$7.3 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033, driven by rising emphasis on soil conservation, efficient water management, and crop productivity improvement.

Agricultural producers increasingly rely on mulching techniques to enhance soil moisture retention and suppress weed growth. In parallel, urban landscaping activities and residential gardening trends are strengthening retail demand for packaged mulching products.

Organic mulches dominate the current market due to their environmental compatibility, while plastic and engineered mulch films represent the fastest-growing category as commercial horticulture adopts advanced cultivation practices. The market outlook is supported by expanding horticultural production, growing environmental awareness, and technological improvements in biodegradable mulch materials.

Key Industry Highlights:

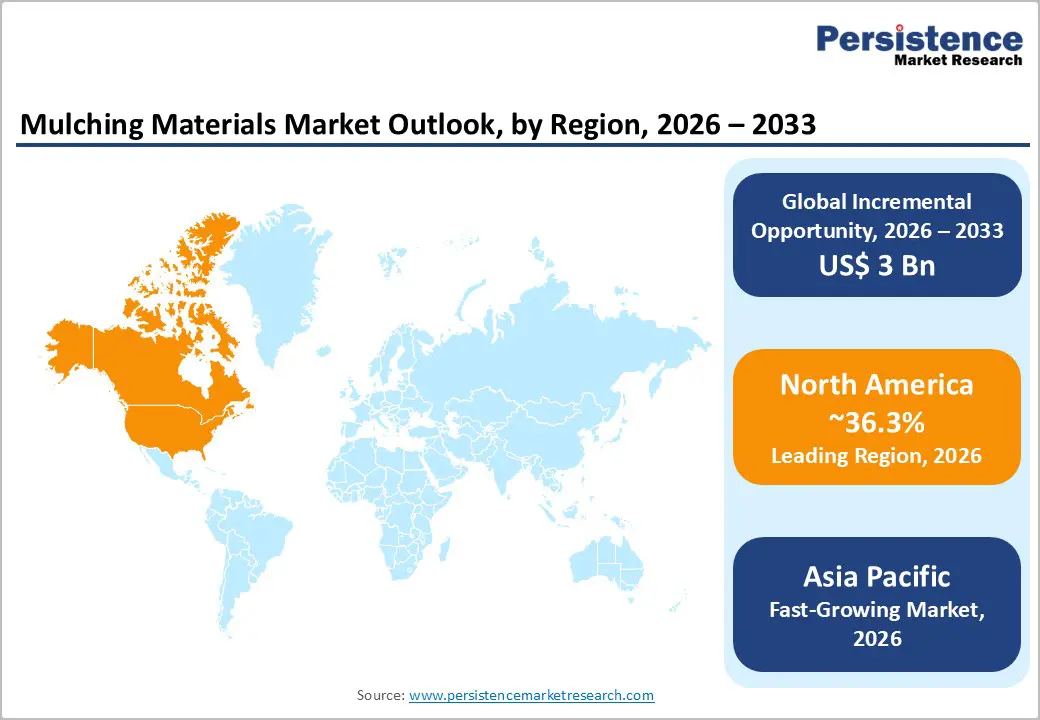

- Leading Region: North America is projected to account for approximately 36.3% of the market share, supported by strong residential landscaping demand, advanced agricultural practices, and high adoption of mulch films in commercial horticulture.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, driven by increasing agricultural modernization, expanding greenhouse cultivation, and rising adoption of plastic mulch films in countries such as China and India.

- Investment Plans: Major industry participants are increasing investments in biodegradable mulch film technologies and sustainable material innovations, particularly in North America and Europe, as regulatory pressure on conventional plastic waste accelerates the transition toward environmentally friendly mulching solutions.

- Dominant Product Type: The organic segment is anticipated to account for approximately 59.7% of market share, primarily due to its environmental compatibility, widespread availability, and benefits for soil health and moisture retention.

- Leading Material: The wood chips segment leads the market with an anticipated share of 40.6%, supported by abundant supply from forestry by-products, cost-effectiveness, and strong demand in residential landscaping and municipal landscaping projects.

| Key Insights | Details |

|---|---|

|

Mulching Materials Market Size (2026E) |

US$4.3 Bn |

|

Market Value Forecast (2033F) |

US$7.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Water Conservation and Yield Optimization in Agriculture

Mulching plays a critical role in improving agricultural productivity by reducing soil evaporation and maintaining optimal soil temperature conditions. By covering the soil surface, mulch minimizes water loss and reduces weed competition, enabling crops to utilize available nutrients more efficiently. Agricultural research institutions consistently report improved crop yields and irrigation efficiency when mulching is combined with drip irrigation systems. This advantage is particularly important in regions facing water scarcity and climate variability. As agricultural producers seek cost-effective methods to maximize yields while reducing water consumption, demand for mulching materials continues to rise, particularly in high-value vegetable and fruit cultivation systems.

Environmental Regulations Encouraging Sustainable Materials

Environmental concerns regarding plastic waste and microplastic accumulation in agricultural soils is prompting regulatory authorities to encourage the adoption of biodegradable alternatives. Governments and agricultural organizations increasingly promote sustainable farming practices that reduce environmental impact. As a result, manufacturers are investing heavily in the development of soil-biodegradable polymers and compostable mulch films. These materials decompose naturally after use, eliminating the need for costly removal and disposal processes. The shift toward biodegradable mulching solutions is creating new revenue opportunities for manufacturers while helping growers comply with environmental regulations and sustainability standards.

Growth in Residential Landscaping and Urban Gardening

Residential landscaping and home gardening have become important demand drivers for mulching materials. Urban homeowners increasingly invest in garden maintenance and aesthetic landscaping, which requires regular mulch application to maintain plant health and soil moisture levels. Landscaping contractors and retail garden centers continue to expand their product offerings to meet this demand. Bagged and decorative mulch products have gained popularity in residential markets due to their convenience and visual appeal, encouraging repeated purchases. As urban green infrastructure initiatives expand globally, landscaping demand will remain a consistent contributor to market growth.

Barrier Analysis - Environmental Concerns Related to Conventional Plastic Mulches

Although plastic mulch films provide significant agronomic benefits, their disposal presents environmental challenges. After harvest, plastic residues must be collected and processed, which adds labor costs and operational complexity for farmers. In some cases, fragments of plastic mulch remain in soil, contributing to long-term microplastic contamination. These environmental concerns have led to stricter regulations and increasing pressure on growers to adopt sustainable alternatives. The cost of removal, recycling, and disposal of conventional polyethylene mulch films can limit adoption in certain regions, particularly where waste management infrastructure remains underdeveloped.

Raw Material Price Volatility

Mulching materials rely on diverse raw materials, including wood, bark, straw, and polymer resins. Prices of these inputs fluctuate based on forestry output, agricultural supply cycles, and petrochemical market conditions. Increases in polymer resin costs can significantly raise the price of plastic mulch films, while fluctuations in timber supply can affect organic mulch availability. Such cost volatility creates pricing uncertainty for manufacturers and distributors, potentially slowing adoption among price-sensitive agricultural producers and landscaping businesses.

Opportunity Analysis - Expansion of Biodegradable Mulch Film Technologies

Technological advancements in biodegradable polymer materials present a major opportunity for the mulching materials market. Modern biodegradable mulch films can perform similarly to conventional plastic films while decomposing naturally in soil after use. This eliminates the need for removal and disposal, reducing labor costs for farmers. Manufacturers investing in biodegradable film technologies are likely to capture significant market share as agricultural producers increasingly prioritize sustainable farming solutions. Strategic partnerships between polymer producers, agricultural research institutions, and growers are accelerating the commercialization of these products.

Growth of Value-Added Retail Mulch Products

The retail gardening segment continues to expand with growing consumer interest in landscaping, home gardening, and outdoor aesthetics. Manufacturers are introducing premium mulch products, including colored mulch, nutrient-enriched blends, and decorative bark. Packaged mulch products designed for convenience and easy transportation are becoming increasingly popular among homeowners. Retail innovation in packaging, branding, and product differentiation provides companies with opportunities to increase profit margins while strengthening customer loyalty.

Rising Demand for Erosion Control Applications

Mulching materials are widely used in environmental restoration and erosion control projects. Infrastructure development, highway construction, and land rehabilitation programs often require erosion control solutions to stabilize soil surfaces. Geotextile-based mulch products and fiber mulches are particularly suitable for these applications. Governments and environmental organizations continue to invest in soil restoration initiatives and watershed protection programs. These projects create long-term demand for specialized mulching products designed to support soil stabilization and vegetation establishment.

Category-wise Analysis

Product Type Analysis

Organic mulches represent the leading segment and are anticipated to account for approximately 59.7% of the market share in 2026. Their dominance is primarily attributed to environmental compatibility, widespread availability, and proven benefits for soil health. Materials such as wood chips, bark, compost, and straw are commonly used across residential landscaping, horticulture, and agricultural fields. These materials gradually decompose, adding organic matter to soil, improving moisture retention, and enhancing soil structure over time. Organic mulches are also widely favored in sustainable landscaping and organic farming systems because they support microbial activity and reduce dependence on synthetic soil treatments. For example, municipal landscaping programs in the United States and Europe frequently use bark and wood-chip mulch derived from forestry by-products to maintain parks, roadside plantations, and urban green spaces. Similarly, residential garden centers offer bagged compost and decorative bark mulch to homeowners seeking environmentally friendly garden maintenance solutions.

Plastic mulch films are the fastest-growing segment as commercial agricultural producers increasingly adopt advanced cultivation practices to maximize productivity and crop quality. Plastic mulch films provide effective weed suppression, maintain soil moisture levels, and regulate soil temperature, which is particularly beneficial in controlled horticultural environments. These materials are widely used in high-value crop production such as tomatoes, strawberries, cucumbers, and melons, where consistent soil conditions directly influence yield and product quality. For instance, strawberry growers in California and vegetable producers in Mediterranean countries frequently utilize polyethylene mulch films combined with drip irrigation systems to improve water efficiency and extend growing seasons. Recent innovations in biodegradable plastic mulch films have further accelerated market growth by addressing environmental concerns associated with conventional polyethylene films. As mechanized farming systems and precision agriculture technologies expand globally, demand for both traditional and biodegradable plastic mulch films is expected to increase steadily.

Material Insights

Wood chips hold the largest share and are anticipated to account for approximately 40.6% of the market share in 2026. Their widespread availability and relatively low cost make them a preferred material across landscaping and agricultural applications. Wood chips provide excellent insulation for soil, helping to regulate temperature while maintaining moisture levels. In addition, they gradually decompose and contribute organic nutrients to soil, improving fertility and soil structure over time. Landscaping contractors and municipal landscaping programs frequently use wood-chip mulch in parks, gardens, and roadside landscaping projects due to its durability and aesthetic appeal. For example, city landscaping departments often utilize recycled tree trimmings and forestry residues to produce wood-chip mulch for public landscaping projects. Similarly, commercial orchard operators use wood-chip mulch around fruit trees to maintain soil moisture and reduce weed competition, improving long-term plant health and productivity.

Plastic materials represent the fastest-growing material category as engineered mulch films gain wider adoption in commercial agriculture. Plastic mulch films offer superior weed suppression, soil temperature control, and moisture retention compared to many traditional mulching materials. These characteristics make them particularly suitable for intensive farming systems and high-value crop cultivation. For example, vegetable farmers cultivating crops such as peppers, eggplants, and tomatoes often use black polyethylene mulch films to improve early crop growth and increase yields. In addition, strawberry farms in North America and Europe commonly rely on plastic mulch films to maintain clean fruit surfaces and reduce soil-borne diseases. Continuous innovation in biodegradable polymer materials has further expanded the use of plastic mulch solutions, allowing farmers to benefit from improved crop productivity while reducing environmental impact and disposal costs.

Regional Insights

North America Mulching Materials Market Trends - Residential Landscaping Demand and Plastic Mulch Use in Commercial Farming

North America is projected to lead the market, accounting for approximately 36.3% of the market share in 2026. The U.S. represents the largest market within the region, supported by a well-developed landscaping industry and extensive commercial horticulture operations. High consumer spending on residential landscaping and home improvement projects contributes significantly to market demand. Retail garden centers, landscaping companies, and agricultural suppliers play a critical role in distributing mulching materials across the region. For instance, major consumer gardening brands such as Scotts Miracle-Gro have expanded their mulch product portfolios with decorative and color-enhanced mulch products widely sold through home improvement retailers.

These products have strengthened retail sales by appealing to homeowners seeking convenient, aesthetically appealing landscaping solutions. Agricultural producers in North America increasingly adopt mulch films to improve irrigation efficiency and crop yields. Vegetable and fruit producers frequently use plastic mulch films combined with drip irrigation systems to maximize productivity, particularly in crops such as strawberries, tomatoes, and peppers. For example, large-scale strawberry growers in California widely use polyethylene mulch films to maintain soil temperature and prevent fruit contact with soil, improving both yield and product quality.

Water conservation initiatives in drought-prone regions, particularly in the western U.S., have further encouraged the adoption of mulching practices. Government programs promoting sustainable agriculture and soil conservation also support the use of biodegradable mulch materials. Companies such as Berry Global Inc. have introduced advanced agricultural film technologies designed to enhance durability and water-use efficiency in commercial farming systems.

Technological innovation and product development remain key growth drivers in the region. Manufacturers continue to invest in biodegradable mulch films and advanced polymer technologies to meet regulatory requirements and environmental expectations. Chemical companies such as BASF SE have expanded biodegradable polymer solutions used in agricultural mulch films, enabling farmers to reduce disposal costs associated with conventional plastic films. Retail innovation in bagged mulch products has also strengthened consumer demand, with landscaping suppliers offering premium organic mulch blends for residential gardening. These developments collectively reinforce North America’s leadership position in the global mulching materials market.

Europe Mulching Materials Market Trends - Biodegradable Mulch Adoption and Greenhouse Horticulture Expansion

Europe represents a significant market for mulching materials, characterized by strong environmental regulations and advanced agricultural practices. Countries such as Germany, the U.K., France, and Spain play important roles in regional demand, particularly in horticulture and greenhouse cultivation. European farmers frequently adopt mulch films to improve crop quality, extend growing seasons, and increase productivity in high-value crops such as berries, vegetables, and ornamental plants. Spain’s greenhouse vegetable industry in regions such as Almería, for example, widely uses mulch films and ground-cover materials to support intensive greenhouse production systems that supply fresh produce across Europe.

Environmental sustainability remains a major focus across European markets. Regulations addressing plastic waste management have encouraged the development and adoption of biodegradable mulch materials. Many agricultural producers are transitioning toward environmentally responsible farming practices, including the use of compostable mulch films and organic mulching materials. Companies such as Novamont S.p.A. have played an important role in this transition by developing biodegradable polymer materials used in agricultural mulch films that decompose naturally in soil. These innovations help farmers comply with environmental regulations while maintaining high crop productivity.

Landscaping and urban greening initiatives also support regional market growth. Municipal governments across Europe continue to invest in public parks, urban gardens, and green infrastructure projects that require landscaping mulch products to support soil moisture retention and plant health. For example, city-level urban greening programs in countries such as Germany and France incorporate organic mulching techniques in public landscaping projects to reduce irrigation requirements and improve soil quality. Retail garden centers across Europe are also expanding their product offerings of organic mulch products designed for residential gardeners, reflecting growing consumer awareness of sustainable gardening practices.

Asia Pacific Mulching Materials Market Trends - Agricultural Modernization and Rapid Adoption of Plastic Mulch Films

Asia Pacific represents the fastest-growing regional market for mulching materials. Rapid agricultural development, population growth, and increasing food demand are driving the adoption of modern farming techniques across the region. China and India represent the largest agricultural markets, while Japan and Southeast Asian countries are expanding protected cultivation systems to support high-value crop production. Governments across the region actively promote modern agricultural practices to improve food security and farm productivity. For example, China has widely implemented plastic mulch film technology across vegetable and cotton farming areas to improve soil moisture retention and crop yields. Farmers across Asia Pacific increasingly utilize plastic mulch films to improve crop productivity and reduce water consumption. Government initiatives supporting agricultural modernization have encouraged the adoption of advanced cultivation technologies, including mulching systems and drip irrigation.

In India, mulching practices are promoted through agricultural extension programs that encourage farmers to use plastic mulch films for crops such as tomatoes, chilies, and strawberries. These initiatives aim to increase crop yields while improving water efficiency in regions facing water scarcity. Japan has also advanced the use of mulch films in precision agriculture and protected cultivation systems, particularly in greenhouse vegetable production.

Regional manufacturing advantages also contribute significantly to market growth. Many global producers of mulch films and polymer materials operate manufacturing facilities in Asia Pacific, enabling cost-efficient production and regional supply. For example, several international polymer manufacturers have expanded production capacity for biodegradable agricultural films in China and Southeast Asia to meet rising regional demand. As awareness of sustainable agriculture increases, biodegradable mulch materials are expected to gain greater adoption throughout the region. These developments, combined with strong agricultural expansion and supportive government policies, position Asia Pacific as a key growth engine for the global mulching materials market.

Competitive Landscape

The global mulching materials market is moderately fragmented, with a mix of multinational corporations and regional suppliers. Large chemical and materials companies dominate the production of polymer-based mulch films, while regional manufacturers supply organic mulch products such as wood chips and bark. Local landscaping suppliers and agricultural distributors play an important role in market distribution. Competition in the market is driven by product quality, innovation, pricing strategies, and distribution networks. Companies investing in biodegradable materials and sustainable product solutions are gaining competitive advantages as environmental regulations become more stringent. Leading companies focus on product innovation, sustainability initiatives, and market expansion strategies. Investment in biodegradable polymer technology, partnerships with agricultural distributors, and expansion of retail mulch product lines remain key strategic priorities for market leaders.

Key Industry Developments

- In November 2025, Novamont S.p.A. announced that its Mater-Bi biodegradable mulch film achieved certification under the EU Fertilizer Regulation 2019/1009. The certification confirms that the product meets strict environmental standards for biodegradability and ecotoxicity in soil, strengthening the company’s position in Europe’s sustainable agriculture segment and supporting the wider adoption of biodegradable mulch films among commercial growers.

- In June 2025, BASF SE showcased advancements in sustainable materials at the K 2025 industry exhibition, highlighting solutions based on renewable feedstocks and its ecovio® biopolymer portfolio used in agricultural mulch films. The initiative demonstrates BASF’s continued investment in circular material solutions and sustainable polymer technologies aimed at reducing environmental impact in agriculture and packaging.

Companies Covered in Mulching Materials Market

- BASF SE

- Berry Global Inc.

- Novamont S.p.A.

- BioBag International AS

- RKW Group

- Armando Alvarez Group

- AEP Industries Inc.

- Plastika Kritis S.A.

- Kingfa Sci. & Tech. Co., Ltd.

- Trioplast Industrier AB

- Ab Rani Plast Oy

- Al-Pack Enterprises Ltd.

- British Polythene Industries PLC

- Agriplast Tech India Pvt. Ltd.

- Dubois Agrinovation

- Iris Polymers Industries Pvt. Ltd.

Frequently Asked Questions

The global mulching materials market is estimated to be valued at US$4.3 billion in 2026.

The mulching materials market is projected to reach US$7.3 billion by 2033.

Major trends shaping the market include the growing adoption of biodegradable mulch films, increased use of plastic mulch in high-value crop production, and rising demand for organic mulches in residential landscaping and urban gardening.

The organic mulch segment is the leading product category, accounting for an anticipated share of approximately 59.7% of the market, due to its environmental compatibility, soil fertility benefits, and widespread use in landscaping and agricultural applications.

The mulching materials market is expected to grow at a CAGR of 7.8% between 2026 and 2033.

Some of the major companies include BASF SE, Berry Global Inc., Novamont S.p.A., The Scotts Miracle‑Gro Company, and Dow Inc.