- Medical Devices

- Minimally Invasive Surgery Market

Minimally Invasive Surgery Market Size, Share, and Growth Forecast 2026 - 2033

Minimally Invasive Surgery Market by Product (Surgical Devices, Endoscopic Devices, Robotic-Assisted Surgical Systems, Monitoring & Visualization Devices, Others), Surgery Type (Laparoscopic Surgery, Endoscopic Surgery, Arthroscopic Surgery, Robotic-Assisted Surgery, Others), Application (Cardiology, Orthopedics, Gynecology, Urology, Others), End-user (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Academic & Research Institutes, Others), and Regional Analysis, 2026 - 2033

Minimally Invasive Surgery Market Size and Trend Analysis

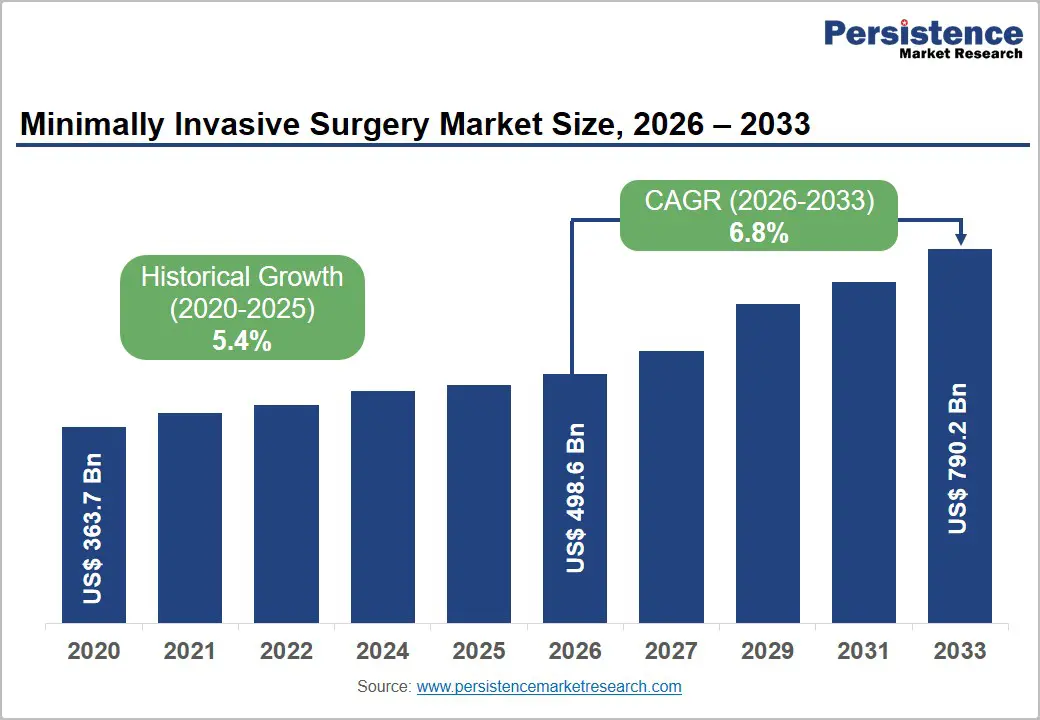

The global minimally invasive surgery market size is expected to be valued at US$ 498.6 billion in 2026 and projected to reach US$ 790.2 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

The accelerating adoption of robotic-assisted surgical platforms, increasing prevalence of chronic diseases requiring surgical intervention, and the global shift toward outpatient and ambulatory care settings.

According to the World Health Organization (WHO), an estimated 313 million surgical procedures are performed globally every year, with minimally invasive approaches now constituting a rapidly expanding proportion. Favorable reimbursement policies for MIS procedures in key markets such as the United States and Germany, combined with technological convergence of artificial intelligence, 3D visualization, and flexible robotics, are collectively reinforcing the long-term growth trajectory.

Key Industry Highlights:

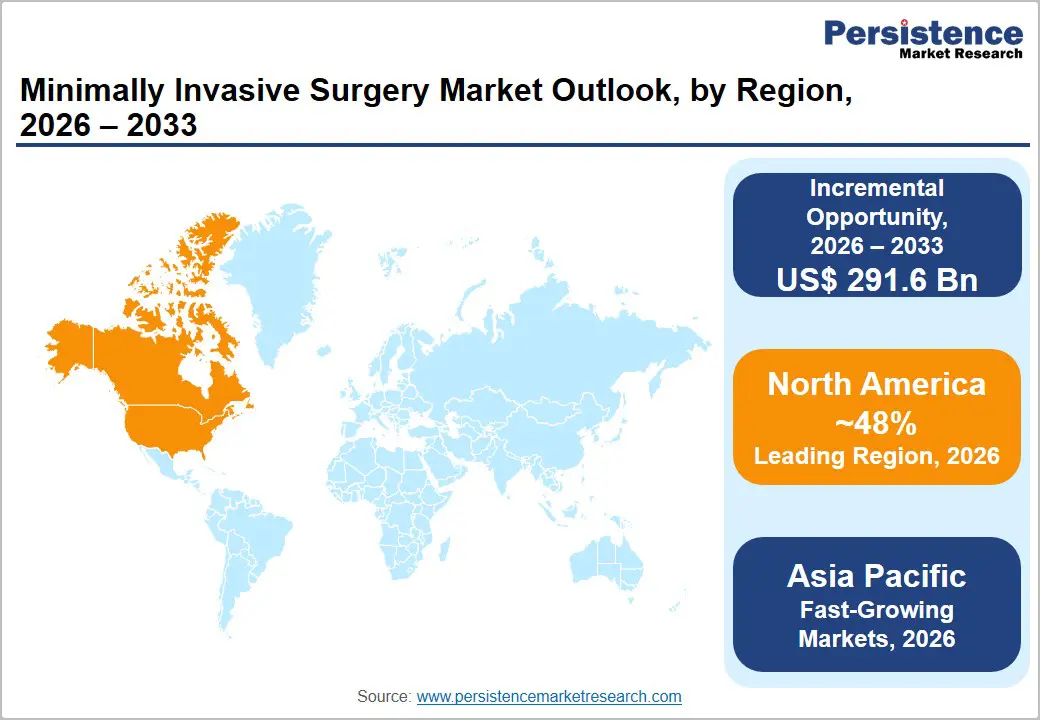

- Leading Region: North America is likely to capture approximately 48% share in 2026, anchored by the U.S. innovation ecosystem, high robotic surgical system density, CMS reimbursement expansion for ASCs, and the world's most active MIS clinical trial pipeline.

- Fast-Growing Market: Asia Pacific is the highest-growth region, driven by China's Healthy China 2030 initiative, India's PLI manufacturing scheme, Japan's Olympus-led endoscopy ecosystem, and rising surgical infrastructure investment across ASEAN, collectively fueling demand for MIS technologies.

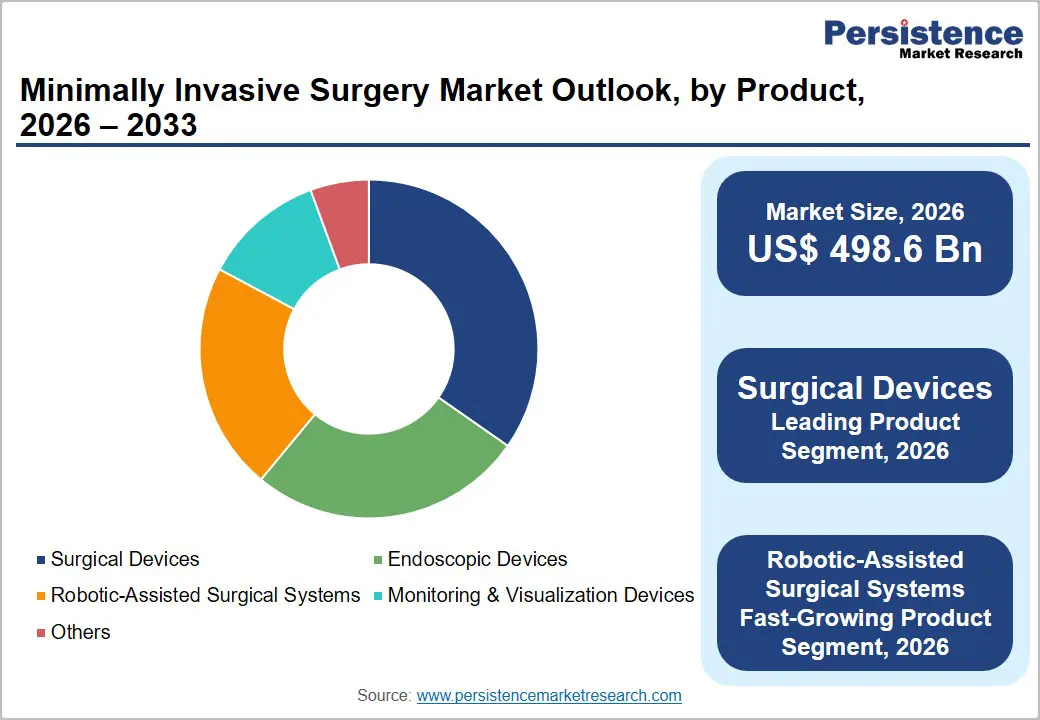

- Dominant Product Segment: Surgical devices account for ~35% of the MIS product market in 2025 due to universal, high-frequency use across all procedure types, strong consumable pull-through economics, and diversified portfolios held by Medtronic, Stryker, and Johnson & Johnson MedTech.

- Fast-Growing Product: Robotic-assisted surgical systems are the fast-growing product category, driven by da Vinci® 5 commercialization, OTTAVA™ FDA clearance, Hugo™ RAS global rollout, and ASC-optimized compact robotic platforms from Moon Surgical and Virtual Incision.

- Opportunity: The proliferation of Ambulatory Surgical Centers with 6,100+ Medicare-certified ASCs in the U.S. and accelerating ASC development in Europe and Asia Pacific offers a high-growth, high-margin channel for compact, cost-optimized MIS and robotic surgical platforms.

Market Dynamics

Drivers - Surging Demand for Robotic-Assisted Surgery and Technological Convergence

The rapid proliferation of robotic-assisted surgical platforms is one of the most powerful demand catalysts in the minimally invasive surgery market. Intuitive Surgical's da Vinci® system had installed over 9,900 systems globally as of Q4 2024, with more than 2.3 million da Vinci® procedures performed in 2024 alone. Next-generation systems such as da Vinci® 5, launched in 2024, integrate AI-powered force feedback and enhanced 3D visualization, substantially expanding surgical precision.

Competitive entrants including CMR Surgical's Versius® and Medtronic's Hugo™ RAS system are broadening access to robotic platforms beyond tertiary centers to community hospitals. This democratization of surgical robotics, coupled with declining system costs over time, is significantly expanding the addressable procedural base.

Rising Chronic Disease Burden and Preference for Shorter Recovery

The rise in global burden of cardiovascular disease, cancer, musculoskeletal disorders, and urological conditions is generating structural demand for MIS procedures. The Global Burden of Disease Study 2023 estimated that chronic diseases account for over 74% of all deaths globally, with millions requiring surgical management annually.

MIS procedures offer documented advantages over open surgery including 30–50% shorter hospital stays, lower infection rates, and reduced blood loss as evidenced by outcomes data published in the New England Journal of Medicine and The Lancet. These clinical benefits, reinforced by patient preference for faster recovery and reduced post-operative pain, are driving a systemic shift toward minimally invasive approaches across surgical specialties worldwide.

Restraints - High Capital Costs and Limited Accessibility in Developing Markets

The substantial capital investment required for advanced MIS systems particularly robotic surgical platforms remains a significant barrier to market penetration. The acquisition cost of a da Vinci® robotic system ranges from approximately US$ 1.5 million to US$ 2.5 million, with annual maintenance and consumable costs adding US$ 100,000–US$ 200,000 per system.

This financial burden restricts adoption to well-resourced tertiary hospitals in high-income countries, leaving lower-middle-income markets substantially underserved. The WHO estimates that over 5 billion people globally lack access to safe surgical care, with affordability representing the primary constraint, limiting the overall addressable market for premium MIS technologies.

Steep Learning Curves and Specialized Training Requirements

Proficiency in minimally invasive surgical techniques requires extensive training and a significant case volume to achieve optimal outcomes. Studies published in the British Journal of Surgery indicate that laparoscopic surgeons typically require between 50 and 100 supervised procedures before reaching competency, while robotic surgery programs necessitate structured credentialing processes.

The shortage of trained MIS surgeons particularly in Asia, Latin America, and Africa constrains procedure growth rates and delays technology adoption in these high-potential regions. Simulation-based training infrastructure remains underdeveloped outside major academic medical centers, creating a meaningful capacity bottleneck that tempers near-term market expansion in emerging economies.

Opportunities - Expansion of Ambulatory Surgical Centers as High-Growth End-User Segment

Ambulatory Surgical Centers (ASCs) are emerging as one of the most dynamic growth frontiers in the minimally invasive surgery market. In the United States, the Centers for Medicare & Medicaid Services (CMS) has progressively expanded the list of procedures approved for ASC reimbursement including complex laparoscopic and orthopedic procedures with the 2024 Outpatient Prospective Payment System (OPPS) rule adding several high-acuity MIS codes. The Ambulatory Surgery Center Association (ASCA) reported over 6,100 Medicare-certified ASCs operating in the U.S. as of 2024.

Globally, ASC penetration in Europe and Asia Pacific is accelerating, driven by healthcare cost containment policies. Compact, cost-optimized robotic systems purpose-built for ASC environments such as Moon Surgical's Maestro™ and Virtual Incision's MIRA™ are specifically designed to capitalize on this structural shift, representing a substantial incremental revenue opportunity.

Artificial Intelligence Integration and Single-Port Robotic Surgery Innovation

The integration of artificial intelligence and machine learning into surgical platforms represents a transformative opportunity for value creation in the MIS market. Johnson & Johnson MedTech's OTTAVA™ and Asensus Surgical's Intelligent Surgical Unit (ISU™) platform incorporate AI-driven performance analytics, real-time tissue differentiation, and intraoperative guidance capabilities that meaningfully improve safety and reproducibility. Concurrently, single-port and flexible robotic platforms are enabling procedures in anatomically challenging spaces previously inaccessible via MIS approaches. The FDA's Digital Health Center of Excellence has published frameworks for AI/ML-based surgical device authorization, accelerating regulatory clarity. Companies that combine AI-driven surgical intelligence with platform interoperability and cloud-based data analytics are positioned to command significant premium pricing and long-term customer lock-in within hospital systems globally.

Category-wise Analysis

Product Insights

Surgical devices lead the product segment of the minimally invasive surgery market, accounting for approximately 35% of total market revenue in 2026. This dominance reflects the fundamental and universal requirement for precision instruments including laparoscopic trocars, graspers, scissors, clip appliers, and energy-based cutting and sealing devices across virtually every MIS procedure type. High-volume consumable usage per procedure creates a durable and recurring revenue base.

Companies such as Medtronic, Stryker Corporation, and Johnson & Johnson MedTech maintain diversified portfolios of MIS surgical instruments. The segment benefits from well-established reimbursement and high procedure frequency globally. Additionally, innovations such as single-use laparoscopic instruments gaining traction for infection control are extending market value and driving incremental adoption across hospital and ASC settings.

Application Insights

Gynecology represents the leading application segment in the MIS market, holding approximately 28% of total application revenue in 2026. The segment's dominance is driven by the high prevalence of gynecological conditions amenable to MIS including uterine fibroids, endometriosis, ovarian cysts, and cervical and endometrial cancers and a strong historical transition from open to laparoscopic and robotic-assisted procedures. According to the American College of Obstetricians and Gynecologists (ACOG), over 600,000 hysterectomies are performed annually in the United States alone, with minimally invasive approaches now preferred in clinical guidelines. The expanding use of robotic platforms for complex gynecological oncology further reinforces the segment's leadership position through the forecast period.

End-user Insights

Hospitals remain the dominant end-user segment, representing approximately 58% of the minimally invasive surgery market in 2025. Tertiary and secondary care hospitals house the multidisciplinary infrastructure including operating theater suites, sterile processing departments, intensive care units, and specialized surgical teams required for the full spectrum of MIS procedures, from routine laparoscopic cases to complex robotic-assisted cancer resections.

The American Hospital Association (AHA) reports over 6,100 registered hospitals in the U.S., the majority equipped with advanced surgical capabilities. Globally, hospital-based MIS adoption is being accelerated by national surgical quality improvement programs and the integration of robotic systems into academic medical centers, ensuring sustained segment leadership.

Regional Insights

North America Minimally Invasive Surgery Market Trends and Insights

North America accounted for nearly 48% of the global minimally invasive surgery market in 2026, supported by advanced healthcare infrastructure, rapid robotic surgery adoption, and strong reimbursement coverage. The region benefits from widespread penetration of laparoscopic and image-guided procedures across hospitals and ambulatory surgical centers. Continuous FDA approvals for next-generation robotic systems and increasing AI integration in surgical navigation platforms are further strengthening regional growth. Expanding outpatient surgical volumes and rising investments in digital operating rooms are expected to maintain North America’s leadership position.

U.S. Minimally Invasive Surgery Market Trends and Insights

The U.S. represented approximately 84.5% of the North American market in 2026, driven by extensive deployment of robotic-assisted surgical systems from Intuitive Surgical, Stryker, and Medtronic. Growth is supported by favorable CMS reimbursement for minimally invasive procedures and increasing adoption of robotic oncology and urology surgeries. The country is also witnessing rising integration of AI-enabled visualization and navigation technologies in operating rooms.

Canada Minimally Invasive Surgery Market Trends and Insights

Canada accounted for close to 10.8% of the regional market and is projected to expand at a CAGR of 7.9%. Provincial healthcare systems are steadily increasing investments in laparoscopic and robotic surgery programs to reduce patient recovery times and hospital burden. Growing adoption of minimally invasive orthopedic and gynecological procedures, along with Health Canada approvals for advanced endoscopic platforms, continues to support market expansion.

Europe Minimally Invasive Surgery Market Trends and Insights

Europe held around 28.6% of the global minimally invasive surgery market in 2026, supported by strong public healthcare systems, rising robotic surgery adoption, and favorable reimbursement frameworks. Demand for minimally invasive procedures is increasing across general surgery, gynecology, and orthopedics due to shorter hospital stays and improved patient outcomes. The implementation of EU MDR regulations is improving product quality standards and accelerating innovation in advanced surgical technologies. Increasing investments in robotic-assisted surgical training and digital operating infrastructure are expected to sustain Europe’s long-term market growth.

Germany Minimally Invasive Surgery Market Trends and Insights

Germany contributed nearly 26.4% of the European minimally invasive surgery market in 2026. The country’s advanced hospital infrastructure and DRG-based reimbursement system have enabled strong adoption of robotic-assisted and laparoscopic procedures. German healthcare providers are increasingly integrating image-guided surgical systems in oncology and cardiovascular interventions, while domestic manufacturing capabilities continue to strengthen the country’s MIS ecosystem.

UK Minimally Invasive Surgery Market Trends and Insights

The UK captured approximately 19.2% of the regional market and is anticipated to register a CAGR of 8.1% during the forecast period. NHS-backed investments in robotic surgery programs and minimally invasive treatment pathways are driving adoption across public hospitals. Increasing surgical backlog recovery initiatives and expansion of robotic-assisted colorectal and urological surgeries are further accelerating market growth.

Asia Pacific Minimally Invasive Surgery Market Trends and Insights

Asia Pacific represented nearly 18.9% of the global minimally invasive surgery market in 2026 and is projected to witness the fastest CAGR of 9.8%. Rapid healthcare infrastructure modernization, growing medical tourism, and increasing healthcare expenditure are fueling demand for minimally invasive procedures across emerging economies. Governments across China, India, Japan, and Southeast Asia are expanding access to advanced surgical technologies through healthcare reforms and domestic medical device manufacturing initiatives. Rising awareness regarding faster recovery procedures and growing penetration of robotic surgical systems are expected to drive substantial regional expansion.

China Minimally Invasive Surgery Market Trends and Insights

China accounted for nearly 38.7% of the Asia Pacific market in 2026, supported by large-scale investments under the “Healthy China 2030” initiative. Expansion of tertiary hospitals and increasing NMPA approvals for robotic and laparoscopic surgical devices are accelerating MIS adoption. Domestic manufacturers are also expanding production of cost-effective endoscopic systems, strengthening China’s competitive position in the regional market.

Japan Minimally Invasive Surgery Market Trends and Insights

Japan held approximately 24.1% of the regional market, supported by strong endoscopy adoption and advanced healthcare infrastructure. The country benefits from high procedural volumes in gastroenterology and oncology surgeries, alongside widespread reimbursement coverage for minimally invasive procedures. Continuous innovation by Olympus and increasing adoption of robotic-assisted surgeries in aging patient populations are contributing significantly to market growth.

Competitive Landscape

The global minimally invasive surgery market is moderately consolidated at the premium technology tier, with Intuitive Surgical, Medtronic, Johnson & Johnson MedTech, Stryker, Boston Scientific, and Olympus Corporation collectively commanding dominant market share. Key competitive differentiators include installed base depth, disposable instrument ecosystem lock-in, clinical outcomes data, and breadth of surgical specialty coverage.

The market is simultaneously experiencing fragmentation at the innovation frontier, with venture-backed entrants CMR Surgical, Asensus Surgical, Moon Surgical, Virtual Incision, and PROCEPT BioRobotics challenging incumbents in targeted procedure niches. Strategic M&A, licensing agreements, and platform interoperability partnerships are the dominant competitive strategies, alongside aggressive investment in simulation-based surgical training ecosystems to expand surgeon adoption.

Key Developments:

- In May 2026, PainTEQ announced the U.S. commercial launch of TRAQ SI Joint Fusion, the first posterior sacroiliac joint implant engineered to achieve bi-cortical fixation by engaging both the sacral and iliac cortices through a minimally invasive 1-inch incision. The addition of TRAQ broadens the company’s posterior SI joint fusion portfolio alongside LINQ, offering surgeons and interventional specialists two differentiated fixation solutions within the same surgical approach.

- In May 2026, Intuitive announced multiple recent and upcoming innovations across its minimally invasive care portfolio, including upgrades to the da Vinci 5 robotic surgical system and its connected ecosystem, the introduction of extended-use Force Feedback instruments, and new advancements aimed at improving product security, instrument reliability, and overall surgical performance.

- In December 2025, Medtronic announced that the U.S. Food and Drug Administration (FDA) granted clearance for the Hugo™ robotic-assisted surgery (RAS) system for urologic surgical procedures. The approval enables U.S. hospitals and surgeons to adopt a flexible robotic-assisted platform aimed at expanding soft-tissue robotic surgery capabilities and improving access to minimally invasive treatment options.

Companies Covered in Minimally Invasive Surgery Market

- Medtronic

- Intuitive Surgical Operations, Inc.

- CMR Surgical Ltd.

- Smith+Nephew plc

- Renishaw plc

- Monteris Medical

- PROCEPT BioRobotics Corporation

- EndoQuest Robotics

- Moon Surgical

- Asensus Surgical, Inc.

- Olympus Corporation

- Stryker Corporation

- Johnson & Johnson MedTech

- Virtual Incision Corporation

- Boston Scientific Corporation

- Others

Frequently Asked Questions

The global minimally invasive surgery market is estimated to be valued at US$ 498.6 billion in 2026, growing to US$ 790.2 billion by 2033 at a CAGR of 6.8%. Growth is driven by expanding robotic-assisted surgery adoption, rising chronic disease burden, and the proliferation of ambulatory surgical centers globally.

Rising preference for shorter hospital stays, faster recovery, lower surgical trauma, increasing robotic-assisted surgery adoption, and growing prevalence of chronic diseases are the primary demand drivers for the minimally invasive surgery market.

North America is the global leader, accounting for approximately 48% of market share in 2025. The United States drives this dominance through its high concentration of robotic surgical systems, FDA-facilitated device innovation pathways, CMS reimbursement for outpatient MIS procedures, and the world's largest network of 6,100+ Medicare-certified Ambulatory Surgical Centers.

The expansion of robotic-assisted and AI-enabled minimally invasive procedures across emerging healthcare markets and ambulatory surgical centers.

The leading companies include Intuitive Surgical Operations Inc., Medtronic plc, Johnson & Johnson MedTech, Stryker Corporation, Boston Scientific Corporation, Olympus Corporation, CMR Surgical Ltd., PROCEPT BioRobotics Corporation, Asensus Surgical Inc., Smith+Nephew plc, Moon Surgical, Virtual Incision Corporation, and EndoQuest Robotics, among others, driving platform innovation and global MIS adoption.