- Pharmaceuticals

- Melasma Treatment Market

Melasma Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Melasma treatment market by Product Type (Medication, Skin Peels, Laser and Light Treatment, Others), Route of Administration (Oral, Topical), End-user (Hospitals, Dermatology, Others), and Regional Analysis for 2026 - 2033

Melasma Treatment Market Size and Trends Analysis

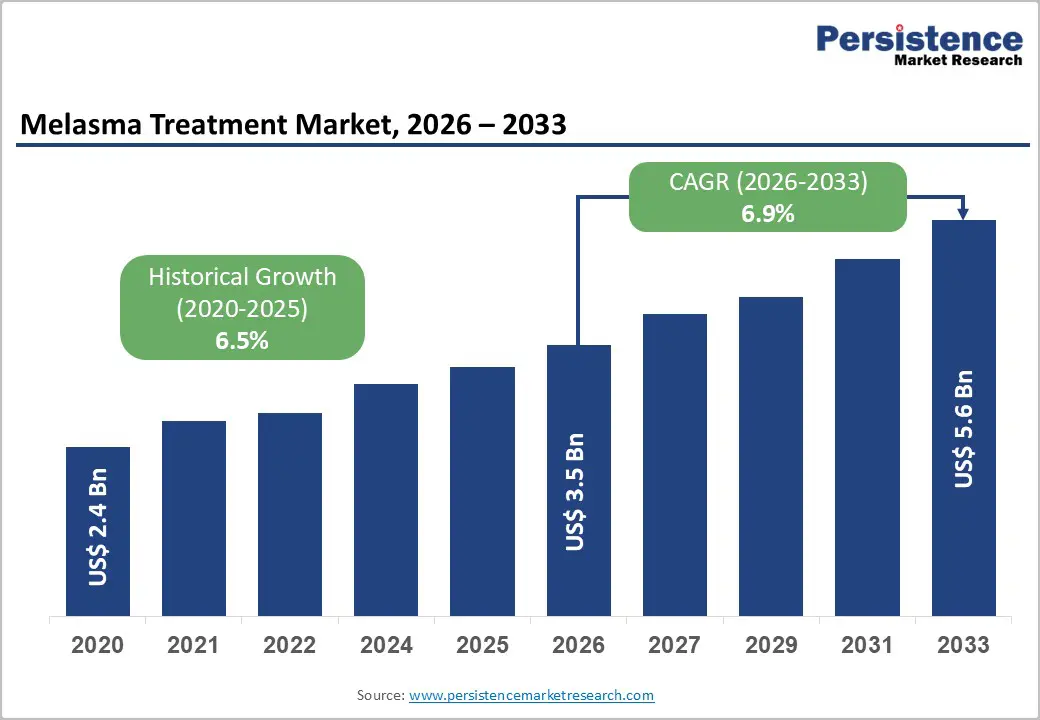

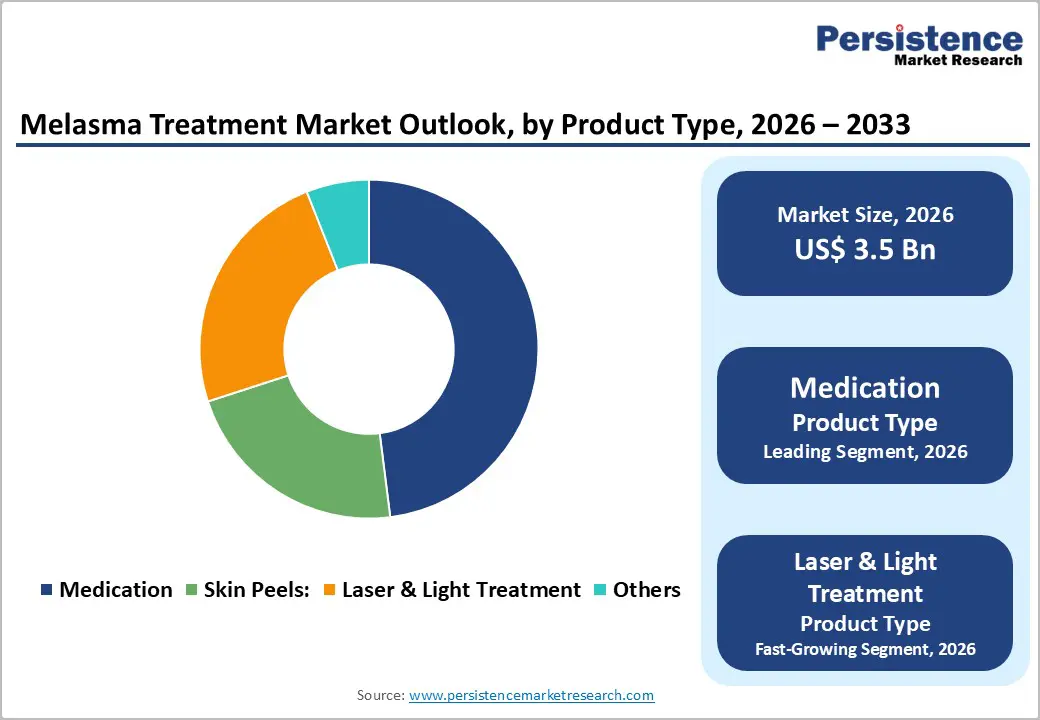

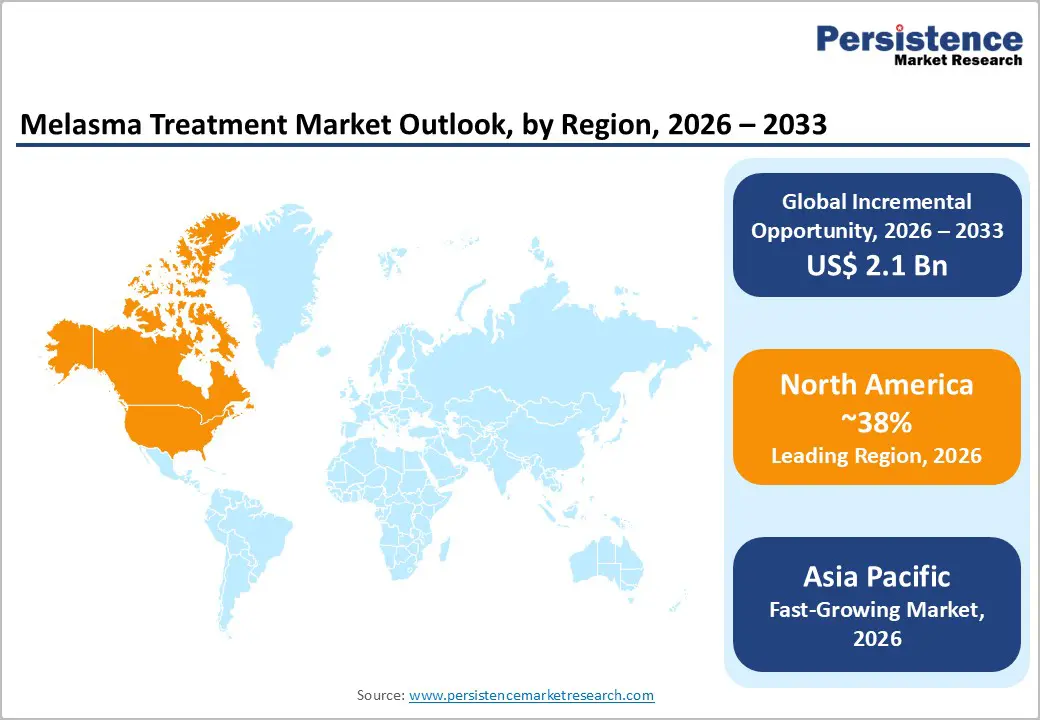

The global melasma treatment market size is likely to be valued at US$3.5 billion in 2026, and is expected to reach US$5.6 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the increasing prevalence of melasma among women of reproductive age, rising aesthetic consciousness, growing demand for non-invasive and combination therapies, and expanding access to dermatology services in urban populations.

Advances in triple-combination creams, picosecond lasers, and tranexamic acid formulations are further boosting uptake by offering faster pigment reduction and lower recurrence rates. Increasing recognition of melasma treatment as critical for improving quality of life, reducing psychological distress, and achieving long-term clearance in emerging aesthetic dermatology markets remains a major driver of market growth.

Key Industry Highlights:

- Leading Region: North America, anticipated to account for a 38% market share in 2026, driven by high aesthetic procedure volumes, strong reimbursement for dermatology, and premium demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising disposable incomes, increasing melasma awareness, and rapid expansion of medical aesthetics in India and Southeast Asia.

- Dominant Product Type: Medication, to hold approximately 48% of the market share, as topical therapies remain the first-line treatment.

- Leading Route of Administration: Topical, contributing nearly 72% of the market revenue, due to the non-invasive nature and patient preference.

| Key Insights | Details |

|---|---|

|

Melasma Treatment Market Size (2026E) |

US$3.5 Bn |

|

Market Value Forecast (2033F) |

US$5.6 Bn |

|

Projected Growth CAGR (2026-2033) |

6.9% |

|

Historical Market Growth (2020-2025) |

6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Aesthetic Consciousness and Melasma Prevalence

The demand for melasma treatments is supported by its notable prevalence and rising focus on appearance and skin health, which together drive more patients to seek dermatological care. Epidemiological data from the U.S. National Library of Medicine show that melasma prevalence varies widely by population, ranging from 1.5% up to 33% depending on demographic and environmental factors, and is particularly common among women of reproductive age and individuals with darker skin types. This variability reflects how exposure to triggers like sunlight and hormonal influences contributes to the condition’s burden across different communities.

As individuals become more conscious of skin aesthetics and the psychological impact of facial pigmentation, treatment uptake has increased. Clinical prevalence data emphasize a strong female predominance, with women affected far more frequently than men, influencing both clinical demand and consumer willingness to pursue therapeutic solutions. Rising aesthetic expectations, combined with variable but significant melasma rates in diverse populations, fuel interest in topical agents, procedural therapies, and combination approaches offered by dermatologists, positioning aesthetic awareness and high prevalence as core market drivers.

Expanding Laser and Light-Based Technologies

Advancements in laser and light-based technologies have significantly expanded treatment options for melasma and other pigmentation disorders by improving precision, safety, and outcomes compared to traditional approaches. Government-regulated medical lasers are designed to deliver focused light energy that targets melanin in affected skin layers while sparing surrounding tissues, enabling clinicians to correct uneven pigmentation more effectively with fewer sessions. According to the U.S. FDA information on medical lasers, these devices are approved for use in removing sunspots, birthmarks, and other skin conditions, illustrating broad recognition of their clinical value in pigment-related treatments. In clinical practice patterns documented in medical literature, 19% of dermatologists reported spending more than half of their clinical time performing laser treatments, and 53% spent at least 25% of their time on laser procedures, reflecting high utilization of these technologies in dermatologic settings.

In melasma care, established systems such as Q-switched lasers, fractional non-ablative lasers, and intense pulsed light (IPL) complement topical regimens by selectively disrupting pigment with controlled energy and stimulating skin remodeling. As clinicians adopt advanced platforms that offer adjustable wavelengths and pulse durations tailored to individual skin types, treatment outcomes for melasma have improved, encouraging broader patient demand. This alignment of regulatory clearance, clinical application, and patient acceptance continues to drive adoption of laser-based interventions across aesthetic and medical dermatology.

Barrier Analysis - High Cost of Laser and Light Treatments

High treatment costs limit the broader adoption of laser and light therapies in melasma care, restraining market expansion despite strong clinical interest. Capital-intensive devices require significant upfront investment by clinics, followed by ongoing costs for maintenance, consumables, calibration, and staff training. These expenses translate into higher procedure prices for patients, narrowing access beyond urban and premium dermatology centers.

Out-of-pocket payment models dominate aesthetic dermatology, which reduces uptake among price-sensitive consumers and delays repeat treatment cycles needed for sustained pigment control. Cost barriers also influence provider expansion plans, slowing equipment penetration in tier-2 and tier-3 cities. As melasma management often requires multiple sessions and long-term maintenance, total treatment cost escalates over time, increasing patient drop-off rates. This pricing dynamic concentrates demand in higher-income segments and constrains volume growth for device-driven treatment pathways.

Recurrence Risk and Patient Compliance

Recurrence risk and patient compliance constraints limit the sustained effectiveness of melasma treatment pathways and act as a restraint on market growth. Melasma presents a chronic, relapsing profile, which requires long-term maintenance therapy and strict photoprotection to preserve outcomes. Many patients discontinue treatment after visible improvement, reducing long-term therapy adherence and weakening repeat demand for clinical procedures and prescription topicals. Daily sunscreen use, avoidance of peak UV exposure, and consistent use of maintenance regimens demand behavioral discipline that is difficult to sustain at scale.

Inconsistent follow-through increases relapse frequency, leading to patient dissatisfaction and lower perceived treatment value. This dynamic affects clinic retention metrics and slows revenue continuity for device-based therapies that depend on multi-session protocols. Providers face higher counselling burdens to set realistic expectations, while variable adherence undermines predictable treatment cycles and reduces conversion rates from initial consultation to long-term care plans.

Opportunity Analysis - Innovation in Combination Therapies and Tranexamic Acid

Research shows melasma prevalence varies significantly, affecting an estimated 1% to 33% of people depending on population and sun exposure levels, and is more common in darker skin phototypes where UV exposure is high, highlighting the need for effective treatments. Clinical studies registered on government-linked trial registries confirm that tranexamic acid (TA) has been investigated in structured clinical settings for melasma management, evaluated as both oral and topical formulations alongside standard therapies.

Emerging evidence supports combining TA with established agents such as hydroquinone and tretinoin to improve outcomes, offering an opportunity to enhance therapeutic effectiveness beyond conventional monotherapies. Combination approaches involving TA target melanogenesis pathways more effectively, potentially reducing pigmentation severity and recurrence while aligning with clinical practice patterns that favor multimodal regimens. Given the high prevalence of melasma and the limitations of current treatments, innovation in combination therapies that incorporate tranexamic acid represents a meaningful avenue for market growth and improved clinical results.

Teledermatology and Digital Consultations

Digital access to dermatology specialists through remote consultations is expanding treatment opportunities for melasma patients by reducing geographic and logistical barriers to specialized care. According to the Ministry of Health and Family Welfare, India’s national telemedicine platform eSanjeevani, has served over 311 million patients through teleconsultations, allowing individuals to connect with registered practitioners for a range of conditions without traveling to clinics or hospitals, which supports broader access to dermatology advice and follow-up care. This level of uptake highlights the scale at which digital consultations are being used in a public health context. Integrating teledermatology into existing telehealth infrastructure enables patients in underserved or rural regions to receive timely evaluation, treatment planning, and ongoing support for melasma management, strengthening continuity of care and reducing the burden on in-person specialist services.

Advanced digital health policy frameworks have significantly increased clinician engagement and patient outreach. Government-endorsed telemedicine guidelines ensure that dermatologists can deliver remote care within regulated standards, enhancing diagnostic convenience and patient adherence to treatment regimens. Such digital enablement supports early intervention, improves patient education on skincare protocols, and facilitates monitoring of treatment outcomes, which can enhance patient satisfaction and overall market utilization rates for melasma therapies across broader demographic groups.

Category-wise Analysis

Product Type Insights

The medication segment is anticipated to dominate the market, accounting for approximately 48% of the market share in 2026. Its dominance is driven by routine clinical use of topical and oral therapies in dermatology practice. Prescription agents such as hydroquinone, azelaic acid, retinoids, and combination creams remain first-line options due to documented efficacy in reducing hyperpigmentation severity and improving skin tone uniformity. Public health guidance emphasizes sun protection alongside pharmacologic therapy, reinforcing adherence and outcomes. Real-world treatment pathways favor medicines as they are affordable, scalable through primary care and dermatology clinics, and suitable for long-term management. Prescription use of Tri-Luma cream by Galderma. Tri-Luma combines fluocinolone acetonide, hydroquinone, and tretinoin and is approved for short-term treatment of moderate-to-severe facial melasma. This approval and labeling are officially documented by the U.S. Food and Drug Administration.

Laser and light treatment represent the fastest-growing product type, due to clinics adopting device-based therapies to address treatment-resistant pigmentation. These procedures target melanin with controlled energy delivery, supporting pigment dispersion and skin tone improvement under medical supervision. Growth is supported by rising availability of dermatology clinics, increasing patient demand for faster visible results, and expanding clinical training in energy-based devices. Public health guidance highlights sun protection and clinician-directed care for pigmentary disorders, which aligns with supervised in-clinic procedures. PicoWay laser system developed by Candela Corporation. In 2023, the U.S. Food and Drug Administration cleared PicoWay for treating melasma, lentigines, and other pigmentary conditions, expanding its use beyond prior indications such as acne scarring.

Route of Administration Insights

The topical segment is expected to dominate the market, contributing nearly 72% of revenue in 2026, fueled by its role as first-line therapy in routine dermatology care. Creams and gels allow localized delivery of depigmenting agents, supporting consistent use under medical guidance. Public health guidance promotes sun protection and clinician-directed management of pigmentary disorders, pairing naturally with daily topical regimens. Topicals fit outpatient workflows, require no specialized equipment, and suit long-term maintenance plans. Esoterica Cream is an over-the-counter lightening cream used for melasma and other hyperpigmentation. Esoterica contains 2 % hydroquinone, a well-recognized tyrosinase-inhibiting agent that reduces melanin production in affected areas and is applied directly to dark patches to lighten them over weeks of regular use.

The oral segment represents the fastest-growing route of administration, propelled by research and clinical practice that increasingly explore systemic therapies to complement topical care. Oral agents such as tranexamic acid have gained traction for moderate to severe cases due to evidence showing reduced pigment formation through inhibition of plasmin activity in the skin. This systemic approach is sought when topicals alone are insufficient, especially in patients with recurrent or widespread melasma. TRANSINO EX, an oral tablet containing tranexamic acid that is marketed in Japan for the improvement of melasma and age-spot pigmentation. TRANSINO EX tablets are taken orally, typically twice a day, and contain tranexamic acid as the active ingredient, shown in clinical studies to significantly reduce melasma severity when administered systemically rather than topically.

Regional Insights

North America Melasma Treatment Market Trends

North America is projected to dominate, accounting for nearly 38% of the share in 2026, driven by the region’s high aesthetic dermatology expenditure, strong OTC and prescription availability, and high public awareness of pigmentation solutions. Distribution systems in the U.S. and Canada provide extensive support for melasma treatment programs, ensuring wide accessibility across topical, medication, and dermatology populations. Increasing demand for fast-acting, convenient, and easy-to-use forms is further accelerating adoption, as these formats improve skin appearance and reduce barriers associated with chronic pigmentation.

Innovation in melasma treatment technology, including stable tranexamic, improved laser delivery, and targeted combination enhancement, is attracting significant investment from both public and private sectors. Government initiatives and AAD campaigns continue to promote use against pigmentation risks, psychological concerns, and emerging aesthetic threats, creating sustained market demand. The growing focus on oral grades and specialty uses, particularly for topical and others, is expanding the target applications for melasma treatment.

Europe Melasma Treatment Market Trends

Market growth in Europe is increasing awareness of pigmentation treatment benefits, strong regulatory systems, and government-led dermatology programs. Countries such as Germany, the U.K., France, and Italy have well-established aesthetic frameworks that support routine melasma treatment use and encourage adoption of innovative laser and oral delivery methods. These high-efficacy formulations are particularly appealing for topical populations, regulation-conscious clinics, and dermatology users, improving clearance and coverage rates.

Technological advancements in melasma treatment development, such as enhanced picosecond lasers, application-targeted delivery, and improved tranexamic grades, are further boosting market potential. European authorities are increasingly supporting research and trials for treatments against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, safe options is aligned with the region’s focus on preventive psychological impact and skin health. Public awareness campaigns and promotion drives are expanding reach in both dermatology and hospital segments, while suppliers are investing in combination therapies and novel variants to increase efficacy.

Asia Pacific Melasma Treatment Market Trends

Asia Pacific is likely to be the fastest-growing market for melasma treatment, driven by rising aesthetic awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, South Korea, and Thailand are actively promoting treatment campaigns to address pigmentation growth and emerging beauty needs. Melasma treatments are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale dermatology and topical drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-use melasma treatments, which can withstand challenging sun exposure and minimize recurrence. These innovations are critical for reaching domestic clinics and improving overall skin-care coverage. Growing demand for topical medications and dermatology applications is contributing to market expansion. Public-private partnerships, increased aesthetic expenditure, and rising investment in melasma research and clinic capacity are further accelerating growth. The convenience of treatment delivery, combined with improved clearance and reduced risk of relapse, positions it as a preferred choice.

Competitive Landscape

The global melasma treatment market reflects active competition between established dermatology leaders and emerging laser-technology specialists. In North America and Europe, Galderma and Lutronic maintain strong positions through sustained R&D investment, dense clinic networks, and long-term physician engagement, supported by innovation across topical therapies and energy-based devices. These strengths reinforce brand trust and accelerate clinical adoption. In Asia Pacific, regional manufacturers expand access with cost-competitive solutions, supporting broader uptake across private clinics and outpatient centers.

Topical delivery anchors daily management, supports maintenance regimens, and reduces relapse risk when paired with sun-protection counseling. Laser-based modalities address deeper or treatment-resistant pigmentation, increasing procedure demand in refractory cases. Strategic partnerships, co-development programs, and targeted acquisitions combine pharmaceutical expertise with device innovation, broadening portfolios, strengthening distribution, and shortening time-to-market across high-growth regions.

Key Industry Developments

- In October 2025, Pearl E. Grimes, MD, a leading authority on vitiligo and pigmentary disorders, launched P’erl: The Melasma Research & Treatment Institute, a center dedicated to advancing research and care for melasma. Grimes established the institute to drive focused scientific inquiry, expand clinical innovation, and raise awareness of a condition long underrecognized in dermatology. She stated that the initiative aimed to bring awareness and research to the forefront for a disease that had remained neglected for too long.

Companies Covered in Melasma Treatment Market

- Lutronic

- Lumenis

- Asclepion Laser Technologies

- Galderma

- Syneron Candela

- Fotona

- BISON Medical

- Lynton Lasers

- Cynosure

- Astanza Laser

- Others

Frequently Asked Questions

The global melasma treatment market is projected to reach US$3.5 billion in 2026.

Growing awareness of pigmentary disorders and better access to dermatology clinics increase diagnosis and treatment uptake, pushing demand for prescription topicals and in-clinic procedures.

The melasma treatment market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Co-prescribing topicals with laser or light procedures improves outcomes in resistant cases, opening room for bundled care pathways and higher clinic revenues.

Galderma, Lutronic, Lumenis, Cynosure, and Syneron Candela are the key players.