- Bulk Chemicals

- Maleic Anhydride Market

Maleic Anhydride Market Size, Share, and Growth Forecast 2026 - 2033

Maleic Anhydride Market by Raw Material (n-Butane, Benzene), by Production Process (n-Butane Oxidation, Benzene Oxidation), by Application (Unsaturated Polyester Resins, 1,4-Butanediol, Lubricating Oil Additives, Copolymers, Surfactants & Plasticizers, Fumaric Acid & Malic Acid, Alkenyl Succinic Anhydride, Others), by End-Use, by Regional Analysis, 2026 - 2033

Maleic Anhydride Market Size and Trend Analysis

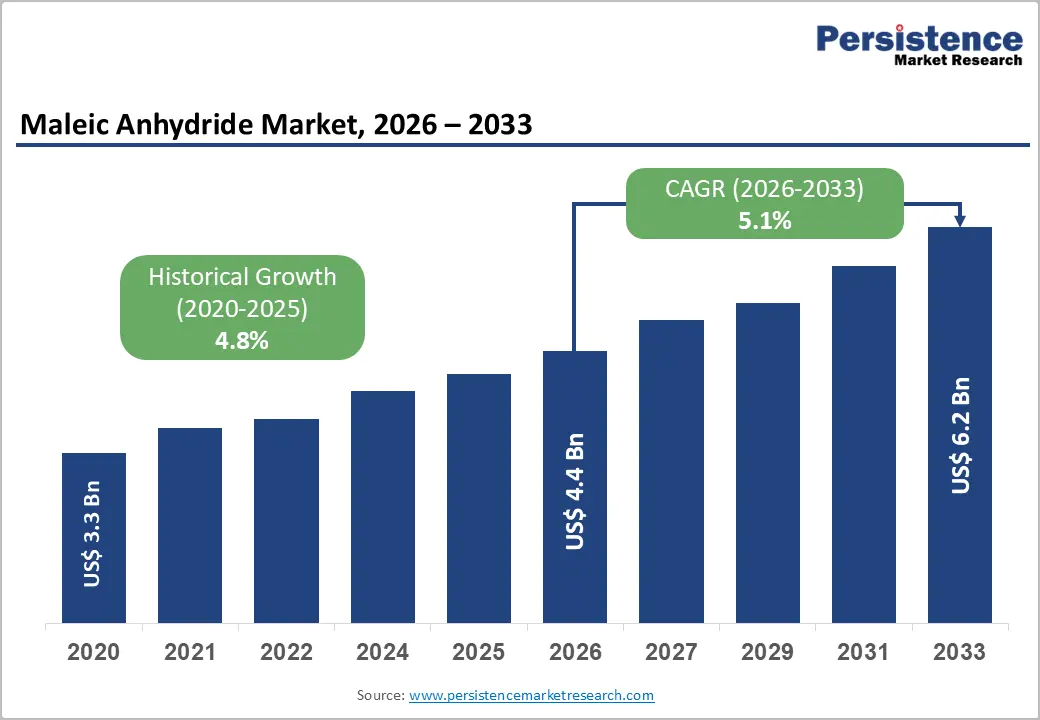

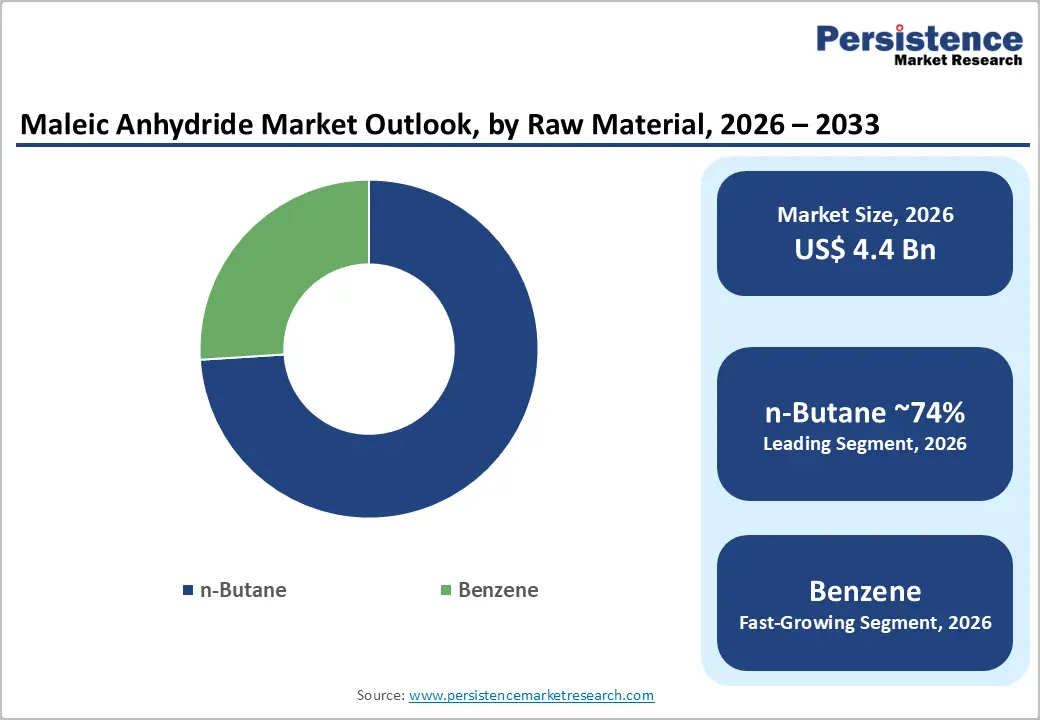

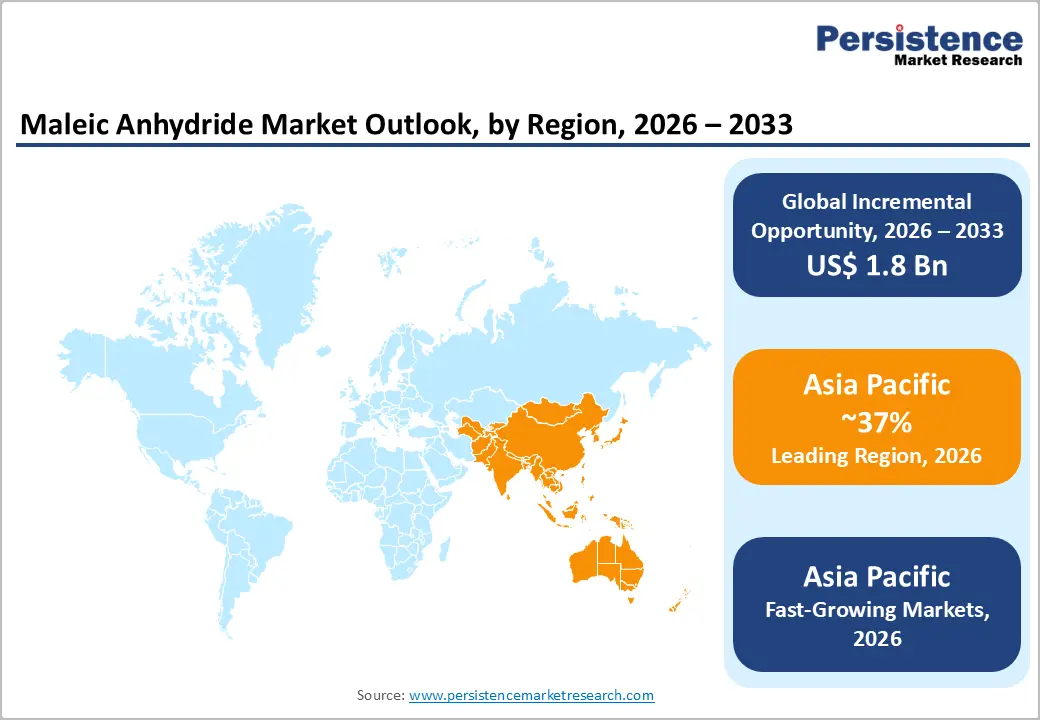

The global maleic anhydride market size is likely to be valued at US$4.4 billion in 2026 and is expected to reach US$6.2 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033.

The market is expanding steadily, driven by robust demand from unsaturated polyester resin manufacturers serving the construction and automotive sectors, growing consumption of 1,4-Butanediol (BDO) in engineering polymers and spandex fiber production, and the progressive shift from benzene-based to n-butane-based production processes delivering superior cost economics and environmental compliance.

Key Market Highlights

- Leading Region: East Asia, led by China, dominates the global maleic anhydride market holding 37% share, commanding the majority of production capacity and consumption, supported by the China Petroleum and Chemical Industry Federation (CPCIF) and government-backed chemical industrial park investment under the 14th Five-Year Plan.

- Fastest Growing Region: India and Southeast Asia are the fastest-growing sub-regional markets within Asia Pacific with rising CAGR of 6.8%, driven by the National Infrastructure Pipeline (NIP), expanding automotive composites demand, and a growing UPR consumption base across construction and packaging industries.

- Dominant Segment: Unsaturated Polyester Resins (UPR) lead the Application segment with approximately 48% market share, underpinned by robust glass fiber-reinforced plastic demand from construction, wind energy composites, and marine applications globally, and by ACMA's reported 9 billion-pound U.S. composites output.

- Fastest Growing Segment: The Automotive & Transportation end-use segment is registering above-market growth, fueled by EV lightweighting mandates and global EV sales surpassing 14 million units in 2023 per the IEA, driving demand for maleic anhydride-based UPR composites in EV structural components.

- Key Market Opportunity: Bio-based maleic anhydride production represents the most strategically significant growth opportunity, aligned with the EU Bioeconomy Strategy and European Green Deal incentives, enabling producers to reduce their dependency on fossil feedstocks, access sustainability premiums, and hedge against fossil fuel price volatility through 2033.

Market Dynamics

Market Growth Drivers

Rising Demand for Unsaturated Polyester Resins in Construction and Composites

Unsaturated polyester resins (UPR), the single largest downstream application of maleic anhydride, are experiencing accelerating demand driven by large-scale infrastructure investment, renewable energy deployment, and the adoption of lightweight composites across the automotive and marine sectors. Maleic anhydride serves as the critical difunctional acid component in UPR synthesis, accounting for approximately 50-55% of global maleic anhydride production.

According to the U.S. Department of Transportation (DOT), the Infrastructure Investment and Jobs Act authorized US$1.2 trillion in federal infrastructure spending through 2026, driving substantial construction activity and demand for fiber-reinforced polymer (FRP) composites, which rely heavily on UPR, in bridge decking, piping, and structural applications. The global wind energy sector's expansion, with the International Energy Agency (IEA) projecting wind power capacity to triple by 2030, further amplifies UPR and maleic anhydride demand for turbine blade composites.

Expanding 1,4-Butanediol (BDO) Production and Downstream Polymer Demand

The 1,4-Butanediol (BDO) production chain, which uses maleic anhydride as a key feedstock via the Reppe or maleic anhydride hydrogenation processes, is emerging as a high-growth driver of demand for the global maleic anhydride market. BDO is a critical precursor for polybutylene terephthalate (PBT), tetrahydrofuran (THF), and gamma-butyrolactone (GBL), materials extensively used in engineering plastics, spandex fiber, and pharmaceutical solvents.

According to IHS Markit (now S&P Global Commodity Insights), global BDO demand has been growing at approximately 4-5% annually, supported by robust growth in spandex fiber production, particularly in China and India, and by the expanding engineering thermoplastics market, driven by automotive lightweighting mandates. The accelerating adoption of bio-based BDO derived from renewable maleic anhydride also adds a sustainability dimension, reinforcing long-term demand.

Market Restraints

Volatility in Feedstock Prices, n-Butane and Benzene

The maleic anhydride market is highly susceptible to price volatility in its primary feedstocks, n-butane and benzene, both of which are derivatives of crude oil and natural gas processing. According to the U.S. Energy Information Administration (EIA), natural gas liquid (NGL) prices, which govern n-butane costs, have exhibited significant interannual volatility, with price swings of 30-50% observed during periods of geopolitical disruption and supply-demand imbalances. Benzene prices are similarly linked to crude oil market dynamics.

This feedstock price instability compresses producer margins and complicates long-term contract pricing for maleic anhydride manufacturers, particularly mid-tier producers lacking backward integration into feedstock supply chains.

Environmental Regulations and VOC Emission Controls on Production Facilities

Maleic anhydride production, particularly via benzene oxidation, generates volatile organic compound (VOC) emissions and requires stringent waste gas treatment systems to comply with environmental regulations. The U.S. Environmental Protection Agency (EPA) classifies maleic anhydride production facilities under the National Emission Standards for Hazardous Air Pollutants (NESHAP), imposing compliance costs that constrain capacity expansion for legacy producers.

In the European Union, the Industrial Emissions Directive (IED) mandates best available techniques (BAT) for chemical production, escalating operating costs for European maleic anhydride manufacturers and reducing their cost competitiveness relative to Asian producers operating under less stringent regulatory frameworks.

Market Opportunities

Bio-Based Maleic Anhydride Production from Renewable Feedstocks

The development of bio-based maleic anhydride derived from renewable feedstocks, including furfural from agricultural residues and itaconic acid from fermentation, represents a high-potential growth opportunity aligned with global chemical industry decarbonization objectives. The European Green Deal and the EU Bioeconomy Strategy are actively promoting bio-based chemical production as a pathway to reducing dependency on fossil feedstocks and carbon emissions.

According to the European Bioplastics Association, the bio-based chemicals sector is expected to grow significantly through 2030, with bio-based succinic acid and maleic anhydride derivatives positioned as key commercial targets. Companies investing in bio-based maleic anhydride production technologies stand to access premium pricing in sustainability-focused markets, capture EU regulatory incentives, and reduce exposure to fossil feedstock price volatility, a significant competitive differentiator as carbon pricing mechanisms tighten.

Growing Demand from the Automotive Lightweighting and EV Composites Sector

The global automotive industry's accelerating shift toward electric vehicles (EVs) and lightweight composite materials is generating incremental and structurally growing demand for maleic anhydride through its UPR and engineering polymer derivatives. According to the International Energy Agency (IEA), global EV sales surpassed 14 million units in 2023, representing approximately 18% of all new car sales, with the global EV fleet projected to reach 240 million vehicles by 2030 under stated policy scenarios.

EV battery enclosures, structural body panels, and underbody components increasingly use glass fiber-reinforced UPR composites to reduce weight and improve thermal management. Additionally, maleic anhydride-derived alkenyl succinic anhydride (ASA) is gaining adoption as a paper sizing agent in EV battery separator production. The European Automotive Manufacturers Association (ACEA) reports that the use of composite materials in new vehicle platforms is expected to grow significantly through 2030, creating a durable and expanding demand vector for maleic anhydride.

Category-wise Insights

Raw Material Analysis

n-Butane is the dominant raw material in the global Maleic Anhydride Market, accounting for approximately 74% of total production volume. The decisive shift from benzene to n-butane as the preferred feedstock has been driven by n-butane's lower cost, higher maleic anhydride yield per unit of feedstock processed, and significantly more favorable environmental and regulatory profile.

The U.S. Environmental Protection Agency (EPA) and EU REACH regulations classify benzene as a confirmed human carcinogen, compelling producers in regulated markets to phase out benzene-based production routes in favor of the n-butane oxidation process. According to the American Fuel and Petrochemical Manufacturers (AFPM), the United States, the world's largest n-butane producer by virtue of its extensive shale gas processing infrastructure, benefits from abundant and cost-competitive n-butane supply, reinforcing the feedstock's dominance in North American maleic anhydride production.

Production Process Analysis

n-Butane Oxidation constitutes the dominant production process, accounting for approximately 73% of global maleic anhydride production capacity. The n-butane oxidation process, commercialized through fixed- and fluidized-bed reactor technologies using vanadium phosphorus oxide (VPO) catalysts, has largely supplanted benzene oxidation in modern production facilities due to its lower feedstock cost, higher selectivity, and compliance with environmental regulations that restrict benzene handling and emissions.

According to the American Chemistry Council (ACC), virtually all new maleic anhydride capacity additions in North America and Western Europe since 2000 have employed n-butane oxidation technology. The process delivers maleic anhydride yields of approximately 55-60 mol%, superior to benzene oxidation routes. Leading producers including BASF SE, Huntsman Corporation, and INEOS operate large-scale n-butane oxidation facilities as their primary production technology.

Application Analysis

Unsaturated Polyester Resins (UPR) represent the dominant application segment, accounting for approximately 48% of total maleic anhydride consumption globally. UPR, synthesized from maleic anhydride and glycols, serves as the matrix resin in glass fiber-reinforced plastic (GRP) composites used across construction, marine, wind energy, transportation, and sanitary ware applications. The versatility of UPR formulations, ranging from general-purpose to fire-retardant and corrosion-resistant grades, ensures broad end-market applicability.

According to the American Composites Manufacturers Association (ACMA), the U.S. composites industry produces approximately 9 billion pounds of product annually, with UPR-based systems accounting for the majority of production volume. The global wind energy buildout, with the IEA projecting over 7,000 GW of installed wind capacity by 2030, is a major structural growth catalyst for UPR and maleic anhydride demand.

End-Use Analysis

Construction represents the dominant end-use segment, accounting for approximately 32% of total Maleic Anhydride Market demand. Maleic anhydride, primarily through its UPR and fumaric acid derivatives, is extensively used in construction applications, including fiber-reinforced polymer (FRP) pipes, tanks, cladding, roofing, and sanitary ware components.

The global construction industry's sustained expansion, particularly in Asia Pacific and the Middle East, is generating robust and recurring demand for composite materials reliant on maleic anhydride-based resins. According to the Oxford Economics Global Construction Outlook, global construction output is projected to grow by 35% to reach approximately US$15.2 trillion by 2030, with infrastructure and residential construction in emerging markets serving as the primary growth catalysts. Maleic anhydride-derived coatings and adhesives are also used in construction-grade sealants and waterproofing membranes.

Regional Insights

North America Maleic Anhydride Market Trends

The United States leads the North American maleic anhydride market, supported by abundant and cost-competitive n-butane feedstock availability from the country's expansive shale gas processing infrastructure, and a large, mature downstream composites and chemical manufacturing industry. According to the U.S. Energy Information Administration (EIA), the U.S. produces approximately 700,000-750,000 barrels per day of n-butane as a natural gas liquid byproduct, providing domestic maleic anhydride producers with a structural feedstock cost advantage over global peers. The Infrastructure Investment and Jobs Act is generating sustained demand for FRP composites in infrastructure rehabilitation, catalyzing maleic anhydride consumption through UPR applications.

Canada's market is supported by its petrochemical manufacturing base in Alberta and Ontario, with maleic anhydride consumed primarily in UPR for construction and marine applications. The U.S. EPA's NESHAP regulations governing maleic anhydride plant emissions are compelling capacity modernization among legacy producers, incentivizing investment in next-generation n-butane oxidation processes with superior emission control performance. North America's advanced composites manufacturing cluster, anchored in the U.S. Southeast and Midwest, sustains strong baseline demand for maleic anhydride and its downstream derivatives.

Europe Maleic Anhydride Market Trends

Europe represents a mature but innovation-driven maleic anhydride market, anchored by significant production capacity in Germany, Italy, and the United Kingdom. BASF SE (Germany), Polynt-Reichhold Group (Italy/Germany), and INEOS (U.K.) operate major European production facilities. The EU's Industrial Emissions Directive (IED) and the European Green Deal are compelling producers to adopt best available techniques (BAT) for emission reduction and to transition toward more sustainable production pathways, including bio-based feedstocks. According to Eurostat, the EU chemical industry generates approximately €750 Billion in annual output, with specialty chemicals including maleic anhydride representing a critical intermediary layer.

Germany's robust automotive manufacturing sector, with ACEA reporting over 3.5 Million vehicle production units in 2023, drives UPR and engineering polymer demand directly linked to maleic anhydride consumption. France and Spain are significant consumers of maleic anhydride-based UPR in construction and wind energy applications, aligned with the EU's renewable energy deployment targets under REPowerEU. Regulatory harmonization under EU REACH restricts benzene-based production, accelerating the region's transition to n-butane oxidation technology and supporting the development of bio-based maleic anhydride production initiatives funded through Horizon Europe research programs.

Asia Pacific Maleic Anhydride Market Trends

Asia Pacific dominates global maleic anhydride production and consumption, with China accounting for the majority of regional and global output. According to the China Petroleum and Chemical Industry Federation (CPCIF), China's maleic anhydride production capacity has expanded rapidly over the past decade, driven by government investment in chemical industrial parks and robust domestic demand from UPR manufacturers serving the construction, wind energy, and sanitary ware sectors. China's 14th Five-Year Plan designates high-performance composite materials as a strategic industry, supporting sustained capital investment in maleic anhydride and UPR production capacity. Major Chinese producers, including Zibo Qixiang Tengda Chemical Co., Ltd. and Tianjin Bohai Chemical Industry Group, supply both domestic and export markets.

India is an increasingly significant growth market, supported by rapid infrastructure development under the National Infrastructure Pipeline (NIP) targeting US$1.4 trillion in investment through 2025, and strong domestic demand from the automotive composites and agricultural chemicals sectors. According to the Ministry of Chemicals and Fertilizers of India, the Indian specialty chemicals sector is growing at approximately 12% annually. In Southeast Asia, the expanding construction and packaging industries are driving incremental demand for maleic anhydride. Japan maintains a technologically advanced maleic anhydride derivatives industry, with Nippon Shokubai Co., Ltd., a leading producer of maleic anhydride-based specialty chemicals serving global markets.

Competitive Landscape

The global Maleic Anhydride Market is moderately consolidated, with a limited number of large-scale producers including BASF SE, Huntsman Corporation, Polynt-Reichhold Group, INEOS, and Mitsubishi Chemical Corporation commanding significant collective share of global capacity. These leaders differentiate through backward integration into feedstock supply chains, proprietary VPO catalyst technology, and diversified downstream derivative portfolios.

Asian producers, particularly in China, compete aggressively on cost, leveraging economies of scale and lower operating costs to export into global markets. Key competitive strategies include capacity expansion in high-growth Asian markets, R&D investment in bio-based maleic anhydride production routes, and strategic partnerships with UPR and BDO manufacturers. Long-term offtake agreements with downstream composites and polymer producers are an emerging business model trend providing revenue visibility and margin stability.

Key Market Developments

- In January 2025: BASF SE announced an investment in upgrading its Ludwigshafen maleic anhydride production facility with enhanced emission control systems and process efficiency improvements, aligned with the company's carbon neutrality targets under its BASF sustainability roadmap.

- In September 2024: Huntsman Corporation expanded its maleic anhydride derivative portfolio through a strategic supply agreement with a major European composites manufacturer, targeting UPR demand growth driven by the offshore wind energy sector expansion in the North Sea.

- In March 2024: Polynt-Reichhold Group commissioned capacity expansion at its Italian maleic anhydride production facility, responding to growing UPR demand in southern European construction and marine markets and strengthening its position as the leading European maleic anhydride producer.

Maleic Anhydride Market Report - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.3 Bn |

| Current Market Value (2026) | US$ 4.4 Bn |

| Projected Market Value (2033) | US$ 6.2 Bn |

| CAGR (2026-2033) | 5.1% |

| Leading Region | East Asia, 37% share |

| Dominant Application | Unsaturated Polyester Resins (UPR), 48% share |

| Top-ranking Raw Material | n-Butane, 74% |

| Incremental Opportunity | US$ 1.8 Bn |

Companies Covered in Maleic Anhydride Market

- Huntsman Corporation

- LANXESS AG

- Mitsubishi Chemical Corporation

- Nippon Shokubai Co., Ltd.

- Polynt-Reichhold Group

- BASF SE

- Ashland Global Holdings Inc.

- Thirumalai Chemicals Ltd.

- IG Petrochemicals Ltd.

- MOL Hungarian Oil & Gas Plc

- Zibo Qixiang Tengda Chemical Co., Ltd.

- Changzhou Yabang Chemical Co., Ltd.

- Jiangyin Shunfei Fine Chemical Co., Ltd.

- Tianjin Bohai Chemical Industry Group

- INEOS

- Lonza Group

- Bartek Ingredients Inc.

- Flint Hills Resources

Frequently Asked Questions

The global Maleic Anhydride Market is projected to reach US$ 6.2 Billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026-2033 from an estimated US$ 4.4 Billion in 2026. The market recorded a historical CAGR of 4.8% during 2020-2025, driven by sustained growth in UPR demand, BDO production expansion, and increasing construction and automotive composite applications.

The primary drivers are rising demand for Unsaturated Polyester Resins (UPR) in glass fiber-reinforced composites for construction and wind energy applications, supported by the U.S. Infrastructure Investment and Jobs Act (US$ 1.2 Trillion) and the IEA's projection of tripled global wind capacity by 2030, combined with expanding 1,4-Butanediol (BDO) production for engineering plastics and spandex fibers growing at 4.5% annually.

n-Butane is the dominant raw material, accounting for approximately 74% of global maleic anhydride production. Its dominance is driven by lower cost versus benzene, superior yield, and the classification of benzene as a human carcinogen under EPA and EU REACH regulations, compelling producers to transition to n-butane oxidation processes. The U.S. benefits from abundant n-butane supply from shale gas processing, producing approximately 700,000-750,000 barrels per day per the EIA.

Asia Pacific, led by China, dominates the global Maleic Anhydride Market in both production capacity and consumption. China's leadership is supported by government-backed chemical industrial park investment under the 14th Five-Year Plan, the China Petroleum and Chemical Industry Federation (CPCIF), and large domestic UPR markets serving construction, wind energy, and sanitary ware manufacturing sectors. India and Southeast Asia represent the fastest-growing regional sub-markets.

Bio-based maleic anhydride production from renewable agricultural feedstocks represents the defining strategic growth opportunity. Aligned with the EU Bioeconomy Strategy and European Green Deal decarbonization mandates, bio-based maleic anhydride enables producers to access sustainability premiums, qualify for regulatory incentives, and reduce dependence on volatile fossil feedstock pricing, positioning early movers for significant competitive advantage as carbon pricing mechanisms intensify through 2033.

Leading companies in the global Maleic Anhydride Market include BASF SE, Huntsman Corporation, Polynt-Reichhold Group, INEOS, Mitsubishi Chemical Corporation, Nippon Shokubai Co., Ltd., LANXESS AG, Ashland Global Holdings Inc., Thirumalai Chemicals Ltd., IG Petrochemicals Ltd., MOL Hungarian Oil & Gas Plc, Zibo Qixiang Tengda Chemical Co., Ltd., Tianjin Bohai Chemical Industry Group, and Changzhou Yabang Chemical Co., Ltd., among others.