- Automation & Robotics

- Radar Simulator Market

Radar Simulator Market Size, Share, and Growth Forecast 2026 - 2033

Radar Simulator Market by Component (Hardware, Software, Services), by Platform (Airborne, Naval/Marine, Ground, Space-based), by Application (Training & Education, System Testing & Validation, Research & Development, Mission Rehearsal), by End-user (Military & Defence, Commercial Aviation, Research Institutions, Others), by Regional Analysis, 2026 - 2033

Radar Simulator Market Size and Trend Analysis

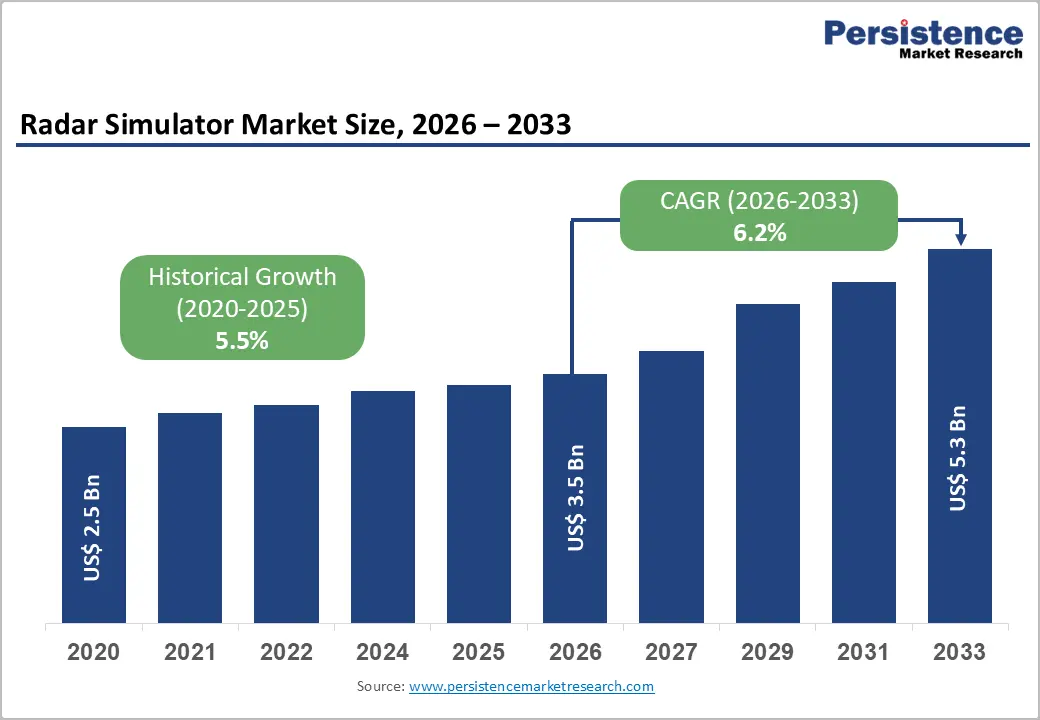

The global radar simulator market size is expected to be valued at US$ 3.5 billion in 2026 and is projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Rising geopolitical tensions, surging defense modernization budgets, and the growing complexity of next-generation radar systems are collectively driving robust global demand for high-fidelity radar simulation platforms. According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure reached US$ 2,718 billion in 2024, a real increase of 9.4%, the steepest year-on-year rise since the end of the Cold War, with all 32 NATO member states increasing their defense spending.

Simultaneously, the shift toward cost-effective, risk-free simulation-based training over live radar exercises, the integration of active electronically scanned array (AESA) radar systems that require sophisticated test validation tools, and the acceleration of civil aviation safety mandates are reinforcing market growth across both military and commercial end-user segments.

Key Industry Highlights

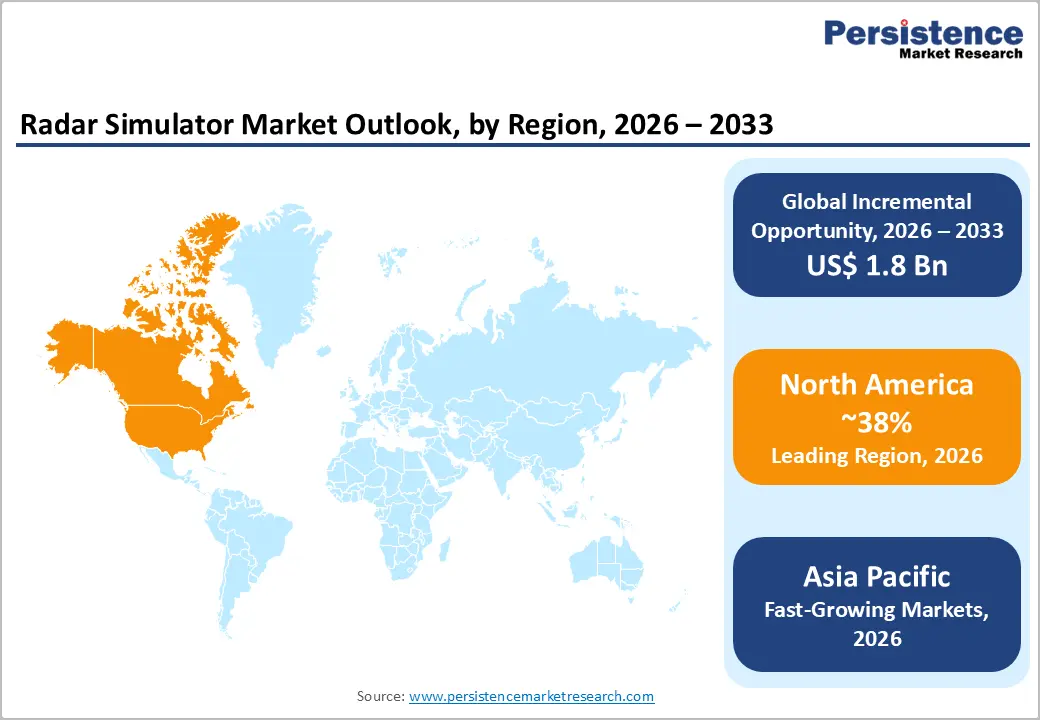

- Leading Region: North America leads the global radar simulator market with approximately 38% share in 2025, anchored by U.S. defense spending of US$ 997 billion in 2024 and deep institutional adoption of simulation-based training across defense and civil aviation sectors.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market over 2026 - 2033, with Japan's 21% defense spending surge, China's sustained 7% annual military budget growth, and India's US$ 86.1 billion defense program driving unprecedented radar simulator procurement demand.

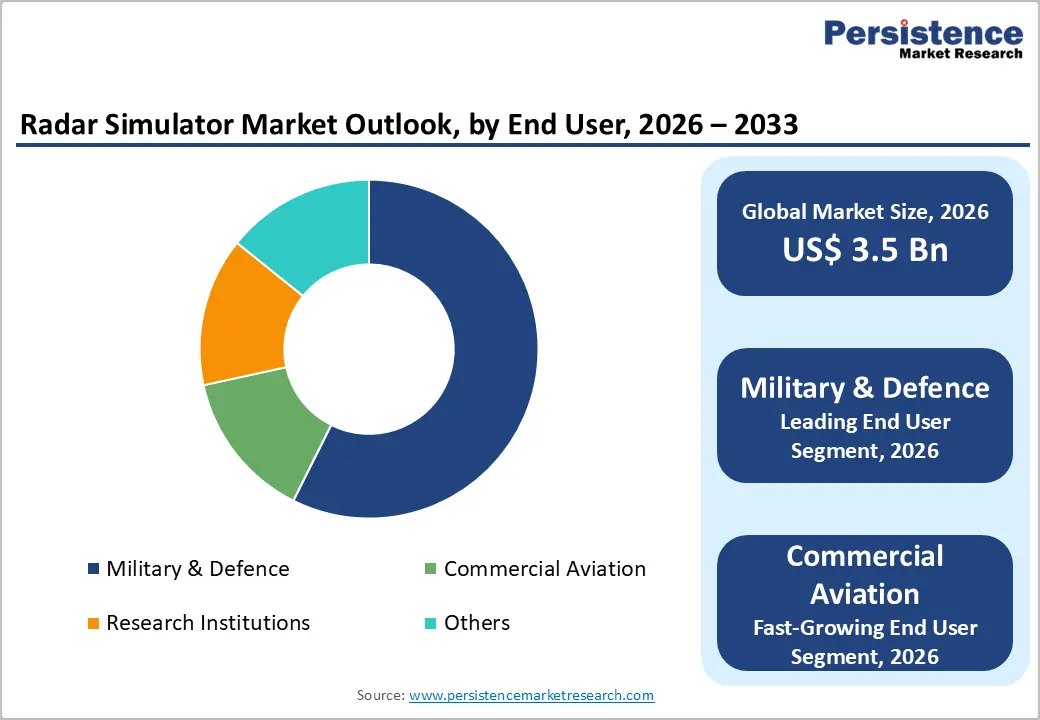

- Dominant End-User: The military & defence commands approximately 60% of global radar simulator market revenue in 2025, driven by mandatory training certification requirements, NATO modernization commitments, and the U.S. DoD's US$ 179 billion FY2026 RDT&E budget request.

- Fastest Growing Component Type: The Software component segment is the fastest-growing category over 2026 - 2033, fueled by AI-powered simulation platforms, cloud-based delivery models, digital twin integration, and high total cost of ownership advantages over hardware-intensive configurations.

- Key Opportunity: Vendors offering AI-driven adaptive simulation environments and cloud-hosted, subscription-based radar training platforms are positioned to capture the highest incremental growth, lowering barriers for emerging defense forces and commercial aviation operators across the Asia Pacific and beyond.

Market Dynamics

Drivers - Surging Global Defense Budgets and Military Radar Modernization Programs

The unprecedented surge in global defense spending is the most powerful structural driver of the radar simulator market. SIPRI's April 2025 data confirms that the United States allocated US$ 997 billion to defense in 2024, representing 37% of all global military spending, with a significant portion channeled toward modernizing radar, electronic warfare, and surveillance systems.

NATO members collectively spent US$ 1,506 billion in 2024, representing 55% of world military expenditure. The U.S. Department of Defense proposed US$ 179 billion for Research, Development, Test and Evaluation (RDT&E) in its FY2026 budget, a 27% year-on-year increase, directly stimulating demand for advanced radar simulation tools used in system validation, electronic countermeasure testing, and operator proficiency training.

Growing Complexity of Radar Systems Driving Demand for Simulation-Based Testing

The proliferation of advanced radar architectures, including AESA, digital beamforming, cognitive radar, and multifunction radar systems, has made traditional hardware-in-the-loop testing increasingly expensive and logistically complex. Radar simulators provide a controlled, repeatable, and cost-efficient environment for system design validation, performance benchmarking, and operator training without the risks inherent to live operations.

In March 2024, the Indian Navy inducted its first Radar Simulator (RADSIM) at the Aircraft Carrier Training School (AIRCATS) in Goa, reflecting the growing institutional preference for simulation-based training among defense forces globally. Similarly, commercial aviation authorities increasingly mandate radar simulator training for air traffic controllers, as rising global air traffic volumes make live radar training impractical and costly. These dual drivers, military and civil, are creating a sustained demand environment that will persist well into the 2033 forecast horizon.

Restraints - High Upfront Capital Investment and System Integration Complexities

The deployment of advanced, high-fidelity radar simulators demands significant capital expenditure spanning hardware acquisition, software licensing, facility preparation, and system integration. For defense agencies in emerging economies or those operating under constrained defense budgets, these upfront costs represent a formidable procurement barrier.

Cost remains a significant barrier for many organizations in defense simulation, while integration of new simulation platforms with legacy mission systems continues to pose considerable technical challenges. These challenges can delay procurement timelines by 12 to 24 months, reducing near-term revenue visibility for radar simulator suppliers and limiting market penetration in price-sensitive segments.

Cybersecurity Risks and Export Control Restrictions on Sensitive Simulation Technologies

Radar simulators, particularly those replicating advanced military radar waveforms, electronic warfare environments, and classified threat libraries, are subject to stringent export control regulations, including the U.S. International Traffic in Arms Regulations (ITAR) and the Export Administration Regulations (EAR). These frameworks limit the geographic markets accessible to U.S.-based suppliers and complicate international joint development programs.

Furthermore, the increasing digitization of simulation platforms raises cybersecurity concerns, as networked simulation environments can become vectors for adversarial infiltration and intellectual property theft. Compliance costs associated with export licensing, cybersecurity hardening, and classified data management add operational overhead that can materially impact supplier profitability and limit competitive market participation.

Opportunities - Expansion of AI-Integrated and Cloud-Based Radar Simulation Platforms

The integration of artificial intelligence (AI) and machine learning into radar simulation platforms represents a transformative opportunity for market participants. AI-powered simulators can generate dynamic, adaptive threat environments that evolve in real-time, providing more realistic and operationally relevant training scenarios than conventional scripted simulations.

In March 2024, Thales launched cortAIx, an AI accelerator combining radar, sensor, and systems expertise deployed across over 100 products for critical defense applications. Concurrently, DARPA awarded Lockheed Martin a US$ 4.6 million contract in July 2024 to develop AI tools for dynamic airborne mission simulation. Cloud-based delivery models are further democratizing access to advanced simulation capabilities, enabling smaller defense forces and research institutions to deploy scalable, subscription-based radar simulation environments without the prohibitive capital costs of on-premises hardware, presenting a compelling growth avenue for agile platform vendors.

Rapid Defense Modernization in the Asia Pacific: Creating Greenfield Deployment Opportunities

Asia Pacific's accelerating defense modernization programs represent the most significant geographic growth opportunity for radar simulator suppliers over the 2026 - 2033 forecast period. SIPRI data confirms that Japan's military spending surged 21% to US$ 55.3 billion in 2024, the largest annual increase since 1952, while China's defense budget grew 7% to an estimated US$ 314 billion, sustaining three decades of consecutive growth. India's defense expenditure reached US$ 86.1 billion in 2024, with the country actively modernizing its armed forces through programs including the indigenously developed Tejas fighter jet, requiring advanced radar test validation.

Australia committed to a record US$ 37 billion defense budget in 2024, exceeding 2% of GDP. These sustained regional defense investments, combined with the near-absence of mature domestic radar simulation supply chains across many Asia Pacific nations, create substantial greenfield procurement opportunities for both established and emerging radar simulator vendors.

Category-wise Analysis

Component Insights

The hardware component segment, encompassing signal generators, display systems, radar transceivers, signal processors, and high-performance computing platforms, holds the leading share in the radar simulator market, accounting for approximately 57% of total market revenue in 2025. Hardware dominance is underpinned by the critical role of physical signal generation and processing infrastructure in creating authentic, high-fidelity radar environments that accurately replicate real-world electromagnetic conditions.

Defense agencies including the U.S. Department of Defense and NASA, maintain a strong institutional preference for hardware-based simulators in applications including air surveillance validation, missile defense system testing, and advanced navigation research, where software-only environments cannot achieve the required signal fidelity. The Software segment is the fastest growing component over 2026 - 2033, driven by AI integration, digital twin platforms, cloud-based simulation delivery, and the high total cost of ownership advantages over hardware-intensive configurations.

Platform Insights

The Airborne platform segment commands the leading share in the radar simulator market, contributing approximately 38% of total market revenue in 2025. Airborne radar systems, spanning fighter aircraft, airborne early warning and control (AEW&C) platforms, unmanned aerial vehicles (UAVs), and maritime patrol aircraft, represent the most complex and operationally critical radar applications, requiring correspondingly sophisticated simulation environments for system qualification and crew training.

The U.S. Air Force, UK Royal Air Force, and Indian Air Force are among the major end-users driving airborne radar simulator procurement. In October 2024, BAE Systems completed the maiden flight test of the ECRS Mk2 radar on a UK Typhoon test aircraft, a next-generation AESA system developed with Leonardo UK, underlining the sustained demand for advanced airborne radar test and simulation infrastructure. The Space-based platform segment is the fastest growing over 2026 - 2033, reflecting accelerating investment in satellite-based radar for surveillance and intelligence gathering.

Application Insights

The training & education application segment holds the dominant position in the radar simulator market, accounting for approximately 42% of total market revenue in 2025. The segment's leadership reflects the fundamental value proposition of radar simulators, providing military operators, air traffic controllers, and aviation professionals with realistic, risk-free training environments at a fraction of the cost of live exercises.

Approximately 68% of defense institutions in North America utilize radar simulators for personnel training and system testing. As air traffic volumes recover and grow globally post-pandemic, the International Air Transport Association (IATA) projects passenger numbers to surpass 5 billion by 2030, the demand for air traffic controller radar training is intensifying. The Mission Rehearsal application segment is the fastest growing over 2026 - 2033, driven by increasing military emphasis on pre-mission simulation for complex, multi-domain operational scenarios involving contested electromagnetic environments.

End-user Insights

The military & defence end-user segment dominates the radar simulator market by a commanding margin, accounting for approximately 60% of total market revenue in 2025. Defense forces globally are the primary institutional procurers of radar simulation technology, driven by mandatory training certification requirements, system lifecycle management obligations, and the increasing complexity of modern battlefield radar environments.

The U.S. DoD's sustained focus on Modeling, Simulation, and Training (MS&T) as a core competency, reflected in its FY2026 RDT&E budget request of US$ 179 billion, directly supports military radar simulator demand. Commercial Aviation is the fastest-growing end-user segment over 2026 - 2033, propelled by regulatory mandates from aviation authorities, including the Federal Aviation Administration (FAA), European Union Aviation Safety Agency (EASA), and their counterparts requiring simulation-based competency for radar operators and air traffic management personnel.

Regional Insights

North America Radar Simulator Market Trends and Insights

North America is the leading regional market for radar simulators, holding approximately 38% of global market share in 2025. The region's leadership is anchored by the world's largest defense budget, SIPRI recorded U.S. military expenditure at US$ 997 billion in 2024, representing 37% of all global military spending, and a deep ecosystem of radar technology companies, defense contractors, and research institutions. The U.S. Department of Defense's Defense Innovation Unit scaled its budget to nearly US$ 1 billion in 2024 to accelerate AI-driven defense simulation, while the FY2026 RDT&E budget request of US$ 179 billion underscores the administration's commitment to advanced system testing infrastructure. In June 2024, GE Vernova and National Grid reinforced U.S. grid and defense infrastructure investment, reflecting broader industrial capacity development.

Approximately 55% of defense modernization projects in North America incorporate simulation-based solutions, highlighting the region's institutional embrace of the simulation-based training paradigm. Civil aviation growth, with the FAA managing the world's largest airspace system, further drives commercial radar simulator demand for air traffic control training. Canada is an emerging contributor, with its defense budget increases following NATO commitments supporting the procurement of advanced training simulation systems.

Europe Radar Simulator Market Trends and Insights

Europe represents the second-largest and fastest-growing developed-market region for radar simulators, propelled by a historic wave of defense spending increases across NATO member states. SIPRI data for 2024 reveals that Germany's defense expenditure surged 28% to US$ 88.5 billion, making it the largest military spender in Western Europe for the first time since reunification. Poland's defense budget grew 31% to US$ 38.0 billion (4.2% of GDP), while the United Kingdom is projected to spend US$ 74.5 billion in 2025, with AI systems and electronic warfare prioritized. European NATO members collectively spent €343 billion on defense in 2024, with plans for an additional €100 billion annually by 2027.

In October 2024, BAE Systems conducted the maiden flight test of the ECRS Mk2 radar system on a UK Typhoon aircraft, a milestone that directly stimulates demand for compatible radar simulation and testing infrastructure. France and Spain are increasing their simulation procurement as EASA-mandated air traffic management modernization programs advance. Regulatory harmonization through EASA and EUROCONTROL frameworks is standardizing radar training requirements across the continent, creating a durable structural demand environment for radar simulator vendors targeting multiple European procurement cycles simultaneously.

Asia Pacific Radar Simulator Market Trends and Insights

Asia Pacific is the fastest-growing regional market for radar simulators over the 2026 - 2033 forecast period, driven by unprecedented defense spending increases and large-scale military modernization programs across China, Japan, India, and South Korea. SIPRI data confirms that Japan's defense spending rose 21% to US$ 55.3 billion in 2024, its largest annual increase since 1952, while China increased its military budget by 7% to an estimated US$ 314 billion, sustaining 30 consecutive years of growth according to SIPRI. India's US$ 86.1 billion defense expenditure in 2024 funds active radar procurement programs, including the RADSIM program inducted by the Indian Navy at AIRCATS in March 2024.

China accounts for 50% of all military spending in Asia and Oceania according to SIPRI, with its radar modernization program encompassing naval, airborne, and ground-based systems requiring extensive simulation support. Australia's record US$ 37 billion defense budget and the AUKUS submarine program are generating substantial demand for advanced sensor and radar simulation capabilities. The region's rapid urbanization and air traffic growth, with IATA projecting Asia Pacific as the world's largest aviation market by passenger numbers within this decade, also drives commercial radar simulator procurement for air traffic management training.

Competitive Landscape

The global radar simulator market exhibits a moderately consolidated structure, led by a group of established defense contractors alongside specialized simulation technology providers. Market concentration is supported by high entry barriers, including stringent regulatory requirements, long procurement cycles, and the need for proven technical capabilities in complex defense and aviation environments. Established players benefit from strong relationships with government agencies and a track record of executing large-scale, mission-critical contracts.

Competition is primarily driven by advancements in simulation fidelity, software integration, and system scalability. Key business strategies include forming strategic technology partnerships, investing in AI and machine learning for adaptive simulation environments, and adopting modular, open-architecture designs to enable faster upgrades. Vendors are increasingly shifting toward cloud-based platforms and subscription-driven models, including software-as-a-service offerings and integrated lifecycle support contracts. Additionally, niche players are focusing on specialized capabilities such as radar signal processing and compact, cost-effective training solutions to target institutional and commercial customers.

Key Developments:

- October 2025: Infineon Technologies AG announced advancements in its radar simulation and sensing solutions, enhancing system-level testing capabilities for automotive and industrial applications with improved accuracy, scalability, and real-time performance.

- September 2024: Rohde & Schwarz launched the Radar Essential Tester (RadEsT), a new radar target simulator supporting automotive ADAS and autonomous driving radar testing, dynamically simulating targets with adjustable distance, velocity, and attenuation parameters.

- October 2024: BAE Systems successfully conducted the maiden flight test of the ECRS Mk2 AESA radar on a UK Typhoon aircraft in Lancashire, developed jointly with Leonardo UK, showcasing next-generation airborne radar capabilities requiring advanced simulation and test infrastructure.

- March 2024: The Indian Navy inducted its first Radar Simulator (RADSIM) at the Aircraft Carrier Training School (AIRCATS) in Goa, marking a significant milestone in Asia Pacific's growing institutional adoption of simulation-based radar training solutions.

Companies Covered in Radar Simulator Market

- Acewavetech

- Adacel Technologies Limited

- ARI Simulation

- Buffalo Computer Graphics

- Cambridge Pixel Ltd.

- Keysight Technologies

- Kratos Defense & Security Solutions Inc.

- L3Harris Technologies, Inc.

- Mercury Systems, Inc.

- Micro Nav Limited

- Mistral Solutions

- MVRsimulation Inc.

- Remcom Inc.

- RTX Corporation

- SkyRadar

- Rohde & Schwarz GmbH & Co. KG

- Thales Group

- QinetiQ Group PLC

Frequently Asked Questions

The global radar simulator market is valued at US$ 3.5 billion in 2026 and is projected to reach US$ 5.3 billion by 2033 at a CAGR of 6.2%.

Key drivers include rising global defense spending, increasing complexity of radar systems, and growing demand for simulation-based training in defense and aviation.

North America leads with around 38% share, driven by high defense budgets and strong adoption of simulation technologies, while Asia Pacific is the fastest growing region.

Major opportunities include AI-integrated and cloud-based simulation platforms and expanding defense modernization programs in Asia Pacific.

Key players include L3Harris Technologies, RTX, Keysight Technologies, Kratos Defense, Mercury Systems, Thales, Rohde and Schwarz, QinetiQ, and Adacel.