- Beverages

- Lysine Market

Lysine Market Size, Share, and Growth Forecast, 2026 - 2033

Lysine Market by Product Type (L-Lysine Hydrochloride, L-Lysine Sulfate, Others), Form (Powder, Dry Form, Others), Grade, Application, and Regional Analysis for 2026 - 2033

Lysine Market Size and Trends Analysis

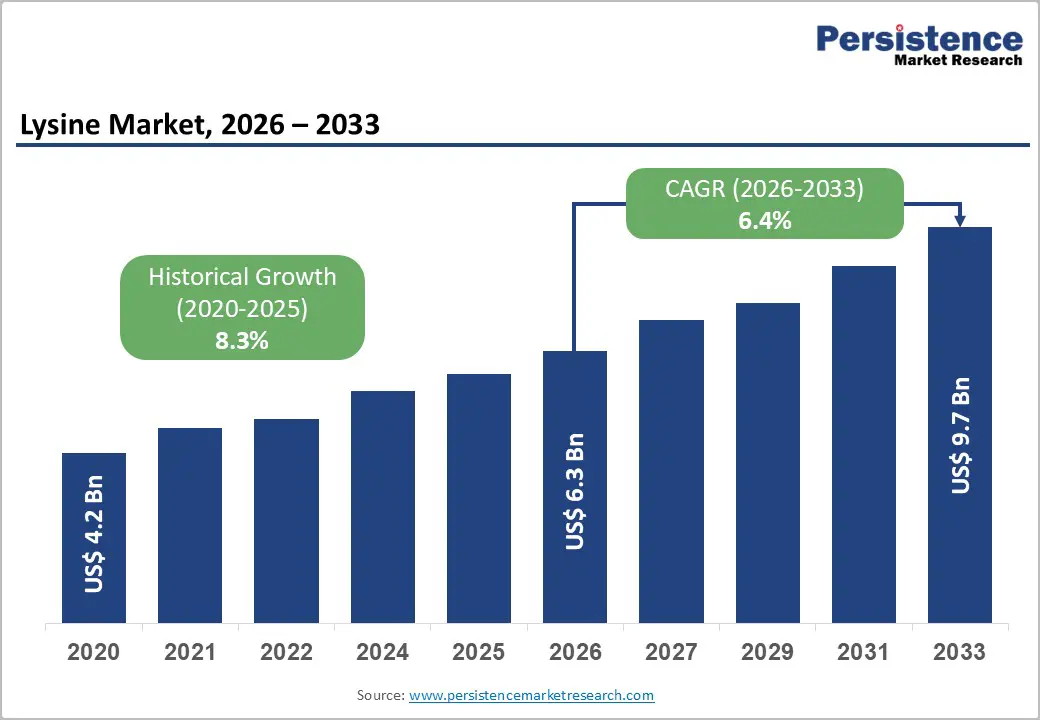

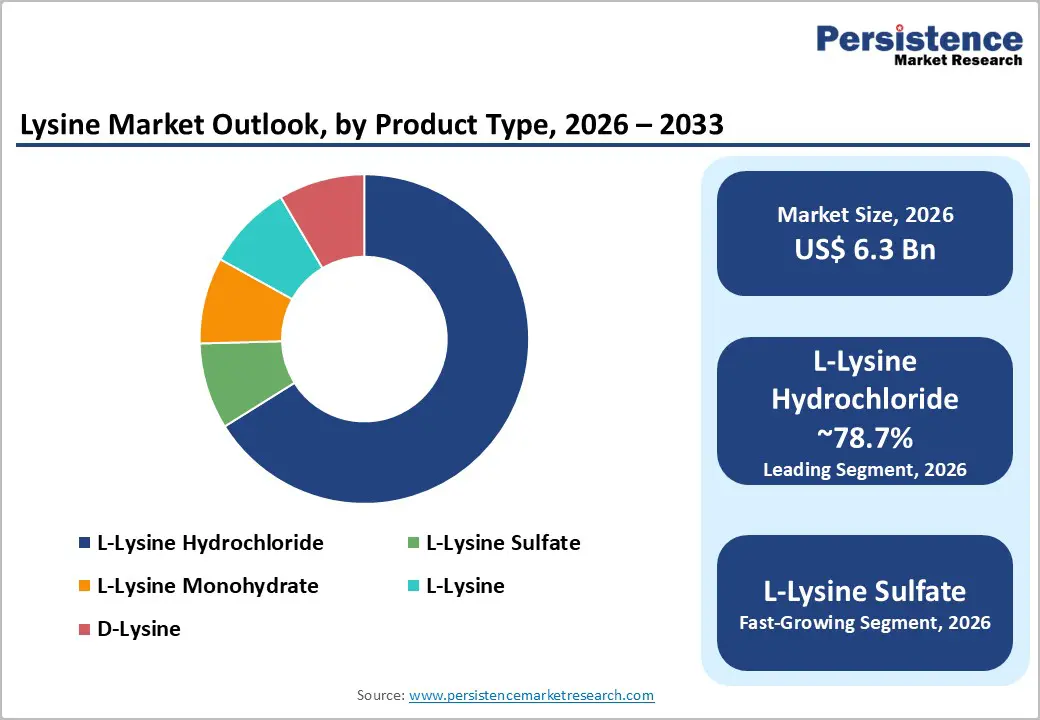

The global lysine market size is likely to be valued at US$6.3 billion in 2026 and is expected to reach US$9.7 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033, driven primarily by rising demand for animal protein and high-efficiency feed formulations, particularly in poultry, swine, and aquaculture production systems.

Lysine supplementation enables feed producers to reduce crude protein levels while maintaining animal growth performance and lowering nitrogen emissions. Industrial fermentation improvements and regional manufacturing investments are strengthening supply stability. While feed-grade lysine remains the dominant demand driver, food, nutraceutical, and pharmaceutical applications are expanding into higher-value market segments, contributing to steady global revenue growth.

Key Industry Highlights:

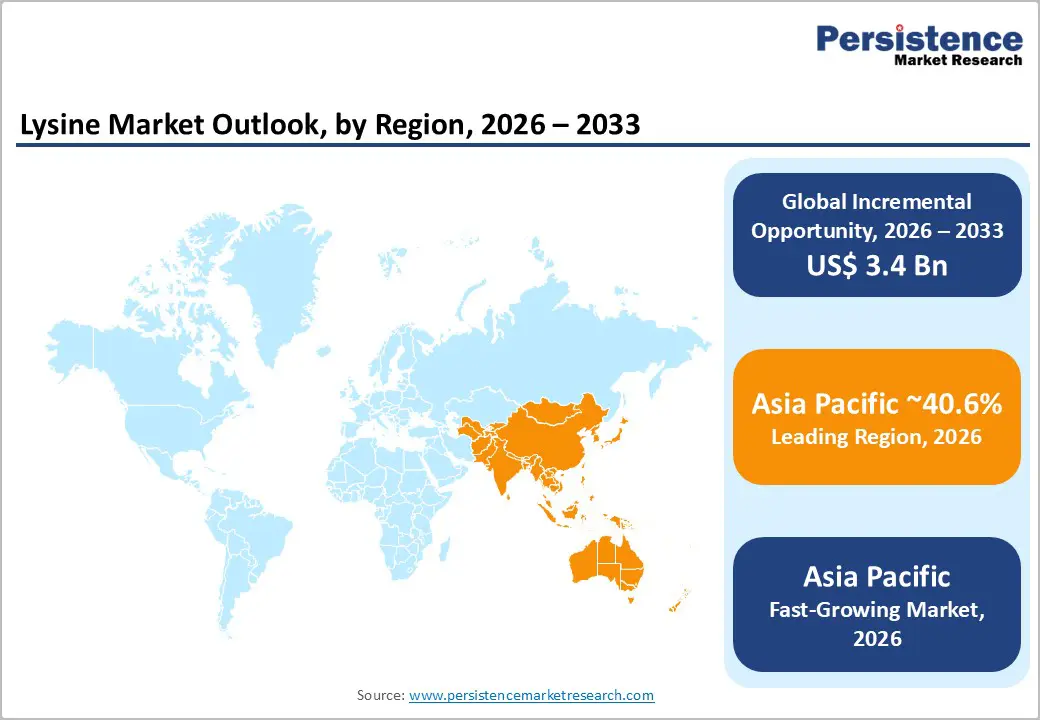

- Leading Region: Asia Pacific is projected to dominate the market, accounting for approximately 40.6% of market share, supported by large-scale amino acid manufacturing capacity in China and strong livestock production growth across China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also the fastest-growing regional market, driven by expanding poultry and aquaculture industries, rising meat consumption, and increasing investment in fermentation-based amino acid production facilities.

- Investment Plans: Major lysine producers such as Meihua Holdings Group, CJ CheilJedang, and COFCO Biochemical are expanding fermentation capacity and strengthening export capabilities, particularly in Asia Pacific, to meet rising demand from global animal feed industries.

- Dominant Product Type: L-Lysine Hydrochloride is anticipated to lead the market with approximately 78.7% share, due to its high lysine concentration, production scalability, and widespread use in poultry and swine feed formulations.

- Leading Product Form: Powdered lysine is estimated to hold about 66.4% of the market share, primarily because it integrates easily into conventional feed manufacturing systems and enables uniform nutrient distribution in large-scale feed production.

| Key Insights | Details |

|---|---|

| Lysine Market Size (2026E) | US$6.3 Bn |

| Market Value Forecast (2033F) | US$9.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis -Rising Global Demand for Animal Protein and Feed Efficiency

Global consumption of poultry, pork, and aquaculture products has increased significantly as population growth and income expansion shift dietary patterns toward higher protein intake. Livestock producers rely on amino acid supplementation to improve feed efficiency and reduce production costs. Lysine plays a critical role in optimizing animal growth and feed conversion ratios in monogastric animals such as pigs and poultry. The use of crystalline amino acids allows feed formulators to lower crude protein levels while maintaining nutritional balance, reducing nitrogen waste and environmental emissions. International agricultural organizations report steady increases in meat production worldwide, which directly increases demand for feed additives, including lysine. As commercial livestock production intensifies, the use of precision nutrition strategies continues to strengthen long-term demand for lysine-based feed supplements.

Advancements in Industrial Fermentation Technologies

Lysine production relies on microbial fermentation processes using carbohydrate feedstocks such as corn, wheat, and cassava. Advances in biotechnology and fermentation strain development have improved yield efficiency and reduced production costs. Modern fermentation facilities utilize engineered microorganisms capable of higher lysine productivity, improving output per unit of raw material. Process optimization, energy recovery systems, and continuous fermentation techniques also reduce operational expenses and improve environmental performance. These technological improvements have enabled producers to expand capacity while maintaining competitive pricing. Large-scale fermentation plants in Asia Pacific have particularly benefited from these innovations, allowing manufacturers to supply global markets at lower production costs while meeting increasing demand from the feed and food industries.

Environmental Regulations Supporting Low-Protein Feed Formulations

Governments and regulatory agencies increasingly emphasize reducing agricultural nitrogen emissions and improving environmental sustainability in livestock production. Excess protein in animal diets leads to higher nitrogen excretion, which contributes to environmental pollution in soil and water systems. Lysine supplementation allows feed manufacturers to lower crude protein levels in feed while maintaining nutritional balance. Regulatory guidelines and nutrient management frameworks encourage the adoption of amino acid-balanced diets as part of sustainable livestock production strategies. As sustainability initiatives expand globally, livestock producers are increasingly incorporating lysine and other amino acids into feed formulations to meet environmental compliance requirements and improve resource efficiency.

Barrier Analysis- Volatility in Feedstock and Energy Prices

Lysine production depends heavily on agricultural feedstocks such as corn, wheat, and cassava. Fluctuations in global commodity prices can significantly impact manufacturing costs. Feedstock expenses represent a substantial portion of lysine production costs, making manufacturers vulnerable to agricultural supply disruptions and energy price increases. When feedstock prices rise sharply, producers may experience margin pressure or increase product prices, which can affect purchasing decisions among feed manufacturers and livestock producers.

Regulatory and Compliance Requirements for High-Purity Grades

While feed-grade lysine dominates the market, expansion into food-grade and pharmaceutical-grade segments requires strict regulatory compliance. Manufacturers must meet food safety standards, pharmaceutical manufacturing requirements, and traceability protocols. Certification processes, quality control systems, and regulatory approvals increase operational costs and may extend product development timelines. These compliance requirements can limit the speed at which manufacturers transition production capacity toward higher-value applications.

Opportunity Analysis - Expansion of Nutraceutical and Functional Food Applications

Consumer interest in health and nutrition is expanding the demand for amino acid supplements and fortified foods. Lysine is widely used in dietary supplements for supporting immune health, collagen production, and metabolic function. Food manufacturers are increasingly incorporating essential amino acids into functional foods, sports nutrition products, and protein-fortified beverages. This trend is particularly strong in developed markets where consumer awareness of nutrition and wellness products continues to grow. As supplement manufacturers expand their product portfolios, demand for food-grade lysine is expected to increase significantly.

Regional Manufacturing Expansion in Emerging Markets

Emerging markets in Asia, Latin America, and parts of Africa are experiencing rapid growth in livestock production and aquaculture industries. These regions require stable supplies of amino acids to support expanding feed industries. Establishing local production facilities or regional distribution networks helps reduce transportation costs and improve supply chain resilience. Regional manufacturing investments also enable producers to respond quickly to local demand fluctuations while reducing reliance on imports.

Sustainable Fermentation and Circular Bioeconomy Initiatives

The global transition toward sustainable industrial processes presents opportunities for lysine manufacturers to adopt environmentally responsible production methods. Companies are exploring alternative feedstocks derived from agricultural residues, industrial by-products, and renewable biomass. Improved fermentation technologies can reduce greenhouse gas emissions and energy consumption during production. Sustainable lysine manufacturing practices can enhance brand reputation and attract partnerships with livestock producers seeking to reduce the environmental impact of their supply chains.

Category-wise Analysis

Product Type Insight

L-Lysine Hydrochloride is anticipated to account for approximately 78.7% of the market share in 2026, making it the dominant product type across the amino acid industry. This form contains a high concentration of lysine and offers excellent stability during feed processing and storage. Feed manufacturers prefer L-Lysine Hydrochloride because it provides a cost-efficient way to increase lysine content in animal feed formulations. Its consistent quality, ease of blending with other feed ingredients, and compatibility with existing feed production systems support widespread adoption across poultry and swine industries. Large-scale fermentation facilities are optimized for producing this form of lysine, allowing manufacturers to achieve economies of scale and maintain competitive pricing. For example, global amino acid producers such as ADM, Evonik, and CJ CheilJedang operate high-capacity fermentation plants designed primarily for L-Lysine Hydrochloride production. These facilities supply integrated feed manufacturers and premix producers worldwide. The widespread use of this product in swine diets in the U.S. and poultry feed formulations across China and Brazil further reinforces its leadership position within the lysine product landscape.

L-Lysine Sulfate is anticipated to emerge as the fastest-growing product segment within the market, driven by its suitability for cost-sensitive feed formulations and integrated nutrient benefits. This form contains lysine along with sulfate, which can contribute additional sulfur to feed formulations. L-Lysine Sulfate is commonly used in poultry and aquaculture feeds where nutrient balance and cost efficiency are important considerations. Compared with highly refined hydrochloride forms, sulfate variants often require less purification during production, which can lower manufacturing costs. Its increasing adoption in emerging markets is driven by demand for affordable amino acid supplements and the expansion of regional feed industries. For instance, several Asian feed producers are incorporating lysine sulfate into broiler feed formulations to reduce overall feed costs while maintaining protein efficiency. Manufacturers such as Meihua Holdings Group and COFCO Biochemical have expanded production capacity for lysine sulfate to serve the rapidly growing livestock sectors in China, Southeast Asia, and Latin America.

Form Insights

Powdered lysine is anticipated to hold approximately 66.4% of the market share in 2026, making it the most widely used form across feed manufacturing operations. The dominance of powdered lysine is largely attributed to its compatibility with conventional feed manufacturing systems. Feed mills can easily incorporate powdered lysine into premixes and compound feeds, ensuring uniform nutrient distribution across large production batches. This format integrates smoothly into automated mixing and dosing equipment used by large feed manufacturers. Powder forms also offer convenient storage, transportation, and handling advantages. The product maintains stable chemical properties under typical storage conditions, allowing manufacturers and distributors to preserve product quality across long supply chains. For example, multinational feed producers such as Cargill and Nutreco incorporate powdered lysine into commercial feed premixes supplied to poultry and swine farms across North America and Europe. Its ease of handling and compatibility with industrial feed systems continue to sustain its strong market presence.

The dry lysine product segment is likely to be the fastest-growing, reflecting growing demand for formulations that offer superior storage stability and longer shelf life. The dry category includes highly dehydrated powders and granulated lysine products designed to minimize moisture content. These formulations provide extended shelf life and reduce the risk of microbial contamination during storage and transportation. In regions characterized by high humidity or long shipping distances, dry lysine formulations offer clear logistical advantages for distributors and feed producers. For instance, feed manufacturers in Southeast Asia and Latin America increasingly prefer dry lysine products because they maintain quality during maritime transport and extended warehousing periods. Major amino acid suppliers have responded by introducing advanced drying technologies and improved packaging systems to ensure product stability across global supply chains.

Regional Insights

North America Lysine Market Trends - Precision Feed Nutrition and Large-Scale Livestock Production Supporting Stable Demand

North America represents a mature and technologically advanced market, supported by a large livestock production industry and a well-established feed manufacturing sector. The U.S. leads regional demand due to its extensive poultry, pork, and cattle production systems. According to data from the U.S. Department of Agriculture (USDA), the U.S. produces more than 9 billion broiler chickens annually and remains one of the world’s largest pork producers, creating consistent demand for amino acid supplementation in feed. Livestock producers in the country rely heavily on precision nutrition strategies that incorporate lysine to optimize feed efficiency and animal performance while controlling feed costs. Regulatory oversight plays a significant role in shaping the market. Feed additives must comply with safety and labeling standards set by the U.S. Food and Drug Administration (FDA) and the Association of American Feed Control Officials (AAFCO) before entering commercial feed supply chains. These regulatory requirements encourage manufacturers to maintain consistent product quality and transparent supply chains. Feed producers also prioritize traceability and ingredient documentation to meet the expectations of food retailers and consumers demanding responsibly produced animal products.

Precision feeding practices have become widely adopted among large livestock operations, enabling producers to improve feed efficiency and reduce nitrogen emissions. Technological advancements in feed formulation software and nutrient management systems further enhance the use of amino acid supplementation. Companies such as Cargill Animal Nutrition and Land O’Lakes’ Purina Animal Nutrition integrate lysine into precision feed formulations designed for poultry and swine operations. These companies also invest in digital feed formulation platforms that allow farmers to adjust amino acid levels based on livestock growth stages and environmental conditions. Investment activity in the region focuses on improving feed formulation technologies, enhancing supply chain traceability, and strengthening partnerships between amino acid producers and livestock integrators. For instance, Archer Daniels Midland (ADM) continues to expand its global nutrition and amino acid portfolio, supplying lysine ingredients to North American feed manufacturers through its animal nutrition division. Strategic partnerships between amino acid suppliers and large integrators such as Tyson Foods and Smithfield Foods support the development of customized feed programs designed to improve productivity and reduce environmental impacts. As environmental regulations evolve and feed costs remain a major factor in livestock profitability, the role of lysine in reducing crude protein levels in feed formulations remains a critical component of animal nutrition strategies across the region.

Europe Lysine Market Trends - Sustainability-Driven Feed Formulation and Strict EU Regulatory Oversight

Europe represents a high-value market for lysine, characterized by strict regulatory frameworks and a strong emphasis on sustainability within agricultural production systems. Countries such as Germany, the U.K., France, and Spain play key roles in regional demand due to their large livestock industries and advanced feed manufacturing sectors. According to the European Feed Manufacturers’ Federation (FEFAC), Europe produces over 150 million metric tons of compound feed annually, supporting consistent demand for amino acids such as lysine used in poultry, pig, and dairy production systems. European livestock producers prioritize efficient nutrient management and environmental sustainability. Policies designed to reduce nitrogen emissions and agricultural pollution encourage the adoption of amino acid-balanced diets.

Lysine supplementation allows feed producers to reduce the overall protein content in feed while maintaining optimal animal growth performance. This approach aligns with environmental strategies promoted under the European Union Farm to Fork Strategy, which aims to reduce the environmental footprint of food production across the region. Germany plays a leading role in innovation related to feed additives and amino acid technologies. The country hosts major chemical and biotechnology companies involved in amino acid production and research. For example, Evonik Industries, headquartered in Germany, is one of the world’s largest producers of feed amino acids and continuously invests in biotechnology research and fermentation technologies.

The regulatory environment across the European Union promotes consistent standards for feed additives and food safety. Manufacturers must comply with approval procedures overseen by the European Food Safety Authority (EFSA) before selling lysine products within the region. Although these regulations create entry barriers, they also enhance consumer confidence and ensure high product quality. The harmonized regulatory system allows feed additive companies to distribute approved products across multiple European markets. As consumer awareness of sustainable food production increases, European livestock producers continue adopting lysine supplementation as part of broader environmental management strategies.

Asia Pacific Lysine Market Trends - Fermentation Manufacturing Expansion and Rapid Growth in Livestock Feed Demand

Asia Pacific is the largest and fastest-growing regional market, accounting for approximately 40.6% of the market share in 2026. The region benefits from strong livestock production growth, expanding aquaculture industries, and large-scale fermentation manufacturing capacity. Rapid urbanization and rising income levels across many Asian economies have increased consumption of meat, eggs, and seafood, which in turn drives demand for animal feed additives such as lysine. China plays a central role in the regional market as both the largest producer and one of the largest consumers. The country hosts numerous fermentation facilities operated by major amino acid producers, including CJ CheilJedang, Meihua Holdings Group, and COFCO Biochemical. These companies operate large-scale production plants capable of supplying lysine to domestic feed producers as well as international export markets. China’s competitive advantage stems from access to agricultural feedstocks such as corn and established fermentation expertise developed over decades of industrial biotechnology investment.

Recent developments in China illustrate the scale of regional production capacity. Companies such as Meihua Holdings Group have expanded fermentation facilities to increase amino acid output, supporting both domestic livestock industries and export demand. These investments strengthen Asia Pacific’s position as a global manufacturing hub for feed amino acids, including lysine and other essential nutrients used in animal nutrition. India is emerging as a high-growth market for lysine due to rapid expansion in the poultry farming and aquaculture industries. According to data from the Food and Agriculture Organization (FAO) and India’s Department of Animal Husbandry, poultry production has grown steadily in recent years, creating strong demand for balanced feed formulations. Feed manufacturers such as Godrej Agrovet and Suguna Foods integrate amino acid supplementation into commercial poultry feed programs to improve feed conversion efficiency and production output.

Japan represents a technologically advanced market with a strong demand for high-quality amino acids. The country has a long history of innovation in fermentation technology and biotechnology. Companies such as Ajinomoto Co., Inc., a global leader in amino acid production, continue to develop advanced fermentation processes and specialized amino acid products used in feed, food, and pharmaceutical industries. Japanese feed producers emphasize precision nutrition and high-quality feed additives, supporting demand for specialized lysine products tailored to livestock performance optimization. The Asia Pacific region continues to attract substantial investment in fermentation plants and feed additive manufacturing. Large producers are expanding production capacity to meet growing domestic demand while strengthening export capabilities.

Competitive Landscape

The global lysine market is moderately consolidated, with several large global manufacturers controlling significant production capacity. Major companies operate integrated fermentation facilities and maintain global distribution networks that supply feed, food, and the pharmaceutical industries. These firms compete primarily on production efficiency, product quality, and long-term supply agreements with feed manufacturers. Regional producers and smaller biotechnology firms contribute to market diversity but typically focus on niche applications or regional supply.

Leading lysine manufacturers focus on cost-efficient fermentation technology, production capacity expansion, and strategic partnerships with feed manufacturers. Companies also emphasize sustainability initiatives, supply chain traceability, and product diversification into food-grade and pharmaceutical applications to strengthen long-term market competitiveness.

Key Industry Developments

- In February 2026, CJ CheilJedang signed a lysine technology licensing agreement with Chinese biotechnology company Xinghuipin (StarLakeEppen), granting exclusive rights to use its proprietary lysine strains in China.

Companies Covered in Lysine Market

- CJ CheilJedang

- Ajinomoto Co., Inc.

- Archer Daniels Midland Company

- Evonik Industries

- Meihua Holdings Group

- Global Bio-Chem Technology Group

- COFCO Biochemical

- East Hope Group

- Juneng Golden Corn

- Chengfu Group

- Cargill

- Kyowa Hakko Bio Co., Ltd.

- Adisseo

- Novus International

- Ningxia Eppen Biotech

- Shijiazhuang Chiyu Biological Technology

- Prinova Group

- Royal DSM

Frequently Asked Questions

The global lysine market is estimated to be valued at US$6.3 billion in 2026.

The lysine market is projected to reach US$9.7 billion by 2033.

Key trends in the lysine market include the growing use of precision nutrition in livestock production, increasing demand for amino acid-balanced feed formulations, expansion of industrial fermentation capacity in Asia Pacific, and rising adoption of food-grade lysine in dietary supplements and fortified foods.

L-Lysine Hydrochloride is the leading product type segment, accounting for around 78.7% of global market share, due to its high lysine concentration, cost efficiency, and widespread use in poultry and swine feed formulations.

The lysine market is projected to grow at a CAGR of 6.4% between 2026 and 2033.

Some of the major companies with strong product portfolios in the lysine market include CJ CheilJedang, Evonik Industries, Ajinomoto Co., Inc., Fufeng Group, and Meihua Holdings Group.