- Rail

- Locomotive Market

Locomotive Market Size, Share, and Growth Forecast, 2026 - 2033

Locomotive Market by Propulsion (Diesel-Electric, Low-Emission Diesel, Electric, Battery-Electric, Hydrogen Fuel Cell, LNG/CNG), Application (Freight, Passenger, Switcher & Shunting, Industrial & Port, Maintenance-of-Way), Technology (AC Traction Systems, DC Traction Systems, IGBT-based Power Electronics, SiC Power Modules, Permanent Magnet Traction Motors, Regenerative Braking Systems, Others), and Regional Analysis for 2026 - 2033

Locomotive Market Share and Trends Analysis

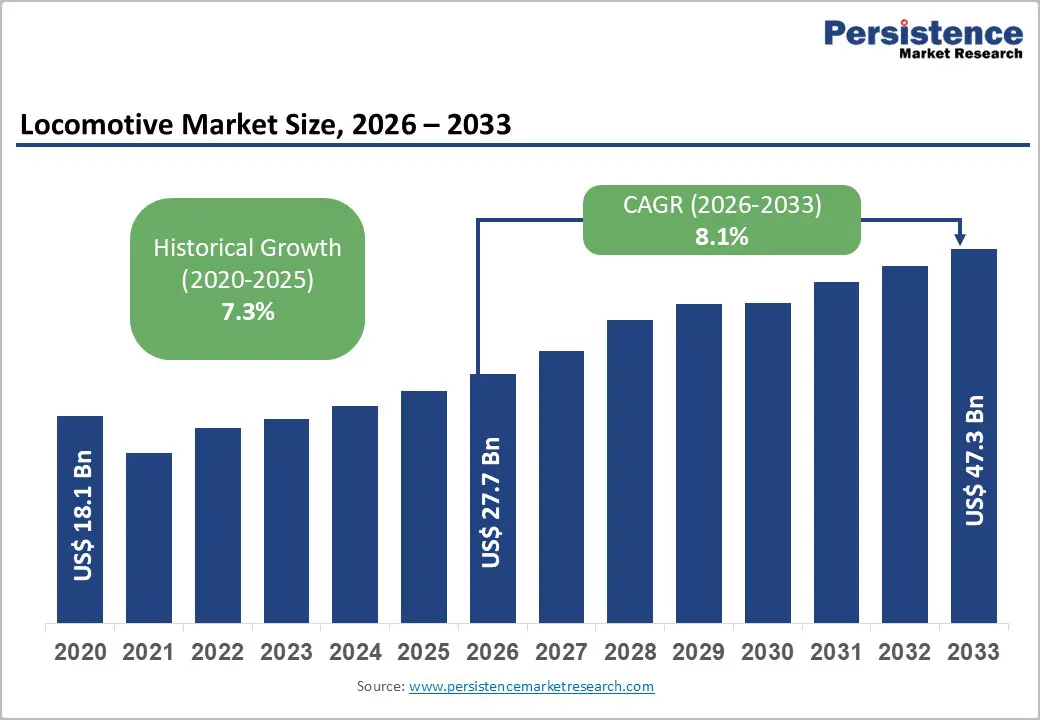

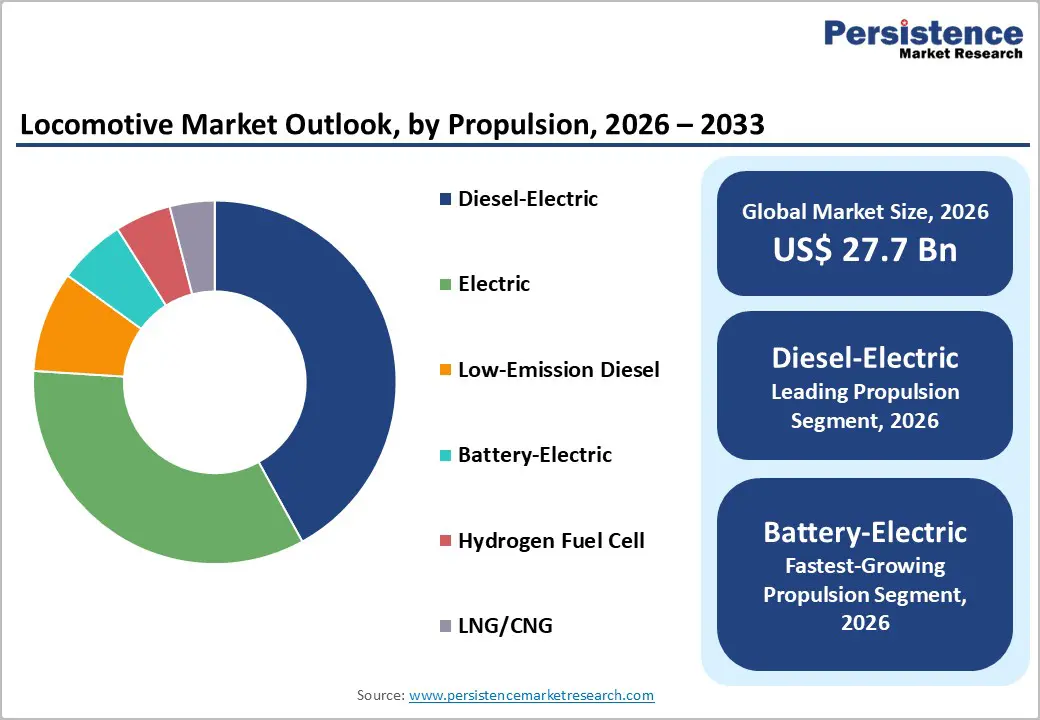

The global locomotive market size is likely to be valued at US$ 27.7 billion in 2026, and is estimated to reach US$ 47.3 billion by 2033, growing at a CAGR of 8.1% during the forecast period 2026 - 2033. The market is expanding due to sustained investment in rail infrastructure, digitalization of fleet operations, and regulatory mandates for decarbonization across transport sectors.

Rail operators in both freight and passenger segments are transitioning from legacy diesel platforms to electric and hybrid propulsion technologies, supported by government funding and international climate goals. The market's growth is also anchored in macro trends, such as urbanization-driven passenger demand and trade-linked freight volumes, which necessitate higher throughput at lower unit costs. Geographic distribution remains concentrated in the Asia Pacific, where infrastructure expansion and freight growth are most pronounced, while developed markets in North America and Europe are leveraging modernization programs to replace aging fleets. Leading market actors are increasingly investing in smart and low-emission locomotive technologies, creating new competitive dynamics and aftermarket service opportunities. The trajectory reflects a structural transformation of the locomotive industry, where environmental compliance, technology integration, and network expansion are key drivers shaping capital allocation and long-term procurement strategies across public and private rail operators.

Key Industry Highlights

- Leading Propulsion Type: Diesel-electric locomotives are expected to dominate with around 44% revenue share in 2026, reflecting the continued reliance on diesel-electric fleets in non-electrified routes.

- Top Application: Freight locomotives are projected to contribute approximately 60% of total market revenue in 2026, supported by rising bulk commodity transport and intermodal freight growth.

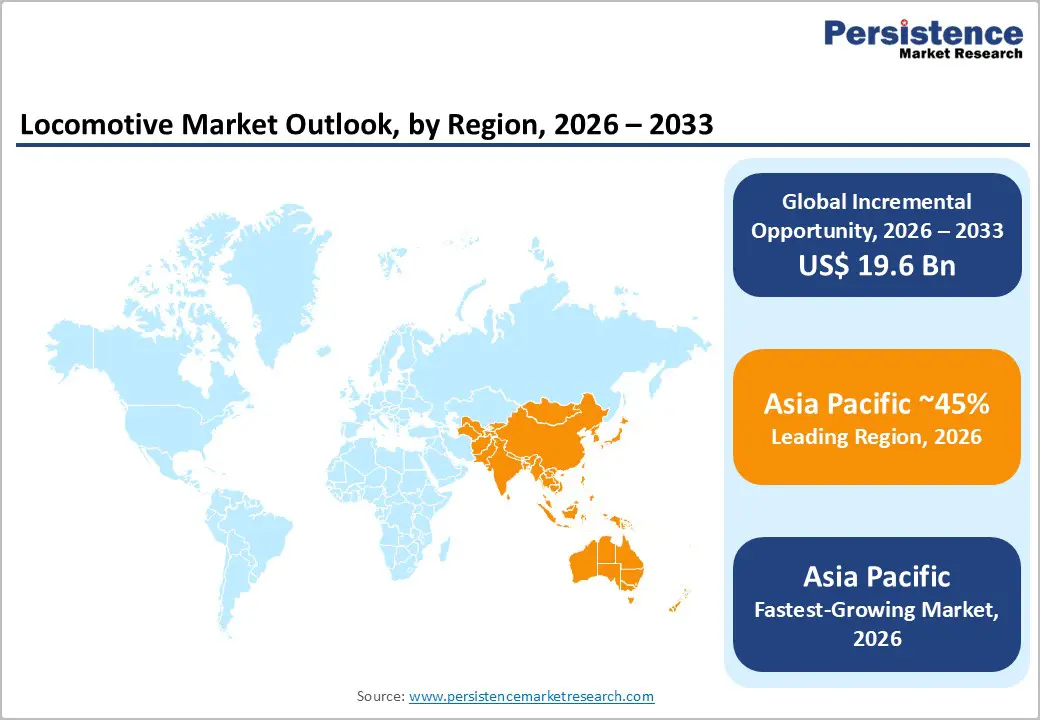

- Dominant Region: Asia Pacific is expected to account for approximately 45% market share in 2026, owing to large-scale rail infrastructure expansion.

- Fastest-Growing Market: Asia Pacific is projected to register an estimated 9% CAGR during 2026 - 2033, driven by rapid network electrification and passenger rail expansion.

- Competitive Trends: A concentrated group of global rolling stock manufacturers is influencing market growth by leveraging long-term government contracts and technology-led differentiation in low-emission propulsion systems.

- May 2025: CRRC Ziyang rolled out the CKD6H new energy locomotive for export to Kazakhstan, designed as a diesel-battery model and optimized for extreme cold.

| Key Insights | Details |

|---|---|

| Locomotive Market Size (2026E) | US$ 27.7 Bn |

| Market Value Forecast (2033F) | US$ 47.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Electrification and Decarbonization Mandates

Global regulatory frameworks, including the Fit for 55 climate package and guidelines from the International Energy Agency (IEA), are currently rerouting capital toward sustainable rail technologies. Multilateral financing institutions are prioritizing infrastructure bonds and development bank loans for projects that demonstrate high carbon abatement performance. As a result of these shifts, national governments and rail operators are aligning fleet replacement cycles with aggressive emission-reduction targets. This transition is actively fostering the adoption of hybrid drives and electric propulsion systems to replace aging diesel units. By the time these initiatives conclude, stakeholders will have achieved substantial reductions in greenhouse gas (GHG) emissions and lifetime operating costs through advanced rolling stock.

The global market is presently observing a significant surge in the procurement of dual-mode locomotives and advanced traction systems. Rail operators are integrating comprehensive electrification strategies into long-term asset management plans (AMP) to secure federal or regional funding. This strategic alignment is currently creating multi-year procurement pipelines that favor power electronics and supporting infrastructure. By the end of the current fiscal decade, industry leaders will have solidified the dominance of low-carbon platforms within global order books. This transformation is ensuring that future transportation networks operate with much higher energy efficiency and stricter environmental compliance.

High Capital Intensity and Infrastructure Gaps

Significant structural restraints are currently hindering the locomotive market growth due to high capital intensity and existing infrastructure gaps. Advanced platforms, such as hydrogen-ready or hybrid units, require a much higher upfront investment than traditional diesel models. Rail operators are presently managing the combined burden of high acquisition prices and the essential development of supporting infrastructure. These necessary additions include overhead catenary systems, specialized maintenance depots, and sophisticated refueling facilities. By the time these projects are completed, operators will have invested over €13 million per unit in cutting-edge hydrogen systems and site development. Consequently, the high total cost of ownership (TCO) is preventing many budget-constrained organizations from transitioning to cleaner technologies.

The uneven penetration of electrification infrastructure is currently forcing many regions to rely on high-emission alternatives for their transport needs. While some areas report electrification rates above 50%, many developing markets still lag below 20%. This disparity is creating a formidable barrier for the adoption of electric-only locomotives and is slowing the modernization of rolling stock. Maintenance costs are also rising as technological complexity requires specialized skills and equipment that are not yet available in smaller markets. By the end of this investment cycle, deferred network upgrades and extended payback periods will increase financial risk for private operators. These dynamics are currently discouraging rapid fleet transitions in any region that lacks strong fiscal support or clear policy mandates.

Digital and Predictive Maintenance Platforms

The integration of digital technologies is currently transforming the locomotive sector by replacing reactive, scheduled maintenance frameworks with proactive, data-driven strategies. Industry leaders are presently deploying Internet of Things (IoT) sensors and machine learning (ML) analytics to monitor traction systems and braking performance in real time. These advanced cloud-based fleet management systems (CBFMS) are identifying early wear patterns and degradation indicators before mechanical failures occur. By the time these digital transitions mature, rail operators will have significantly maximized asset availability and minimized costly service disruptions through condition-based maintenance (CBM). This evolution is actively fostering operational efficiency across global rail networks by ensuring that critical subsystems remain functional under rigorous duty cycles.

Original equipment manufacturers (OEMs) are currently capturing a high-value market opportunity expected to reach US$ 1 billion annually through digital retrofits and aftermarket services. By 2033, these providers will have successfully shifted to a tiered revenue model, with recurring software subscriptions and automated diagnostics complementing traditional hardware sales. This strategic shift is allowing operators to contain costs by allocating technical resources only when predictive analytics indicate a genuine requirement for intervention. Furthermore, stakeholders are leveraging aggregated performance data to refine future product designs and optimize complex network scheduling algorithms. This ongoing data monetization is ensuring that digital locomotive services become a dominant share of total market revenues in developed economies.

Category-wise Analysis

Propulsion Insights

In 2026, diesel-electric locomotives are expected to account for the largest share of the propulsion market, with an estimated 44% of revenue. Diesel-electric platforms continue to dominate the installed base across major rail networks due to their proven reliability, long asset life, and broad operational compatibility with non-electrified and partially electrified routes. Freight rail operators, in particular, are heavily reliant on diesel-electric locomotives, as these systems provide high hauling capacity without requiring extensive fixed infrastructure investment. Ongoing fleet renewal programs are therefore prioritizing upgraded diesel-electric models with improved fuel efficiency and emissions performance, reinforcing the segment’s leadership position in 2026 despite the gradual expansion of alternative propulsion technologies.

Battery-electric locomotives are emerging as the fastest-growing propulsion segment during the 2026-2033 forecast period, supported by zero-emission transport mandates and sustained declines in battery system costs. Although current penetration remains limited, pilot deployments and early commercial rollouts are expanding steadily as improvements in energy density, charging efficiency, and lifecycle performance are strengthening the commercial case for battery-electric traction. Policy support across Europe, North America, and select Asia Pacific market is accelerating adoption, particularly in urban rail yards, short-haul passenger routes, and regional freight corridors where charging infrastructure can be deployed at a manageable scale. The improving economics of onboard energy storage and grid-based charging are enabling operators to integrate battery-electric locomotives without full network electrification, reducing both emissions and operating costs. As a result, capital investment and procurement strategies are increasingly prioritizing battery-electric platforms, with order pipelines and retrofit programs expanding year-over-year in response to regulatory pressure and long-term decarbonization targets.

Application Insights

The freight segment is expected to account for approximately 60% of total locomotive demand in 2026. Global trade expansion and the ongoing modal shift from road to rail are presently reinforcing the necessity for high-power traction platforms. Logistics providers are choosing rail transport to achieve superior cost efficiency and to meet demanding bulk commodity transport requirements. Heavy-haul corridors and intermodal transport networks are likely to solidify their roles as cornerstones of major purchase cycles over the next decade. This sustained reliance on robust machinery is ensuring that freight operations remain the backbone of locomotive utilization for the foreseeable future.

The passenger locomotive sector is anticipated to display the highest CAGR through 2033 as rapid urbanization accelerates across Asia, Latin America, and Africa. National rail development plans are currently allocating significant capital to electrify commuter routes and expand high-speed networks. These investments are driving the procurement of advanced passenger platforms that prioritize enhanced performance, rider comfort, and lifecycle reliability. As the 2026-2033 forecast period concludes, the passenger segment will have achieved revenue growth that surpasses the freight category in percentage terms. This dynamic transition is successfully transforming public transit systems into modern, high-efficiency corridors that meet the needs of increasingly populous regions.

Technology Insights

Insulated gate bipolar transistor (IGBT) power electronics are set to occupy a leading position in the technology category, expected to secure roughly 60% of the locomotive control systems market share in 2026. These modules provide mature, efficient, and reliable power conversion, which ensures they remain the default choice for modern traction systems. Their extensive application across electric and hybrid locomotives has successfully solidified their dominance within the global technology stack. By the time this fiscal period ends, these systems will have provided a stable foundation for the majority of new rolling stock procurement. Silicon carbide (SiC) modules and digitally integrated traction systems are currently anticipated to have the fastest growth rates through 2033. This advanced technology offers superior thermal performance and higher power density than traditional silicon alternatives, significantly improving energy efficiency. When combined with artificial intelligence (AI) driven fleet management and predictive diagnostics, these modules are supporting lower lifecycle costs and higher asset availability. By the end of the next decade, rail operators will have achieved much greater efficiency in both new procurement and retrofit markets through these smart control systems. This ongoing innovation is ensuring that future locomotive designs reach unprecedented levels of energy savings and operational reliability.

Regional Insights

North America Locomotive Market Trends

The North American locomotive market features advanced rail infrastructure and modernization programs. These efforts focus on emissions reduction and fleet renewal. Federal funding supports rail upgrades and freight capacity improvements. As a result, the region is anticipated hold a market of around 27% in 2026. A key factor that is driving this growth includes the modernization of legacy diesel fleets and the integration of positive train control (PTC) systems by rail operators in the region. They also allocate capital to expand electrification corridors. The United States and Canada lead with strong freight rail activity. This demand persists even as electrification advances more slowly than in Europe or Asia. Stakeholders are actively monitoring these trends closely to identify investment opportunities in sustainable rail technologies.

Regulatory frameworks shape procurement strategies in this market. The United States Environmental Protection Agency (EPA) sets emissions standards, while state incentives promote low-carbon technologies. Operators use grants and tax credits to cover costs of advanced propulsion systems. Domestic manufacturers and OEM partnerships are further boosting competition by localizing production and maintenance to enhance cost efficiency and supply chain strength. The electrified and hybrid locomotive segment is set to grow the fastest in the region from 2026 to 2033, reflecting broader decarbonization goals. Rail operators are also investing heavily in digital fleet management and predictive maintenance platforms with a view to reduce the total cost of ownership and enhance asset utilization.

Europe Locomotive Market Trends

Europe is currently maintaining a significant presence in the locomotive market and is expected to secure a share between 20% and 23% in 2026. Stringent climate policies and the dominance of electrified rail are presently directing substantial investments toward the procurement of advanced electric and hybrid models. Initiatives such as the Trans-European Transport Network (TEN-T) and various national high-speed rail expansions are actively anchoring demand for locomotives that are capable of seamless cross-border operations. By the time these infrastructure projects reach their 2030 milestones, regional operators will have successfully integrated next-generation rolling stock into a more cohesive and high-performance network.

The regulatory environment, currently centered on the Fit for 55 package, is pushing operators to transition to zero-emission fleets. This shift is actively stimulating the development of emerging hydrogen solutions and low-emission propulsion technologies. Major manufacturers, such as Siemens and Alstom, are presently leveraging robust research & development (R&D) ecosystems to accelerate the commercialization of digital services. These offerings include real-time condition monitoring and automated control systems that comply with European Union (EU) safety standards. Over the next decade, these digital integrations are likely to dictate the flow of market revenues, ensuring that future rail networks operate with unprecedented efficiency and environmental compliance.

Asia Pacific Locomotive Market Trends

Asia Pacific is projected to account for approximately 45% of the locomotive market share in 2026. This leadership position is being driven by sustained rail network expansion and freight rail modernization across high-growth economies such as China, India, and Southeast Asian countries. Rapid urbanization is increasing passenger mobility requirements, while industrial growth is expanding the need for efficient bulk and intermodal freight transport. Government-backed infrastructure programs are actively supporting this demand, such as China’s continued investment in high-speed rail corridors and India’s nationwide locomotive fleet renewal and electrification initiatives. These programs are channeling long-term capital into rolling stock procurement and are strengthening order visibility for manufacturers and system suppliers across the region.

Policy focus on rail electrification and transport emission reduction is accelerating the adoption of electric traction systems along high-density routes, while hybrid and battery-electric locomotive platforms are increasingly entering service in selected use cases. Competition is intensifying as domestic manufacturers are scaling production through state railway support and international technology partnerships, which are improving cost efficiency and local supply resilience. Rail operators are prioritizing operational outcomes such as higher freight throughput, improved network utilization, and predictive maintenance through digital fleet management systems. Hybrid and battery-electric locomotive applications are expected to expand at the fastest pace in the region as electrification infrastructure continues to extend into secondary and regional networks. These structural shifts are positioning Asia Pacific as a volume-driven market that is simultaneously advancing toward next-generation locomotive technologies.

Competitive Landscape

The global locomotive market landscape features a combination of large multinational OEMs, established regional producers, and emerging technology-focused suppliers. Market concentration varies by propulsion type and geography, with diesel and electric locomotive segments remaining moderately consolidated among a limited number of established manufacturers. In contrast, newer propulsion segments such as hydrogen fuel cell and battery-electric locomotives are more fragmented, as technology partnerships, pilot deployments, and specialized entrants are actively shaping early-stage competition. This structure is allowing innovation-led firms to gain initial market access, while incumbents are leveraging scale and manufacturing depth to defend core segments.

Leading manufacturers are securing a substantial share of global revenues through long-term supply agreements with national and state-owned rail operators, supported by integrated service portfolios that are increasingly including maintenance, repair, and digital monitoring solutions. Competitive positioning is shifting toward technology differentiation, as companies are investing in low-emission propulsion platforms, software-driven fleet management systems, and modular locomotive architectures that are enabling cost-effective upgrades over the asset life cycle. High capital requirements, complex certification processes, and stringent safety and emissions regulations are continuing to limit new large-scale entrants. These barriers are reinforcing the competitive advantage of players with diversified product portfolios, global service networks, and the financial capacity to support multi-year development and deployment programs.

Key Industry Developments

- In December 2025, Banaras Locomotive Works (BLW), a unit of Indian Railways, dispatched the sixth indigenously manufactured 3300 HP AC-AC diesel-electric locomotive to Mozambique. This shipment forms part of a 10-unit export contract secured by RITES Limited, with the first loco sent in June 2025. The cape gauge locomotive achieves a top speed of 100 kmph and supports Mozambique's freight operations.

- In June 2025, Siemens Mobility introduced the Charger B+AC, a next-generation battery-electric locomotive designed for the North America passenger rail market. It is built on Siemens’ established Charger platform and can operate under overhead catenary power and switch seamlessly to battery mode where overhead wires are unavailable, enabling emission-free operation across partially electrified networks.

- In June 2025, Sitav unveiled a prototype hydrogen locomotive at the Hydrogen Expo 2025 in Piacenza, marking progress in zero-emission rail traction. The modular locomotive has cleared early certification stages and integrates remote diagnostics, energy recovery braking, and low-pressure hydrogen refuelling. Developed with partners such as OMG Manufacturing, BluEnergy Revolution, and Dako-CZ, the project supports scalable diesel-to-hydrogen retrofitting.

Companies Covered in Locomotive Market

- CRRC Corporation Limited

- Siemens Mobility GmbH

- Alstom SA

- Wabtec Corporation

- Hitachi Rail Ltd.

- Bharat Heavy Electricals Limited (BHEL)

- Kawasaki Heavy Industries Ltd.

- GE Transportation

- Stadler Rail AG

- Bombardier Transportation

- Mitsubishi Heavy Industries Ltd.

- Toshiba Infrastructure Systems & Solutions

- Hyundai Rotem Company

- National Railway Equipment Company (NRE)

Frequently Asked Questions

The global locomotive market is projected to reach US$ 27.7 billion in 2026.

Steady rise in investments in rail infrastructure, digitalization of fleet operations, and regulatory mandates for decarbonization across transport sectors are driving the market.

The market is poised to witness a CAGR of 8.1% from 2026 to 2033.

The transition from legacy diesel platforms to electric and hybrid propulsion technologies, supported by government funding and international climate goals, a huge urbanization-driven passenger demand, and trade-linked freight volumes are creating new market opportunities.

CRRC Corporation Limited, Siemens Mobility GmbH, Alstom SA, and Wabtec Corporation are some of the key players in the market.