- Automotive Components & Materials

- Automotive ABS and ESC Market

Automotive ABS and ESC Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Automotive ABS and ESC Market by Product Type (Anti-lock Braking System, Integrated ABS + ESC Systems), Vehicle Type (Passenger Vehicle (Compact Car, Midsize Car, SUVs, Luxury), Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicle), Sales Channel (OEM, Aftermarket), and Region Analysis for 2026 to 2033

Automotive ABS and ESC Market Share and Trends Analysis

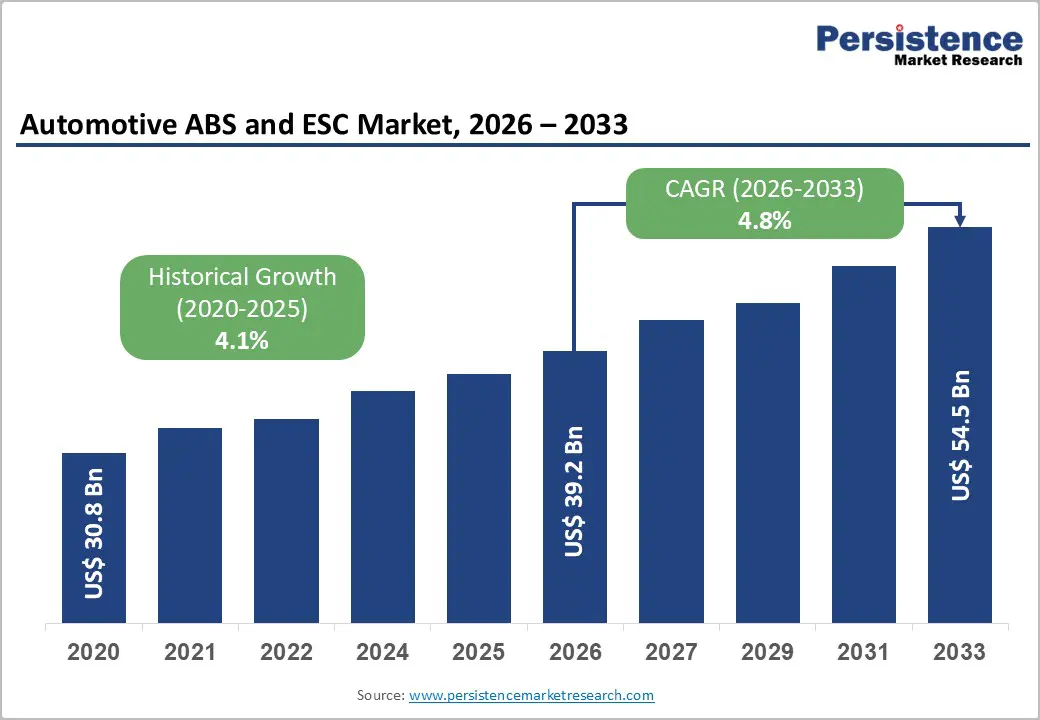

The global automotive ABS and ESC market size is anticipated at US$ 39.2 Bn in 2026 and is projected to reach US$ 54.5 Bn by 2033, growing at a CAGR of 4.84% between 2026 and 2033.

Stringent government safety mandates across North America, Europe, and the Asia Pacific, combined with accelerating electric vehicle adoption, expanding automotive production in emerging economies, and growing integration of ABS and ESC with ADAS platforms, are the primary forces fueling this sustained market expansion. Rising consumer safety awareness and OEM partnerships further reinforce market momentum through the forecast period.

Key Industry Highlights:

- Leading Product: Integrated ABS + ESC Systems leads with 61.4% market share and is also the fastest-growing product segment at 6.2% CAGR, driven by ADAS integration and global OEM mandates.

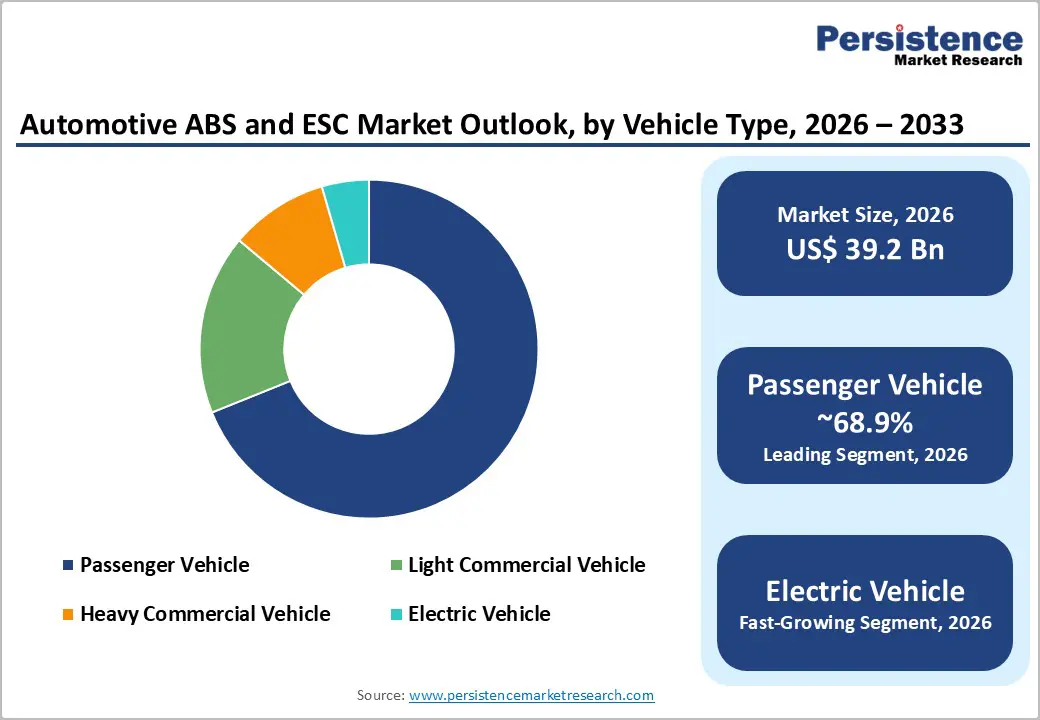

- Leading Vehicle Type: Passenger Vehicles command 68.9% vehicle type share; Electric Vehicles are the fastest-growing sub-segment at 11.5% CAGR, reflecting global electrification acceleration.

- Dominant Sales Channel: OEM channel dominates at 91.8% share; Aftermarket growing at a steady 2.9% CAGR in emerging markets.

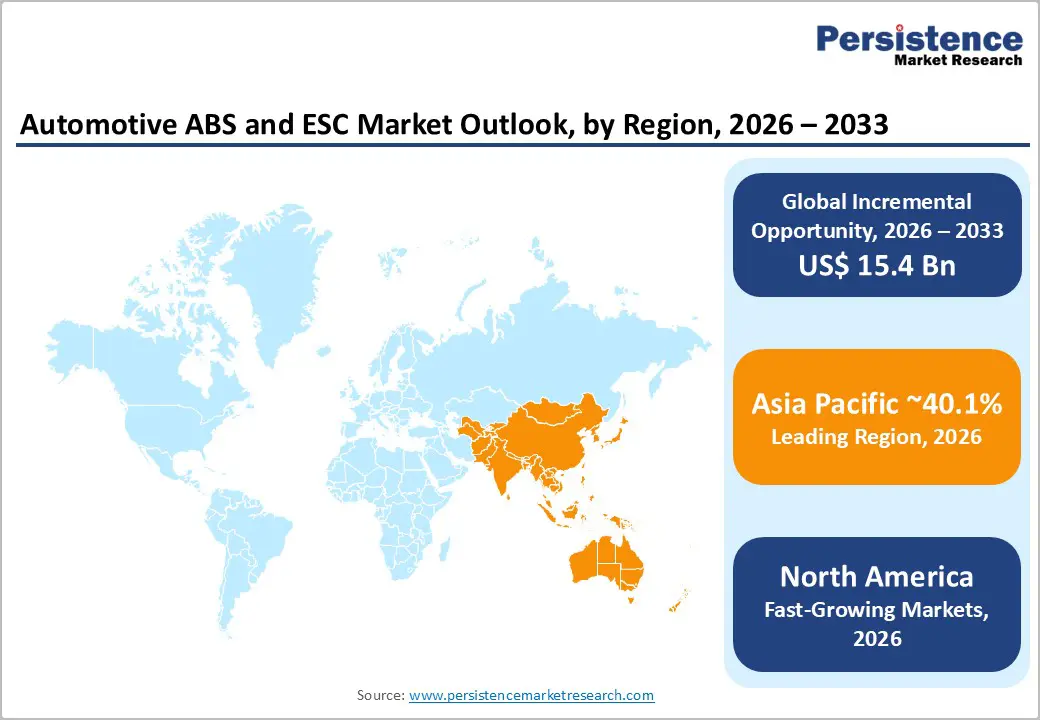

- Regional Leadership: Asia Pacific is the fastest-growing & dominating region, with a 40.1% share, anchored by China's EV production scale and India's expanding ABS mandate coverage.

- Opportunities: Key strategic developments, including ZF's brake-by-wire launch, Bosch's OTA braking platform, and Continental's China capacity expansion, are reshaping the competitive landscape with software-defined, EV-optimized braking architectures.

Market Dynamics

DRO Analysis - Stringent Government Regulatory Mandates for Vehicle Safety Systems

Regulatory pressure from major automotive governance bodies worldwide remains the single most powerful driver of ABS and ESC adoption. In the United States, the National Highway Traffic Safety Administration (NHTSA) mandated ESC under Federal Motor Vehicle Safety Standard (FMVSS) No. 126 as early as March 2007, requiring its fitment across all new passenger vehicles. The European Union has enforced ABS requirements on all new passenger cars since 2004, while the Indian government extended ABS mandates to all passenger cars and mini-buses from April 2018 onward, with further coverage for two-wheelers with an engine displacement above 125cc.

These policy-driven interventions directly translate into sustained volume growth for ABS and ESC suppliers, as automakers are legally obligated to integrate these systems into new model launches. With developing markets, particularly across Southeast Asia, Latin America, and Sub-Saharan Africa, now formulating comparable regulatory frameworks, the addressable market continues to expand structurally. The WHO Global Road Safety Report highlights that vehicle stability control technologies can reduce single-vehicle crash fatalities by up to 47%, reinforcing the global regulatory urgency.

Accelerating ADAS Integration and Technological Convergence

The convergence of ABS and ESC with Advanced Driver Assistance Systems (ADAS) represents a critical technology-driven growth lever for the market. Leading OEMs and Tier-1 suppliers are increasingly embedding ABS and ESC as foundational building blocks for higher-order autonomous and semi-autonomous vehicle architectures. Bosch's 2024 updates to its brake control platform, specifically enabling over-the-air software updates and configurable braking profiles for ADAS-compatible vehicles, exemplify this integration trend.

ZF Friedrichshafen's 2024 development of a fully brake-by-wire system for BEV and automated vehicle platforms further illustrates how ABS and ESC are evolving beyond standalone safety functions into intelligent, electronically coordinated modules. Industry data indicates over 150 million ABS units were produced annually as of 2025, reflecting mature volume baselines from which value-added, software-enriched ESC and integrated systems are capturing an increasing share. This technological escalation directly drives unit pricing uplift and market value expansion.

Restraints - Supply Chain Complexity and Semiconductor Dependency

ABS and ESC systems rely heavily on electronic control units (ECUs) and precision sensors, components acutely vulnerable to semiconductor supply disruptions. The global chip shortage of 2020-2023, which caused automotive production losses exceeding 7.7 million vehicles (AlixPartners estimate), demonstrated how supply chain fragility can directly constrain ABS/ESC system assembly, delay vehicle launches, and disrupt OEM production schedules. Geopolitical tensions and geographic concentration of chip fabrication continue to present structural supply risk for the market through the forecast horizon.

Complexity of Integration with Emerging Electrified Powertrains

The rapid proliferation of battery electric vehicles introduces unique technical and validation challenges for traditional ABS and ESC architectures. EVs deploy regenerative braking as the primary deceleration mechanism, requiring seamless coordination between mechanical ABS intervention and the electric motor's regenerative torque management. This integration complexity demands substantial R&D reengineering and calibration effort, potentially slowing the pace of ESC system certification and regulatory compliance for new EV platforms. Smaller Tier-2 and Tier-3 suppliers face particular constraints in meeting evolving EV-specific braking standards.

Opportunities - Electric Vehicle Proliferation and Specialized Braking Demand

The global EV market offers a transformative growth corridor for developers of ABS and ESC systems. Global EV sales surpassed 17 million units in 2024 (International Energy Agency), and are projected to exceed 40 million units annually by 2030. Each EV platform demands purpose-engineered ABS and ESC solutions that harmonize with regenerative braking, one-pedal driving dynamics, and lower center-of-gravity vehicle architectures, all of which require differentiated stability-control calibration.

This segment is projected to grow at the fastest CAGR of 11.5% within the Automotive ABS and ESC market through 2033. Tier-1 suppliers capable of delivering EV-optimized integrated safety modules stand to capture significant incremental revenue, particularly as premium EV OEMs in China, Europe, and North America ramp production volumes. The addressable opportunity within EV-specific ABS/ESC alone is estimated to exceed US$ 4-5 Bn by 2030, based on per-vehicle system value projections.

Emerging Market Penetration through Regulatory Expansion

Countries across South Asia, Southeast Asia, Africa, and Latin America are progressively aligning their vehicle safety regulatory frameworks with international standards. India's phased ABS mandate, already extended to two-wheelers, sets a precedent for broader ASEAN and African market regulation timelines. As these regions formalize mandatory fitment requirements, OEM production in local assembly hubs will drive incremental demand for ABS and ESC at scale.

With Asia Pacific representing the fastest-growing region at a 5.2% CAGR and home to several of the world's largest automotive production centers, localized manufacturing and supply chain investments in this region offer compelling commercial expansion opportunities for both established players and agile regional entrants. The untapped vehicle parc in these markets represents a multi-billion dollar addressable base for aftermarket ABS/ESC retrofitting programs as well.

Category-wise Analysis

Product Type Insights

Integrated ABS + ESC Systems commands the leading position in the product type category with a 61.4% market share in 2026. This dominance is driven by global regulatory mandates that increasingly require both functions as a bundled safety standard rather than standalone systems. Automakers across all vehicle segments, passenger cars, SUVs, and commercial vehicles, favor integrated modules due to their cost efficiency at scale, reduced system weight, and superior safety performance compared to single-function ABS alone. The growing deployment of ADAS platforms further entrenches integrated systems as the preferred OEM specification, and given current regulatory trajectories and EV adoption curves, dominance of this segment is expected to intensify through 2033.

The Integrated ABS + ESC Systems segment is also the fastest-growing, expanding at a CAGR of 6.2% through 2033. Rising OEM mandates for combined safety architectures in EV and autonomous vehicle platforms, coupled with ADAS integration, are the primary accelerants of this growth trajectory.

Vehicle Type Insights

Passenger Vehicles, encompassing Compact Cars, Midsize Cars, SUVs, and Luxury segments, lead the vehicle type category with a 68.9% market share in 2026. This position reflects the sheer volume of global passenger car production, the early and comprehensive regulatory mandates targeting this segment, and the strong consumer preference for safety-equipped vehicles in mature markets. Luxury and SUV sub-segments command particularly high ABS/ESC system values due to premium electronic integration requirements. While passenger vehicles will retain dominance, the rapid expansion of electric variants in this category is gradually increasing the technology complexity and per-unit value.

Electric Vehicles are the fastest-growing segment, posting a remarkable 11.5% CAGR through 2033. Purpose-built ABS/ESC architectures for EV platforms, driven by global electrification mandates and OEM commitments, are the primary catalysts fueling this exceptional growth rate.

Sales Channel Insights

The OEM channel dominates with a commanding 91.8% share in 2026, reflecting the capital-intensive, design-in nature of ABS and ESC integration, executed at the vehicle platform development stage rather than post-sale. Global automakers maintain long-term, multi-year supply contracts with Tier-1 safety system providers, thereby structurally entrenching the OEM channel. The deep technical collaboration required for system calibration, software integration, and regulatory certification creates high switching barriers that reinforce OEM channel supremacy. While the Aftermarket channel currently represents a modest share, quality and compliance improvements may incrementally expand its relevance in developing markets.

OEM remains the fastest-growing channel, driven by the surge in global vehicle production volumes; however, the Aftermarket is growing steadily at a 2.9% CAGR, supported by increasing vehicle replacement cycles, rising safety awareness in emerging markets, and the growing availability of OEM-equivalent ABS/ESC retrofit kits.

Regional Market Insights

North America Automotive ABS and ESC Market Insights

North America holds a prominent regional position in the global Automotive ABS and ESC Market, with a 4.1% CAGR in 2025, underpinned by the United States' comprehensive regulatory framework mandating ESC across all new vehicles under NHTSA's FMVSS No. 126. The U.S. automotive market, producing over 10 million vehicles annually, drives consistent ABS/ESC system volumes, with Canada representing an additional stable demand pool.

The region benefits from a robust innovation ecosystem, with technology leaders such as Bosch, Continental, and ZF operating major R&D centers. Ongoing NHTSA rulemaking on Automatic Emergency Braking (AEB) from 2029 will further stimulate ABS/ESC upgrades. Mexico's expanding vehicle manufacturing base further adds to North American production volumes and regional demand.

North America's growth is anchored by accelerating EV adoption, premium vehicle penetration, and ongoing ADAS mandates, creating sustained demand for high-value integrated ABS + ESC modules. The region remains the primary destination for investments in next-generation braking technology.

Europe Automotive ABS and ESC Market Insights

Europe maintains a significant and technologically advanced position in the global market, growing at a steady 3.7% CAGR through 2033, supported by the EU's long-standing mandatory safety framework and the European New Car Assessment Program (Euro NCAP).

Germany leads as the automotive engineering hub, home to Bosch, Continental, and ZF, with domestic OEM demand from BMW, Mercedes-Benz, and Volkswagen sustaining premium ABS/ESC system volumes. France and the U.K. contribute significant passenger car production volumes, while Spain anchors commercial vehicle assembly output. Euro NCAP's continuous tightening of safety star-rating criteria ensures European OEMs invest in increasingly sophisticated integrated stability systems.

Europe's regulatory harmonization under the General Safety Regulation (EU) 2019/2144, mandating ESC, AEB, and advanced braking across all new vehicles by 2024-2026, is a structural demand driver maintaining the region's strong technology adoption curve.

Asia Pacific Automotive ABS and ESC Market Insights

Asia Pacific is the fastest-growing and dominant region, with a 40.1% share, driven by the world's largest automotive production base and rapidly formalizing safety regulations across China, India, Japan, and ASEAN economies. China dominates regional demand, producing over 30 million vehicles annually and enforcing GB standards mandating ABS on all new passenger cars; its aggressive EV production scale, exceeding 9 million units in 2023, creates outsized incremental demand for EV-optimized braking systems. Japan contributes high-value ABS/ESC system manufacturing through Denso, Aisin, and Hitachi Astemo. India is a high-growth sub-market, with ABS mandates now covering passenger cars, commercial vehicles, and two-wheelers above 125cc, creating multi-segment demand acceleration.

The region's manufacturing cost advantages, growing middle-class vehicle ownership rates, and ongoing EV infrastructure investment make Asia Pacific the most strategically significant growth arena for ABS and ESC market participants through 2033.

Competitive Landscape

The global Automotive ABS and ESC Market is moderately consolidated, with the top four players, Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, and Denso Corporation, collectively accounting for over 60% of global market revenue. This concentration is sustained by decades of OEM relationship depth, proprietary ECU software platforms, and global manufacturing footprints that smaller competitors cannot readily replicate. Emerging players are differentiating through EV-specific braking solutions, sensor fusion capabilities, and software-defined braking architectures.

Innovation leadership, platform consolidation, and geographic expansion into Asia Pacific and emerging markets define the dominant strategic themes. Leading firms are investing aggressively in software-defined vehicle compatibility, OTA braking profile update capabilities, and AI-augmented predictive braking algorithms to maintain competitive differentiation and capture value-added pricing premiums in the evolving market.

Strategic Developments

- In May 2025, Knorr-Bremse AG entered a strategic collaboration with a major European commercial vehicle OEM to integrate advanced ESC and lane-keeping stability systems across its heavy truck platform lineup, aligning with forthcoming EU General Safety Regulation mandates for commercial vehicles.

- In March 2024, Robert Bosch launched an updated brake control platform with OTA update capability and configurable braking profiles, specifically engineered for ADAS and semi-autonomous vehicle architectures requiring adaptive safety calibration.

- In September 2024, Continental AG expanded its integrated ABS + ESC production footprint in China, investing in localized manufacturing capacity to serve rapidly growing domestic EV OEM demand and reduce supply chain lead times for Asian customers.

Companies Covered in Automotive ABS and ESC Market

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Hyundai Mobi

- Denso Corporation

- Aisin Corporation

- Hitachi Astemo

- Knorr-Bremse AG

- WABCO (ZF Division)

- Brembo S.p.A.

- Autoliv Inc.

- Mando Corporation

- Valeo S.A.

- Haldex AB

- Tenneco Inc.

Frequently Asked Questions

The automotive ABS and ESC market is valued at US$ 39.2 Bn in 2026 and is projected to reach US$ 54.5 Bn by 2033.

Stringent government safety mandates, ADAS integration requirements, and accelerating EV adoption are the primary growth drivers.

The market is projected to grow at a CAGR of 4.8% from 2026 to 2033.

The market is projected to grow at a CAGR of 4.8% from 2026 to 2033.

EV-specific braking system demand and regulatory expansion in emerging markets across Asia, Latin America, and Africa represent the most actionable growth opportunities.

Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Hyundai Mobis, Denso Corporation, Aisin Corporation, Hitachi Astemo, Knorr-Bremse, Brembo, and Autoliv are the leading global participants.