- Automotive Components & Materials

- Gear Motor Market

Gear Motor Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Gear Motor Market by Gear Type (Helical Gear Motor, Planetary Gear Motor, Bevel Gear Motor, Worm Gear Motor, Spur Gear Motor, Miscellaneous), Rated Power (Up to 7.5 kW, 7.5 kW - 75 kW, Above 75 kW), Torque (Up to 10,000 Nm, Above 10,000 Nm), Industry (Industrial Machinery, Automotive, Aerospace & Defense, Consumer Electronics, Agriculture, Energy & Power, Marine, Others), and Region Analysis for 2026 to 2033

Gear Motor Market Trends & Analysis

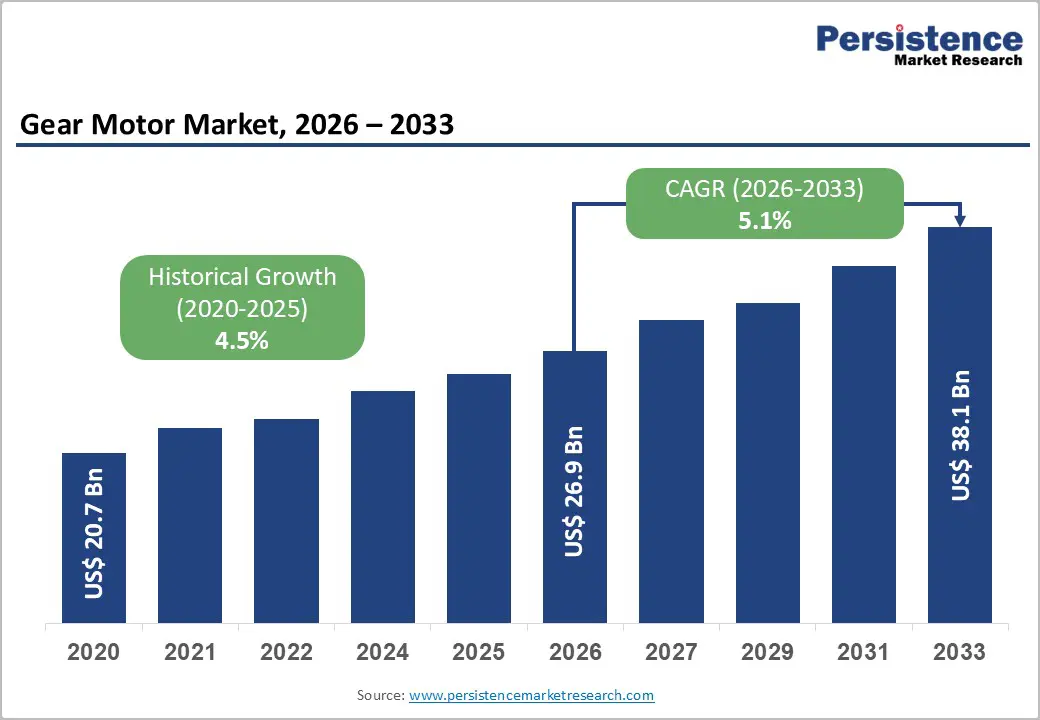

The global gear motor market size is anticipated to reach US$ 26.9 billion in 2026 and US$ 38.1 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033. This growth reflects broad-based demand across industrial machinery, energy infrastructure, and defense sectors, with gear motors serving as critical motion-control components in over 100 million installed units globally.

Industrial automation expansion, investment in the renewable energy sector, and the progressive integration of IoT-enabled predictive maintenance into manufacturing operations are the primary growth catalysts. The rising adoption of compact, high-torque planetary gear motors in robotics and EV powertrain applications is expanding the addressable markets beyond conventional industrial machinery.

Emerging markets across the Asia Pacific, particularly India and ASEAN, are sustaining volume-driven growth through infrastructure investment and manufacturing capacity expansion through 2033.

Key Industry Highlights:

- Leading Gear Type: Helical gear motors lead at 46.8% share; planetary gear motors are likely to grow fast at 6.1% CAGR, driven by robotics, EV auxiliary systems, and the global adoption of precision automation.

- Top Industry: Industrial machinery leads at 33.2% share; aerospace & defense is expected to grow fast at 6.1% CAGR, driven by UAV actuator, satellite drive, and defense precision gear motor procurement.

- Dominant Power Segment: Up to 7.5 kW leads at 51.6% share; Above 75 kW grows fastest at 5.7% CAGR, driven by wind energy, mining, and heavy industrial infrastructure programs.

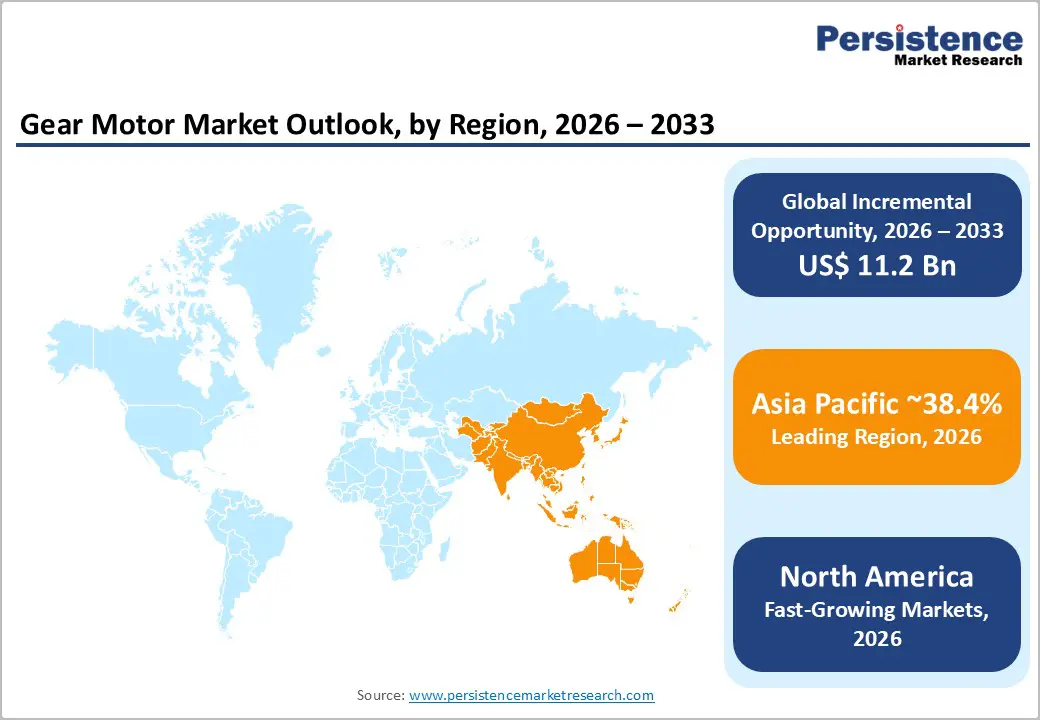

- Regional Performance: Asia Pacific dominates with a 38.4% share, led by China at US$ 4.4 Bn and India at US$ 1.5 Bn; North America is expected to grow at a 5.8% CAGR, with the U.S. at US$ 5.6 Bn in the forecast period.

- Strategic Developments: SEW-Eurodrive's ASEAN market expansion (November 2024) and Siemens Flender's advancement in offshore wind gear motors (September 2024) are reshaping the global competitive landscape.

Market Dynamics Analysis

Drivers - Industrial Automation and Smart Manufacturing Adoption Across Global Economies

The accelerating adoption of industrial automation, driven by labor cost pressures, precision manufacturing requirements, and Industry 4.0 digital transformation programs, is creating sustained structural demand for gear motors as foundational motion control components across conveyor systems, robotic arms, automated packaging lines, and material handling equipment. The International Federation of Robotics (IFR) reported 553,052 industrial robot installations globally in 2023, a 3% year-on-year increase, each requiring one or more gear motor assemblies for joint actuation and end-effector control. The global industrial automation market is projected to grow at 9% CAGR through 2028 (IFR), directly sustaining gear motor procurement pipelines.

Germany's Industrie 4.0 initiative, the U.S. Manufacturing USA network's advanced manufacturing programs, and China's "Made in China 2025" policy collectively represent over US$ 300 billion in smart manufacturing investment commitments. Each smart factory installation requires tens to hundreds of gear motors for precision motion control across assembly, welding, packaging, and logistics sub-systems. Japan's Ministry of Economy, Trade and Industry (METI) identified gear motors as critical components in its robotics infrastructure roadmap for 2030, reinforcing sustained procurement demand from Asia's advanced manufacturing base. These coordinated industrial policy investments create durable multi-year demand pipelines for gear motor manufacturers across all gear type configurations.

Renewable Energy Infrastructure Expansion and Wind Turbine Deployment

The global transition toward renewable energy, particularly wind and solar power, is generating a significant and growing demand base for high-torque, high-cycle-life gear motors in wind turbine pitch control systems, solar tracker drives, and hydroelectric plant actuators. The International Energy Agency's World Energy Outlook 2024 identified wind power capacity additions reaching 680 GW between 2023 and 2030, each modern onshore turbine requiring 3-5 precision planetary or helical gear motor assemblies for blade pitch and nacelle yaw control. The U.S. Inflation Reduction Act's US$ 369 billion clean energy investment framework is directly accelerating domestic wind farm construction.

The European Union's REPowerEU Plan targets 600 GW of offshore and onshore wind capacity by 2030, requiring hundreds of thousands of high-performance gear motor units across pitch, yaw, and auxiliary systems. India's Ministry of New and Renewable Energy targets 500 GW of renewable capacity by 2030, including 140 GW of wind, creating large-scale gear motor procurement demand for domestic and internationally sourced systems.

Solar tracking systems, increasingly deployed across utility-scale photovoltaic installations globally, require compact, weatherproof gear motor drives for single and dual-axis tracker actuation, adding a parallel high-volume application segment that expands gear motor demand beyond conventional industrial machinery markets.

Restraints - Global Supply Chain Fragility for Rare Earth Permanent Magnet Components

Gear motors incorporating permanent magnet synchronous motor (PMSM) drives depend on neodymium and dysprosium, rare-earth materials, with China controlling approximately 85% of global rare-earth processing capacity (U.S. Geological Survey, 2024). China's export quota restrictions on rare earth minerals, announced in July 2023 and extended in 2024, have introduced supply uncertainty and extended lead times for PMSM-integrated gear motor assemblies. The EU's Critical Raw Materials Act identifies rare earth supply chain resilience as a strategic industrial priority, underscoring the structural exposure that gear motor manufacturers face from rare earth concentration risk in procurement and production scheduling.

Restraint 2: Compatibility and Integration Complexity in Retrofit Automation Programs

Industrial operators undertaking automation retrofits and upgrading legacy machinery with modern gear motor assemblies face significant mechanical and electrical compatibility challenges when integrating new gear motor specifications into existing drivetrain architectures designed for older standards. NEMA and IEC gear motor mounting standards diverge across

North American and European industrial bases, creating customization requirements that extend installation timelines by 30-60% compared to greenfield deployments. These integration complexities slow replacement cycle velocity in existing industrial facilities, constraining addressable market growth velocity in the large installed-base retrofit segment, which represents over 40% of annual gear motor procurement by volume globally.

Opportunities - IoT-Enabled Smart Gear Motors and Predictive Maintenance Integration

The convergence of Industrial IoT sensor technology with gear motor systems, enabling real-time vibration monitoring, thermal performance tracking, torque load analysis, and predictive failure detection, is creating a differentiated, premium-priced product category of smart gear motors that command significantly higher margins than conventional mechanical assemblies. Siemens SIMOTICS, SEW-Eurodrive's MOVI-C ecosystem, and Bonfiglioli's connected drive platforms represent early commercial implementations where embedded sensors and digital interfaces transform gear motors from passive mechanical components into active data nodes within Manufacturing Execution System (MES) architectures.

The global industrial predictive maintenance market is projected to grow from US$ 5.5 billion in 2023 to over US$ 28 billion by 2030, with smart gear motor connectivity identified as a primary data input layer for machine health monitoring systems. Manufacturers capable of delivering IIoT-ready gear motor assemblies with standardized communication protocols (OPC-UA, PROFINET, EtherNet/IP) are positioned to capture a US$ 3-5 Bn addressable premium product market by 2030, representing a significant value-add opportunity above the commodity gear motor replacement market, rewarding technology-integrated platform providers.

Aerospace & Defense and E-Mobility Applications Driving High-Specification Gear Motor Demand

Aerospace & Defense, the fastest-growing end-use segment at 6.1% CAGR, and electric vehicle powertrains are jointly creating demand for ultra-precision, high-torque-density gear motor configurations that exceed conventional industrial specifications in reliability, weight optimization, and environmental survivability. UAV actuator systems, satellite antenna positioning drives, missile fin control actuators, and naval vessel auxiliary systems each require custom-engineered gear motor solutions that meet qualification standards far exceeding commercial industrial-grade standards, creating high-barrier, high-margin procurement opportunities for certified defense-grade gear motor suppliers.

Electric vehicle traction and auxiliary systems, including EV window regulators, seat adjustment mechanisms, HVAC blower motors, and e-axle gear reduction stages, are creating a high-volume gear motor demand stream that aligns with the global EV production trajectory, exceeding 40 million annual units by 2030. The EV-specific gear motor addressable market is estimated at US$ 4-6 Bn by 2030, representing incremental demand above the conventional automotive segment. For gear motor manufacturers investing in miniaturized, lightweight, and thermally optimized designs for EV applications, this segment offers both volume scale and premium pricing versus standard industrial gear motor configurations.

Category-wise Analysis

Gear Type Insights

Helical gear motors lead the gear type segment with a 46.8% share in 2026. Their dominance stems from superior load-bearing efficiency, smooth and quiet torque transmission, and broad applicability across industrial machinery, conveyor systems, and material handling, the highest-volume end-use categories. Helical gears' ability to distribute tooth engagement load progressively across multiple contact points delivers higher torque capacity at lower noise and vibration levels versus spur gears, making them the standard specification for general industrial applications.

Worm and bevel gear motors serve specific orientation and angle transmission requirements, while planetary gear motors are gaining share in compact high-torque applications. Helical dominance is expected to remain structurally intact through 2033, given its entrenched position in industrial machinery procurement specifications.

Planetary gear motors are the fastest-growing gear type, with a 6.1% CAGR through 2033. Their superior torque density, minimal backlash, and compact form factor align directly with robotics, EV auxiliary systems, and precision automation applications, the fastest-growing end-use categories, driving accelerated adoption above all other gear type configurations.

Rated Power Insights

Up to 7.5 kW gear motors lead the rated power segment with a 51.6% share in 2026. This power band serves the largest-volume applications, including light industrial automation, consumer electronics manufacturing, agricultural equipment, packaging machinery, and small conveyor systems, where compact, energy-efficient, low-power drives are specified in high volume. The sub-7.5 kW segment benefits from the broadest available product range, lowest per-unit manufacturing costs, and widest distribution network coverage across industrial, OEM, and MRO channels globally. The 7.5-75 kW mid-range serves medium industrial machinery, while the segment above 75 kW serves heavy industrial, mining, and marine applications at lower volume but with significantly higher per-unit values. Sub-7.5 kW dominance is expected to persist through 2033.

Above 75 kW gear motors are the fastest-growing segment by rated power, with a 5.7% CAGR through 2033. Heavy-duty industrial applications in mining, offshore energy, and large wind turbine auxiliary systems, combined with infrastructure investment programs requiring high-power motion systems, are driving accelerated procurement in the high-power gear motor segment.

Torque Insights

Up to 10,000 Nm gear motors lead the torque segment with a 66.7% market share in 2026. The sub-10,000 Nm torque range encompasses the vast majority of industrial gear motor applications, including robotics, packaging, conveyors, agricultural equipment, HVAC systems, and automotive assembly, where moderate-torque, high-speed configurations are the dominant specification.

This torque band's broad applicability across virtually all industrial end-use sectors sustains high-volume procurement across general industrial, OEM, and replacement channels. Above 10,000 Nm configurations serve specialized heavy industry, marine, mining, and large-scale renewable energy applications at significantly lower unit volumes but higher per-unit values. The dominance of sub-10,000 Nm is structurally underpinned by the volume-weighted demand for light-to-medium industrial applications globally.

Above 10,000 Nm gear motors are the fastest-growing torque segment at 5.6% CAGR through 2033. Heavy-duty industrial applications in wind energy pitch systems, offshore platform drives, and large-scale conveyor systems for mining and port logistics are driving accelerating high-torque gear motor procurement through 2033.

Industry Analysis

Industrial machinery leads the Industry segment with a 33.2% market share in 2026. Industrial machinery encompasses the widest and most volume-intensive gear motor application base, covering conveyors, mixers, extruders, presses, hoists, and automated manufacturing equipment across virtually every manufacturing sub-sector globally.

Its dominance reflects both the structural dependence of industrial machinery on gear-motor-based motion control and the high replacement cycle volumes generated by the world's installed base of over 100 million industrial gear-motor units (Interact Analysis, 2025). Automotive and energy sectors contribute significant revenue at a lower share, while emerging applications in aerospace and consumer electronics are growing in strategic importance. Industrial machinery's structural leadership is expected to be sustained through 2033, given the depth and breadth of its application coverage.

Aerospace & Defense is the fastest-growing Industry at 6.1% CAGR through 2033. Defense UAV actuator systems, satellite drive mechanisms, naval auxiliary drives, and next-generation missile control system requirements are collectively driving accelerating high-specification gear motor procurement through 2033.

Regional Insights

North America Gear Motor Market Insights

North America is the fastest-growing regional market at 5.8% CAGR through 2033, with the U.S. market estimated at US$ 5.6 Bn in 2026, driven by industrial automation investment, defense procurement programs, and manufacturing reshoring initiatives expanding domestic gear motor demand.

U.S. Gear Motor Market Trends

The U.S. Manufacturing USA network's 16 advanced manufacturing institutes, the IRA's US$ 369 Bn clean energy investment framework driving wind and solar gear motor demand, and DoD aerospace procurement programs requiring defense-grade precision gear motor assemblies collectively sustain North America's high-growth trajectory. Regal Rexnord, Emerson Electric, and Eaton anchor the regional competitive landscape with broad industrial and aerospace product portfolios. Canada contributes mining and energy sector gear motor demand. North America's growth is driven by industrial reshoring investment, aerospace & defense program expansion, and IRA-funded renewable energy infrastructure requiring high-torque gear motor configurations across wind and solar applications.

Europe Gear Motor Market Trends

Europe holds a prominent 22.4% share of the global Gear Motor Market in 2025, with Germany's market estimated at US$ 1.7 Bn, anchored by the continent's concentration of world-leading gear motor OEMs, advanced industrial machinery demand, and EU energy transition investment programs.

Germany Gear Motor Market

Germany hosts SEW-Eurodrive, Siemens, Flender (Siemens division), and Bauer Gear Motor, four of the world's most technically differentiated gear motor manufacturers, sustaining Germany's position as both the largest national market and the global technology standard-setter. The EU's REPowerEU wind capacity expansion program, EU machinery regulation upgrades mandating higher efficiency motor systems, and Industry 4.0 smart manufacturing investment sustain premium demand. France contributes aerospace gear motor demand through Airbus procurement, Spain drives wind energy applications, and the U.K. sustains defense gear motor programs. Europe's growth is anchored by wind energy infrastructure gear motor procurement, EU energy-efficiency motor regulations, and the adoption of IoT-integrated smart gear motor platforms across advanced manufacturing facilities.

Asia Pacific Gear Motor Market Insights

Asia Pacific holds the leading regional position with 38.4% share of the global Gear Motor Market in 2025, driven by China's dominant industrial manufacturing base, India's rapidly expanding infrastructure and automation investments, and ASEAN's growing manufacturing capacity across the electronics, automotive, and consumer goods sectors.

China & India Gear Motor Market Trends

China is estimated to have a US$ 4.4 Bn market in 2026, anchored by its position as the world's largest industrial machinery, automotive, and consumer electronics production base, which requires high-volume gear motor procurement, alongside domestic manufacturers Jiangsu Guomao and Hengdrive, which offer competitive, low-cost alternatives to global brands.

India, estimated at US$ 1.5 Bn, is growing rapidly, driven by the PLI scheme for manufacturing, the PM Gati Shakti infrastructure investment, and expanding domestic adoption of automation. Japan contributes to precision gear motor demand through Nabtesco, Nidec, and Sumitomo Heavy Industries. Asia Pacific's manufacturing scale, cost advantages, and expanding automation investment make it the structural volume and growth anchor of the global gear motor market through 2033.

Competitive Landscape

The global gear motor market is moderately consolidated, with the top 30 manufacturers accounting for approximately 84-86% of global sales (Interact Analysis, 2025), led by SEW-Eurodrive, Siemens/Flender, Bonfiglioli, and Regal Rexnord. Market leaders differentiate through proprietary gear geometry, integrated drive electronics, IIoT connectivity platforms, and application engineering support. Emerging business models center on gear motor-as-a-service and digital twin maintenance subscription platforms.

Technology investment in IoT-integrated smart gear motor platforms, geographic expansion into Asia Pacific and Middle East industrial markets, energy efficiency standard compliance, and aerospace-grade precision gear motor portfolio development define the dominant competitive strategy themes shaping the global gear motor competitive landscape through 2033.

Key Developments:

- In February 2025, Regal Rexnord Corporation completed portfolio optimization of its industrial gear motor division, divesting non-core product lines and redirecting R&D investment toward IoT-connected smart gear motor platforms for automated material handling and precision manufacturing applications globally.

- In November 2024, SEW-Eurodrive expanded its MOVI-C integrated gear motor and drive platform into Southeast Asian markets, establishing new application engineering centers in Vietnam and Thailand to support the region's rapidly scaling electronics and automotive manufacturing automation investment programs.

Companies Covered in Gear Motor Market

- SEW

- Eurodrive GmbH & Co KG

- Siemens AG (Flender Division)

- Bonfiglioli Riduttori S.p.A.

- Regal Rexnord Corporation

- ABB Ltd.

- Nidec Corporation

- Emerson Electric Co.

- Sumitomo Heavy Industries Ltd.

- Nabtesco Corporation

- Bauer Gear Motor GmbH

- Eaton Corporation PLC

- Johnson Electric Holdings Limited

- Jiangsu Guomao Reducer Co. Ltd.

- WEG S.A. - Portescap (Danaher Division)

Frequently Asked Questions

The gear motor market is valued at US$ 26.9 Bn in 2026, projected to reach US$ 38.1 Bn by 2033.

Industrial automation expansion, renewable energy infrastructure investment, and IoT-enabled smart gear motor integration across manufacturing and robotics applications are the primary growth drivers.

The gear motor market is projected to reach a CAGR of 5.1% from 2026 to 2033.

IoT-integrated smart gear motor platforms for predictive maintenance and high-specification aerospace and EV application gear motor development represent the most strategically actionable near-term growth opportunities.

SEW-Eurodrive, Siemens (Flender), Bonfiglioli, Regal Rexnord, ABB, Nidec, Emerson Electric, Sumitomo Heavy Industries, Nabtesco, and Bauer Gear Motor are the leading global participants.