- Automotive Components & Materials

- Automotive Headliner Market

Automotive Headliner Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Automotive Headliner Market by Headliner Type (Built-in (Standard Headliners), Tilt & Slide Headliners, Top Mount Headliners, Solar Glass / Panoramic Headliners, Pop-up / Tilt Panoramic Systems), Material Type (Fabric, Polyester, Plastic), Vehicle Type (Passenger Vehicle (Compact Car, Midsize Car, SUV's, Luxury), Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicle), and Region Analysis for 2026 to 2033

Automotive Headliner Market Trends & Analysis

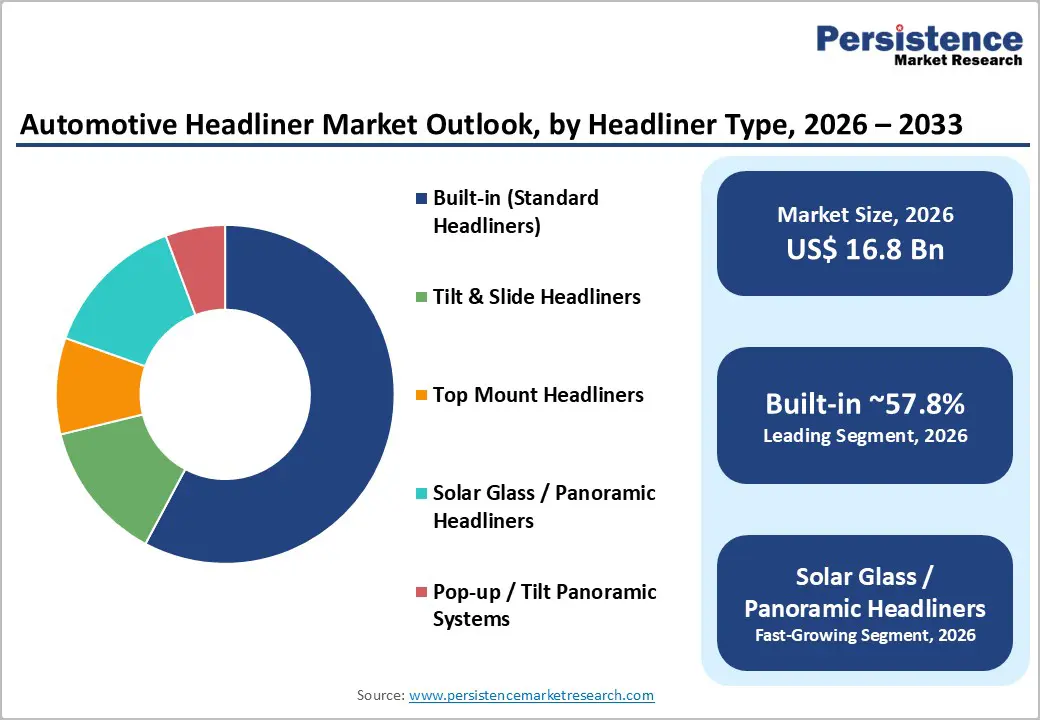

The global automotive headliner market size is projected at US$ 16.8 billion in 2026 and is projected to reach US$ 23.0 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033. This growth reflects rising consumer demand for premium vehicle interiors, acoustic comfort, and lightweight headliner solutions as automakers compete to differentiate the cabin experience across passenger and electric vehicle platforms globally.

The rise in consumer preference for enhanced in-cabin aesthetics, OEM investment in lightweight composite headliner materials to support fuel-efficiency targets, and EV platform interior premiumization driving panoramic and solar-glass headliner adoption are the primary growth catalysts. Acoustic performance requirements under tightening EU and U.S. noise-emission standards are driving fabric and polyester headliner upgrades. Asia Pacific's vehicle production scale and premiumization trends are anchoring volume-driven demand growth through 2033.

Key Industry Highlights:

- Leading Headliner Type: Built-in Standard Headliners lead at 57.8% share; Solar Glass / Panoramic Headliners grow fastest at 7.0% CAGR, driven by premium EV and SUV panoramic roof adoption globally.

- Top Material Segment: Fabric leads with a 41.5% share; Plastic grows fastest at a 5.9% CAGR, driven by lightweighting mandates and the adoption of thermoplastic headliners in EV and premium vehicle platforms.

- Vehicle Type Performance: Passenger Vehicles lead with a 67.8% share; Electric Vehicles grow fastest at a 7.2% CAGR, driven by EV premiumization and acoustic performance requirements across global EV production.

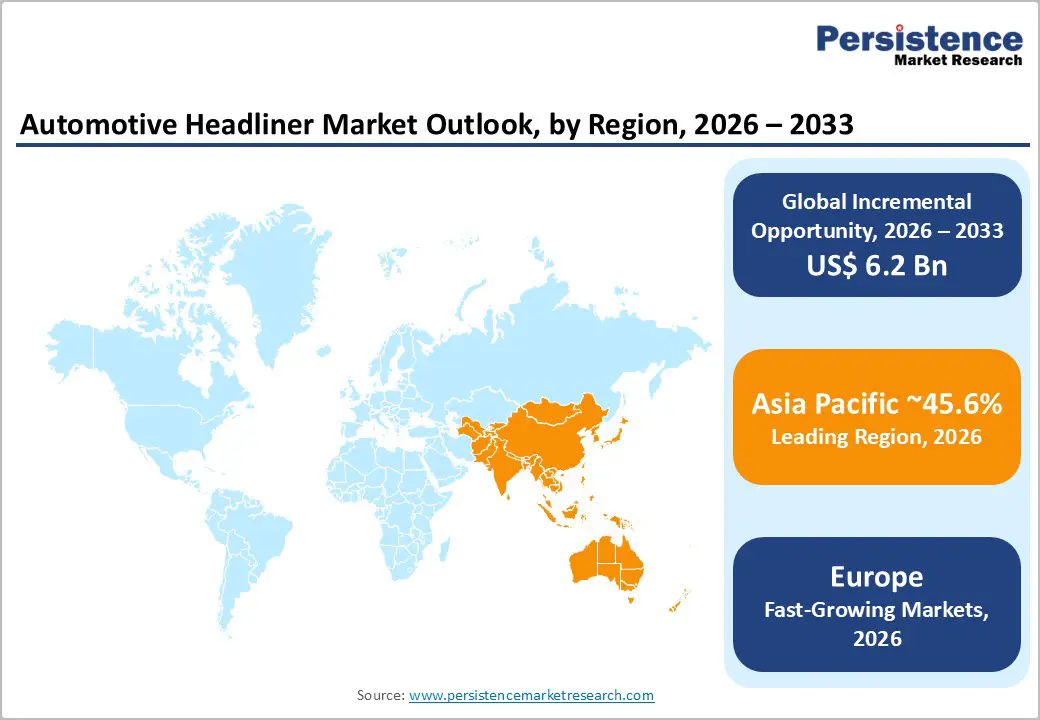

- Regional Performance: Asia Pacific leads with a 45.6% share, driven by China at US$ 3.0 Bn and India at US$ 689.1 Mn; North America holds a 24.8% share, led by the U.S. at US$ 3.4 Bn in 2026.

- Strategic Developments: Grupo Antolin's advancement of its smart headliner platform (February 2025) and IAC Group's expansion of its China panoramic headliner line (January 2024) are defining next-generation competitive positioning in the global headliner market.

Market Dynamics Analysis

Drivers - Rising Consumer Demand for Premium Vehicle Interior Aesthetics and Acoustic Comfort

Growing consumer expectations for premium cabin environments, driven by rising disposable incomes, premiumization trends across compact and midsize vehicle segments, and increasing crossover and SUV ownership, are structurally elevating OEM headliner specification standards beyond basic coverage toward acoustically optimized, visually differentiated interior surfaces. The International Organization of Motor Vehicle Manufacturers (OICA) reported global passenger vehicle production at 70.2 million units in 2023, with premium and SUV categories growing disproportionately, each requiring higher-specification headliner assemblies incorporating multi-layer acoustic substrates, integrated ambient lighting channels, and premium fabric finishes.

J.D. Power's 2024 U.S. Initial Quality Study identified interior comfort and noise insulation among the top five factors influencing vehicle purchase satisfaction, directly incentivizing OEMs to invest in high-performance headliner systems as a competitive differentiator in interior quality. Luxury automakers, including BMW, Mercedes-Benz, and Audi, specify multi-functional headliner assemblies incorporating Alcantara fabric, integrated surround-sound channels, and panoramic glass sections, establishing premium specification benchmarks that are progressively adopted across mid-range segments. This premiumization cascade from luxury to mainstream vehicle segments creates a structurally expanding addressable market for advanced headliner configurations across all vehicle categories globally through 2033.

Lightweighting Mandates and EV Platform Interior Innovation Requirements

Global automotive fuel efficiency and emissions regulations, including the EU's CO2 fleet average target of 95g/km, U.S. CAFE standards targeting 55 mpg by 2026, and China's CAFC Phase 5 fuel consumption standards, are mandating systemic vehicle weight reduction programs in which headliner assemblies represent an actionable lightweighting opportunity through advanced composite substrate and thermoplastic component adoption. Every kilogram saved in headliner assembly weight contributes directly to meeting fleet CO2 compliance targets for ICE vehicles and extending stated range metrics for EVs. Headliner weight reduction programs targeting 20-30% mass savings versus conventional fiber-reinforced polyurethane boards are being actively pursued by Grupo Antolin, Toyota Boshoku, and IAC Group.

Electric vehicle platforms, structurally eliminating engine noise masking that traditionally concealed road and wind noise in ICE vehicles, create heightened acoustic headliner performance requirements that simultaneously drive material innovation and per-unit value escalation. Tesla's cabin acoustic engineering investment, Rivian's premium headliner specifications for its R1T and R1S platforms, and BYD's premium EV interior programs collectively demonstrate that EV OEMs are specifying higher-value headliner assemblies than their conventional ICE vehicle equivalents. With global EV production projected at 40 million units per year by 2030 (IEA), EV-driven headliner specification premiumization represents a significant per-unit revenue uplift opportunity for headliner manufacturers investing in EV-optimized acoustic and aesthetic product configurations.

Restraints - Supply Chain Vulnerability for Specialty Fabric and Composite Substrate Materials

Automotive headliner manufacturing depends on specialty nonwoven fabric substrates, polyurethane foam layers, and glass fiber composites sourced from a limited number of qualified automotive-grade material suppliers globally. Disruptions in polyurethane and glass fiber supply chains, exacerbated by volatility in petrochemical feedstocks and concentrated supplier geographies, have extended headliner material procurement lead times by 15-30% across key manufacturing regions.

The Society of Plastics Engineers' automotive division identified composite substrate supply reliability as a top-three procurement risk for interior component manufacturers in 2024, directly constraining production scheduling flexibility for headliner assemblers serving just-in-time OEM delivery requirements globally.

Stringent OEM Qualification Cycles Limiting New Entrant Competitive Access

Automotive headliner suppliers face rigorous OEM qualification processes, encompassing flammability (FMVSS 302), volatile organic compound (VOC) emissions (ISO 12219), and dimensional stability testing requirements, that extend new product development and supplier approval cycles to 18-36 months per OEM program. This qualification burden creates structural entry barriers that protect incumbent suppliers while limiting competitive pricing pressure from entrants using alternative materials or manufacturing technologies. For emerging lightweight composite or bio-based headliner material manufacturers, the complexity of OEM qualification effectively delays market commercialization by 2-3 vehicle production cycles, constraining the pace at which innovative headliner solutions penetrate high-volume OEM production programs globally.

Opportunities - Smart and Connected Headliner Systems for Autonomous and Premium Vehicle Platforms

The convergence of automotive interior intelligence with headliner structures, integrating ambient lighting arrays, overhead display projection surfaces, microphone arrays for voice recognition, overhead sensor clusters for autonomous driving, and capacitive touch controls, is creating a high-value smart headliner product category with substantially higher per-unit content value than conventional assemblies.

Autonomous vehicle interior design concepts from Waymo, Cruise, and major OEMs allocate a significantly larger functional role to the headliner as a primary passenger interface surface, replacing conventional dashboard-centric architectures with overhead-mounted display and control systems.

The global automotive smart interior market is projected to exceed US$ 12 Bn by 2030, with smart headliner systems estimated to capture 15-20% of that addressable value as integrated overhead ambient systems become standard specification in Level 3+ autonomous and premium EV platforms. Headliner manufacturers investing in electronics integration capabilities and partnering with lighting suppliers (Hella, Osram), sensor integrators (Valeo, Bosch), and display technology companies are positioned to capture the high-margin smart headliner segment and structurally increase revenue per vehicle unit above the conventional headliner assembly value.

Sustainable and Bio-Based Headliner Materials Aligned with OEM Circular Economy Commitments

Major global OEMs, including Volkswagen Group, BMW Group, Ford, and Toyota, have publicly committed to measurable sustainability targets, including 40-50% recycled or renewable material content in vehicle interiors by 2030 under their respective sustainability roadmaps. These commitments are creating direct procurement mandates for headliner suppliers capable of offering bio-based fabric substrates, recycled PET fiber nonwovens, and formaldehyde-free bonding systems meeting automotive performance specifications, a market segment where incumbent suppliers have only partially developed compliant product portfolios.

Natural fiber composite headliners, incorporating hemp, flax, or kenaf fiber substrates, offer comparable acoustic performance to conventional glass fiber boards at 20-25% lower weight and significantly reduced carbon footprint across the lifecycle assessment metrics increasingly required for OEM supply chain sustainability reporting.

The European automotive bio-based materials market for interior components is estimated to grow at 8-10% CAGR through 2030 driven by EU End-of-Life Vehicle Directive revisions and OEM supply chain sustainability KPI mandates. For headliner manufacturers, establishing bio-based material qualification ahead of regulatory enforcement timelines positions them to capture a premium-priced, compliance-driven product category estimated at US$ 1.5-2.5 Bn within the broader headliner addressable market by 2030.

Category-wise Analysis

Headliner Type Insights

Built-in (Standard Headliners) lead the headliner type segment with a 57.8% market share in 2026. Their dominance reflects universal specification across the broadest vehicle production volume base, covering compact, midsize, and entry-level SUV categories, where fixed-panel headliner assemblies offer the lowest production complexity, highest design flexibility, and most cost-efficient manufacturing integration for OEM assembly lines globally.

Tilt & slide and top mount headliners serve specialized vehicle configurations requiring sunroof compatibility, while solar glass and panoramic systems are growing rapidly from premium-vehicle-driven adoption. Built-in headliner structural dominance is expected to persist through 2033 given the volume weight of standard vehicle production, though Solar Glass and Panoramic variants are steadily narrowing share as premium specifications cascade to mainstream vehicle segments.

Solar glass / panoramic Headliners are the fastest-growing headliner type at 7.0% CAGR through 2033. Consumer demand for open, premium cabin experiences in SUVs and EVs, combined with OEM differentiation strategies that deploy full-length panoramic roofs as standard features across premium and electric vehicle platforms, is driving rapid adoption of solar glass and panoramic headliner assemblies globally.

Material Type Insights

Fabric leads the material type segment with a 41.5% share in 2026. Fabric headliners dominate by virtue of their superior acoustic absorption performance, broad design aesthetic versatility, the ability to accommodate diverse textures, patterns, and colors across vehicle interior design programs, and well-established integration with headliner substrate bonding processes. Fabric's cost-effectiveness at scale, wide OEM acceptance across passenger and commercial vehicle platforms, and compatibility with acoustic foam laminate systems sustain its structural market leadership.

Polyester serves as a cost-competitive fabric alternative across value segment vehicles, while Plastic headliner systems serve specific hard-molded overhead console and structural applications. Fabric dominance is expected to be maintained through 2033, despite growing adoption of plastics in lightweight and EV platform applications.

Plastic is the fastest-growing material type at 5.9% CAGR through 2033. Thermoplastic headliner substrates delivering superior weight reduction, dimensional stability in high-temperature EV thermal environments, and design freedom for integrated sensor and lighting mounting are driving the acceleration of plastic material adoption across premium and electric vehicle headliner programs globally.

Vehicle Type Insights

Passenger vehicles lead the vehicle type segment with a 67.8% share in 2026. Passenger vehicles, spanning compact cars, midsize sedans, SUVs, and luxury categories, represent the highest-volume and most design-intensive headliner application base globally, where acoustic performance, aesthetic differentiation, and integrated functional systems create premium procurement specifications across all price segments.

The global passenger vehicle production base, exceeding 70 million annual units, drives high-volume headliner procurement, with SUV and crossover growth progressively elevating per-unit headliner content value through larger surface areas and premium material specifications. Light and Heavy Commercial Vehicles require durable, functional headliners at lower per-unit costs, while EV adoption is driving premium-specification escalation. Passenger Vehicle dominance will persist structurally through 2033.

Electric vehicles are the fastest-growing vehicle type at 7.2% CAGR through 2033. EV-specific acoustic requirements to eliminate engine noise masking, OEM premiumization of EV interiors, and growing EV production volumes, projected at 40 million units annually by 2030 per the IEA, are driving accelerating high-value headliner specification and procurement globally in the EV segment.

Regional Insights

North America Automotive Headliner Market Insights

North America holds a prominent 24.8% share of the global automotive headliner market in 2025, driven by the U.S.'s high-volume SUV and crossover vehicle production base, consumer preference for premium interior specifications, and OEM investment in lightweight acoustic headliner systems supporting CAFE fuel efficiency compliance. FMVSS 302 flammability and VOC emission regulations shape material qualification requirements across the regional supply base.

Motus Integrated Technologies, Lear Corporation, and IAC Group anchor the regional competitive landscape with vertically integrated headliner design, material, and assembly capabilities serving major U.S. OEM programs. North America's growth is driven by EV interior premiumization, panoramic headliner adoption in SUV segments, and smart headliner technology integration programs supporting the development of autonomous vehicle interiors.

U.S. Automotive Headliner Market: SUV & EV Interior Premiumization

The U.S. market is estimated at ~US$ 3.4 Bn in 2026, sustained by high SUV and crossover production volumes at Ford, GM, and Stellantis facilities, EV interior upgrade programs at Tesla and Rivian, and increasing adoption of panoramic roof headliners across mainstream vehicle segments. Canada contributes to OEM assembly plant headliner procurement demand, supporting Honda and Toyota Canadian manufacturing programs through 2033.

Europe Automotive Headliner Market Insights

Europe is growing at a prominent pace of 4.5% CAGR through 2033, driven by EU CO2 fleet emissions mandates accelerating lightweight headliner adoption, premium OEM vehicle production in Germany requiring advanced acoustic and aesthetic headliner specifications, and circular-economy regulatory frameworks stimulating bio-based and recycled-material headliner development across the regional automotive supply chain.

EU End-of-Life Vehicle Directive revisions mandating higher recycled-material content in vehicle interiors are directly incentivizing sustainable headliner-material development at Grupo Antolin, Freudenberg, and Borgers. The competitive landscape features technically differentiated suppliers with OEM co-development relationships at BMW, Volkswagen, and Stellantis European plants, sustaining premium program sourcing.

Germany Automotive Headliner Market: Lightweighting & Premium OEM Demand

Germany's market is estimated at ~US$ 1.3 Bn in 2026, anchored by BMW, Volkswagen, and Mercedes-Benz premium vehicle headliner programs requiring advanced acoustic and sustainable material specifications. The U.K. contributes Jaguar Land Rover luxury headliner procurement and JLR EV platform interior programs. France sustains Stellantis and Renault mainstream headliner procurement with growing bio-based material integration under EU sustainability mandates through 2033.

Asia Pacific Automotive Headliner Market Insights

Asia Pacific commands the leading and fastest-growing regional position at 45.6% share in 2025, driven by China's dominant vehicle production scale, India's rapidly expanding passenger vehicle market, Japan's precision automotive interior manufacturing, and ASEAN's growing OEM assembly plant headliner procurement across Thailand, Indonesia, and Vietnam.

China, India & Japan Automotive Headliner Market: Production Scale & Premiumization

China's market is estimated at US$ 3.0 Bn in 2026, sustained by China State Grid's EV expansion, driving premium EV headliner demand at BYD, NIO, and Geely platforms, alongside Toyota Boshoku and Kasai domestic manufacturing operations. India's market, at ~US$ 689.1 Mn, is growing under the PLI scheme, vehicle production investments and rising SUV segment adoption. Japan contributes precision headliner manufacturing through Toyota Boshoku and Hayashi Telempu, serving global OEM programs.

Competitive Landscape

The global automotive headliner market is moderately consolidated, with the leading players accounting for approximately 55-60% of global market share, led by Grupo Antolin, Motus Integrated Technologies, Toyota Boshoku, and IAC Group, who differentiate through vertically integrated material-to-assembly capabilities, OEM co-development partnerships, and smart headliner technology investment. Emerging business models center on sustainable material platform development and smart interior integration partnerships.

Technology investment in smart and acoustic headliner systems, geographic expansion into India and ASEAN OEM supply chains, lightweight composite material development for EV platforms, and sustainable bio-based material qualification aligned with OEM circular economy mandates define the dominant strategic themes across the global competitive landscape through 2033.

Key Developments:

- In February 2025, Grupo Antolin advanced its smart headliner platform integrating ambient lighting arrays, microphone systems, and overhead display projection surfaces, targeting Level 3+ autonomous vehicle interior programs at European and U.S. OEM partners through co-development agreements supporting next-generation premium vehicle interior architectures.

- In October 2024, Toyota Boshoku Corporation expanded headliner manufacturing capacity at its India facility in Gujarat, targeting growing domestic passenger vehicle and EV headliner demand under India's PLI scheme, committing investment toward lightweight composite and bio-based substrate headliner production lines.

Companies Covered in Automotive Headliner Market

- Grupo Antolin

- Irausa S.A.

- Motus Integrated Technologies LLC

- Toyota Boshoku Corporation

- IAC Group

- Lear Corporation

- Howa Co. Ltd.

- UGN Inc.

- SA Automotive

- Hayashi Telempu Corporation

- Kasai North America Inc.

- Freudenberg Performance Materials

- Borgers SE & Co. KGaA

- International Automotive Components Group

- Johns Manville

- Toray Plastics Inc.

Frequently Asked Questions

The automotive headliner market is valued at US$ 16.8 Bn in 2026, projected to reach US$ 23.0 Bn by 2033.

Rising consumer demand for premium cabin acoustics and aesthetics, EV interior premiumization, and OEM lightweighting mandates driving advanced composite headliner material adoption are the primary structural growth drivers.

The automotive headliner market is projected to grow at a CAGR of 4.6% from 2026 to 2033.

Smart connected headliner systems for autonomous vehicle platforms and sustainable bio-based material development aligned with OEM circular economy commitments represent the most actionable near-term growth opportunities.

Grupo Antolin, Motus Integrated Technologies, Toyota Boshoku, IAC Group, Lear Corporation, Howa, UGN, Hayashi Telempu, Freudenberg Performance Materials, and Borgers are the leading global participants.