- Automotive Components & Materials

- Ride-Hailing Taxi Market

Ride-Hailing Taxi Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Ride-Hailing Taxi Market by Service Type (E-Hailing, Ride Pooling / Shared Mobility, Micro-Mobility, Luxury / Premium Ride Services, Corporate / Business Ride Services), Trip Type (Intracity, Airport Transfers, Intercity Rides), Booking Mode (Mobile Application-Based Booking, Web-Based Booking), Vehicle Type (Four Wheeler, Two Wheeler, Others), and Regional Analysis for 2026 - 2033

Ride-Hailing Taxi Market Trends & Analysis

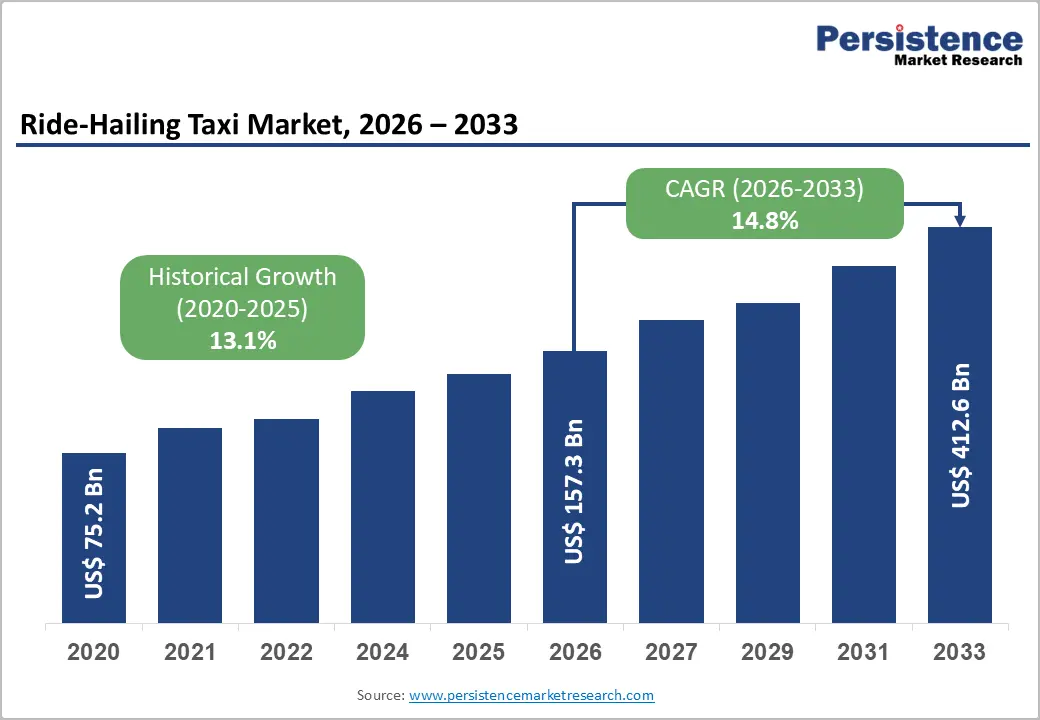

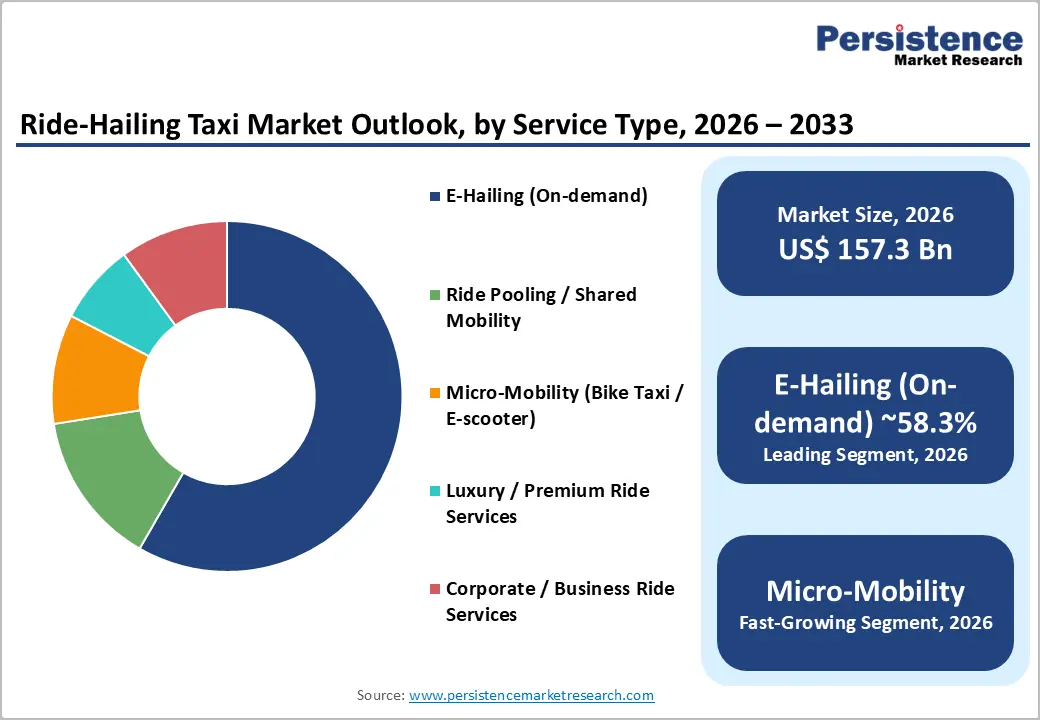

The global Ride-Hailing Taxi Market size is anticipated at US$ 157.3 billion in 2026 and is projected to reach US$ 412.6 billion by 2033, growing at a CAGR of 14.8% between 2026 and 2033.Traditional Taxi operations alongside digitally integrated app-based platforms, reflecting the progressive structural shift from conventional street-hail models toward technology-mediated on-demand mobility globally.

Rapid smartphone penetration driving app-based mobility adoption, urban population growth increasing demand for on-demand shared transportation, and EV fleet electrification programs by major platforms accelerating sustainable ride-hailing infrastructure are the primary growth catalysts. Regulatory frameworks formalizing ride-hailing operations across emerging markets are expanding the addressable driver and rider base structurally. Asia Pacific's digitally native urban population base is compounding platform volume growth through 2033.

Key Industry Highlights:

- Leading Service Type: E-Hailing leads service type at 58.3% share; Micro-Mobility grows fastest at 18.5% CAGR, driven by bike taxi and e-scooter integration on platforms across South and Southeast Asia.

- Leading Trip Type: Intracity rides lead trip type at 71.2% share; Intercity Rides grow fastest at 17.5% CAGR via BlaBlaCar and inDrive expansion across Africa, Central Asia, and Latin America.

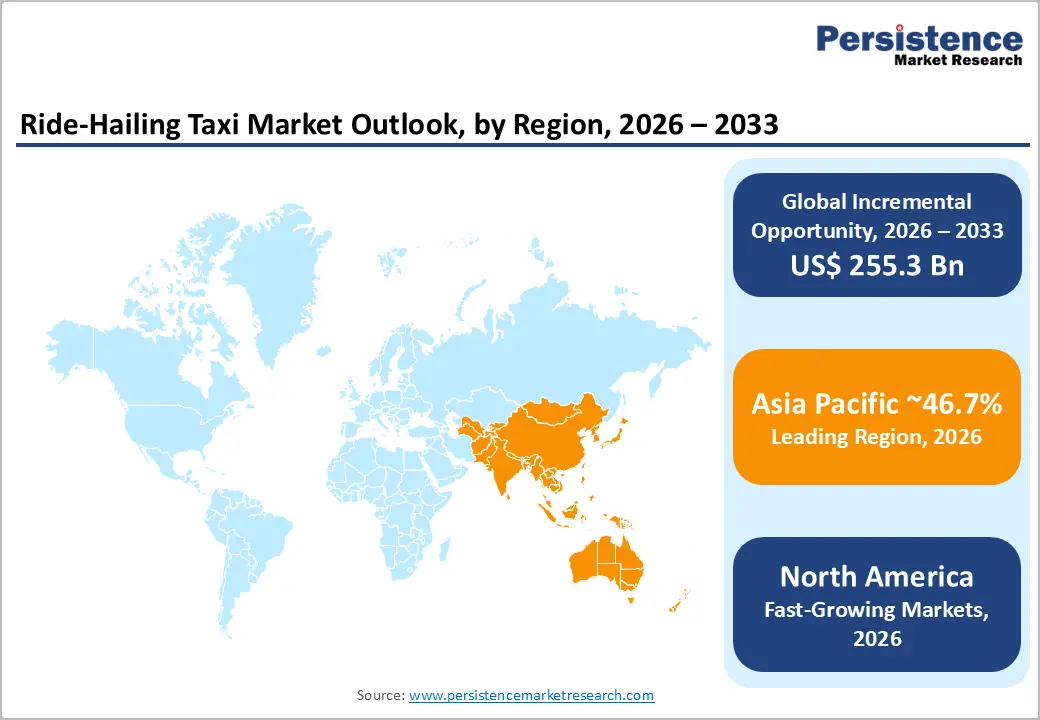

- Regional Leadership: Asia Pacific dominates at 46.7% share; China at US$ 34.2 Billion and India at US$ 18.5 Billion in 2026; North America holds 32.8% share with the U.S. at US$ 46.1 Billion.

- Uber-Waymo AV partnership expansion (March 2025) and Grab-BYD EV fleet integration (October 2024) are defining autonomous and electric ride-hailing competitive strategy globally.

Market Dynamics Analysis

Drivers - Rapid Urbanization and Smartphone Penetration Accelerating App-Based Mobility Adoption

Accelerating global urbanization, with the United Nations projecting 68% of the world's population residing in urban areas by 2050, is structurally expanding the addressable market for on-demand ride-hailing platforms that address last-mile urban mobility gaps unserved by conventional public transit systems. The GSMA Mobile Economy Report 2024 recorded 5.6 billion global smartphone users, representing a 69% global penetration rate, directly expanding the reachable population for app-based ride-hailing services across developed and emerging markets. Mobile internet access in South and Southeast Asia, Sub-Saharan Africa, and Latin America is progressively bringing first-time ride-hailing users onto platforms.

Uber's Q1 2025 results, reporting 3 billion trips and 28 million daily average trips, demonstrate the operating scale that sustained urbanization and smartphone adoption enable for platform leaders. India's urban population is projected to reach 600 million by 2030 (UN-Habitat), adding a structurally large addressable urban commuter base for domestic platforms, including Ola Cabs and inDrive. China's DiDi processed 30 million rides per day in Q1 2025, underscoring how urbanization and digital infrastructure investment in the Asia Pacific translate directly into platform transaction volume at scale. Urban congestion and parking constraints further structurally incentivize ride-hailing over private vehicle ownership among economically active urban millennials globally.

EV Fleet Electrification Programs and Sustainability-Driven Policy Frameworks

Major ride-hailing platforms are executing large-scale EV fleet transition programs in response to municipal zero-emission vehicle mandates, corporate sustainability commitments, and EV driver incentive programs, with Uber committing to 100% electric vehicles in the U.S., Canada, and Europe by 2030 and Lyft targeting full EV operations by the same deadline under its Clean Program initiative. The International Energy Agency's Global EV Outlook 2024 confirmed 17 million EV sales in 2023, with commercial ride-hailing fleet operators identified as a primary institutional EV procurement channel given predictable high-utilization operating profiles that optimize EV total cost of ownership relative to ICE vehicles.

London's Transport for London zero-emission taxi fleet mandate, requiring all new private hire vehicles to be fully electric from 2023, and New York City's Taxi and Limousine Commission EV incentive programs demonstrate the regulatory enforcement momentum embedding EV procurement requirements into ride-hailing platform driver economics globally. DiDi's EV rental program for drivers, Grab's Southeast Asia EV fleet initiative, and BYD's ride-hailing fleet supply partnerships collectively confirm EV-ride-hailing ecosystem convergence as a structural market driver. Platform EV programs reduce driver fuel expenditure by 40–60% versus ICE vehicles, improving driver net income economics and platform supply-side recruitment in high-utilization urban markets through 2033.

Restraints - Driver Classification Regulatory Disputes Creating Operational and Scaling Uncertainty

Ongoing legal disputes over gig worker classification, including the California AB5 law, the EU Platform Work Directive requiring employment status re-evaluation for gig workers, and equivalent legislation emerging across the U.K., Australia, and India, create structural compliance uncertainty for ride-hailing platforms operating driver-as-independent-contractor models. The EU Platform Work Directive, formally adopted in 2024, is projected to reclassify up to 5.5 million platform workers across Europe, imposing social contribution costs that could increase per-ride operational expenses by 15–25% across affected markets, directly pressuring platform economics and market expansion velocity.

Regulatory Caps and Licensing Restrictions Limiting Platform Supply Expansion

Municipal licensing caps on ride-hailing vehicle registrations, implemented in New York City (capping TNC vehicles at approximately 80,000 since 2018), London (Uber's licence suspension history under TfL), and multiple Asian cities, impose structural supply constraints that limit platform capacity expansion and create sustained surge pricing during peak demand periods. The European Court of Justice's ruling classifying Uber as a transport company rather than an information society service provider in multiple jurisdictions mandates compliance with local transport licensing frameworks, extending market entry timelines and increasing regulatory compliance burden across EU member states and precedent-following markets globally. Risk quantification: licensing delays in 3–5 new markets annually represent a collective US$ 2–4 Billion annual foregone revenue opportunity at platform scale.

Opportunities - Autonomous Vehicle Integration Transforming Ride-Hailing Unit Economics

The commercial deployment of autonomous vehicle (AV) ride-hailing services, pioneered by Waymo's commercial robotaxi operations in San Francisco, Phoenix, and Austin, generating over 200,000 weekly paid rides by 2025, represents the most structurally transformative opportunity in the ride-hailing market by eliminating driver labor costs that currently constitute 60–70% of platform per-ride operating expenditure. Uber's Waymo partnership for AV ride deployment on the Uber app in Austin and Atlanta, and Baidu's Apollo Go autonomous taxi commercial service processing over 1 million rides monthly across 11 Chinese cities, are demonstrating scalable AV ride-hailing commercial viability ahead of broad regulatory approval timelines.

The global autonomous vehicle market is projected to exceed US$ 600 Billion by 2030, with AV ride-hailing representing the leading commercial deployment pathway. AV integration in ride-hailing eliminates driver compensation, reducing per-ride marginal costs by an estimated 40–60%, creating the potential for ride fares competitive with or below private vehicle ownership costs and structurally expanding the addressable rider market. For ride-hailing platforms securing early AV fleet deployment agreements with Waymo, Cruise, and Chinese robotaxi operators, AV integration represents a decisive long-term competitive moat.

Micro-Mobility Integration and Multimodal Platform Expansion in Emerging Markets

Two-wheeler bike taxis and e-scooter integration within ride-hailing platforms are creating a high-growth sub-segment particularly suited to the congested urban traffic environments of South and Southeast Asia, where India's bike taxi market (Rapido, OlaAuto) and Indonesia's Gojek two-wheeler platform serve urban commuters at price points and traffic maneuverability inaccessible to four-wheeler ride-hailing models. India's bike taxi sector is estimated to serve 100+ million urban commuters annually with government frameworks progressively formalizing bike taxi operations across states following Rapido's 2024 licensing expansion across 15 Indian states.

Multi-modal Mobility-as-a-Service (MaaS) platform integration, connecting ride-hailing with public transit, bike sharing, and intercity rail ticketing within a single app interface, represents a US$ 40–60 Billion incremental revenue opportunity by 2030 for platforms successfully executing MaaS integration strategies. Grab's SuperApp model in Southeast Asia, integrating ride-hailing, food delivery, financial services, and public transit payments, demonstrates the commercial viability of multi-modal platform monetization, generating 3x higher average revenue per user versus standalone ride-hailing. This model provides a compelling blueprint for platform expansion in India, Africa, and Latin America.

Category-wise Analysis

Service Type Insights

E-Hailing (On-demand rides via app) leads the service type segment with a 58.3% share in 2026. E-hailing's dominant position reflects its foundational role as the original and highest-volume ride-hailing service model, delivering the most direct value proposition of immediate, app-dispatched personal transportation that displaced traditional taxi street-hail and phone dispatch models globally. Uber's 28 million daily rides and DiDi's 30 million daily China rides collectively demonstrate the transaction volume that mature e-hailing infrastructure sustains. Ride Pooling and Corporate Ride Services represent growing revenue categories, but neither approaches E-hailing's volume scale. Micro-Mobility is expanding rapidly from a lower base. E-hailing structural dominance will be maintained through 2033, reinforced by autonomous vehicle integration, enhancing cost efficiency.

Micro-Mobility (Bike Taxi / E-scooter integration) is the fastest-growing service type at 18.5% CAGR through 2033. Urban traffic congestion, price sensitivity in emerging markets, and integration of e-scooters and bike taxis on Grab, Gojek, Rapido, and Uber platforms in South and Southeast Asia are driving Micro-Mobility at an accelerating growth rate substantially exceeding all other service type segments.

Trip Type Insights

Intracity rides (Daily Commute, <15 km) lead the trip type segment estimated at 71.2% share in 2026. Intracity commutes represent the highest-frequency use case in ride-hailing, driven by daily urban workers substituting private vehicles or public transit commutes with on-demand app-based rides across major metropolitan areas globally. The density of urban populations, concentration of employment centers within city boundaries, and short-trip economics favoring ride-hailing over taxi alternatives structurally sustain intracity trip dominance across all major ride-hailing markets. Airport Transfers serve a predictable high-value niche, while Intercity Rides remain in early commercial scaling stages. Intracity leadership will persist through 2033, given continued urban population and commuter density growth in Asia Pacific, Africa, and Latin America.

Intercity Rides are the fastest-growing trip type at 17.5% CAGR through 2033. BlaBlaCar's intercity carpooling growth, InDrive's intercity fare-negotiation model expansion in Africa and Central Asia, and platform investments in intercity scheduled ride services filling gaps between urban ride-hailing and formal bus or rail alternatives are driving this rapidly expanding niche.

Booking Mode Insights

Mobile application-based booking dominates with a 90.4% share of the global Ride-Hailing Taxi Market in 2026. Mobile app booking's dominance reflects the foundational architecture of modern ride-hailing, built entirely on smartphone-mediated GPS dispatch, real-time driver matching, cashless payment processing, and user review systems that are structurally inaccessible through web or phone-based alternatives. The 5.6 billion global smartphone user base, mobile-first consumer behavior in Asia Pacific's two largest markets (China and India), and continuous UX investment by Uber, DiDi, and Grab in seamless in-app booking experiences entrench mobile app booking's overwhelming share. No meaningful share shift from mobile to web booking is expected through 2033 given smartphone penetration trajectories globally.

Web-Based Booking is the fastest-growing booking mode at 7.3% CAGR through 2033. Corporate travel management platform integrations, pre-scheduled ride booking for airport transfers, and accessibility-focused interfaces serving users without smartphone access are driving measured Web-Based Booking volume growth from its currently minimal share base.

Regional Insights

North America Ride-Hailing Taxi Market Share

North America holds a prominent 32.8% share of the global Ride-Hailing Taxi Market in 2025, underpinned by Uber and Lyft's dominant platform positions, world-leading per-capita ride-hailing spending, and AV commercial deployments positioning the region at the global technology frontier.

U.S. Ride Hailing Taxi Market: AV Innovation and TNC Platform Leadership

The U.S. market is estimated at ~US$ 46.1 billion in 2026, driven by Uber's market-leading platform volume, Lyft's urban operations, and AV ride-hailing scaling across Phoenix, San Francisco, and Austin under federal EV infrastructure investment via the Bipartisan Infrastructure Law and state TNC licensing frameworks in California, New York, and Illinois. Canada contributes to growing ride-hailing adoption across Toronto, Vancouver, and Montreal under provincial TNC licensing frameworks operational since 2017, with Waymo and Uber AV partnership investments sustaining regional innovation leadership globally.

Europe Ride-Hailing Taxi Market Trends

Europe is growing at a considerable 11.1% CAGR through 2033, driven by urban sustainability mandates compelling EV fleet transition, expanding MaaS integration with public transit systems, and intra-European penetration by Bolt, FREE NOW, and Uber following post-pandemic urban mobility recovery.

U.K. Ride Hailing Taxi Market: EV Transition and Multi-Modal Mobility Expansion

The U.K. market is estimated at ~US$ 5.0 billion in 2026, sustained by Uber's market-leading London position post-TfL licensing restoration, Bolt's competitive UK city expansion, and growing corporate ride service adoption across major business hubs. Germany and France are registering accelerated platform adoption under multi-modal urban mobility policies supporting ride-hailing as a public transit complement, while the EU Platform Work Directive, requiring gig worker reclassification across member states, represents the dominant regulatory risk shaping platform labor model adaptation and per-ride cost structures through 2033.

Asia Pacific Ride-Hailing Taxi Market Trends

Asia Pacific commands the dominant 46.7% share and fastest-growing regional market in 2026, driven by China's unparalleled DiDi platform volumes, India's 100+ million active ride-hailing users, and ASEAN's Grab and Gojek super-app ecosystems across 8 Southeast Asian countries.

China & India Ride Hailing Taxi Market: EV Fleet Electrification and Super-App Scale

China's market is estimated at US$ 34.2 billion in 2026, anchored by DiDi's 30 million daily rides and strong government EV ride-hailing fleet electrification support under its New Energy Vehicle mandate. India's market at ~US$ 18.5 billion is growing on urban commuter demand through Ola, Uber, and Rapido, supported by PLI scheme investment attracting EV manufacturer participation in ride-fleet supply chains. Japan and ASEAN markets sustain Grab's super-app monetization expansion, underpinned by the ASEAN digital economy projected at US$ 300 Billion by 2025 (Google-Temasek), through 2033.

Competitive Landscape

The global Ride-Hailing Taxi Market is moderately consolidated at the platform layer but highly fragmented regionally, with Uber holding 67.5% global brand share across 70 countries while facing strong regional incumbents, DiDi in China (30 million daily rides), Grab in Southeast Asia, and Ola in India, who collectively limit Uber's penetration in Asia Pacific's highest-growth markets. Differentiation centers on super-app ecosystem integration, AV partnership depth, and EV fleet transition scale.

Autonomous vehicle integration, EV fleet electrification, micro-mobility expansion, and emerging market geographic scaling define the dominant competitive strategic themes, with platforms investing in AV partnerships and multi-modal MaaS integration to capture long-term structural revenue growth while defending urban market positions against emerging regional challengers globally through 2033.

Key Developments:

- In September 2024, Uber Technologies Inc. and Waymo LLC expanded their partnership to launch fully driverless ride-hailing in Austin and Atlanta via the Uber app, with deployments beginning in March 2025, advancing scalable urban autonomous mobility operations.

- In January 2025, Grab Holdings Inc. partnered with BYD Company to deploy up to 50,000 electric vehicles across Southeast Asia, enabling large-scale fleet electrification, lowering driver costs, and accelerating sustainable ride-hailing adoption.

- In May 2024, Bolt Technology OÜ secured a €220 million credit facility to strengthen liquidity and prepare for a potential IPO, supporting strategic flexibility and expansion across its ride-hailing and shared mobility operations.

Companies Covered in Ride-Hailing Taxi Market

- Uber Technologies Inc.

- DiDi Global Inc.

- Grab Holdings Inc.

- Lyft Inc.

- ANI Technologies Pvt. Ltd. (Ola Cabs)

- Gojek (GoTo Group)

- Bolt Technology OÜ

- SUOL Innovations Ltd. (inDrive)

- Careem Networks FZ LLC

- BlaBlaCar

- FREE NOW (FREENOW)

- Cabify Spain SLU

- Yandex Go

- Addison Lee Group

- Wheely Technologies Ltd.

Frequently Asked Questions

The ride-hailing taxi market is valued at US$ 157.3 Billion in 2026, projected to reach US$ 412.6 Billion by 2033.

Rapid urbanization expanding app-based mobility demand, EV fleet electrification mandates, and autonomous vehicle commercial deployments reducing per-ride operating costs are the primary structural growth drivers.

The ride-hailing taxi market is projected to grow at a CAGR of 14.8% from 2026 to 2033.

Autonomous vehicle integration eliminating driver labor costs and micro-mobility and MaaS multi-modal platform expansion in emerging South and Southeast Asian markets represent the highest-value near-term growth opportunities.

Uber Technologies, DiDi Global, Grab Holdings, Lyft, Ola Cabs, Gojek, Bolt, inDrive, Careem, and BlaBlaCar are the leading global and regional platform participants.