- LED & Lighting (Optoelectronics)

- LED Backlight Driver Market

LED Backlight Driver Market Size, Share, and Growth Forecast 2026 - 2033

LED Backlight Driver Market by Supply Type (Constant Current, Constant Voltage), Luminaire Type (Type A Lamps/Bulbs, Decorative Lamps, T Lamps/Tubular, Reflectors, Integral Modules, Other Lamps), Application (General Lighting, Automotive Lighting, Backlighting, Other Applications), and Regional Analysis for 2026 - 2033

LED Backlight Driver Market Size and Trend Analysis

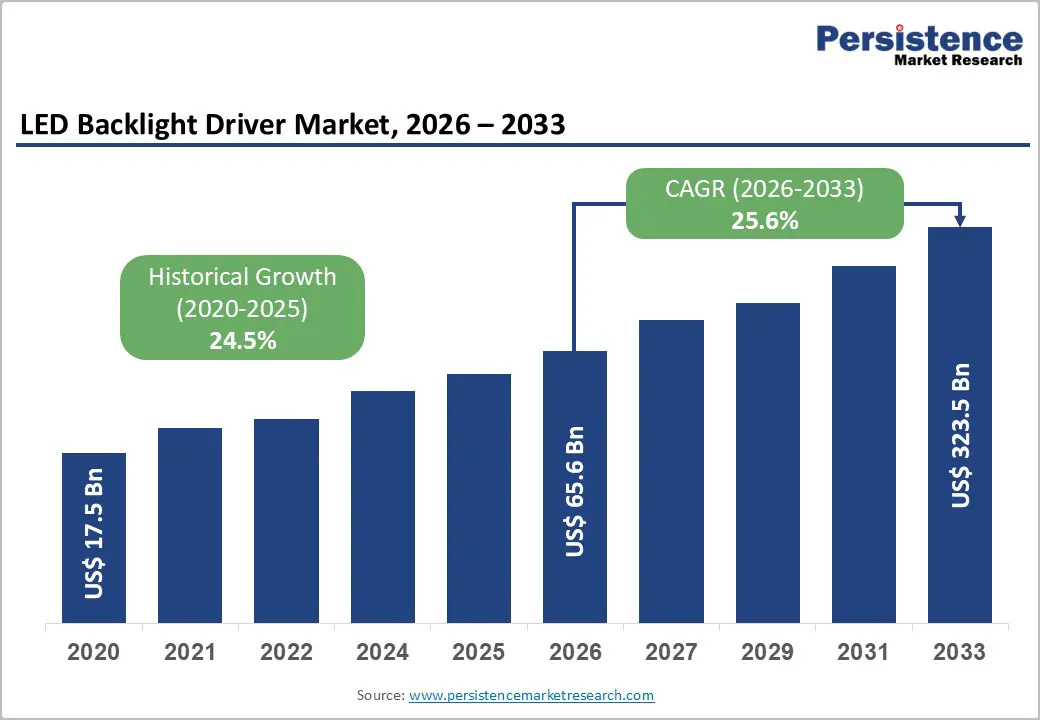

The global LED backlight driver market size is expected to be valued at US$ 65.5 billion in 2026 and is projected to reach US$ 323.5 billion by 2033, growing at a CAGR of 25.6% between 2026 and 2033.

This extraordinary growth trajectory is driven by the accelerating global replacement of traditional lighting infrastructure with LED-based systems, the proliferation of energy efficiency mandates across major economies, and surging demand for LED backlighting in consumer electronics, automotive displays, and smart lighting applications.

Key Industry Highlights:

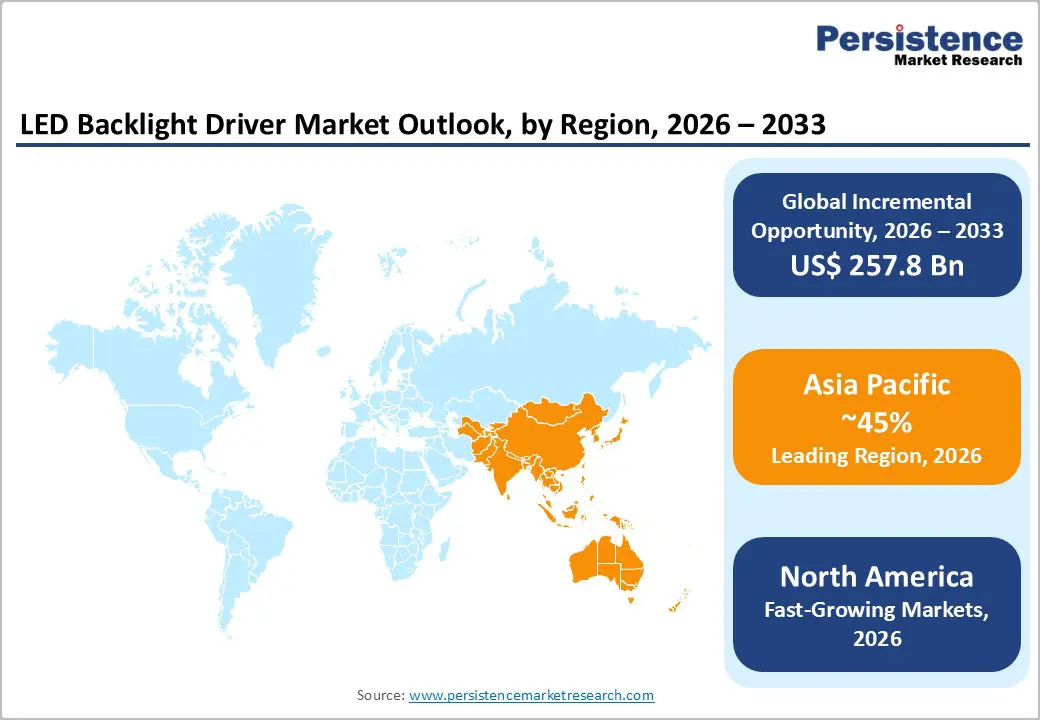

- Leading Region - Asia Pacific commands 45% of the global LED backlight driver market share in 2025, led by China's dominant LED manufacturing ecosystem, India's UJALA and SLNP government deployment programs, and Japan's advanced consumer electronics and automotive LED driver demand.

- Fastest-Growing Region - MEA is the fastest growing LED backlight driver region through 2026 - 2033, driven by Gulf Cooperation Council smart city LED street lighting programs, UAE and Saudi Arabia Vision 2030 building efficiency mandates, and rapid LED adoption across Sub-Saharan Africa's expanding urban infrastructure.

- Dominant Supply Segment - Constant-current LED drivers hold 68% market share in 2025, driven by LEDs' fundamental current-driven nature, with IEC 62384 and ENERGY STAR standards specifically mandating constant-current regulation for reliable lumen output, color consistency, and extended LED lifespan.

- Fastest-Growing Segment - Automotive lighting is the fastest-growing application, driven by Euro NCAP matrix LED headlight testing from 2024, 32-84 addressable LED segments per ADB headlight system, and expanding in-vehicle infotainment display backlighting requiring AEC-Q100-qualified multichannel driver ICs.

- Key Market Opportunity - Intelligent LED drivers integrating DALI-2, Bluetooth Mesh, and Zigbee connectivity can reduce commercial building energy use by an additional 40-50% per U.S. DOE estimates, commanding significant price premiums and representing the highest-margin growth segment through 2033.

DRO Analysis

Drivers - Global LED Lighting Transition and Regulatory Phase-Out of Inefficient Light Sources

The worldwide legislative phase-out of incandescent and halogen lamps is the most powerful structural driver of LED backlight driver demand. The European Union completed the ban on most halogen lamps under Regulation (EU) 2019/2020 as part of its Ecodesign Directive, while the U.S. Department of Energy (DOE) enacted rules under the Energy Policy Act that effectively phase out incandescent bulbs.

The International Energy Agency (IEA) estimates that LED lighting now accounts for over 50% of global lighting sales, with the share projected to exceed 80% by the end of the decade. Each LED luminaire installation, from a single retrofit bulb to a multi-zone smart commercial lighting system, requires one or more LED driver circuits to regulate current and voltage, creating a direct and proportional demand relationship between LED penetration rates and driver market growth.

Explosive Growth of LED Displays in Consumer Electronics, Automotive, and Digital Signage

The global proliferation of LED-backlit displays across smartphones, tablets, laptops, televisions, automotive infotainment systems, and large-format digital signage is driving massive incremental demand for LED-backlight driver ICs. According to the Consumer Electronics Association (CTA), global consumer electronics shipments remain in the billions of units annually, with virtually all modern display-equipped devices utilizing LED backlighting.

The automotive sector is a particularly dynamic growth vector. The Society of Automotive Engineers (SAE) reports that the average modern vehicle incorporates 10-20 or more LED-driven display and lighting zones. The rapid adoption of mini-LED and micro-LED backlighting technologies in premium televisions and monitors, as pursued by Apple Inc., Samsung Electronics, and LG Electronics, demands significantly more sophisticated multi-channel LED backlight driver ICs, driving higher ASPs and revenue growth.

Restraints - Design Complexity and Thermal Management Challenges at High Power Densities

As LED driver ICs are required to operate at increasingly high power densities in compact form factors, particularly for automotive, industrial, and high-brightness display applications, thermal management and electromagnetic interference (EMI) compliance pose significant design barriers.

Meeting IEC 61000 EMC standards and ENERGY STAR efficiency requirements simultaneously while shrinking driver footprints adds engineering complexity and development cost. These challenges extend design cycles, increase NRE (non-recurring engineering) costs for OEMs, and can limit the pace of adoption in cost-sensitive consumer segments where simpler, lower-cost driver topologies are preferred.

Supply Chain Vulnerabilities and Semiconductor Shortages Impacting Driver IC Availability

The global semiconductor supply chain disruption of 2020-2022 exposed the vulnerability of LED driver IC availability to broader constraints on chipmaking capacity. LED driver ICs, typically manufactured on mature 0.18-0.35 µm CMOS process nodes, compete for fab capacity with a wide range of analog and mixed-signal chips.

During peak shortage periods, lead times for driver ICs extended to 52 weeks or more, according to IPC's supply chain assessment reports, disrupting lighting OEM production schedules and causing project delays. While the acute shortage has eased, structural capacity constraints on mature nodes remain a medium-term risk for the supply chain.

Opportunities - Smart and Connected Lighting: The Convergence of LED Drivers with IoT and DALI/Wireless Protocols

The transition from simple LED current regulation to intelligent, networked lighting control systems represents the most significant value-creation opportunity in the LED backlight driver market. Smart LED drivers integrating DALI-2 (Digital Addressable Lighting Interface), Bluetooth Mesh, Zigbee, and Thread connectivity enable granular dimming, occupancy-responsive control, daylight harvesting, and integration with building management systems.

The U.S. DOE's Connected Lighting Systems program estimates that networked LED lighting can reduce commercial building energy consumption by an additional 40% beyond the baseline savings from simple LED replacement. Companies including Texas Instruments, Inc., On Semiconductor and Rohm Semiconductors are developing highly integrated smart driver SoCs that combine power management, wireless connectivity, and sensor interfaces, commanding significant price premiums over commodity drivers.

Automotive LED Driver Opportunity: ADAS, Matrix Headlights, and Interior Display Expansion

The automotive sector presents the highest-margin, highest-growth application for LED backlight and lighting drivers, driven by the rapid proliferation of adaptive driving beam (ADB) matrix headlight systems, ambient interior lighting, and multi-zone infotainment display backlighting. The European New Car Assessment Program (Euro NCAP) introduced matrix LED headlight performance testing from 2024, incentivizing automakers to accelerate adoption.

Each ADB headlight system may contain 32-84 individually addressable LED segments, each requiring a dedicated multichannel driver IC. Texas Instruments, Inc. and Rohm Semiconductors offer automotive-grade (AEC-Q100-qualified) LED driver families specifically designed for matrix headlight and display backlight applications. As global EV and premium vehicle production grow, automotive LED driver content per vehicle is expanding significantly, offering a structurally superior growth vector compared to general illumination applications.

Category-wise Analysis

Supply Type Insights

Constant current LED drivers represent the dominant Supply Type segment, accounting for approximately 68% market share in 2025. Constant current drivers are the preferred topology for most LED lighting applications because LEDs are fundamentally current-driven devices; their luminous output and colour temperature are directly governed by the forward current rather than applied voltage. A constant-current driver precisely regulates current regardless of load-voltage variations caused by temperature changes, binning differences, or aging, ensuring consistent lumen output and an extended LED lifespan.

Texas Instruments, Inc., Maxim Integrated, and Macroblock, Inc. offer extensive constant-current driver portfolios spanning single-string to multi-channel architectures for applications ranging from residential bulbs to high-power industrial floodlights. ENERGY STAR and IEC 62384 performance standards specifically address constant current driver specifications, reinforcing their design dominance.

Luminaire Type Insights

Integral Modules represent the leading Luminaire Type segment in terms of revenue contribution, accounting for approximately 34% market share in 2025. Integral LED modules, where the LED array, driver, and thermal management are designed as a single optimized unit, are increasingly preferred by lighting OEMs for commercial downlights, troffer luminaires, streetlights, and high-bay fixtures because they enable superior photometric performance, longer system lifetimes, and more compact form factors.

The Zhaga Consortium, a global standards body for LED light engine interfaces, has standardized integral module footprints enabling interchangeable LED modules and drivers across manufacturers. Cree Inc. and Osram GmbH have established strong positions in the integral module segment, with products meeting DLC (Design Lights Consortium) qualification requirements for commercial energy rebate eligibility.

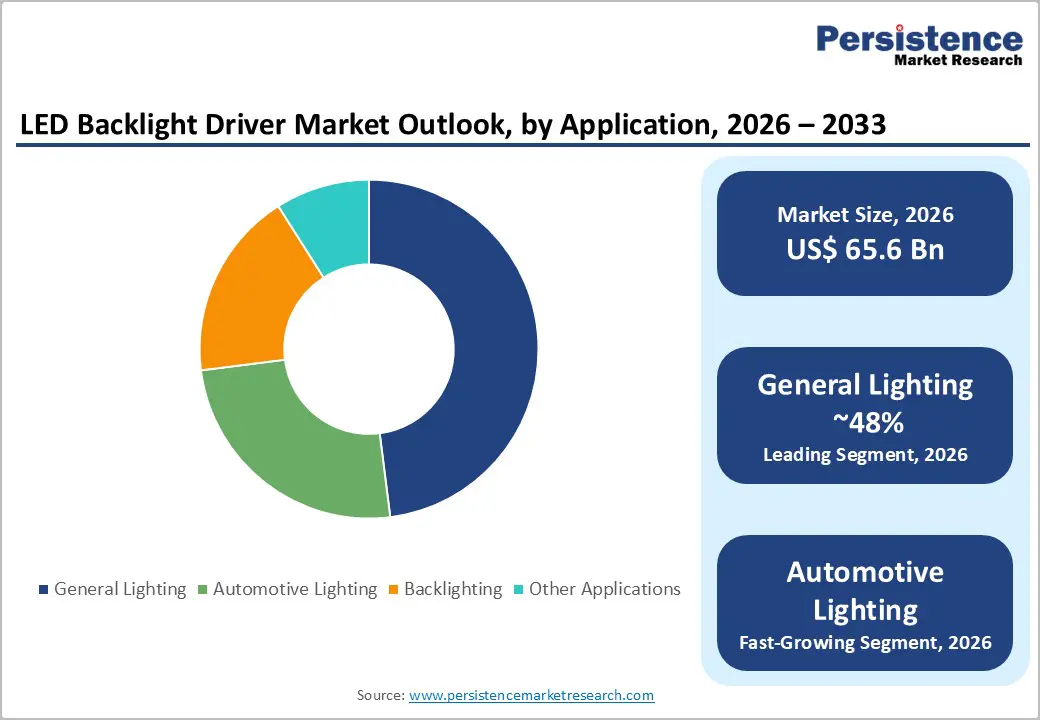

Application Insights

General Lighting is the dominant Application segment, accounting for approximately 48% of the total LED backlight driver market share in 2025. The global replacement of billions of installed incandescent, fluorescent, and halogen lamps with LED-based systems has created the world's largest single application category for LED drivers. According to the IEA, there are approximately 20 billion light points globally, with LED penetration continuing to grow rapidly across both residential and commercial lighting.

Government programs such as India's UJALA scheme, which distributed over 360 million LED bulbs, and China's Energy Efficiency Subsidy Programs for LED lighting have demonstrated how policy-driven replacement programs can mobilize hundreds of millions of driver unit deployments in short timeframes, reinforcing General Lighting's position as the foundational demand pillar for the LED driver market.

Regional Analysis

North America LED Backlight Driver Market Trends & Analysis

North America is a mature, technologically advanced LED backlight driver market driven by commercial building lighting upgrades, stringent energy codes under ASHRAE 90.1 and California Title 24, and strong automotive LED adoption. The U.S. DOE estimates that LED lighting now accounts for the majority of U.S. commercial and industrial installations, with the retrofit market for smart connected drivers growing fastest. The region's consumer electronics and automotive industries sustain high-value display backlight driver demand.

U.S. LED Backlight Driver Market Size

The United States accounts for approximately 79% of the North America LED backlight driver market revenue in 2025. Driven by energy code compliance for commercial buildings, DOE ENERGY STAR incentives, and the world's largest consumer electronics and automotive markets, the U.S. is the single largest national market outside Asia for LED driver ICs. Texas Instruments, Inc., ERP Power LLC, and On Semiconductor are among the key domestic driver technology providers.

Europe LED Backlight Driver Market Trends, Drivers & Insights

Europe's LED backlight driver market is structurally driven by the EU Ecodesign Directive, Energy Labeling Regulation, and the Green Deal mandating building energy renovation. The halogen phase-out has accelerated retrofit demand, while smart building regulations in countries such as Germany, France, and the Netherlands are mandating connected driver specifications for new commercial construction. Automotive LED driver demand is supported by the region's concentration of premium automakers.

Germany LED Backlight Driver Market Size

Germany holds approximately 23% of the European LED backlight driver market in 2025. Germany's combination of world-class automotive manufacturing with BMW, Mercedes-Benz, and Volkswagen driving advanced matrix headlight and interior display LED adoption and stringent EnEV/GEG building energy standards ensuring commercial LED retrofit demand, makes it the region's most valuable national market. Osram GmbH's headquarters in Munich further reinforces Germany's depth in the driver ecosystem.

U.K. LED Backlight Driver Market Size

The United Kingdom represents approximately 14% of the European LED backlight driver market in 2025. The UK's Building Regulations Part L energy efficiency requirements and BEIS energy efficiency programs are driving commercial LED adoption. The UK's active consumer electronics retail market and strong automotive component manufacturing base, including Jaguar Land Rover's LED system procurement, sustains multi-channel display and automotive driver demand.

France LED Backlight Driver Market Size

France accounts for approximately 11% of the European LED backlight driver market revenue in 2025. France's RT2020 building standard, which mandates near-zero-energy new construction, is driving LED specification in commercial and residential projects. The country's active smart city programs in Paris, Lyon, and other municipalities, converting street lighting to connected LED systems requiring advanced driver controls, are supplementary demand drivers alongside the broader residential retrofit market.

Asia Pacific LED Backlight Driver Market Drivers & Analysis

Asia Pacific dominates global LED backlight driver consumption, accounting for approximately 45% of the market in 2025, driven by China's dominant LED manufacturing ecosystem and massive domestic deployment programs. China alone accounts for over 45% of global LED production and consumption, according to China Solid State Lighting Alliance (CSA) data, with domestic driver IC manufacturers, including Macroblock, Inc., serving large production volumes. India, Japan, and Southeast Asia collectively represent rapidly expanding LED driver demand markets, each driven by distinct policy and demand factors.

China LED Backlight Driver Market Size

China holds approximately 53% of the Asia Pacific LED backlight driver market revenue in 2025, making it the world's largest single national market. Government programs, including China's 14th Five-Year Plan energy efficiency targets and municipal LED street lighting rollouts across tier-1 and tier-2 cities, have driven hundreds of millions of driver unit deployments. China is simultaneously the world's largest LED driver IC manufacturer, with domestic players serving both domestic and global export markets.

India LED Backlight Driver Market Size

India represents approximately 14% of Asia Pacific LED backlight driver market revenue in 2025. India's UJALA scheme, distributing over 360 million LED bulbs through the Energy Efficiency Services Limited (EESL)has been one of the world's largest LED deployment programs, directly driving driver demand at scale. India's Street Lighting National Programme (SLNP), converting 13 million streetlights to LED, and growing smartphone and consumer electronics manufacturing, further accelerate driver market expansion.

Japan LED Backlight Driver Market Size

Japan contributes approximately 12% of Asia Pacific LED backlight driver market revenue in 2025. Japan's advanced consumer electronics industry, home to Sony, Sharp, and Panasonic, drives premium display backlight driver demand for televisions, monitors, and mobile devices. Japan's Top Runner Program energy efficiency standards mandate LED adoption in lighting products, sustaining structural retrofit driver demand alongside Japan's active automotive LED component supply chain.

Competitive Landscape

The global LED backlight driver market exhibits a moderately fragmented competitive structure, with established semiconductor majors including Texas Instruments, Inc., On Semiconductor, and Rohm Semiconductors competing alongside specialized LED driver IC providers like Macroblock, Inc., Maxim Integrated, and ERP Power LLC.

Key differentiators include power conversion efficiency (90%+ efficiency benchmarks per IEC 62384), integration of wireless connectivity for smart lighting, AEC-Q100 automotive qualification, and breadth of current/voltage range coverage. R&D trends centre on GaN-based driver power stages, single-stage PFC topologies, and AI-optimized dimming algorithms. Direct OEM supply agreements and reference design ecosystems are dominant go-to-market strategies for market leaders.

Key Developments:

- In March 2025, Texas Instruments, Inc. released the TPS92520-Q1 dual-channel automotive LED matrix driver IC with integrated diagnostics and AEC-Q100 Grade 1 qualification, targeting adaptive driving beam (ADB) headlight applications in electric and hybrid vehicles.

- In October 2024, On Semiconductor launched its NCP5397B multi-string LED backlight driver for large-format mini-LED television panels, featuring precision current balancing across 16 independent strings and integrated fault detection for premium display OEM customers.

LED Backlight Driver Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 11.6 Bn |

| Current Market Value (2026) | US$ 323.5 Bn |

| Projected Market Value (2033) | US$ 65.5 Bn |

| CAGR (2026 - 2033) | 25.6% |

| Leading Region | Asia Pacific, 45% share |

| Dominant Application | General Lighting, 48% share |

| Top-ranking Product | Integral Modules, 34% |

| Incremental Opportunity | US$ 257.8 Bn |

Companies Covered in LED Backlight Driver Market

- Philips N.V. (Signify)

- Osram GmbH

- Texas Instruments, Inc.

- Maxim Integrated, Inc.

- Macroblock, Inc.

- Cree Inc.

- Rohm Semiconductors

- On Semiconductor (onsemi)

- ERP Power LLC

- General Electric

- STMicroelectronics

- Infineon Technologies AG

Frequently Asked Questions

The global LED backlight driver market is projected to reach US$ 323.5 billion by 2033, growing from an estimated US$ 65.5 billion in 2026 at a CAGR of 25.6%. This exceptional growth reflects the accelerating global LED lighting transition, the proliferation of LED-backlit consumer electronics and automotive display systems, and the rapid adoption of smart connected driver technologies with DALI-2 and wireless protocol integration.

Primary demand drivers include the mandatory phase-out of incandescent and halogen lamps under the EU Ecodesign Directive and U.S. Energy Policy Act, with the IEA reporting LED's share of global lighting sales exceeding 50% and targeting 80% by end of decade.

Constant current LED drivers are the dominant supply type, holding approximately 68% market share in 2025. Their dominance reflects LEDs' fundamental current-driven nature, where forward current not voltage governs lumen output and colour temperature.

Asia Pacific leads the global LED backlight driver market with approximately 45% market share in 2025, primarily driven by China which accounts for ~53% of Asia Pacific demand through its world-dominant LED manufacturing ecosystem and government deployment programs per China Solid State Lighting Alliance (CSA) data.

Key companies include Texas Instruments, Inc., Osram GmbH, Cree Inc., On Semiconductor (onsemi), Rohm Semiconductors, Maxim Integrated, Inc., Macroblock, Inc., Philips N.V. (Signify), ERP Power LLC, STMicroelectronics, Infineon Technologies AG, and Monolithic Power Systems (MPS).