- Aerospace & Defense

- Jet Engine Market

Jet Engine Market Size, Share, and Growth Forecast 2026 - 2033

Jet Engine Market by Engine Type (Turbojet Engines, Turbofan Engines, Turboprop Engines, Turboshaft Engines, Ramjet & Scramjet Engines), Aircraft Type (Commercial Aircraft, Military Aircraft, Business Jets, Regional Aircraft, Helicopters, Unmanned Aerial Vehicles), Technology (Conventional Engines, Hybrid-Electric Propulsion, Others), End-user (OEM, MRO, Defense Organizations), and Regional Analysis, 2026 - 2033

Jet Engine Market Size and Trend Analysis

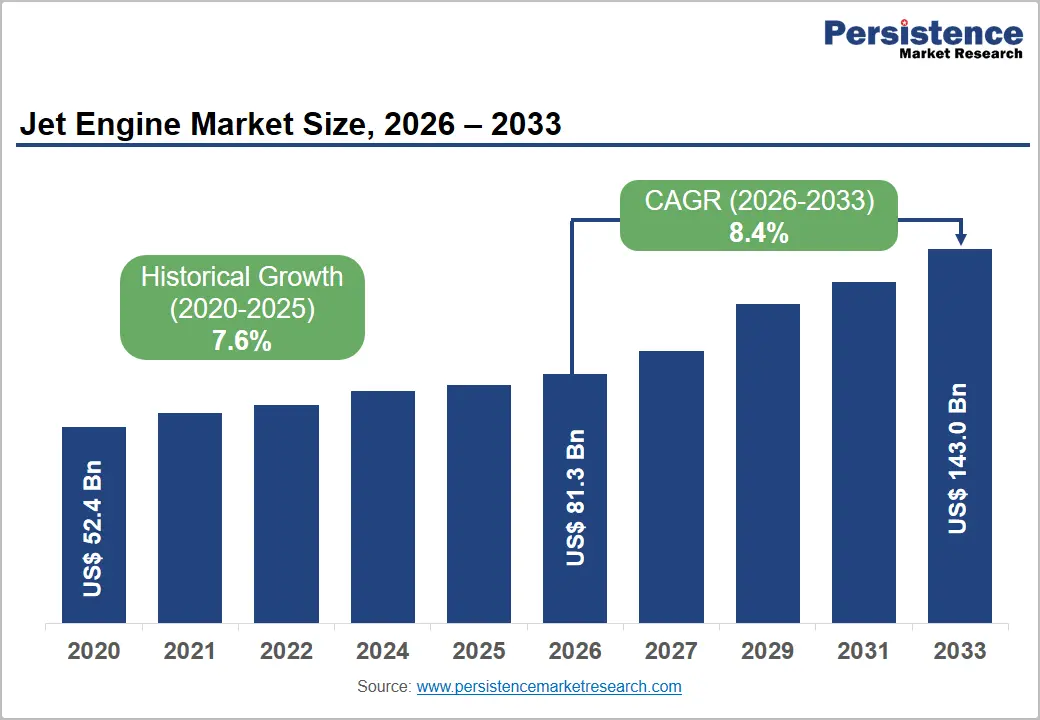

The global jet engine market size is expected to be valued at US$ 81.3 billion in 2026 and projected to reach US$ 143.0 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

The expansion is propelled by a steep rebound in global air travel, with the International Air Transport Association (IATA) reporting that worldwide revenue passenger kilometres surpassed pre-pandemic 2019 levels in 2024 and projecting passenger numbers to reach 5.2 billion in 2025. This traffic surge has triggered record backlogs at Boeing and Airbus, together exceeding 14,400 aircraft, while defense modernization budgets and accelerated adoption of next-generation propulsion architectures are reinforcing the order pipeline through the forecast window.

Key Industry Highlights:

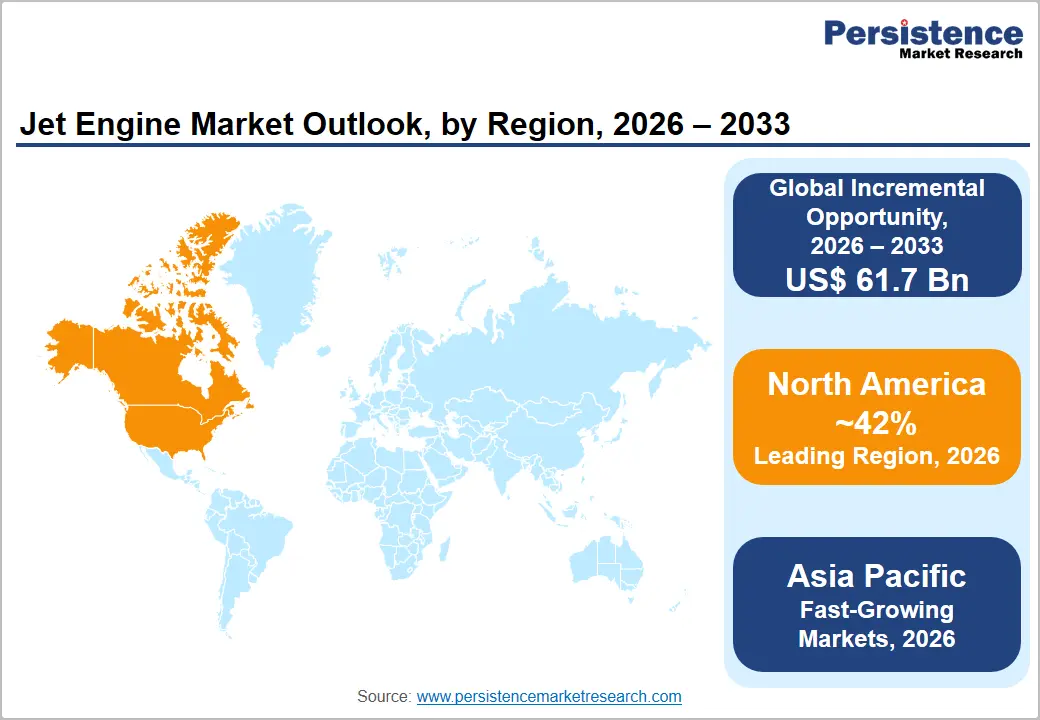

- Leading Region: North America leads the global jet engine market with a 42% share in 2025, anchored by GE Aerospace, Pratt & Whitney, FAA-driven certification leadership, and unmatched U.S. defense propulsion spending.

- Fastest Growing Market: Asia Pacific is the fast-growing region at a CAGR of 10.6% propelled by China's domestic aviation surge, India's 1,000-plus aircraft orders, and regional sixth-generation fighter programmes.

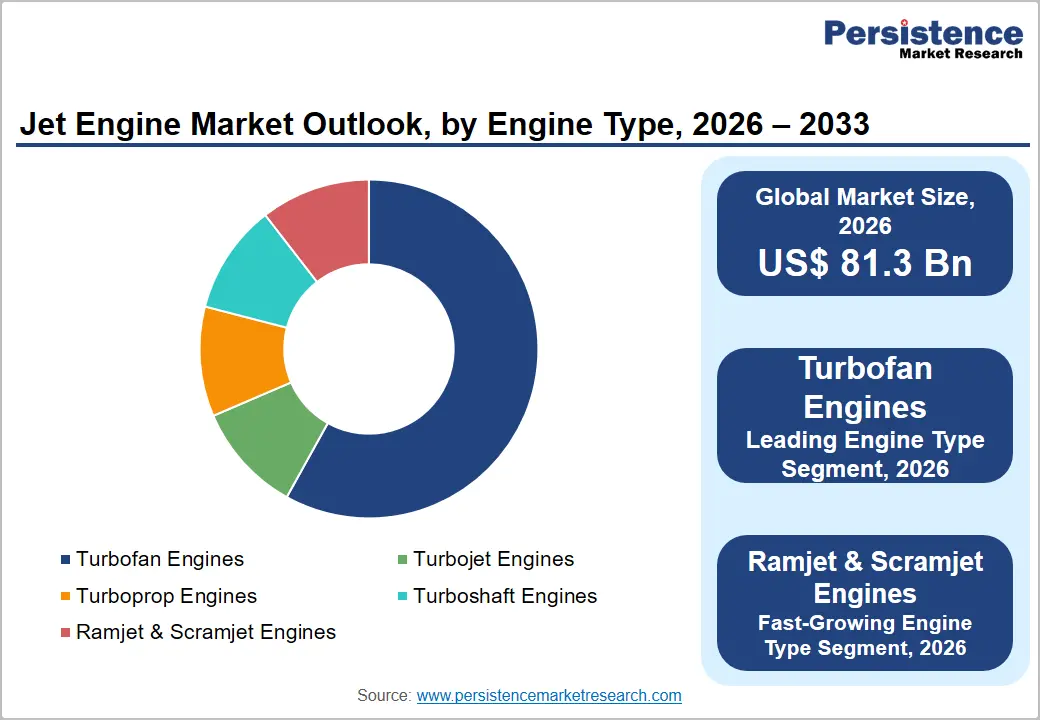

- Dominant Engine Type: Turbofan engines are likely to dominate with 62% share in 2026, underpinned by their near-monopoly on commercial narrow-body and wide-body propulsion across the Boeing-Airbus combined 14,400-aircraft backlog.

- Fast-Growing Technology: Hybrid-electric propulsion is the fastest-growing technology segment at an 18.5% CAGR, driven by NASA's EPFD funding, EASA's VTOL certification framework, and regional aircraft electrification pilots.

- Key Opportunity: The MRO super-cycle is the headline opportunity: aging 29,000-aircraft global fleet plus delayed new-build deliveries are extending engine service lives, creating multi-decade aftermarket annuity revenue.

Market Dynamics

Drivers - Surging Commercial Aircraft Deliveries Anchoring Long-Cycle Demand

For propulsion suppliers, this driver translates into a decade-long visibility on production line utilization that few capital-goods sectors can claim. Airbus delivered 766 aircraft in 2024 and is targeting roughly 820 aircraft in 2025, while Boeing is ramping its 737 MAX line back to 38 units per month under U.S. Federal Aviation Administration (FAA) oversight. Because every narrow-body airframe requires two engines plus a robust spares pool, this backlog mechanically pulls forward demand for CFM International LEAP and Pratt & Whitney GTF shipments, and it sets the strategic floor for aftermarket revenue accruing to engine OEMs over the next 15 to 20 years.

Defense Modernization and Sixth-Generation Programs Lifting Military Propulsion Spend

For defense propulsion incumbents, this driver re-centres the competitive battleground on adaptive-cycle and hypersonic capability rather than pure thrust-to-weight optimization. The U.S. Department of Defense enacted a base budget of US$ 849.8 billion for fiscal year 2025 with sustained funding for the F-35 and the Next Generation Air Dominance (NGAD) programme, while NATO members crossed the 2% of GDP defense-spending floor on average for the first time in 2024.

The resulting awards to Pratt & Whitney, GE Aerospace and Rolls-Royce Holdings for engine cores, lift fans and adaptive-cycle demonstrators are reshaping R&D allocation and pulling forward dual-use technology that will eventually migrate into the commercial aviation segment.

Restraints - Tightening Sustainable Aviation Mandates Pressuring Engine Economics

For market participants, the binding nature of these mandates converts a long-running narrative into immediate engineering and capital-allocation risk. The European Union's ReFuelEU Aviation regulation requires fuel suppliers to blend a minimum of 2% sustainable aviation fuel (SAF) from 2025, climbing to 70% by 2050, while the International Civil Aviation Organization (ICAO) CORSIA scheme entered its mandatory phase in 2027. Because SAF currently trades at three to five times conventional jet fuel prices and global supply remains under 1% of aviation fuel demand, airlines are intensifying pressure on engine OEMs to deliver double-digit specific fuel consumption improvements, compressing development timelines and elevating warranty and durability exposure.

Supply Chain Fragility and Critical Material Constraints

This restraint is squeezing margins and delivery cadence at precisely the moment the order book demands maximum throughput. Castings, single-crystal turbine blades, titanium forgings and rare-earth elements remain concentrated in a small set of qualified suppliers, and the U.S. Geological Survey notes that the United States imported over 95% of its rare-earth compound requirements between 2020 and 2023, with China supplying the majority. Compounding this, Pratt & Whitney's PW1100G powder-metal contamination issue led to extensive inspections of more than 3,000 GTF engines through 2026, resulting in record AOG (aircraft-on-ground) levels and underlining how a single material defect can cascade into multi-billion-dollar charges across the value chain.

Opportunities - Hybrid-Electric and Hydrogen Propulsion Reshaping the Regional and UAV Segment

The window for capturing first-mover position in sub-100-seat clean-sheet propulsion is narrow and time-sensitive, opening over the 2026 to 2032 horizon as certification frameworks mature. The European Union Aviation Safety Agency (EASA) issued its first special condition for VTOL aircraft propulsion in 2023, while NASA's Electrified Powertrain Flight Demonstration project is jointly funding hybrid-electric demonstrators with GE Aerospace and magniX.

Established turboshaft and turboprop incumbents such as Safran Aircraft Engines, Pratt & Whitney Canada and Rolls-Royce are best positioned to monetize this transition because they own the gas-turbine cores that hybrid architectures still require. This convergence also unlocks adjacent demand in the broader aerospace and defense market, where electrified accessory systems and distributed propulsion will redefine certification standards within the decade.

Aftermarket and MRO Super-Cycle Driven by Aging Fleets and Engine Retrofits

For aftermarket-led franchises, the next eight years represent a structurally favourable demand pocket that rewards scale, digital diagnostics and parts-pool depth. IATA data indicates that the global commercial fleet exceeds 29,000 aircraft with average operating age above 12 years, and delayed new-build deliveries are forcing operators to extend service life on legacy CFM56, V2500 and PW2000 engines well past original retirement schedules.

MTU Aero Engines reported MRO revenues rising 31% year-on-year in 2024, while Lufthansa Technik added new GTF and LEAP shop capacity through 2026. Players investing now in additive-manufactured repairs, predictive analytics and on-wing services will lock in 15-to-20-year revenue annuities, comparable in scale to opportunities in the adjacent commercial aircraft MRO market.

Category-wise Analysis

Engine Type Insights

Turbofan engines command roughly 62% of the global jet engine market in 2026, supported by their dominant role in commercial narrow-body and wide-body aircraft propulsion. Their leadership is deeply structural, as aircraft platforms such as the Airbus A320neo, Boeing 737 MAX, Boeing 787, and Airbus A350 all depend on high-bypass turbofan technology supplied by major global engine manufacturers. The combined order backlog of more than 14,400 aircraft from Airbus and Boeing continues to reinforce long-term turbofan demand and production visibility through the forecast period.

At the same time, ramjet and scramjet engines are emerging as the fastest-growing segment, projected to expand at a CAGR of approximately 12.6% through 2033. Growth is being driven by rising investments in hypersonic missile development programs by the U.S. Department of Defense, India’s DRDO, and China’s military modernization initiatives.

Aircraft Type Insights

Commercial aircraft accounts for approximately 48% of jet engine demand in 2026, reflecting the sheer scale of the global airline fleet and its replacement cycle. IATA projects passenger demand to grow at a long-term CAGR of 3.6% through 2043, and with airlines retiring older A320ceo and 737NG variants, every new-generation delivery converts directly into two turbofan units plus spares, sustaining the leadership of this segment. Unmanned Aerial Vehicles (UAVs) represent the fastest-growing aircraft category at an estimated CAGR of 11.8% between 2026 and 2033, as lessons from the Ukraine and Red Sea conflicts accelerate procurement of jet-powered loitering munitions and high-altitude long-endurance platforms across NATO, Middle Eastern and Indo-Pacific defense ministries.

Technology Insights

Conventional engines are likely to register a dominant 88% share of the jet engine market in 2026, a reflection of certification inertia and the fact that virtually every aircraft entering service today still relies on kerosene-fuelled gas-turbine cores. Type certification with the FAA and EASA typically requires seven-to-ten years for novel architectures, anchoring conventional propulsion as the default selection for the current order book.

Hybrid-electric propulsion, by contrast, is the fastest-growing technology bucket at a projected CAGR of nearly 18.5% through 2033, supported by NASA's EPFD investments, Safran's ENGINeUS programme and dozens of advanced air mobility prototypes targeting the regional and short-haul commuter segments where the propulsion energy budget makes electrification technically viable.

End-user Insights

OEM-channel sales constitute about 55% of the jet engine market in 2026, anchored by record airframer build rates and multi-year defense procurement contracts. The OEM channel benefits from long-cycle visibility, the average commercial engine programme runs 20-to-25 years from launch to retirement, and from bundled service agreements that increasingly tie initial engine sales to long-term aftermarket commitments.

MRO is the fast-growing end-user category at an estimated CAGR of 9.7%, as the global commercial fleet of more than 29,000 aircraft ages and delayed new-build deliveries force airlines to extend service life on legacy engines through additional shop visits and life-extension programs.

Regional Insights

North America Jet Engine Market Trends and Insights

North America leads the global jet engine market with a 42% share in 2026, anchored by an unmatched concentration of propulsion OEsMs, MRO infrastructure and defense procurement budgets. The region hosts GE Aerospace, Pratt & Whitney, Honeywell Aerospace and Williams International, supported by deep institutional R&D from NASA and the U.S. Department of Defense. Looking forward, hypersonic propulsion and the NGAD adaptive-cycle programme will reinforce the region's technology premium and keep North America at the apex of the propulsion value chain through 2033.

U.S. Jet Engine Market Size

The United States accounts for roughly 90% of North American jet engine demand in 2026 sustained by the U.S. Department of Defense's US$ 849.8 billion 2025 budget, F-35 sustainment contracts and Boeing's 737 MAX recovery to 38 units per month. The country's combined OEM and defense propulsion ecosystem is unrivalled. Looking forward, NGAD engine awards and accelerated SAF blending mandates will keep U.S. propulsion R&D investment compounding through the forecast window.

Europe Jet Engine Market Trends and Insights

Europe accounts for an estimated 27% of the global market in 2026, shaped by Airbus's ramp-up to 75 A320-family aircraft per month by 2027 and the strict decarbonization framework imposed by the European Union's ReFuelEU Aviation regulation. Core OEMs Rolls-Royce, Safran Aircraft Engines and MTU Aero Engines anchor the regional supply chain, while sixth-generation fighter programmes such as FCAS and GCAP are reshaping defense demand. The region is heading towards a propulsion landscape defined by sustainability compliance and trans-European programme consolidation.

Germany Jet Engine Market Size

Germany is likely to represent approximately 22% of the Europe jet engine market in 2026, led by MTU Aero Engines with revenues of around €7.5 billion in 2024, growing on the back of the V2500 and GTF programmes. Lufthansa Technik's expansion of GTF shop capacity reinforces the country's MRO leadership. Looking forward, German participation in FCAS and rising hybrid-electric R&D under the LuFo programme will compound demand.

U.K. Jet Engine Market Size

The United Kingdom holds roughly 20% of the European jet engine market in 2025, anchored by Rolls-Royce, whose Civil Aerospace large-engine flying hours recovered to 100% of 2019 levels in 2024. The Trent XWB and Pearl families underpin demand. Looking forward, the U.K.'s leadership role in the Global Combat Air Programme (GCAP) alongside Italy and Japan will lift defense propulsion R&D spending materially through 2033.

France Jet Engine Market Size

France is likely to contribute nearly 25% of the Europe jet engine market in 2026, driven by Safran Aircraft Engines, whose joint venture CFM International delivered more than 1,400 LEAP engines in 2024. Strong Airbus production support and Rafale fighter exports to India, Indonesia and the UAE underpin demand. Looking forward, the FCAS Phase 2 engine demonstrator and ENGINeUS hybrid-electric maturation will sustain France's leadership.

Asia Pacific Jet Engine Market Trends and Insights

Asia Pacific is the fast-growing market with a projected CAGR of 10.6% between 2026 and 2033, propelled by relentless expansion of commercial fleets, defense modernization and an emerging local propulsion industrial base. China alone added over 100 million domestic passenger trips between 2023 and 2024 according to the Civil Aviation Administration of China (CAAC), while India targets 220 operational airports by 2025. Combined with sixth-generation fighter pursuits in China, India and Japan, the region is shifting from a pure import market to a co-development partner, opening multi-decade scaling opportunities for global propulsion OEMs willing to localize.

India Jet Engine Market Size

India is likely to represent approximately 12% of the Asia Pacific jet engine market in 2026, propelled by IndiGo's record 500-aircraft order with Airbus, Air India's 470-aircraft combined Airbus-Boeing order and the GE F414 co-production agreement signed in 2023 for the LCA Tejas Mk2. Looking forward, the Atmanirbhar Bharat initiative and India's indigenous AMCA fighter engine programme will reshape the country's propulsion trajectory.

Japan Jet Engine Market Size

Japan is likely to account for 18% of Asia Pacific jet engine demand in 2026, sustained by IHI Corporation's participation in the PW1100G, GE9X and Trent 1000 programmes, plus Mitsubishi Heavy Industries' defense engine work. Japan's defense budget reached a record JPY 7.95 trillion in fiscal 2024. Looking forward, the trilateral Global Combat Air Programme (GCAP) with the U.K. and Italy positions Japan as a sixth-generation engine co-developer.

South Korea Jet Engine Market Size

South Korea accounts for roughly 9% of Asia Pacific jet engine market in 2025, supported by Hanwha Aerospace, which has manufactured more than 10,000 engines under licence from GE, Pratt & Whitney and Rolls-Royce. The KF-21 Boramae fighter, powered by F414-GE-400K engines, entered low-rate production in 2024. Looking forward, Korea's indigenous fighter-engine R&D programme launched by DAPA will deepen domestic propulsion capability through 2033.

Competitive Landscape

The jet engine market is one of the most consolidated industrial sectors globally, with GE Aerospace, Rolls-Royce Holdings, Pratt & Whitney (a unit of RTX), Safran Aircraft Engines and the CFM International joint venture together controlling more than 85% of commercial propulsion. This is a market that rewards scale above all else, certification capital, multi-decade aftermarket annuities and program-level risk sharing leave little room for new entrants outside niche UAV or hybrid-electric pockets.

The dominant strategic themes are vertical integration into MRO via OEM-controlled shop networks, premiumization through power-by-the-hour service contracts, and aggressive digital investment in predictive maintenance. Emerging shifts include co-development partnerships for hybrid-electric demonstrators and intensifying nation-led industrial policy in India, China and Japan.

Key Developments

- March, 2025: GE Aerospace announced a US$ 1 billion investment in U.S. manufacturing capacity expansion across its MRO, supply chain and engine assembly operations to meet record commercial backlog.

- October, 2024: Pratt & Whitney delivered the first GTF Advantage engine certified by the FAA, offering 1% improved fuel burn and extended time-on-wing for A320neo operators globally.

- February, 2024: Rolls-Royce Holdings successfully ran its UltraFan demonstrator at maximum power, validating a 25%-more-efficient architecture targeted at future wide-body and narrow-body applications beyond 2030.

Companies Covered in Jet Engine Market

- GE Aerospace

- Rolls-Royce Holdings

- Pratt & Whitney (RTX Corporation)

- Safran Aircraft Engines

- CFM International

- MTU Aero Engines

- Honeywell Aerospace

- IAE International Aero Enginess AG

- Williams International

- Klimov

- Saturn NPO (UEC-Saturn)

- Aviadvigatel

- Ivchenko-Progress

- Motor Sich

- Textron Aviation

- IHI Corporation

- Hanwha Aerospace

- Mitsubishi Heavy Industries

- Hindustan Aeronautics Limited (HAL)

Frequently Asked Questions

The global jet engine market is expected to be valued at US$ 81.3 billion in 2026 and is projected to reach US$ 143.0 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

The leading demand driver is the record commercial aircraft backlog at Boeing and Airbus, together exceeding 14,400 aircraft, which mechanically locks in two-decade visibility for turbofan production and high-margin aftermarket revenue.

North America leads with a 38% share in 2025, anchored by GE Aerospace, Pratt & Whitney, Honeywell Aerospace, deep U.S. Department of Defense procurement, and the densest concentration of certification and MRO infrastructure globally.

Hybrid-electric and hydrogen propulsion in the regional aircraft and UAV segment is the most actionable opportunity, growing at a projected CAGR of nearly 18.5% as EASA and the FAA mature certification frameworks for novel propulsion architectures through 2033.

Leading players include GE Aerospace, Rolls-Royce Holdings, Pratt & Whitney, Safran Aircraft Engines, CFM International, MTU Aero Engines, Honeywell Aerospace, IHI Corporation, and Hanwha Aerospace.