- Aerospace & Defense

- Defense HVAC Systems Market

Defense HVAC Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Defense HVAC Systems Market by Product Type (Facility HVAC Systems, Vehicle HVAC, Others), End-user (Military Organizations, Government Agencies, Others), Equipment, Application, and Regional Analysis for 2026 - 2033

Defense HVAC Systems Market Size and Trends Analysis

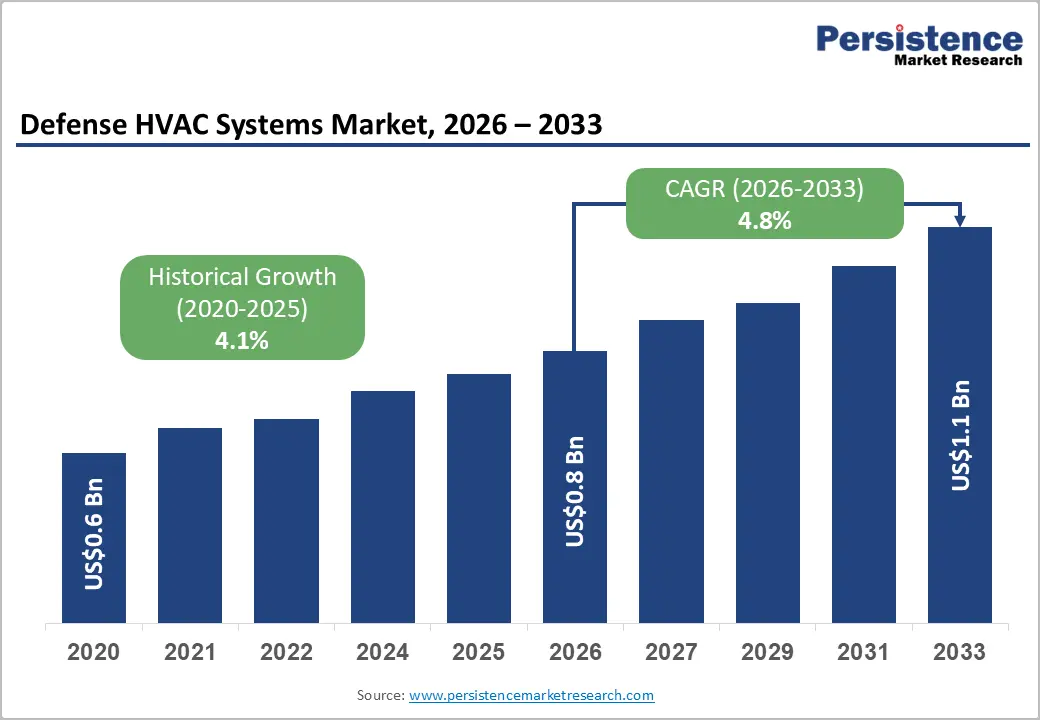

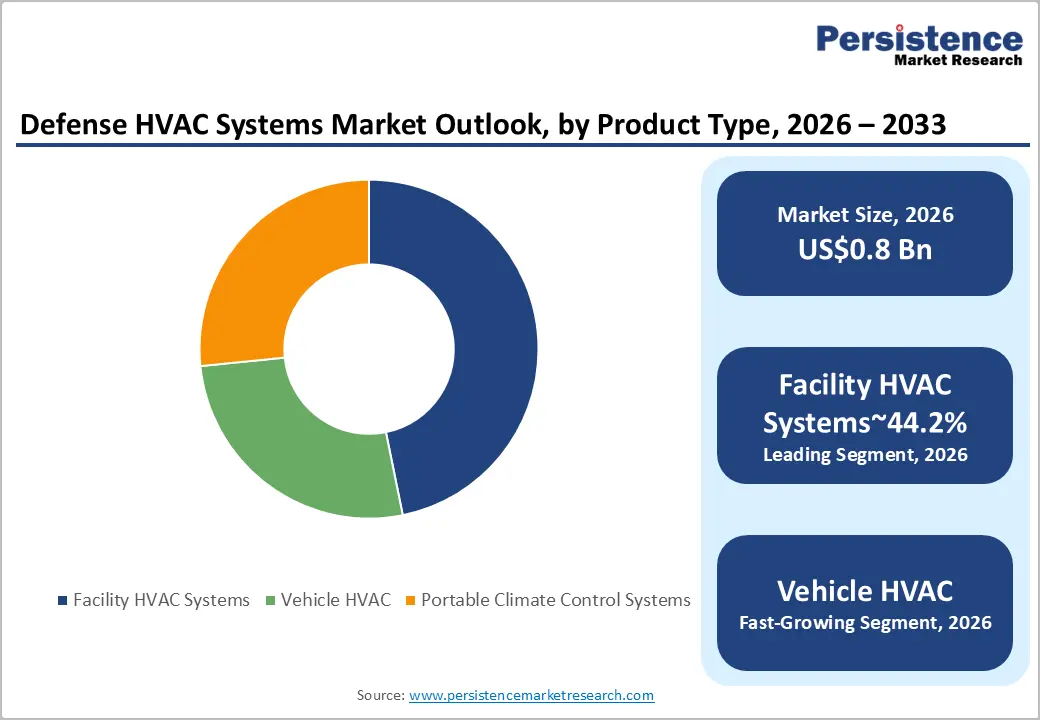

The global defense HVAC systems market size is likely to be valued at US$0.8 billion in 2026 and is expected to reach US$1.1 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by increasing defense modernization programs, rising investments in military infrastructure, and growing demand for climate-controlled environments across mission-critical facilities.

Defense organizations are prioritizing energy-efficient and resilient HVAC systems to support operational readiness, equipment protection, and personnel safety. The increasing integration of advanced electronics, communication systems, and data-intensive command infrastructure is also accelerating demand for precise temperature, humidity, and air-quality management solutions across military installations worldwide.

Key Industry Highlights:

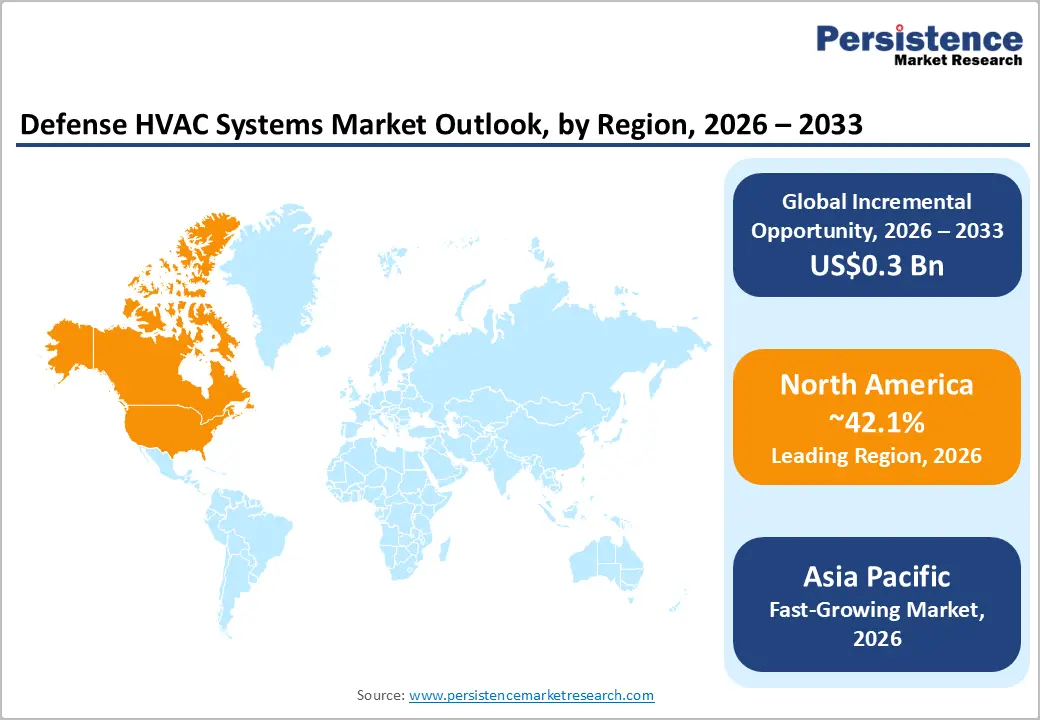

- Leading Region: North America is projected to account for 42.1% of market share in 2026, supported by extensive military infrastructure, defense modernization programs, and strong investments in resilient facility management systems.

- Fastest-growing Region: Asia Pacific is projected to register the highest growth rate through 2033, driven by rising defense expenditure, military infrastructure expansion, and increasing procurement activities across China, India, Japan, South Korea, and ASEAN countries.

- Dominant Product Type: Facility HVAC systems are anticipated to hold 44.2% of market share in 2026, driven by widespread deployment across military bases, command centers, logistics facilities, defense hospitals, and maintenance depots.

- Leading End-user: Military organizations are estimated to account for 51.7% market share in 2026, supported by large-scale ownership of military installations, transportation assets, operational facilities, and mission-critical infrastructure requiring advanced climate-control systems.

DRO Analysis

Driver - Rising Defense Modernization and Infrastructure Investments

Growing global defense expenditure continues to be a primary catalyst for the Defense HVAC Systems Market. Governments across North America, Europe, and Asia Pacific are increasing investments in military facilities, operational bases, command centers, maintenance depots, and strategic infrastructure. Modern military facilities require highly reliable HVAC systems to maintain optimal environmental conditions for personnel, weapons systems, communication networks, and sensitive electronic equipment.

Military modernization programs increasingly incorporate energy resilience initiatives, smart building technologies, and sustainability objectives, creating demand for advanced HVAC solutions capable of supporting uninterrupted operations. HVAC systems have evolved from basic environmental control systems into critical infrastructure assets that directly contribute to mission readiness, operational continuity, and asset protection. As military organizations continue upgrading aging facilities and expanding strategic capabilities, demand for high-performance HVAC systems is expected to remain strong throughout the forecast period.

Climate Resilience, Air Quality Requirements, and Electrification Trends

Increasing climate variability and extreme weather conditions are placing greater emphasis on environmental control systems within military facilities and operational environments. Defense agencies are strengthening requirements for indoor air quality, ventilation performance, humidity management, and thermal comfort to improve personnel effectiveness and equipment reliability.

The growing adoption of advanced sensors, surveillance technologies, communication systems, and computing infrastructure has further increased the need for precise environmental management. Simultaneously, defense organizations are pursuing energy efficiency and carbon reduction initiatives, encouraging the deployment of electrified HVAC technologies such as heat pumps and intelligent building management systems. The integration of AI-enabled controls, predictive maintenance capabilities, and smart energy optimization platforms is enhancing system performance while reducing lifecycle costs, making advanced HVAC solutions increasingly attractive for defense applications.

Restraint - High Capital Costs and Complex Procurement Requirements

Despite favorable market conditions, the Defense HVAC Systems Market faces challenges associated with high installation costs, stringent compliance requirements, and lengthy procurement processes. Military HVAC systems must meet rigorous standards for reliability, redundancy, cybersecurity, environmental protection, and operational resilience, significantly increasing project complexity compared to conventional commercial HVAC installations.

The transition toward low-emission refrigerants, advanced controls, and energy-efficient technologies often requires extensive retrofitting of existing infrastructure, increasing project costs and implementation timelines. In addition, defense procurement procedures typically involve lengthy qualification, testing, and approval processes that can delay project execution. The need for specialized engineering expertise and certified installation personnel further contributes to elevated costs, creating barriers for smaller suppliers and limiting competitive participation in certain defense projects.

Opportunity - Expanding Military Infrastructure Development across Asia Pacific and Europe

Defense infrastructure investments are increasing significantly across Asia Pacific and Europe, creating substantial opportunities for HVAC system manufacturers and service providers. Growing geopolitical tensions, military modernization initiatives, and enhanced national security priorities are driving investments in military bases, logistics hubs, training facilities, command centers, and border security infrastructure.

Countries including China, India, Japan, Germany, France, and the United Kingdom continue expanding defense capabilities through large-scale infrastructure development programs. These projects require sophisticated climate-control solutions capable of supporting personnel, equipment, and mission-critical operations under diverse environmental conditions. The expansion of localized manufacturing and regional service networks is expected to further support market growth by improving supply chain efficiency and reducing project lead times.

Growth of Smart HVAC and Lifecycle Service Models

The increasing adoption of digital building technologies presents significant opportunities for defense HVAC providers. Military organizations are seeking intelligent HVAC systems that offer real-time monitoring, predictive maintenance, automated diagnostics, and energy optimization capabilities. These technologies improve operational efficiency while reducing maintenance costs and system downtime.

The emergence of HVAC-as-a-Service models is creating recurring revenue opportunities beyond traditional equipment sales. Vendors are increasingly offering integrated lifecycle management solutions that combine equipment, software, analytics, maintenance services, and performance optimization. As defense organizations prioritize long-term operational reliability and asset visibility, demand for digitally enabled service-based HVAC solutions is expected to grow steadily.

Category-wise Analysis

Product Type Insight

Facility HVAC systems are anticipated to account for 44.2% of the market share in 2026, maintaining their position as the largest product segment. Demand is driven by extensive deployment across military bases, command centers, maintenance depots, defense hospitals, and logistics facilities, where reliable temperature and air-quality control are essential for operational continuity. For example, modern U.S. and NATO military installations increasingly integrate smart HVAC systems to improve energy resilience and support mission-critical operations. The adoption of energy-efficient controls and advanced filtration technologies continues to strengthen segment growth.

Vehicle HVAC systems are anticipated to be the fastest-growing segment. Growth is supported by increasing deployment of armored vehicles, tactical trucks, and command vehicles equipped with advanced electronics and communication systems that require effective thermal management. Modern military platforms such as infantry fighting vehicles and mobile command units increasingly rely on integrated HVAC systems to enhance crew comfort, equipment performance, and mission readiness in extreme climates.

End-user Insight

Military organizations are anticipated to hold 51.7% of the market share in 2026, remaining the dominant end-user segment. Armed forces operate extensive networks of bases, command facilities, training centers, and military vehicles that require highly reliable HVAC systems. Rising investments in force modernization, infrastructure upgrades, and operational readiness programs continue to support demand. For instance, defense facility modernization initiatives across the United States, China, and Europe are driving procurement of advanced climate-control systems for mission-critical environments.

Government agencies are anticipated to be the fastest-growing end-user segment. Demand is increasing across emergency response centers, homeland security facilities, disaster management hubs, and strategic government infrastructure. Agencies are increasingly adopting energy-efficient HVAC systems with smart monitoring capabilities to improve resilience and reduce operating costs. Investments in critical infrastructure protection and emergency preparedness programs are expected to further accelerate segment growth during the forecast period.

Regional Insights

North America Defense HVAC Systems Market Trends

North America is anticipated to maintain its position as the largest regional market, accounting for 42.1% of market revenue in 2026. The region benefits from extensive defense infrastructure, high military spending, and continuous investments in facility modernization, energy resilience, and mission-critical operations. Growing adoption of intelligent building management systems, advanced air filtration technologies, and energy-efficient HVAC solutions is supporting market expansion across military facilities.

U.S. Defense HVAC Systems Market Trends

The U.S. is expected to dominate the North America market, accounting for 82.6% of regional revenue in 2026. The country's extensive network of military bases, command centers, logistics hubs, naval facilities, and training installations drives substantial demand for advanced HVAC systems. Ongoing investments in defense infrastructure modernization, cybersecurity facilities, and resilient energy systems continue to support the deployment of smart climate-control technologies across military operations.

Canada Defense HVAC Systems Market Trends

Canada is expected to represent 12.9% of the North America market in 2026 and is witnessing steady growth, driven by defense modernization initiatives and infrastructure upgrades. Demand is particularly strong in remote military installations and cold-climate operational environments where reliable heating, ventilation, humidity control, and air filtration systems are essential for maintaining personnel readiness and equipment performance.

Europe Defense HVAC Systems Market Trends

Europe represents a significant growth market, supported by increasing defense budgets, military modernization programs, and infrastructure investments across NATO member states. The region's emphasis on sustainability, energy efficiency, and operational readiness is encouraging the adoption of advanced HVAC systems with intelligent controls and low-emission technologies.

Germany Defense HVAC Systems Market Trends

Germany remains one of Europe's largest defense infrastructure markets. Investments in military facility upgrades, logistics centers, and command operations are creating sustained demand for high-performance HVAC systems. The country's focus on energy-efficient building technologies further supports market growth.

U.K. Defense HVAC Systems Market Trends

The U.K. continues to invest in defense modernization programs, including upgrades to military bases, naval facilities, and strategic command centers. Growing requirements for secure and resilient infrastructure are driving demand for advanced HVAC systems with enhanced monitoring and control capabilities.

France Defense HVAC Systems Market Trends

France is strengthening its defense capabilities through investments in military infrastructure, aerospace facilities, and operational command networks. Demand for energy-efficient climate-control systems is increasing as military organizations seek to improve operational performance while reducing facility operating costs.

Spain Defense HVAC Systems Market Trends

Spain is emerging as a growing market for defense HVAC solutions, supported by military infrastructure improvements and NATO-related investments. The expansion of training facilities, logistics hubs, and defense support infrastructure is contributing to increased demand for modern HVAC technologies.

Asia Pacific Defense HVAC Systems Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market through 2033, driven by rising defense expenditure, expanding military infrastructure, and increasing geopolitical tensions. The region benefits from a strong manufacturing base, cost-competitive production capabilities, and growing investments in advanced defense technologies.

China Defense HVAC Systems Market Trends

China represents one of the largest defense infrastructure markets globally. Continued investments in military bases, naval facilities, aerospace infrastructure, and command systems are creating significant opportunities for HVAC manufacturers. Demand is particularly strong for high-capacity cooling, ventilation, and air-filtration solutions supporting advanced military operations.

India Defense HVAC Systems Market Trends

India is experiencing robust growth due to increasing defense budgets and extensive military modernization initiatives. Expansion of border infrastructure, air force facilities, naval bases, and command centers is driving demand for advanced HVAC systems designed to operate across diverse climatic conditions.

Japan Defense HVAC Systems Market Trends

Japan continues to strengthen its defense preparedness through investments in military facilities, surveillance systems, and command infrastructure. The country's focus on energy efficiency, disaster resilience, and technology integration is supporting the adoption of intelligent HVAC solutions.

South Korea Defense HVAC Systems Market Trends

South Korea remains an important market due to its advanced defense capabilities and ongoing investments in military readiness. Modern command centers, defense manufacturing facilities, and operational bases require sophisticated climate-control systems that support both personnel and mission-critical equipment.

Competitive Landscape

The global defense HVAC systems market is moderately concentrated, with several global HVAC manufacturers maintaining strong positions through technological expertise, extensive service networks, and long-standing relationships with government and defense customers. Large multinational suppliers dominate major defense projects due to their engineering capabilities, product portfolios, and ability to deliver integrated solutions. Smaller specialized providers compete through niche expertise, customized solutions, and regional service capabilities. Competition is increasingly centered on energy efficiency, digitalization, lifecycle services, and operational reliability.

Leading companies are prioritizing technological innovation, digital building platforms, predictive maintenance capabilities, and energy-efficient solutions. Strategic focus areas include AI-driven controls, low-emission HVAC technologies, regional manufacturing expansion, and lifecycle service offerings. Long-term maintenance contracts and integrated building management solutions are becoming increasingly important competitive differentiators.

Key Industry Developments:

- In November 2025, Johnson Controls launched Metasys 15.0, its next-generation building automation platform featuring enhanced scalability, multi-server redundancy, and advanced energy intelligence capabilities designed for mission-critical environments such as military facilities, data centers, and large campuses.

- In March 2025, Daikin Applied announced a strategic investment in Poppy, a smart air-quality monitoring company, aiming to expand its healthy building solutions portfolio and improve indoor environmental quality through advanced sensing and analytics technologies.

Companies Covered in Defense HVAC Systems Market

- Carrier Global Corporation

- Trane Technologies plc

- Johnson Controls International plc

- Daikin Industries, Ltd.

- Mitsubishi Electric Corporation

- Honeywell International Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Modine Manufacturing Company

- Munters Group AB

- Vertiv Holdings Co.

- Lennox International Inc.

- Danfoss A/S

- Bosch Home Comfort Group

- LG Electronics Inc.

- FläktGroup Holding GmbH

Frequently Asked Questions

The global defense HVAC systems market is estimated to be valued at US$ 0.8 billion in 2026.

The market is projected to reach US$ 1.1 billion by 2033.

The market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Key trends include the adoption of smart HVAC technologies, AI-enabled building management systems, energy-efficient heat pumps, advanced air filtration solutions, and increasing investments in mission-critical military infrastructure.

Facility HVAC systems are the leading product segment, accounting for 44.2% of the market share, supported by extensive deployment across military bases, command centers, and defense facilities.

Major companies include Carrier Global Corporation, Trane Technologies plc, Johnson Controls International plc, Daikin Industries Ltd., and Mitsubishi Electric Corporation.