- Pharmaceuticals

- Iron Deficiency Anemia Therapy Market

Iron Deficiency Anemia Therapy Market Size, Share, and Growth Forecast 2026 - 2033

Iron Deficiency Anemia Therapy Market Size, Share & Growth Forecast by, Product Types, Therapy Areas, Age Groups, Formulations, Distribution Channels, by Regional Analysis, from 2026 to 2033

Iron Deficiency Anemia Therapy Market Share and Trends Analysis

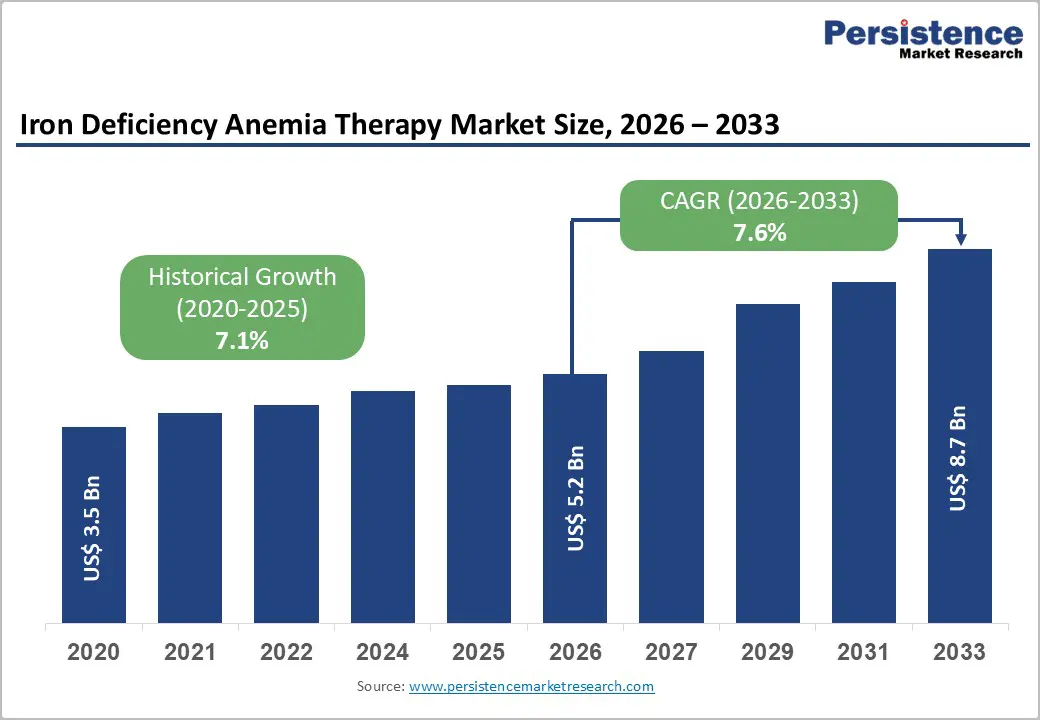

The global iron deficiency anemia therapy market size is expected to be valued at US$ 5.2 billion in 2026 and projected to reach US$ 8.7 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033. Anemia is a physio-health condition driven by nutritional disorders, affecting nearly 30% of the global population, particularly women and children. The condition arises when hemoglobin levels fall due to inadequate iron intake, absorption issues, or chronic blood loss, leading to fatigue, weakness, and impaired immunity. High-risk groups include young children, adolescent girls, pregnant women, and postpartum mothers, making effective therapies critical for public health systems worldwide.

The expanding screening programs, and improved awareness of micronutrient deficiencies highlights efforts and measures against the growing levels of anemia in developing countries. Increasing mortality trends in certain regions, broader access to diagnostics, and innovations in oral and intravenous iron formulations are accelerating demand. Public-health nutrition initiatives and targeted maternal-child health programs further support sustained adoption of anemia therapies globally.

Key Industry Highlights:

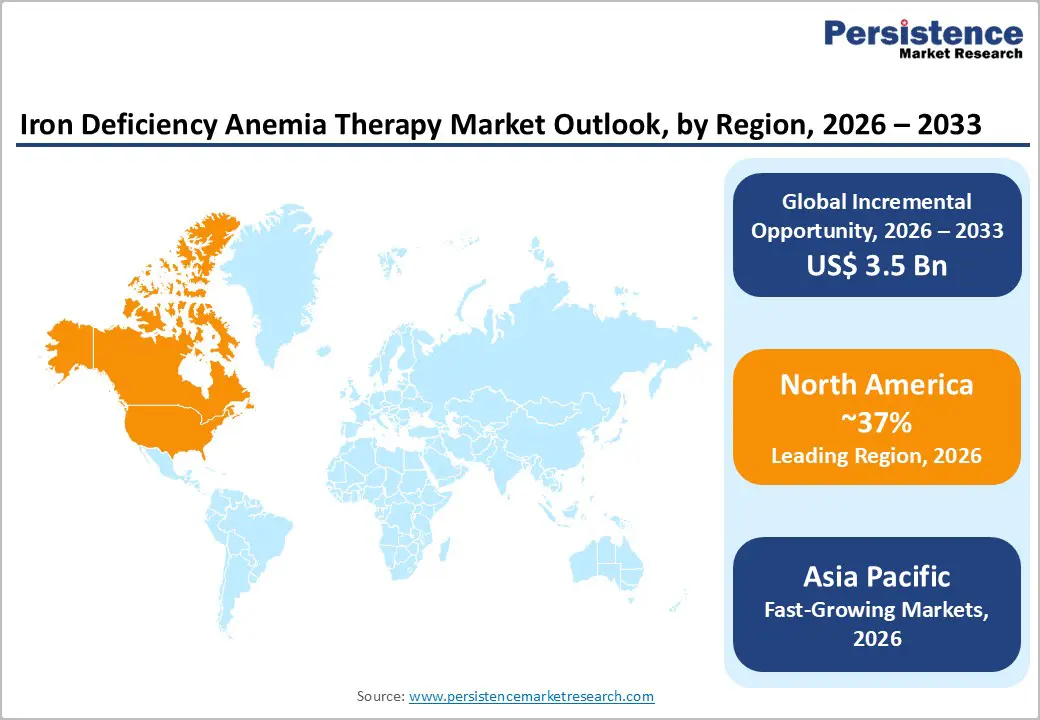

- Leading Region: North America leads the global market, supported by advanced healthcare systems, strong reimbursement coverage, and widespread anemia screening programs.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by high disease prevalence, government nutrition initiatives, and expanding healthcare infrastructure.

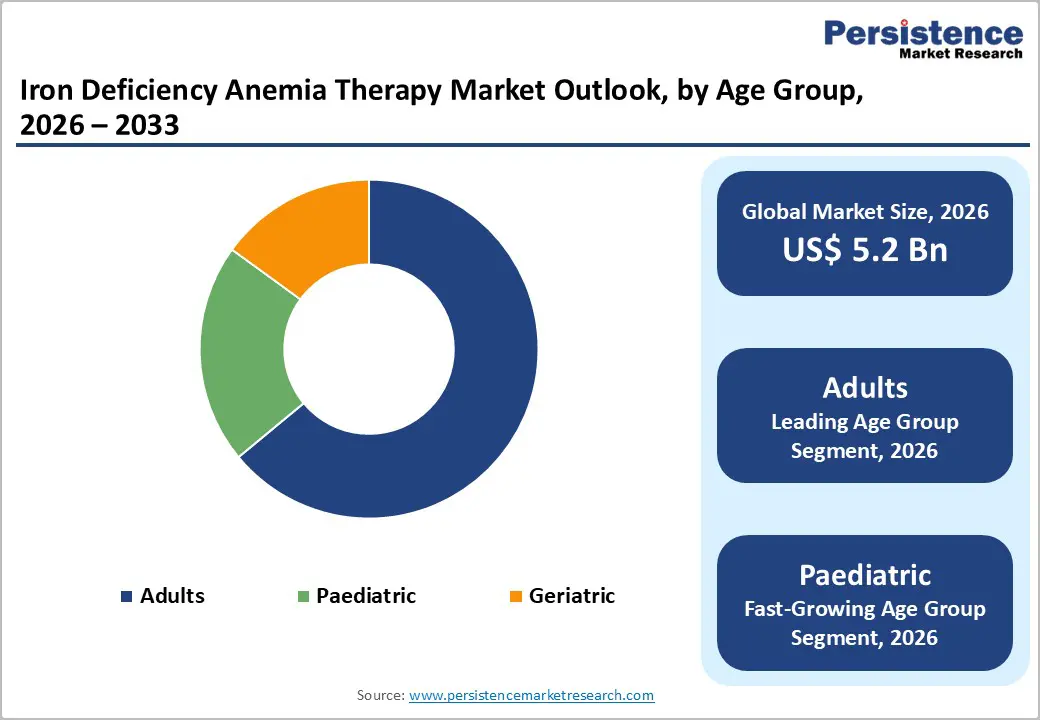

- Dominant Segment: Adult patients dominate due to higher diagnosis rates, chronic disease burden, and routine use of oral and intravenous iron therapies.

- Fastest Growing Segment: Pediatric therapies are growing fastest, fuelled by school-based programs, maternal-child health focus, and child-friendly formulations.

| Key Insights | Details |

|---|---|

|

Iron Deficiency Anemia Therapy Market Size (2026E) |

US$ 5.2 billion |

|

Market Value Forecast (2033F) |

US$ 8.7 billion |

|

Projected Growth CAGR (2026-2033) |

7.6% |

|

Historical Market Growth (2020-2025) |

7.1% |

Market Dynamics

Driver – Rising Healthcare Investment, Disease Burden, and Innovation Driving Market Expansion

Rising healthcare expenditure across developed and emerging economies is a major growth catalyst for the iron deficiency anemia therapy market. Increased public and private investment improves hospital infrastructure, diagnostic access, and availability of specialty drugs, allowing earlier detection and sustained treatment. Expanding insurance coverage and maternal-child health programs further enhance therapy uptake, particularly among vulnerable groups such as pregnant women and children. Simultaneously, population aging and increasingly sedentary lifestyles elevate anemia risk through chronic diseases, malabsorption disorders, and long-term medication use, creating sustained demand for oral and injectable iron products.

Growing public awareness of anemia screening and nutritional deficiencies also supports market expansion. Government campaigns, NGO initiatives, and physician education programs are encouraging routine testing and early intervention. In parallel, pharmaceutical innovation is producing formulations with improved absorption, fewer gastrointestinal side effects, and simplified dosing schedules, boosting patient compliance. The combination of rising disease burden, demographic shifts, technological progress, and better access to care is expected to propel market revenues steadily throughout the forecast period.

Restraints – Barriers to Adoption and Accessibility

Despite strong growth fundamentals, several constraints limit the full potential of the iron deficiency anemia therapy market. A shortage of trained healthcare professionals, especially in low- and middle-income countries, restricts accurate diagnosis and appropriate therapy selection. Limited laboratory infrastructure and insufficient specialist availability often delay treatment initiation, allowing anemia to progress and reducing patient engagement with formal healthcare systems.

High treatment costs also present a significant barrier, particularly for intravenous iron formulations and branded products used in hospital settings. In regions with weak reimbursement structures, out-of-pocket expenses discourage therapy adherence and completion, increasing relapse rates. Supply-chain limitations, uneven distribution networks, and price sensitivity in rural areas further slow market penetration. Together, workforce gaps and affordability challenges continue to constrain broader adoption, especially in emerging economies where disease prevalence is highest.

Opportunity – Innovation and Expansion into Underserved Regions

The iron deficiency anemia therapy market offers substantial opportunities through product innovation and geographic expansion. Rising unmet medical needs have encouraged pharmaceutical companies to introduce new and generic formulations with improved safety profiles and convenient administration. Regulatory approvals, such as newer injectable iron therapies and lower-cost biosimilar alternatives, are expanding treatment choices for hospitals and outpatient clinics while increasing affordability. These launches allow companies to differentiate portfolios and capture growing demand from both acute-care and chronic-management segments.

Significant growth potential also exists in underpenetrated regions including Asia Pacific, Latin America, the Middle East, and Africa, where large patient populations remain undertreated. Expanding public-health nutrition programs, maternal-care initiatives, and government-funded anemia control strategies are improving diagnosis rates and therapy access. Strategic partnerships with local distributors, tiered pricing models, and investments in community screening campaigns can further unlock these markets, positioning companies for long-term revenue growth.

Category-wise Analysis

By Age Group Insights

Adults are expected to account for approximately 64% of the iron deficiency anemia therapy market, reflecting the large disease burden within the working-age and elderly-adjacent population. Adult patients commonly experience iron deficiency due to chronic gastrointestinal disorders, inflammatory diseases, renal conditions, heavy menstrual blood loss among women, and postoperative recovery needs. Routine screening during primary-care visits, pregnancy check-ups, and management of chronic illnesses has increased diagnosis rates, driving sustained demand for both oral and intravenous iron therapies. Greater insurance coverage and access to outpatient infusion centers further support treatment uptake, particularly in developed healthcare systems where early intervention is emphasized.

The pediatric segment is projected to be the fastest growing, driven by expanding government nutrition programs, school-based supplementation initiatives, and heightened awareness of childhood anemia’s impact on cognitive development and physical growth. Rising birth rates in emerging economies and improved neonatal screening protocols are also contributing to higher treatment volumes. Pharmaceutical companies are introducing child-friendly formulations such as flavored syrups, chewable tablets, and lower-dose preparations to improve adherence. These combined clinical, demographic, and policy-driven factors are expected to accelerate pediatric segment growth while adults continue to dominate overall market revenues.

By Distribution Channel Insights

By distribution channel, the iron deficiency anemia therapy market is served through hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies play a critical role in dispensing intravenous iron formulations and prescription-only products used for severe anemia, perioperative management, and chronic kidney disease patients. Specialist clinics and infusion centers further strengthen hospital-linked distribution, ensuring supervised administration and monitoring. Retail pharmacies account for significant volumes of oral iron supplements and branded prescription products, benefiting from widespread geographic reach and strong consumer trust.

Online pharmacies are gaining momentum as digital health adoption increases, offering convenience, competitive pricing, and subscription models for long-term supplementation. In several developing regions, government procurement and public distribution systems remain vital, particularly for maternal and child health programs targeting high-risk populations. Manufacturers increasingly adopt multi-channel strategies, combining institutional sales with consumer-focused retail and e-commerce platforms to maximize penetration. Expansion of pharmacy networks, improved logistics infrastructure, and regulatory support for teleconsultations are expected to further diversify distribution pathways and enhance global market accessibility.

Region-wise Insights

North America Iron Deficiency Anemia Therapy Market Trends

North America represents a major revenue-generating region for iron deficiency anemia therapies, supported by sophisticated healthcare delivery systems, high per-capita medical spending, and strong access to diagnostic testing. Hospitals and outpatient clinics routinely screen high-risk populations such as pregnant women, elderly individuals, and patients with chronic kidney disease or gastrointestinal disorders, creating steady demand for both oral and intravenous iron formulations. The presence of established pharmaceutical manufacturers and specialty drug distributors further strengthens regional supply chains, while continuous investment in formulation upgrades and infusion-center expansion improves patient access.

The region is expected to account for around 37% of global market share in 2026, with the U.S. contributing most revenues. Growth is reinforced by increasing anemia prevalence, broader physician awareness, and clearer clinical guidelines supporting early intervention. A rapidly expanding geriatric population, coupled with lifestyle-related conditions that impair iron absorption, continues to enlarge the treatment pool. Reimbursement coverage for injectable therapies and growing adoption of outpatient infusion services is also enhancing therapy utilization, positioning North America as a stable and mature market throughout the forecast period.

Asia Pacific Iron Deficiency Anemia Therapy Market Trends

Asia Pacific is emerging as a high-growth region for iron deficiency anemia therapies due to its large population base and rising burden of nutritional deficiencies. Countries such as India, China, Indonesia, and Vietnam report substantial anemia prevalence among women and children, creating persistent demand for supplementation programs and therapeutic interventions. Urbanization, dietary transitions, and socioeconomic disparities further contribute to disease incidence, prompting governments to prioritize anemia screening and maternal-health initiatives. Expanding hospital networks, private diagnostic laboratories, and retail pharmacy chains are improving access to iron products across both urban and semi-urban settings.

Regional growth is also supported by increasing healthcare expenditure and domestic pharmaceutical manufacturing, which enables wider availability of cost-effective oral formulations and injectable products. Public nutrition campaigns and school-based supplementation programs are improving diagnosis rates, while physician education efforts promote evidence-based therapy selection. Multinational companies are strengthening distribution partnerships and establishing local production facilities to serve price-sensitive markets efficiently. These combined factors demographic pressure, policy support, infrastructure development, and manufacturing scale are expected to sustain Asia Pacific’s rapid expansion in the iron deficiency anemia therapy market over the coming years.

Competitive Landscape

The competition landscape in the iron deficiency anemia therapy market is quite dynamic, with several key factors influencing its growth and development. North America and Europe continue to regulate the market due to the rising incidence of Iron Deficiency Anemia (IDA) among the older populations. However, the Asia Pacific region is anticipated to witness the fastest growth owing to high population concentration, growing elderly demographic, and rising health awareness The major companies in the market are involved in various aspects of iron deficiency and anemia therapy, including the development and marketing of oral and intravenous iron therapies, as well as other treatment modalities.

Key Industry Developments:

- In September 2025, Sandoz introduced a cost-effective iron sucrose injection in the U.S. for treating iron deficiency anemia among chronic kidney disease patients.

- In March 2024, Cadila Pharmaceuticals announced the launch of an iron supplement injection for the treatment of iron deficiency anemia.

Companies Covered in Iron Deficiency Anemia Therapy Market

- Akebia Therapeutics, Inc.

- Bayer AG

- PHARMACOSMOS A/S

- Sanofi

- Johnson & Johnson Services, Inc

- CSL Vifor

- AbbVie Inc. (Allergan)

- Novartis AG

- Teoxane

- GSK plc

- AdvaCare Pharma

- Apotex Inc.

- Covis Pharma GmbH

- Others

Frequently Asked Questions

The global iron deficiency anemia therapy market is estimated to be valued at US$ 5.2 Bn in 2026.

Increasing awareness amongst consumers worldwide for the significance of sufficient iron intake for human wellbeing is fueling the demand for Iron Deficiency and Anemia Treatment Market.

The global market is expected to witness a CAGR of 7.6% between 2026 and 2033.

Increase on the new product launches is a key opportunity for Iron Deficiency and Anemia Treatment Market.

North America is the leading region in the global iron deficiency anemia therapy market.