- HVAC

- Integrated UPS Market

Integrated UPS Market Size, Share, and Growth Forecast 2026 - 2033

Integrated UPS Market by Product Type (Online Integrated UPS, Offline (Standby) Integrated UPS, Line-Interactive Integrated UPS, Delta Conversion Integrated UPS), Configuration (Tower-based Integrated UPS, Rack-mounted Integrated UPS, Modular Integrated UPS, Standalone Integrated UPS), Technology, End-user, and Regional Analysis, 2026 - 2033

Integrated UPS Market Size and Trend Analysis

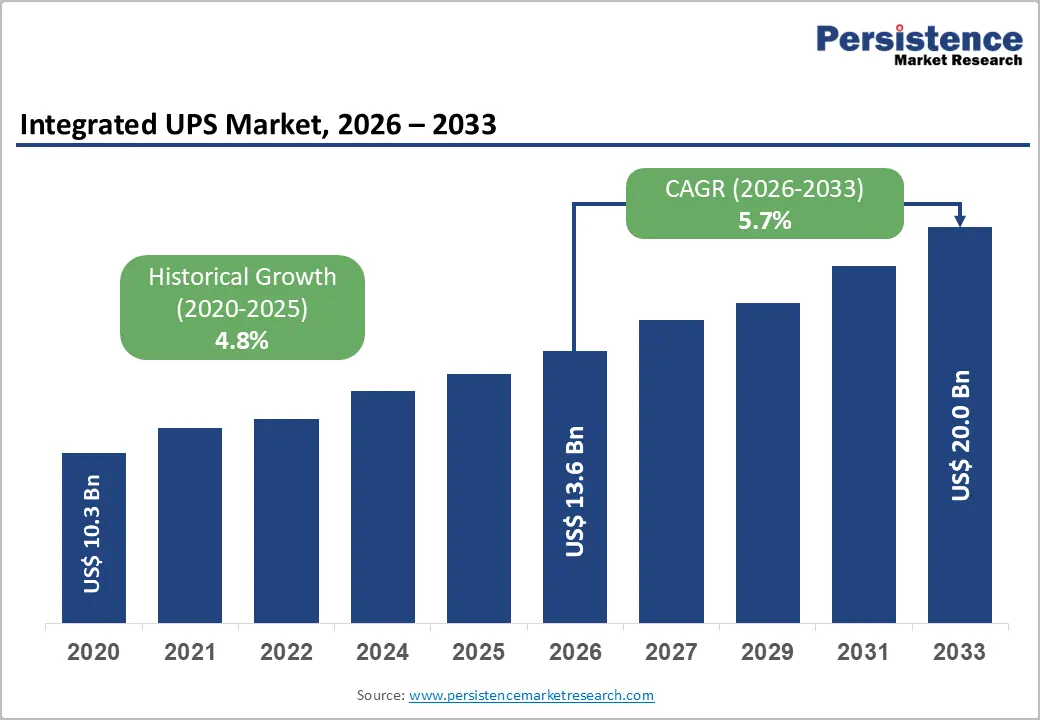

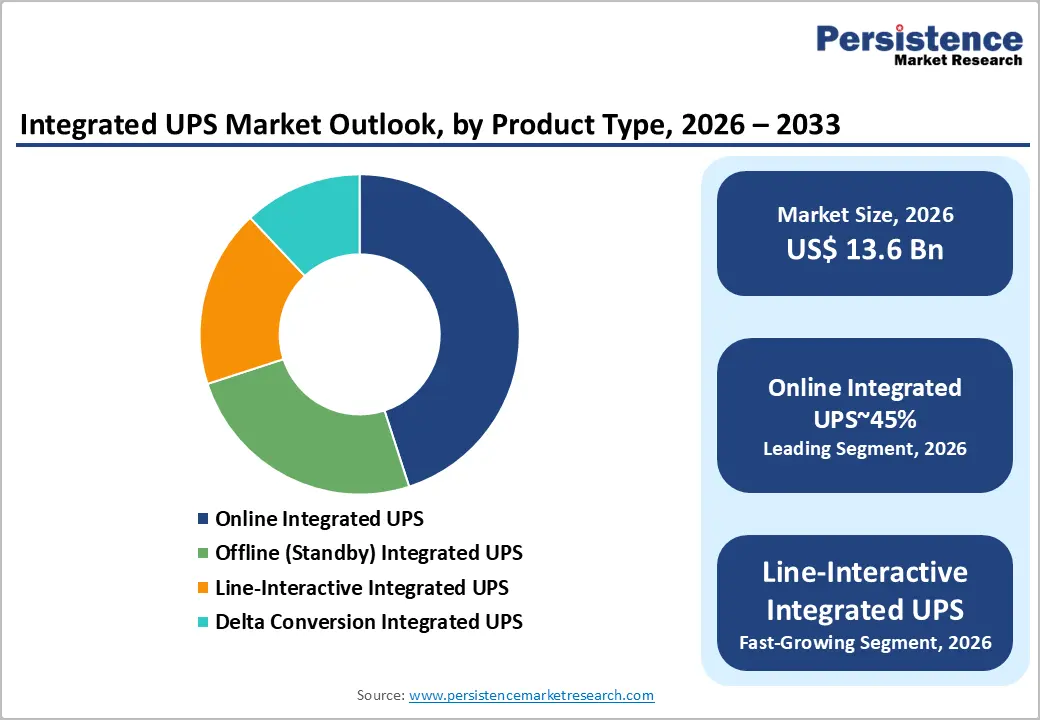

The global integrated ups market size is likely to be valued at US$ 13.6 billion in 2026 and is expected to reach US$ 20.0 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

The market's robust expansion is primarily driven by the accelerating digitalization of global industries and the rising criticality of uninterrupted power supply across data centers, healthcare, and financial services.

Key Industry Highlights:

- Leading Region: North America dominates the global Integrated UPS market with 39% share, driven by extensive data center infrastructure, stringent power reliability regulations such as NFPA 110, and a high concentration of IT and BFSI sector end-users demanding continuous, high-quality power protection.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market with a rising CAGR of 7.1%, fueled by China's East Data West Computing initiative, India's Digital India program, and rapid ASEAN data center expansion, with digital infrastructure investments exceeding US$ 4 billion annually in India alone.

- Dominant Segment: Online Integrated UPS systems lead the product type category with approximately 45% market share, favored by data centers and critical industries for their zero-transfer-time protection, complete electrical isolation, and compliance with Tier III+ data center uptime requirements.

- Fastest-Growing Segment: Modular Integrated UPS systems are the fastest-growing configuration segment, driven by edge computing deployments, 5G base station rollouts, and data center capacity scaling demands that require granular, right-sized power backup expansion.

- Key Opportunity: Healthcare digitalization and smart hospital infrastructure development present a high-value opportunity, with medical-grade UPS demand accelerating as global healthcare IT spending is projected to surpass US$ 390 billion by 2026, supported by WHO mandates for reliable facility power.

| Key Insights | Details |

|---|---|

| Integrated UPS Market Size (2026E) | US$ 13.6 Billion |

| Market Value Forecast (2033F) | US$ 20.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 4.8% CAGR |

Market Dynamics

Drivers - Exponential Growth in Data Center Infrastructure

The rapid expansion of global data center infrastructure is a major driver of the Integrated UPS market. According to the International Energy Agency (IEA), data centers consumed around 200-250 TWh of electricity worldwide in 2022, and this figure is expected to nearly double by 2026 due to the rise of AI workloads and hyperscale deployments. Leading cloud providers such as Microsoft, Amazon Web Services, and Google are investing billions of dollars to build new data centers across North America, Europe, and the Asia Pacific.

Each of these facilities requires highly reliable power conditioning and backup systems, making integrated UPS solutions essential. Additionally, the growth of edge computing and colocation facilities is increasing demand for modular and rack-mounted UPS systems. This widespread infrastructure expansion is directly contributing to strong and sustained revenue growth in the Integrated UPS market.

Rising Frequency of Power Disruptions and Grid Instability

The increasing frequency of power outages and grid instability is driving significant demand for integrated UPS systems. Weather-related disruptions are becoming more frequent and severe, impacting power reliability across regions. The Council of European Energy Regulators (CEER) reports that European customers experience approximately 15-50 minutes of unplanned outages annually, with higher levels in Southern and Eastern Europe.

In developing regions, the situation is more critical, as countries like India and several Southeast Asian nations report grid availability below 95% in certain areas. These conditions force industries such as BFSI, healthcare, and manufacturing to invest in reliable power backup solutions. Integrated UPS systems ensure continuous operations, protect sensitive equipment, and help organizations meet uptime and service-level commitments. As power reliability challenges continue to grow globally, UPS adoption is expected to rise steadily.

Restraints - High Initial Capital Investment

The high upfront cost of integrated UPS systems remains a key barrier to market adoption, particularly for small and medium-sized enterprises (SMEs). Industrial-grade online double-conversion UPS systems typically range from US$5,000 to over US$200,000, depending on capacity and configuration. In addition to equipment costs, businesses must also account for installation, infrastructure upgrades, and specialized commissioning expenses.

For organizations operating with limited budgets, especially in emerging markets, these costs can delay purchasing decisions or restrict adoption altogether. Furthermore, the total cost of ownership is relatively high, as batteries need to be replaced every 3 to 5 years, which adds to ongoing operational expenses. This financial burden often makes businesses cautious about investing in UPS systems, particularly in price-sensitive industries, thereby slowing overall market growth despite strong underlying demand.

Battery Lifecycle and Environmental Disposal Challenges

Battery lifecycle management and environmental disposal issues present significant challenges for the Integrated UPS market. Lead-acid batteries, which still account for a large share of installed UPS systems, require strict handling and disposal in accordance with regulations such as the EU Battery Directive (2006/66/EC) and the updated EU Battery Regulation (2023/1542). Failure to comply with these regulations can result in financial penalties and reputational damage.

At the same time, lithium-ion batteries, while more efficient, are becoming increasingly expensive due to rising prices of key raw materials like lithium and cobalt, driven by strong demand from the electric vehicle sector. These cost pressures impact both manufacturers and end users, limiting widespread adoption. Additionally, concerns about recycling infrastructure and environmental sustainability further complicate battery management, creating challenges for long-term UPS system deployment.

Opportunities - Modular UPS Systems for Edge Computing and 5G Infrastructure

The rapid deployment of 5G networks and the expansion of edge computing present significant growth opportunities for modular, integrated UPS systems. According to GSMA projections, global 5G connections are expected to exceed 5 billion by 2030, driving the need for decentralized micro data centers and edge nodes. These installations require compact, scalable, and remotely manageable power backup solutions, making modular UPS systems highly suitable.

Unlike traditional systems, modular UPS solutions offer flexibility, easier scalability, and efficient space utilization. Leading companies such as Schneider Electric SE and Eaton Corporation plc have already introduced specialized UPS solutions designed for telecom and edge environments. As 5G infrastructure continues to expand across urban and semi-urban areas, the demand for reliable and efficient power backup systems will grow significantly, creating strong revenue opportunities for vendors focusing on compact and intelligent UPS technologies.

Healthcare Digitalization and Smart Hospital Infrastructure

The growing digitalization of healthcare systems worldwide is creating strong demand for reliable power backup solutions. Hospitals, diagnostic labs, and telemedicine platforms increasingly depend on uninterrupted power to ensure patient safety and operational efficiency. The World Health Organization (WHO) highlights reliable electricity as a critical requirement for quality healthcare delivery, while regulatory bodies such as the U.S. Centers for Medicare & Medicaid Services (CMS) mandate backup power systems for accredited facilities.

Global healthcare IT spending is expected to exceed US$ 390 billion by 2026, further driving demand for advanced infrastructure. Integrated UPS systems that meet strict electromagnetic compatibility (EMC) requirements and comply with IEC 62310 standards are well-positioned to serve this sector. As smart hospitals and digital healthcare ecosystems expand, particularly in Asia Pacific and the Middle East, demand for high-quality UPS solutions will continue to grow.

Category-wise Analysis

Product Type Insights

Online integrated UPS systems hold the leading position in the product segment, accounting for approximately 45% of the total market share. Their dominance is primarily due to their ability to provide the highest level of power protection through continuous double-conversion technology. These systems eliminate voltage fluctuations, frequency variations, and electrical disturbances, ensuring a stable power supply.

Critical industries such as data centers, BFSI, and healthcare require zero transfer time during power interruptions, a feature that only online UPS systems can deliver effectively. According to the Uptime Institute, more than 70% of Tier III and Tier IV data centers rely on online UPS systems as a standard. Although line-interactive UPS systems are gaining popularity in less critical applications due to their efficiency, online UPS systems continue to dominate high-value applications and maintain strong demand due to their reliability and performance advantages.

Configuration Insights

Rack-mounted integrated UPS systems lead the configuration segment, holding an estimated market share of around 38%. This growth is mainly driven by the increasing number of server rooms, colocation facilities, and edge data centers, all of which require efficient use of space and high-density equipment deployment. Rack-mounted UPS systems are designed to fit standardized 1U to 4U rack formats, aligning with widely used EIA-310 rack standards in IT infrastructure.

Additionally, the adoption of advanced technologies such as hyper-converged infrastructure (HCI) and software-defined networking (SDN) has increased demand for compact and scalable power solutions. These technologies require dense server setups, further supporting the adoption of rack-mounted UPS systems. Major companies such as APC by Schneider Electric and Eaton Corporation plc are continuously expanding their product portfolios to meet the growing demand in this segment.

Technology Insights

Double conversion technology is the leading segment in the integrated UPS market, accounting for approximately 42% of total technology revenue. This technology works by continuously converting incoming AC power to DC and then back to AC, ensuring complete isolation from grid disturbances. As a result, it eliminates power quality issues such as voltage fluctuations, harmonics, and frequency variations. This makes double conversion technology a preferred choice for mission-critical applications, including financial trading centers, pharmaceutical manufacturing, and high-tier data centers.

Organizations such as the European Power Supply Manufacturers Association (EPSMA) recognize double conversion as the standard for reliable power protection. Advancements in insulated gate bipolar transistor (IGBT) technology have improved system efficiency to above 96%, addressing earlier concerns about energy loss. These improvements have strengthened the adoption of double conversion UPS systems and reinforced their leading position in the market.

End-user Insights

Data centers represent the largest end-user segment in the integrated UPS market, contributing approximately 35% of total demand. The continuous growth of hyperscale and enterprise data centers, driven by cloud computing, artificial intelligence, and digital media consumption, has significantly increased the need for reliable power infrastructure.

The number of hyperscale data centers globally surpassed 900 in 2024, with over 300 additional facilities under development. Each of these data centers requires large-scale UPS installations, often in the multi-megawatt range, making them a high-value segment of the market. Additionally, there is a growing focus on sustainability, leading operators to adopt lithium-ion UPS systems that offer higher energy density, longer lifespan, and reduced maintenance. This trend is further increasing the overall value and demand for advanced UPS solutions.

Regional Insights

North America Integrated UPS Market Trends

North America holds the largest share of the global integrated UPS market, driven primarily by the United States, which is the world’s leading data center hub. According to the U.S. Department of Energy, data centers in the country consumed approximately 200 billion kWh of electricity in 2023, and the demand is expected to grow significantly due to AI infrastructure expansions. Strict regulatory standards such as NFPA 110 and NEC Article 700 require reliable backup power systems, further supporting UPS adoption across sectors like healthcare, finance, and manufacturing.

The region also benefits from strong technological innovation, with companies such as Eaton Corporation plc and Vertiv Holdings Co. investing heavily in advanced UPS technologies. Additionally, Canada’s growing data center market, supported by low-cost hydroelectric power, contributes to regional growth. Government initiatives like the Inflation Reduction Act are also encouraging energy-efficient infrastructure investments.

Europe Integrated UPS Market Trends

Europe is the second-largest market for integrated UPS systems, with key countries such as Germany, the United Kingdom, and France driving demand. Germany’s strong industrial base supports high demand for industrial UPS systems, while the UK’s large financial sector contributes significantly to BFSI-related UPS adoption. The European Union’s Ecodesign Regulation (EU 2019/1782) sets minimum efficiency standards for UPS systems, encouraging the replacement of older systems with more energy-efficient solutions.

Countries like Spain and France are also experiencing rapid growth in data center construction, supported by investments from global cloud providers. Additionally, sustainability initiatives under the European Green Deal are promoting the adoption of lithium-ion UPS systems with higher efficiency and lower environmental impact. Standardization through EN 62040 ensures consistent product quality across the region, enabling smoother market operations and competition.

Asia Pacific Integrated UPS Market Trends

Asia Pacific is the fastest-growing region in the Integrated UPS market, driven by rapid digital infrastructure development across countries such as China, India, Japan, and ASEAN nations. China leads the region due to its large-scale data center initiatives, including the ‘East Data, West Computing’ strategy, which focuses on building multiple national data center clusters. Domestic companies like Huawei Technologies Co., Ltd. and Delta Electronics, Inc. have strengthened their market position by supporting these developments.

India is also emerging as a key growth market, supported by the Digital India initiative and significant investments exceeding US$ 4 billion annually in data center infrastructure. ASEAN countries, including Singapore, Malaysia, and Indonesia, are becoming important data center hubs due to favorable government policies. Japan’s Society 5.0 initiative and the advanced manufacturing sector further contribute to strong demand for reliable and high-performance UPS systems.

Competitive Landscape

The global integrated UPS market is moderately consolidated, with leading companies such as Schneider Electric SE, Eaton Corporation plc, Vertiv Holdings Co., ABB Ltd., and Emerson Electric Co. accounting for a significant share of total market revenue. These companies maintain their competitive position through continuous innovation, including advanced energy management software, integration of lithium-ion batteries, and IoT-enabled monitoring systems.

At the same time, emerging players, particularly from China such as Huawei Technologies Co., Ltd., are increasing competition by offering cost-effective solutions and integrated service ecosystems. Market participants are focusing on strategies such as partnerships, capacity expansion, and the development of energy-efficient products to strengthen their position. Sustainability has also become a key focus area, with companies investing in eco-friendly technologies to meet regulatory requirements and customer expectations. These strategic initiatives are shaping the competitive dynamics of the global Integrated UPS market.

Key Developments:

- March 2025: Schneider Electric SE launched the APC Smart-UPS Ultra series featuring integrated lithium-ion batteries and advanced cloud-based monitoring via its EcoStruxure IT platform, targeting hyperscale and enterprise data center segments with up to 96.5% efficiency ratings.

- November 2024: Vertiv Holdings Co. announced the expansion of its Liebert EXL S1 modular UPS line to include 1,500 kVA configurations, enabling greater scalability for large data center deployments across North America and Europe, with enhanced battery management system (BMS) integration.

- January 2024: Eaton Corporation plc introduced its upgraded 9PX Gen 2 UPS series with extended lithium-ion battery runtime options and integrated cybersecurity features compliant with NERC CIP standards, specifically targeting critical infrastructure and utility sector customers.

Integrated UPS Market Report - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 10.3 Bn |

| Current Market Value (2026) | US$ 13.6 Bn |

| Projected Market Value (2033) | US$ 20.0 Bn |

| CAGR (2026 - 2033) | 5.7% |

| Leading Region | North America, 39% share |

| Dominant Product Type | Online Integrated UPS, 45% share |

| Top-ranking Configuration | Rack-mounted integrated UPS systems, 38% |

| Incremental Opportunity | US$ 6.4 Bn |

Companies Covered in Integrated UPS Market

- Schneider Electric SE

- Eaton Corporation plc

- ABB Ltd.

- Vertiv Holdings Co.

- Emerson Electric Co.

- Siemens AG

- Delta Electronics, Inc.

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Socomec Group S.A.

- Huawei Technologies Co., Ltd.

- Riello Elettronica Group S.p.A.

- Legrand S.A.

- CyberPower Systems, Inc.

- AEG Power Solutions B.V.

- Hitachi Industrial Equipment Systems Co., Ltd.

- General Electric (GE) Power

- Fuji Electric Co., Ltd.

- Piller Power Systems GmbH

- Staco Energy Products Co.

Frequently Asked Questions

The global Integrated UPS market is projected to reach US$ 20.0 billion by 2033, expanding from an estimated US$ 13.6 billion in 2026 at a CAGR of 5.7% during the forecast period 2026 - 2033, driven by rise in data center investments and increasing power reliability requirements across

The primary demand drivers include the rapid global expansion of data center infrastructure, with hyperscale facilities surpassing 900 globally in 2024, rising frequency of grid disruptions as reported by the U.S. EIA, and accelerating digitalization across healthcare, BFSI, and IT & telecommunications sectors requiring an uninterrupted, high-quality power supply.

Online Integrated UPS systems are the leading product type segment, holding approximately 45% of the total market share. Their dominance is driven by superior power quality protection, zero-transfer-time to battery, and widespread adoption in Tier III and Tier IV data centers, financial institutions, and critical healthcare and industrial applications.

North America is the leading regional market, anchored by the United States' extensive data center ecosystem, robust regulatory standards including NFPA 110, and strong end-user demand from IT, BFSI, and healthcare sectors. The U.S. DOE estimates domestic data center electricity consumption at approximately 200 billion kWh annually, reinforcing sustained regional UPS demand.

Key opportunities include the accelerating rollout of 5G networks and edge computing infrastructure globally, requiring scalable modular UPS solutions, and the digitalization of healthcare systems, where WHO mandates and CMS regulations are driving medical-grade UPS procurement. Healthcare IT spending projected to exceed US$ 390 billion by 2026 represents a particularly significant addressable opportunity.

The key players in the global Integrated UPS market include Schneider Electric SE, Eaton Corporation plc, ABB Ltd., Vertiv Holdings Co., Emerson Electric Co., Siemens AG, Delta Electronics Inc., Mitsubishi Electric Corporation, Toshiba Corporation, Socomec Group S.A., Huawei Technologies Co. Ltd., Riello Elettronica Group S.p.A., Legrand S.A., CyberPower Systems Inc., and AEG Power Solutions B.V.