- Smart Packaging

- Insulated Packaging Market

Insulated Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Insulated Packaging Market by Material (Plastic, Bio-Based Aerogels, Others), Product Type (Boxes & Containers, Pallet Shippers, Others), End-user, and Regional Analysis for 2026 - 2033

Insulated Packaging Market Size and Trends Analysis

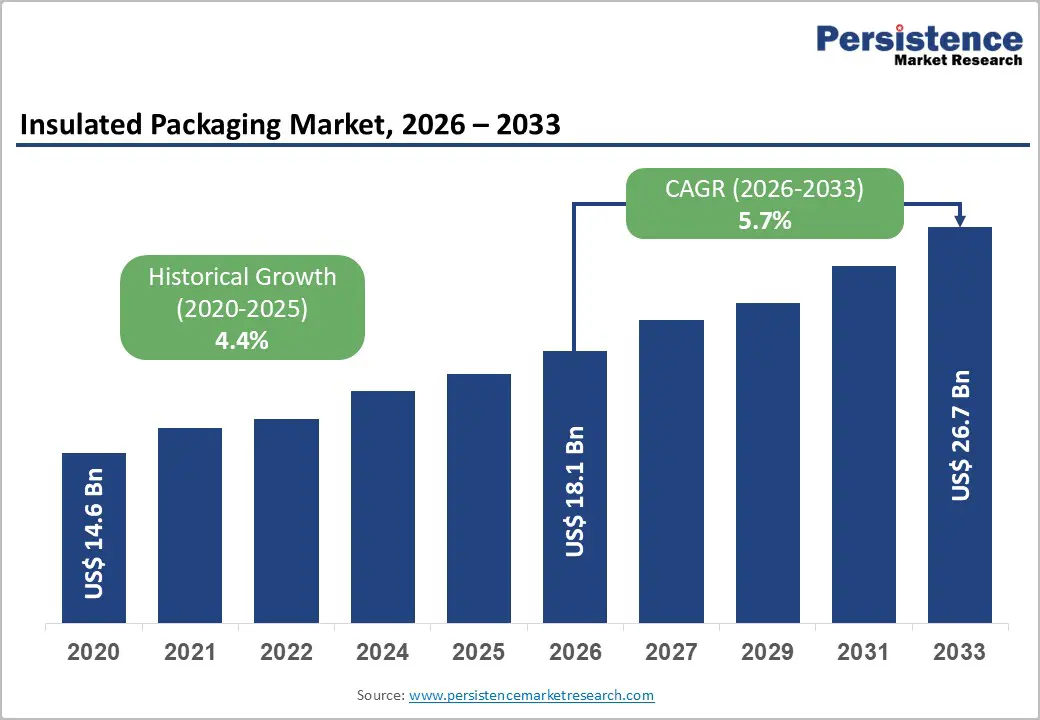

The global insulated packaging market size is likely to be valued at US$ 18.1 billion in 2026 and is expected to reach US$26.7 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033, driven by the rising need for temperature-controlled transportation solutions among pharmaceutical companies, food suppliers, and logistics providers seeking to maintain product integrity across extended supply chains.

Increasing shipments of pharmaceutical and biotechnology products, along with the rapid growth of e-grocery distribution, are emerging as key end-use segments fueling demand. Continuous innovations in materials and packaging designs, such as vacuum insulated panels (VIPs), reusable insulated shipping containers, and advanced insulation foams, are enhancing thermal performance and improving product lifecycle efficiency. Stricter regulatory requirements related to cold-chain stability and sustainability goals are influencing packaging design approaches and shaping supplier selection throughout the value chain.

Key Industry Highlights:

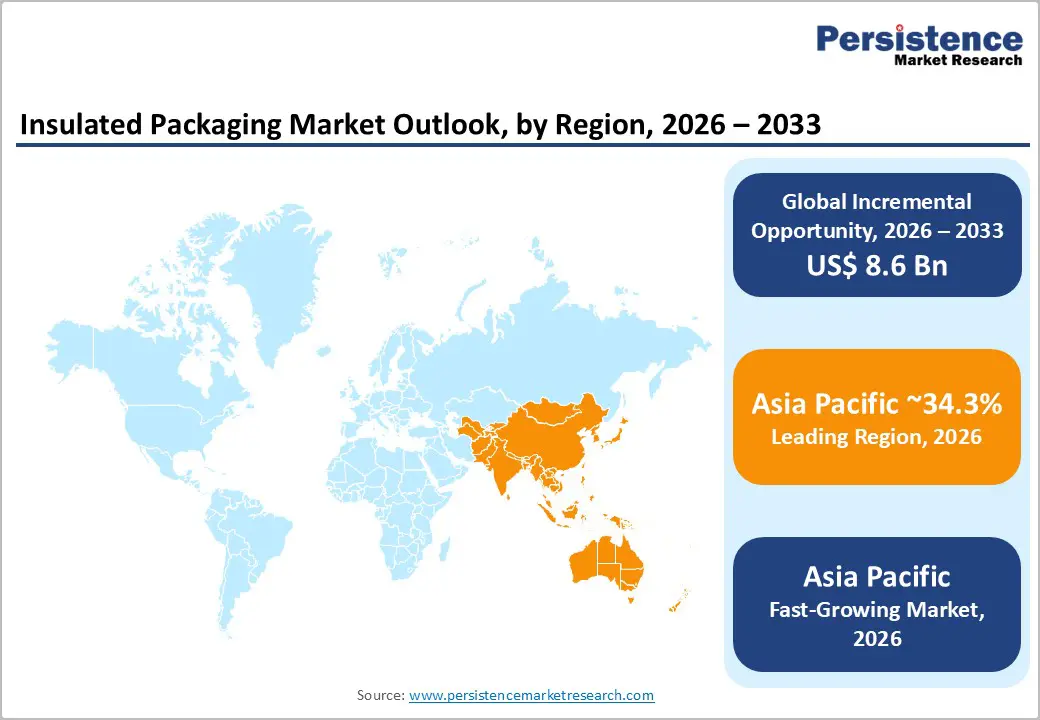

- Leading Region: Asia Pacific holds the leading position in the market with approximately 34.3% market share, supported by strong manufacturing capacity, rapid e-commerce expansion, and increasing pharmaceutical production across China, Japan, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also the fastest-growing regional market, driven by accelerating cold-chain infrastructure investments, rising online grocery demand, and expanding pharmaceutical logistics networks across emerging economies.

- Investment Plans: Major packaging companies and logistics providers are investing in reusable insulated shipping systems, digital temperature monitoring technologies, and regional refurbishment centers, particularly in North America and Asia Pacific, to improve cold-chain reliability and support circular packaging initiatives.

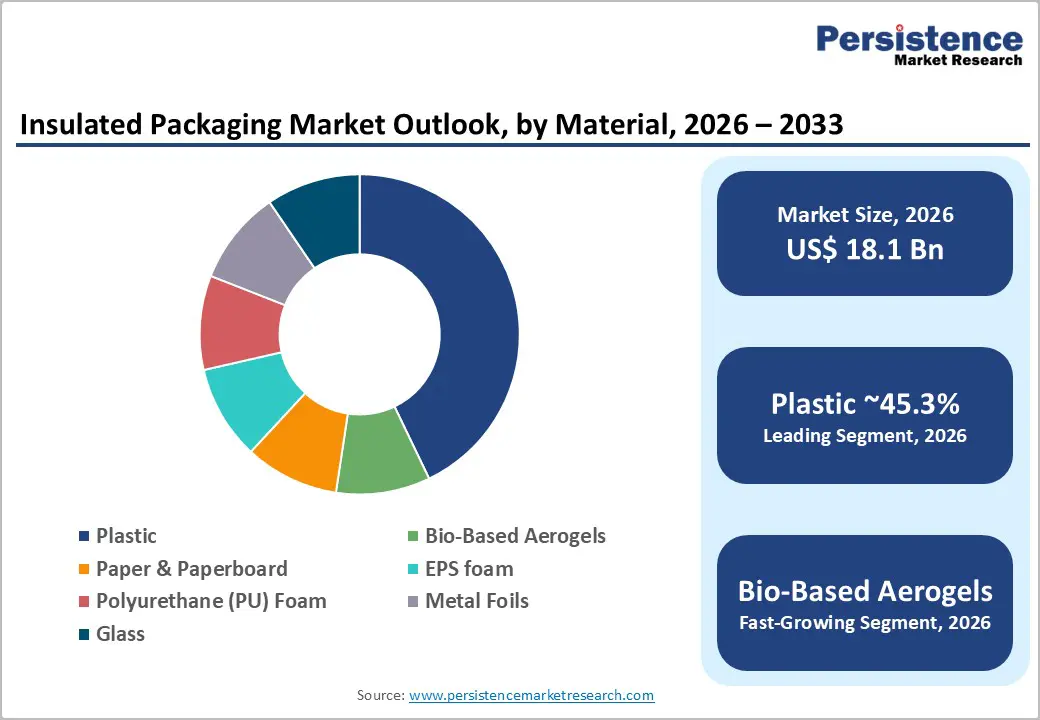

- Dominant Material: Plastic materials are anticipated to dominate the material segment with approximately 45.3% market share, as polyethylene, EPS foam, and polyurethane provide lightweight insulation, cost efficiency, and large-scale manufacturing availability for food and pharmaceutical logistics.

- Leading Product Type: Boxes & containers are estimated to represent the leading product type with around 40.7% market share, due to their wide adoption in pharmaceutical transport, meal-kit delivery services, and e-commerce fulfillment operations that require reliable temperature-controlled shipping solutions.

| Key Insights | Details |

|---|---|

| Insulated Packaging Market Size (2026E) | US$18.1 Bn |

| Market Value Forecast (2033F) | US$26.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Temperature-Sensitive Pharmaceutical Logistics

The increasing global volume of biologics, specialty injectables, and advanced therapies has significantly expanded the need for temperature-controlled transport solutions. Pharmaceutical products often require strict temperature ranges, such as frozen, refrigerated, or controlled room temperature, throughout the distribution process. Insulated packaging systems provide the passive thermal protection required to maintain product stability during shipping and storage. Regulatory guidelines governing drug stability and transportation require validated packaging systems that can maintain defined thermal conditions for extended durations. As a result, pharmaceutical manufacturers are investing more heavily in high-performance insulated packaging solutions. This trend is strengthening demand for reusable thermal shippers, temperature monitoring devices, and advanced insulation materials that can ensure consistent cold-chain performance.

Growth of E-Commerce Perishable and Direct-to-Consumer Food Delivery

Online grocery retail, meal-kit subscriptions, and direct-to-consumer food delivery models are rapidly expanding worldwide. These distribution channels require reliable packaging solutions capable of protecting temperature-sensitive products during transit from fulfillment centers to end consumers. Insulated packaging is essential for preventing spoilage, maintaining freshness, and reducing product returns associated with temperature fluctuations. As e-commerce penetration grows, the number of small parcel shipments containing perishable goods is increasing significantly. Logistics providers are therefore adopting insulated boxes, thermal liners, and gel-pack systems to support last-mile delivery. The growing diversity of product categories shipped through e-commerce platforms further increases packaging requirements, strengthening long-term demand for insulated packaging solutions.

Material Innovation and Sustainability Initiatives

Advances in insulation materials and packaging design are transforming the insulated packaging market. Manufacturers are developing bio-based aerogels, recyclable paper-based insulation systems, and multi-use polymer materials that offer improved thermal efficiency while reducing environmental impact. Increasing regulatory pressure and corporate sustainability commitments are encouraging companies to replace traditional expanded polystyrene (EPS) packaging with recyclable or reusable alternatives. At the same time, innovations in phase-change materials and vacuum-insulated panels enable higher thermal resistance with reduced packaging weight. These technological improvements enhance product performance and reduce transportation energy consumption, making advanced insulated packaging systems more attractive to pharmaceutical companies and environmentally conscious retailers.

Barrier Analysis - Price Volatility of Raw Materials

The insulated packaging industry depends heavily on polymer-based materials such as expanded polystyrene, polyurethane foams, and specialty thermal materials. Prices for these inputs are closely linked to petrochemical feedstocks and global energy markets. Sudden increases in raw-material costs can significantly raise packaging production expenses and compress profit margins for manufacturers. In cost-sensitive sectors such as food retail, buyers may shift toward lower-cost packaging alternatives when material prices rise. This volatility creates uncertainty for suppliers and can slow the adoption of premium insulated packaging technologies.

Regulatory Qualification and Testing Requirements

Packaging systems used in pharmaceutical supply chains must undergo extensive validation and performance testing before commercial adoption. Qualification processes often involve thermal mapping, environmental stress testing, and documentation demonstrating compliance with regulatory transport guidelines. These requirements increase product development costs and extend commercialization timelines. Smaller packaging suppliers may struggle to meet these regulatory standards, limiting their participation in high-value pharmaceutical logistics markets and increasing market concentration among established vendors with validated product portfolios.

Opportunity Analysis - Reusable and Circular Insulated Packaging Systems

Sustainability targets and waste-reduction policies are accelerating the development of reusable insulated packaging solutions. Pharmaceutical companies and large retail distributors are increasingly exploring returnable shipper systems designed for multiple use cycles. Reusable packaging reduces long-term material consumption and lowers total lifecycle costs for high-volume shipping operations. Manufacturers are also developing service models that include refurbishment, reverse logistics management, and tracking systems. These solutions create new revenue opportunities through packaging rental programs and long-term service contracts.

Digital Monitoring and Validation Technologies

The integration of temperature monitoring sensors and digital tracking technologies with insulated packaging systems represents a significant innovation opportunity. Modern cold-chain logistics increasingly rely on connected devices that provide real-time visibility into shipment conditions. IoT-enabled packaging solutions allow companies to track temperature fluctuations, detect shipment delays, and ensure regulatory compliance. Packaging suppliers that combine insulated containers with digital monitoring platforms can offer higher-value service packages and improve operational transparency for pharmaceutical manufacturers and food distributors.

Category-wise Analysis

Material Insights

Plastic materials are anticipated to hold approximately 45.3% of the market share in 2026, making them the dominant material category. Polyethylene, expanded polystyrene (EPS), and polyurethane foams are widely used because they provide reliable thermal insulation while maintaining relatively low manufacturing costs and lightweight structures. These materials are commonly incorporated into insulated liners, molded containers, and temperature-controlled shipping boxes used in food delivery services and pharmaceutical logistics. EPS foam containers, for example, are widely used for transporting seafood, frozen foods, and meal kits, while polyurethane foam panels are frequently used in pharmaceutical shipper systems designed to maintain controlled temperature conditions during transit. Their versatility, durability, and large-scale manufacturing capacity allow plastic-based insulation solutions to remain the preferred choice for high-volume packaging operations across e-commerce and cold-chain logistics networks.

Bio-based aerogels represent the fastest-growing material segment. These advanced insulation materials offer extremely low thermal conductivity while maintaining minimal weight, enabling packaging manufacturers to create thinner yet more thermally efficient insulation layers. Bio-based aerogels derived from renewable sources such as cellulose or silica composites are gaining increasing attention as companies seek environmentally responsible alternatives to petroleum-based foams. Several pharmaceutical packaging solutions have begun integrating aerogel insulation to reduce packaging weight while maintaining strict temperature stability for biologics and vaccines. Similarly, premium meal delivery companies and specialty food distributors are experimenting with aerogel-based liners to improve shipping performance for temperature-sensitive products while meeting sustainability commitments related to recyclable and bio-based materials.

Product Type Insights

Boxes and containers are anticipated to account for approximately 40.7% of the market share in 2026, making them the leading product category. These rigid structures are widely used for transporting temperature-sensitive products across multiple industries, including food distribution, pharmaceutical logistics, and e-commerce fulfillment. Insulated shipping boxes allow the integration of phase-change materials, gel packs, and temperature sensors that help maintain stable internal temperatures during transit. For instance, meal-kit providers commonly rely on insulated corrugated boxes with thermal liners to ship refrigerated ingredients directly to consumers, while pharmaceutical companies use insulated containers to transport vaccines and biologic medicines across regional distribution networks. Their standardized sizes and compatibility with automated warehouse systems make insulated boxes particularly well-suited for high-volume fulfillment operations.

Pallet shippers are the fastest-growing product segment. These large insulated transport systems are designed to protect bulk shipments during long-distance transportation, especially within global pharmaceutical supply chains. Pharmaceutical manufacturers frequently utilize pallet shippers to distribute temperature-sensitive products such as vaccines, insulin, and specialty biologic drugs between production facilities and international distribution centers. Modern pallet shipping systems incorporate advanced insulation technologies, including vacuum-insulated panels and multilayer thermal liners, which allow shipments to maintain stable temperature ranges for extended periods without active refrigeration. As pharmaceutical supply chains become more globalized and biologic drug distribution continues to expand, pallet-level insulated packaging solutions are expected to experience increasing adoption across long-haul logistics operations.

Regional Insights

North America Insulated Packaging Market Trends - Reusable Cold-Chain Shippers and Pharma-Ecommerce Distribution Growth

North America remains one of the most significant markets for insulated packaging due to its advanced pharmaceutical manufacturing industry, well-developed cold-chain logistics infrastructure, and strong e-commerce ecosystem. The U.S. leads the regional market, supported by extensive clinical trial activity and large-scale pharmaceutical production. Several packaging manufacturers have strengthened their presence in the region through technology innovation and production expansion. For instance, Sonoco ThermoSafe introduced reusable temperature-controlled shipper systems designed for pharmaceutical logistics, enabling multiple shipping cycles while maintaining strict thermal protection. Such innovations reflect the region’s emphasis on reusable cold-chain packaging and lifecycle cost reduction.

The U.S. market benefits from high adoption of temperature-controlled shipping technologies across healthcare and food distribution sectors. Pharmaceutical companies rely heavily on validated insulated shipping systems to protect high-value biologic products such as vaccines, specialty injectables, and cell-based therapies. Packaging providers like Pelican BioThermal have expanded the use of reusable temperature-controlled containers used for global pharmaceutical transport, helping manufacturers maintain strict temperature conditions during long-distance distribution.

E-commerce grocery services and meal-kit providers such as HelloFresh and Blue Apron also rely extensively on insulated boxes and thermal liners to ship fresh ingredients directly to consumers. Canada represents a smaller but steadily growing market driven by pharmaceutical distribution and food delivery expansion, while Mexico is emerging as a manufacturing hub where packaging converters produce insulated containers and liners for North American supply chains.

Investment activity across North America increasingly focuses on reusable shipping systems, digital monitoring technologies, and regional refurbishment centers designed to support circular packaging programs. Companies are integrating insulated containers with real-time temperature tracking solutions that allow pharmaceutical manufacturers and logistics providers to monitor shipment conditions throughout transit. These technological advancements improve product security, strengthen regulatory compliance, and increase transparency across the pharmaceutical supply chain.

Europe Insulated Packaging Market Trends - Sustainable Fiber-Based Insulation and Circular Packaging Adoption

Europe represents a mature market characterized by strong environmental regulations and well-developed logistics networks. Countries such as Germany, the U.K., France, and Spain play important roles in regional market development. Germany hosts a large manufacturing base for advanced packaging materials and insulation technologies, while the U.K. serves as a major hub for pharmaceutical logistics and clinical trial distribution. European packaging companies such as Mondi and Smurfit Kappa have introduced fiber-based insulated packaging solutions designed to replace expanded polystyrene containers, reflecting the region’s shift toward sustainable materials and recyclable packaging formats.

European regulatory policies encourage recycling, material recovery, and the reduction of single-use plastics. These regulations are accelerating the transition toward recyclable fiber-based insulation materials and reusable thermal packaging systems. For example, DS Smith has developed recyclable insulated packaging solutions using corrugated materials combined with thermal liners, enabling food retailers to meet sustainability goals while maintaining temperature protection for perishable goods. Many retailers and food delivery companies across the U.K., France, and Germany are adopting these recyclable insulated boxes for grocery delivery operations.

The rapid expansion of online grocery retail and meal delivery services across major European cities has also increased demand for insulated packaging. Logistics providers are investing in last-mile cold-chain infrastructure to accommodate rising shipment volumes. At the same time, pharmaceutical manufacturers are strengthening cross-border cold-chain networks to distribute temperature-sensitive medicines throughout the European Union. Investments in recycling systems, sustainable materials, and reusable shipping programs continue to shape packaging innovation and supply chain strategies across the region.

Asia Pacific Insulated Packaging Market Trends - Rapid E-Commerce Expansion and Large-Scale Cold-Chain Manufacturing

Asia Pacific is projected to lead the market with approximately 34.3% market share in 2026 and is also the fastest-growing regional market. Rapid industrialization, expanding e-commerce platforms, and large-scale pharmaceutical manufacturing contribute to strong demand for temperature-controlled packaging solutions. The region has become a key manufacturing hub for insulated packaging materials and shipping systems, supplying both domestic markets and international distribution networks.

China represents the largest market in the region, supported by extensive manufacturing capacity and the rapid expansion of online grocery and food delivery services. E-commerce platforms such as JD.com and Alibaba’s Freshippo grocery network use insulated packaging and cold-chain logistics systems to deliver fresh foods and temperature-sensitive products across major Chinese cities. To support this growth, logistics companies are investing in advanced cold-chain packaging technologies and regional distribution centers equipped with temperature-controlled storage facilities. Japan maintains a highly developed pharmaceutical logistics sector with strict quality standards for temperature-controlled shipments. Companies such as Softbox Systems and other temperature-controlled packaging providers have collaborated with pharmaceutical manufacturers to develop advanced insulated shipping containers capable of maintaining precise thermal conditions for biologic medicines. These solutions support the distribution of high-value pharmaceutical products across domestic and international supply chains.

India and Southeast Asian countries are emerging as important growth markets due to expanding pharmaceutical production and increasing adoption of e-commerce platforms. Pharmaceutical companies in India, including major vaccine manufacturers, rely on insulated packaging systems to distribute temperature-sensitive vaccines and biologic products domestically and internationally. Governments and logistics providers across the region are investing in cold-chain infrastructure, including refrigerated transport fleets and insulated packaging manufacturing facilities. As a result, Asia Pacific’s combination of large consumer markets, strong pharmaceutical manufacturing capacity, and cost-efficient production capabilities positions the region as a central hub for insulated packaging innovation and supply chain development.

Competitive Landscape

The global insulated packaging market demonstrates a moderately concentrated competitive structure. Large multinational packaging companies account for a significant portion of global revenue, while numerous regional manufacturers serve specialized markets and local supply chains. Leading players differentiate themselves through advanced material technologies, validated packaging systems, and integrated cold-chain services. Companies with strong research capabilities and global logistics partnerships are better positioned to serve pharmaceutical and high-value food distribution markets.

Leading insulated packaging companies focus on innovation, sustainability, and geographic expansion to strengthen market positions. Strategic priorities include the development of recyclable insulation materials, reusable shipping systems, and integrated digital monitoring technologies that enhance supply chain transparency and operational efficiency.

Key Industry Developments:

- In October 2025, Peli BioThermal launched the Vero One™ dry ice shipper, a single-use, curbside-recyclable insulated packaging system developed to simplify deep-frozen pharmaceutical shipments. The cold-chain packaging solutions under new ownership.

Companies Covered in Insulated Packaging Market

- Sonoco ThermoSafe

- Sealed Air Corporation

- Cold Chain Technologies

- Pelican BioThermal

- Intelsius

- Cryopak

- Tempack Packaging Solutions

- Softbox Systems

- Insulated Products Corporation (IPC)

- American Aerogel Corporation

- Snyder Industries

- ThermoSafe Brands

- Marko Foam Products

- Melform S.r.l.

- Inmark Packaging

- Saften Pak

Frequently Asked Questions

The global insulated packaging market is estimated to reach US$18.1 billion in 2026.

The insulated packaging market is projected to reach US$26.7 billion by 2033.

Key trends include growing adoption of reusable insulated shipping systems, development of sustainable insulation materials such as bio-based aerogels, and integration of digital temperature monitoring technologies to improve cold-chain visibility and regulatory compliance.

The plastic material segment is expected to lead the market with approximately 45.3% share, as polyethylene, expanded polystyrene, and polyurethane provide lightweight insulation, cost efficiency, and scalable manufacturing capacity.

The insulated packaging market is expected to grow at a CAGR of 5.7% between 2026 and 2033.

Major companies include Sonoco ThermoSafe, Sealed Air, Amcor, Cold Chain Technologies, and Pelican BioThermal.