- Automation & Robotics

- Industrial Manipulators Market

Industrial Manipulators Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Manipulators Market by Product Type (Electric, Pneumatic, Hydraulic), Mobility (Fixed, Mobile), by Payload Capacity (Up to 50 Kg, 50 to 200 Kg, Above 200 Kg), Industry (Automotive, General Manufacturing, Aerospace & Defence, Electronics & Electrical, Transport & Logistics, Metal & Heavy Engineering, Others), and Regional Analysis, 2026 - 2033

Industrial Manipulators Market Size and Trend Analysis

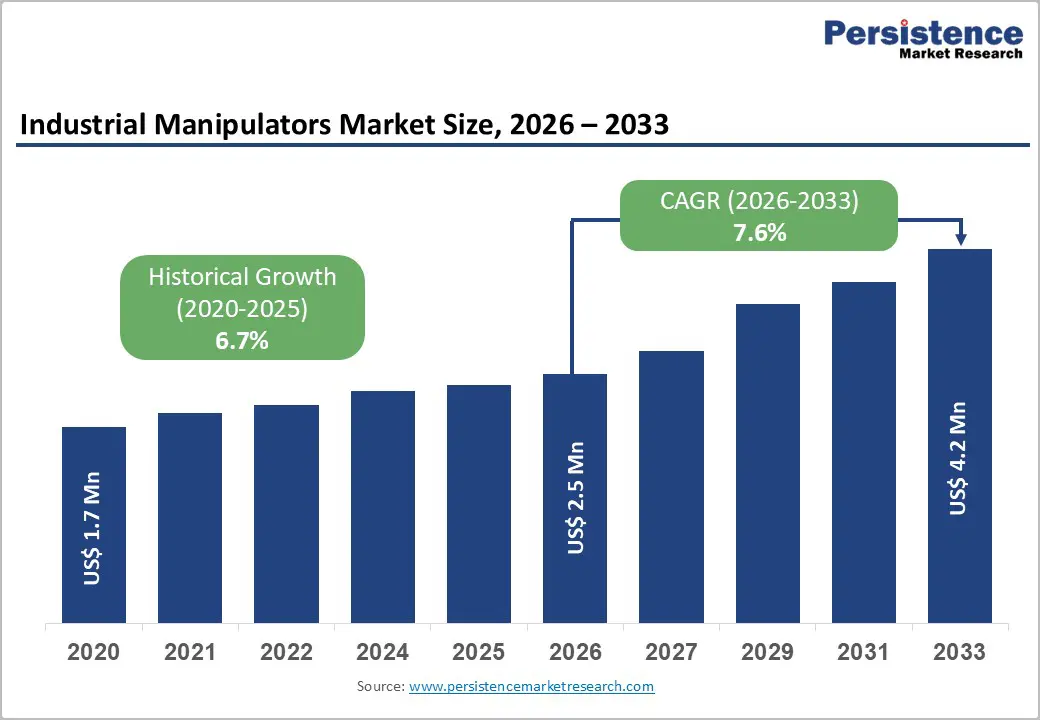

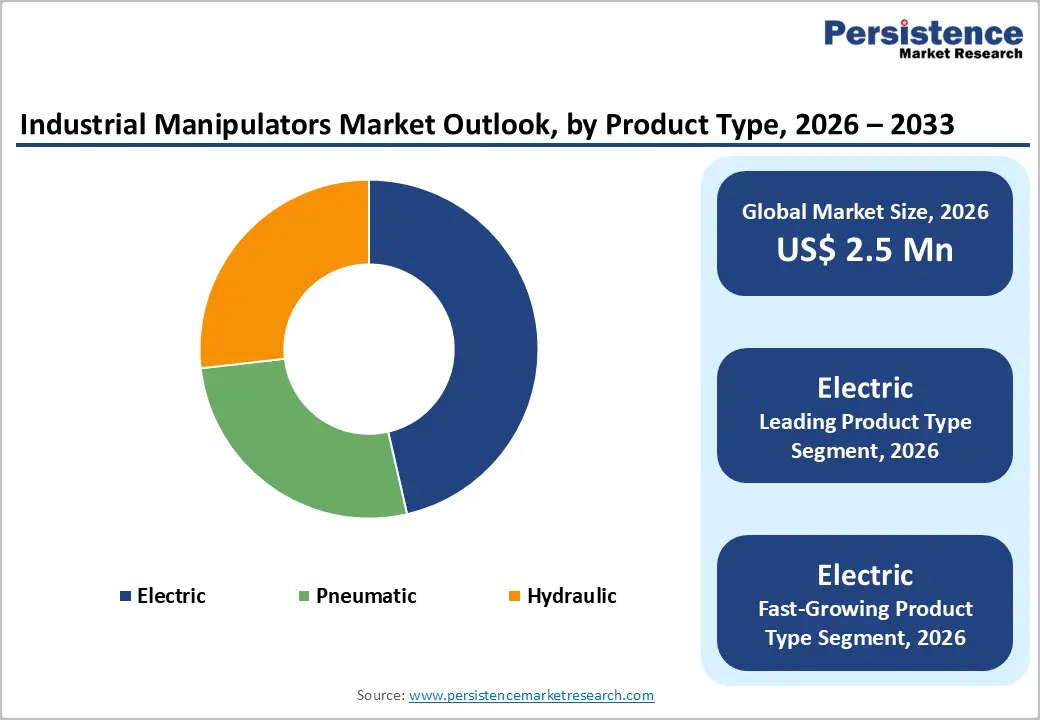

The global industrial manipulators market size is expected to be valued at US$ 2.5 billion in 2026 and projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

This growth is principally driven by accelerating automation across discrete manufacturing industries and mounting workplace ergonomics compliance mandates. Rising incidences of musculoskeletal disorders (MSDs), which the European Agency for Safety and Health at Work (EU-OSHA) identifies as the most common work-related health problem in Europe, affecting over 60% of workers, are compelling manufacturers to adopt assistive handling equipment. Simultaneously, automotive and aerospace OEM production expansions in Asia Pacific, along with Industry 4.0 integration programs in North America and Europe, are widening the addressable market for intelligent, electric industrial manipulators at an above-average growth pace through the forecast horizon.

Key Industry Highlights:

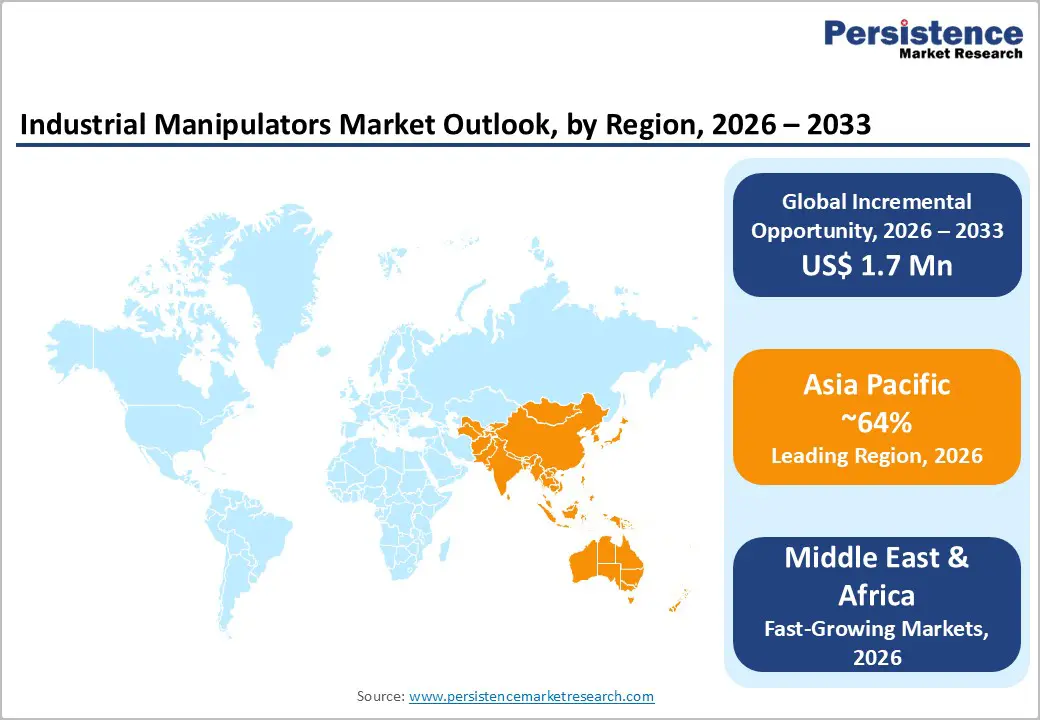

- Leading Region: Asia Pacific leads the global industrial manipulators market with 64% revenue share in 2025, driven by China's massive manufacturing modernization programs, Japan's precision engineering ecosystem, India's PLI-backed industrial expansion, and ASEAN automotive and electronics FDI growth.

- Fastest Growing Region: Middle East & Africa is the fastest growing regional market through 2033, underpinned by gigafactory and smart logistics investments across GCC nations, growing EV supply chains, and rapid industrial diversification initiatives such as Saudi Vision 2030 and UAE Net Zero 2050.

- Dominant Segment: The automotive sector leads all end-use segments with approximately 32% market share in 2025, driven by OEM and Tier-1 supplier ergonomics compliance requirements, EV assembly line buildouts, and zero-defect quality mandates across global vehicle production facilities.

- Fastest Growing Segment: Electric manipulators hold 45% market share in 2025 and represent the fastest-growing product type through 2033, fueled by Industry 4.0 smart factory adoption, EV battery module handling requirements, and the growing preference for IoT-connected, servo-controlled precision handling systems.

- Key Market Opportunity: The dual tailwinds of global EV gigafactory expansion, projected to create over 6,500 GWh of capacity by 2030, and e-commerce fulfillment center automation represent the most significant near-term revenue opportunity for industrial manipulator manufacturers through the forecast period.

| Key Insights | Details |

|---|---|

| Industrial Manipulators Market Size (2026E) | US$ 2.5 Billion |

| Market Value Forecast (2033F) | US$ 4.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.6% |

| Historical Market Growth (2020 - 2025) | 6.7% |

Market Dynamics

Drivers - Rise in Workplace Ergonomics Regulations and MSD Prevention Mandates

Regulatory pressure to eliminate ergonomic risk factors in industrial workplaces is a foundational demand driver for industrial manipulators globally. According to EU-OSHA, musculoskeletal disorders account for 45% of all working days lost across the European Union, costing economies an estimated EUR 240 billion annually. The EU Manual Handling Directive (90/269/EEC) and its amendments require employers to mechanize or assist all manual handling operations exceeding safe weight thresholds. Similarly, the U.S. Occupational Safety and Health Administration (OSHA) has intensified enforcement of ergonomic guidelines under General Industry standards. These legislative mandates directly compel automotive, general manufacturing, and metal fabrication facilities to deploy intelligent lifting and positioning manipulators as primary compliance solutions, making regulatory adherence a sustained structural growth engine for the market.

Industry 4.0 Integration and Smart Factory Transformation

The global roll-out of Industry 4.0 smart factory frameworks is profoundly reshaping the demand profile for industrial manipulators. Modern electric manipulators are increasingly equipped with IoT-enabled sensors, force-torque feedback systems, and collaborative robot (cobot) interfaces that enable real-time monitoring, predictive maintenance, and seamless human-robot collaboration (HRC). According to the International Federation of Robotics (IFR), global robot installations in manufacturing reached a record 553,052 units in 2022, and the integration of intelligent handling devices alongside robotic cells continues to accelerate. Germany's VDMA and Japan's Ministry of Economy, Trade and Industry (METI) have both actively funded smart factory pilot programs where intelligent manipulators serve as essential interfaces between human operators and automated lines. This ecosystem-level transformation is generating strong replacement demand for legacy pneumatic and hydraulic manipulators with connected, electric alternatives.

Restraints - High Initial Capital Investment and Total Cost of Ownership

The upfront procurement, installation, and system integration cost of industrial manipulators, particularly advanced electric models with programmable controls and IoT connectivity, remains a significant adoption barrier for small and medium-sized enterprises (SMEs). A fully integrated electric manipulator system with vacuum tooling and programmable controls can cost between US$ 15,000 and US$ 80,000 per unit, excluding installation and training. According to a 2023 survey by the European Factories of the Future Research Association (EFFRA), capital expenditure constraints are cited by over 55% of surveyed SME manufacturers as the primary barrier to automation adoption, limiting penetration in cost-sensitive markets particularly across Latin America, Southeast Asia, and parts of Eastern Europe.

Complexity of Integration with Diverse Manufacturing Environments

Industrial manipulators must interface with a wide variety of workpiece geometries, surface materials, production line layouts, and safety systems, making application-specific engineering a persistent challenge. Unlike standardized robotic arms, manipulators often require bespoke end-of-arm tooling (EOAT), customized structural mounting, and site-specific safety guarding compliant with ISO 11161 and EN ISO 10218 safety standards for integrated manufacturing systems. These integration complexities extend commissioning timelines and require specialized technical expertise, which is scarce in emerging markets. This creates friction in sales cycles and increases total project costs, dampening adoption velocity, particularly among first-time buyers in developing industrial economies.

Opportunity - Expansion of Electric Vehicle (EV) Battery and Component Manufacturing

The global transition to electric vehicles (EVs) is generating substantial new demand for industrial manipulators in battery module assembly, pack integration, and drivetrain component handling, all of which involve heavy, geometrically complex, and electrochemically sensitive components requiring precision-assisted positioning. According to the International Energy Agency (IEA), global EV sales surpassed 14 million units in 2023, and battery gigafactory investments globally are projected to create over 6,500 GWh of annual production capacity by 2030. Announced gigafactories by Northvolt, LG Energy Solution, CATL, and others across Europe, North America, and Asia incorporate extensive manipulator-assisted assembly lines. Given that battery modules can weigh between 30 kg and 600 kg per unit, manipulators with precision payload control are indispensable to EV production workflows, positioning this as one of the fastest-expanding application niches for the forecast period.

E-commerce Logistics and Warehouse Automation Demand Surge

The explosive growth of e-commerce and third-party logistics (3PL) is driving unprecedented demand for mobile and semi-fixed manipulators in distribution center operations, including palletizing, depalletizing, order picking, and goods-to-person workflows. According to UNCTAD, global e-commerce sales reached US$ 5.8 trillion in 2023, and continued double-digit growth trajectories are compelling logistics operators to automate ergonomically intensive picking and sorting operations at scale. Amazon, DHL, FedEx, and JD Logistics have all deployed manipulator-integrated workstations to reduce picker injury rates and improve throughput. The Transport & Logistics segment is therefore anticipated to be among the fastest-growing end-use verticals for industrial manipulators through 2033, especially as fulfillment centers in Middle East & Africa and Southeast Asia undergo rapid modernization.

Category-wise Analysis

Product Type Insights

Electric industrial manipulators are the dominant product type, commanding approximately 45% of overall market revenue in 2025. Their leadership reflects a broad structural transition across manufacturing industries away from compressed-air-dependent pneumatic systems toward cleaner, more controllable, and digitally integrated electric alternatives. Electric manipulators offer significant advantages: precise load positioning through servo-motor control, programmable multi-axis motion, quiet operation, lower energy consumption per cycle versus hydraulic systems, and compatibility with IoT and Industry 4.0 platforms. The International Federation of Robotics (IFR) has highlighted the convergence of cobots and intelligent handling devices as a key trend in smart assembly environments. Electric manipulators are further favored by clean-room requirements in electronics and pharmaceutical manufacturing, where pneumatic oil mist contamination is unacceptable. They are also the fastest-growing product type, with adoption fueled by EV battery assembly lines and intelligent warehouse workstations demanding force-feedback positioning accuracy unavailable in pneumatic designs.

Mobility Insights

Fixed industrial manipulators constitute the leading mobility segment, accounting for approximately 67% of global market share in 2025. Fixed-mounted manipulators are widely preferred across high-volume, repetitive manufacturing environments, particularly in automotive body-in-white assembly, press shops, and engine component manufacturing, where consistent, high-throughput operation at defined workstations is paramount. Their structural rigidity enables handling of heavier payloads exceeding 200 kg with maintained repeatability, a requirement difficult to satisfy with mobile platforms. ISO 9283 performance characterization standards further support fixed manipulators' advantage in certified production lines requiring documented positioning accuracy. However, mobile manipulators represent the fastest-growing mobility sub-segment, driven by the adoption of autonomous mobile robots (AMRs) in warehouse, logistics, and flexible manufacturing environments where fixed infrastructure installation is impractical or cost-prohibitive.

Payload Capacity Insights

The 50 to 200 Kg payload capacity segment is the leading category, representing approximately 44% of global market share in 2025. This range addresses the broadest cross-section of industrial handling needs, from automotive door and hood assembly to aerospace structural component positioning and metal fabrication tasks, making it the most commercially versatile tier. Components in this weight range are ubiquitous across Tier-1 automotive suppliers, general engineering workshops, and HVAC manufacturing environments. They are simultaneously too heavy for unaided manual handling under EU Directive 90/269/EEC safe limits (typically 25 kg for men, 15 kg for women) yet not heavy enough to mandate full robotic automation. This ergonomic compliance sweet spot generates sustained demand. The Above 200 Kg segment is the fastest-growing payload tier, propelled by heavy engineering, shipbuilding, and offshore energy sector expansion in Asia Pacific, the Middle East & Africa.

Industry Insights

Automotive is the dominant end-use segment for industrial manipulators, accounting for approximately 32% of global market revenue in 2025. The sector's relentless drive to improve assembly line ergonomics, reduce cycle times, and achieve zero-defect quality targets makes it structurally dependent on advanced manipulator technology. Automotive OEMs and their Tier-1 and Tier-2 suppliers worldwide deploy manipulators extensively for engine sub-assembly, door panel installation, windshield fitting, and seat handling operations. According to the International Organization of Motor Vehicle Manufacturers (OICA), global automobile production reached approximately 93.5 million vehicles in 2023, sustaining high baseline demand. The rapid proliferation of EV and hybrid vehicle platforms is further adding new manipulator-intensive assembly workflows around battery modules, power electronics, and e-axle components. Transport & Logistics is the fastest-growing end-use segment, propelled by e-commerce fulfillment center investments globally.

Regional Insights

North America Industrial Manipulators Market Trends and Insights

The United States anchors the North American industrial manipulators market, supported by a robust manufacturing base in automotive, aerospace & defense, and general manufacturing sectors. The OSHA regulatory framework, combined with voluntary ergonomics programs under the National Institute for Occupational Safety and Health (NIOSH), continues to incentivize manipulator adoption across assembly and material handling operations. The U.S. CHIPS and Science Act (2022), with its US$ 52 billion commitments to semiconductor manufacturing, is generating new demand in electronics assembly environments requiring cleanroom-compatible electric manipulators.

Innovation is a key regional differentiator, with companies such as Gorbel Inc. and Positech Corporation developing AI-assisted, load-sensing manipulator systems tailored for aerospace MRO and defense manufacturing environments. Canada's expanding EV battery supply chain, anchored by investments from Volkswagen, Stellantis-LG, and Northvolt in Ontario and Quebec, is emerging as a significant new growth vector, adding battery module handling and assembly manipulator demand to the region's manufacturing footprint.

Europe Industrial Manipulators Market Trends and Insights

Europe is the most regulation-advanced and ergonomics-driven market for industrial manipulators globally. Germany leads regional consumption, home to leading manufacturer Schmalz GmbH and Zasche Handling GmbH, as well as the world's most demanding automotive assembly requirements from BMW, Mercedes-Benz, Volkswagen, and Audi. The EU Strategic Framework on Health and Safety at Work 2021-2027 reinforces pan-European ergonomics compliance mandates that directly stimulate manipulator procurement. France's aerospace industry, anchored by Airbus and its Toulouse and Nantes

assembly facilities, is among the most intensive users of zero-gravity manipulators for fuselage panel and nacelle component positioning.

Italy's specialist industrial manipulator manufacturers, including Dalmec S.p.A., Manibo S.r.l., and Scaglia INDEVA (Indeva Group), are globally recognized for their intelligent balancer and servo-actuated product lines, which are exported across 70+ countries. Sweden's companies, Binar Handling AB, Movomech AB, and Pronomic AB, are recognized leaders in ergonomic handling innovation. Spain's automotive manufacturing hubs in Valencia, Barcelona, and Zaragoza are investing in manipulator-integrated assembly modernization, aligning with EU Green Deal productivity targets.

Asia Pacific Industrial Manipulators Market Trends and Insights

Asia Pacific is the dominant regional market for industrial manipulators with approximately 64% global revenue share in 2025, anchored by China, Japan, and South Korea. China's massive "Made in China 2025" industrial modernization initiative and its 14th Five-Year Plan infrastructure targets are generating unprecedented demand for automation equipment, including advanced industrial manipulators across automotive, electronics, and general manufacturing sectors. The International Federation of Robotics (IFR) reported that China alone accounted for 70% of all new industrial robot installations in Asia in 2022, with adjacent manipulator demand growing in parallel.

Japan is a global leader in manipulator technology development, with precision engineering firms integrating manipulators into semiconductor, automotive, and medical device manufacturing

lines. India's manufacturing expansion, accelerated by the Production Linked Incentive (PLI) scheme across 14 priority sectors, is emerging as a high-growth demand source, particularly in automotive, electronics, and pharmaceuticals. ASEAN nations, including Thailand, Vietnam, and Indonesia, are attracting automotive and electronics foreign direct investment that invariably includes manipulator-integrated assembly and logistics workflows, reinforcing Asia Pacific's commanding market leadership through the forecast period.

Competitive Landscape

The global industrial manipulators market is moderately fragmented, with a mix of specialized automation equipment manufacturers and regional engineering solution providers. European manufacturers maintain strong technological leadership due to their expertise in ergonomic engineering, precision motion control, and advanced load-handling technologies, while North American and Asian suppliers are expanding their presence through competitive pricing and localized manufacturing capabilities.

Market participants primarily compete through product innovation, customization, and system integration capabilities. Companies are increasingly focusing on intelligent manipulators featuring servo-balancing technology, load-sensing systems, and digital connectivity to support smart factory environments. Strategic priorities include expanding global distribution networks, strengthening after-sales service capabilities, and developing application-specific solutions for sectors such as automotive manufacturing, EV battery assembly, and e-commerce logistics.

Key Developments

- February 2026: Artimus Robotics launched a new generation of contracting HASEL artificial muscle actuators delivering over twice the mechanical output of previous versions and is seeking partners to evaluate the technology for integration into dexterous robotic manipulators across humanoid and industrial automation applications.

- December 2025: Ghost Robotics unveiled a lightweight, modular manipulator arm for its Vision 60 quadruped unmanned ground vehicle, enabling tasks such as opening doors, retrieving objects, and handling equipment across defense, inspection, and hazardous-environment missions.

Companies Covered in Industrial Manipulators Market

- Dalmec S.p.A.

- Manibo S.r.l.

- Scaglia INDEVA (Indeva Group)

- Gorbel Inc.

- Positech Corporation

- Binar Handling AB

- ATIS Srl

- VINCA Equipos Industriales

- Movomech AB

- Schmalz GmbH

- Zasche Handling GmbH

- Ergoflex Inc.

- ASE Systems Inc.

- Pronomic AB

- GCI Engineered Solutions

- Tawi AB (part of Piab Group)

- Vaculex AB

- Famatec S.r.l.

Frequently Asked Questions

The global Industrial Manipulators market is estimated to be valued at US$ 2.5 billion in 2026 and is projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 7.6%.

Key demand drivers include stringent workplace ergonomics regulations, Industry 4.0 automation adoption, EV battery manufacturing expansion, and increasing automation in e-commerce logistics operations.

Asia Pacific dominates the market, accounting for around 64% of global revenue share in 2025, supported by strong manufacturing expansion in China, Japan, India, and Southeast Asia.

Major opportunities include integration in EV battery gigafactories and automation of e-commerce fulfillment centers to improve productivity and reduce workplace injuries.

Leading companies include Dalmec S.p.A., Scaglia INDEVA, Schmalz GmbH, Zasche Handling GmbH, Binar Handling AB, Movomech AB, Pronomic AB, Gorbel Inc., Positech Corporation, and GCI Engineered Solutions.